- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

eVTOL Aircraft Market Soars to USD 53.6 Bn by 2034 | 15.2% CAGR

Global Electric Vertical Take-off and Landing Aircraft Market Size, Share, Analysis Report, Application (Air Taxi, Cargo Transport, EMS, Military), Technology (Multirotor, Vectored Thrust, Lift + Cruise), Propulsion Type (Battery Electric, Hybrid Electric, Hydrogen Electric), MTOW (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Historical Data and Forecast 2025-2034

Report Overview:

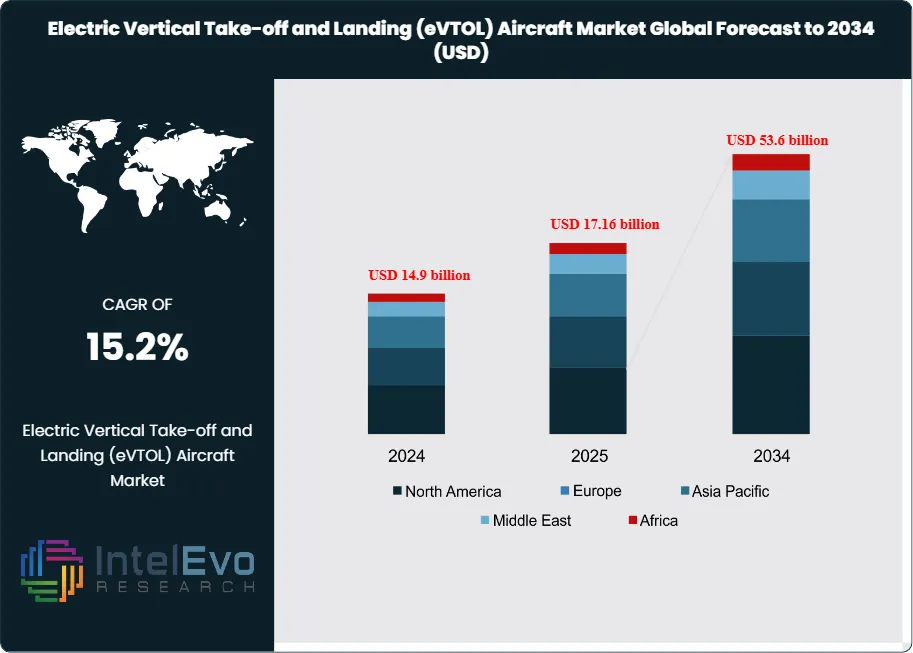

The Global Electric Vertical Take-off and Landing (eVTOL) Aircraft Market size is projected to reach approximately USD 53.6 billion by 2034, up from USD 14.9 billion in 2024, growing at a CAGR of 15.2% during the forecast period from 2025 to 2034. The eVTOL market is gaining momentum as advancements in battery technology, autonomous flight systems, and sustainable air mobility initiatives reshape the future of urban transportation. Governments and aerospace leaders are heavily investing in air taxi networks and regional mobility corridors. With growing emphasis on zero-emission transport and smart city integration, eVTOL aircraft are expected to redefine the global aviation landscape by the next decade.

Get More Information about this report -

Request Free Sample ReportThe Electric Vertical Take-off and Landing (eVTOL) aircraft market represents a revolutionary segment within the aviation sector, focusing on urban air mobility solutions. eVTOLs are designed for vertical take-off and landing, utilizing electric propulsion systems that make them suitable for congested urban environments. The current market is marked by significant technological advancements, increased investment in sustainable transport solutions, and a surge in interest from both public and private sectors. As of 2024, the market is valued at approximately USD 14.9 billion, driven by innovations in eVTOL designs, including hybrid-electric and fully electric models. This transformation is aimed at addressing the challenges of urban congestion and environmental concerns.

The growth dynamics of the eVTOL market are propelled by several key factors. One of the primary drivers is the rising urban congestion, which amplifies the demand for alternative transportation solutions capable of bypassing road traffic. Furthermore, advancements in battery technology are enhancing eVTOL efficiency and operational range, making them more commercially viable. Additionally, supportive government policies and investments in urban air mobility infrastructure are expediting the integration of eVTOLs into existing transport systems. Industry leaders like Joby Aviation, Archer, and Lilium are at the forefront of this innovation, developing prototypes that promise to reshape urban commuting and air travel.

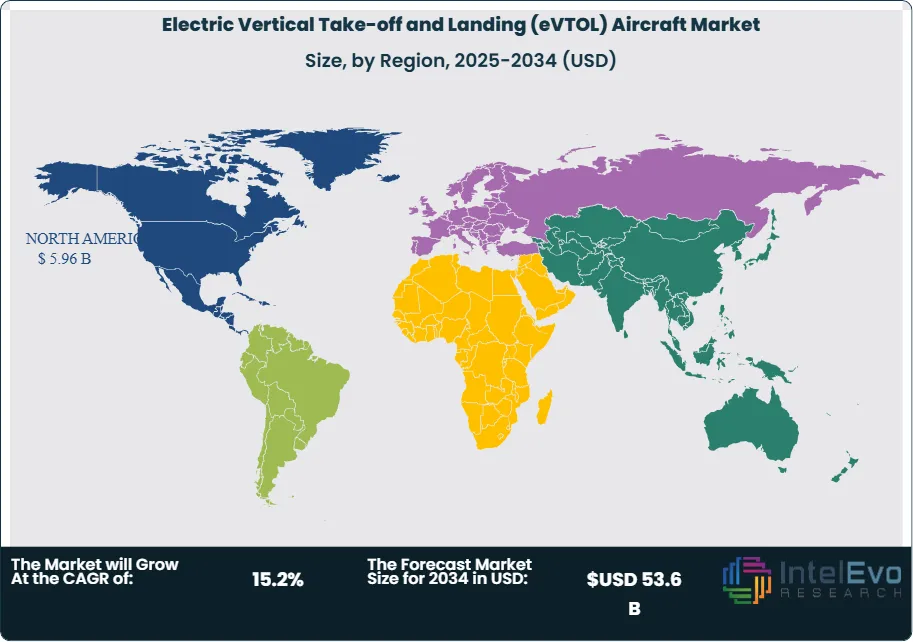

North America is the leading market for eVTOLs, thanks to its advanced aerospace industry and substantial investment in research and development. The United States, in particular, hosts numerous eVTOL startups and established aerospace manufacturers. However, the Asia-Pacific region is anticipated to experience the fastest growth rate, driven by rapid urbanization, an expanding middle class, and increasing government initiatives focused on sustainable transportation solutions. Countries such as China and India are significantly investing in urban air mobility to mitigate growing traffic issues and improve transportation efficiency.

The COVID-19 pandemic had a mixed impact on the eVTOL market. Initially, the crisis disrupted supply chains and delayed development timelines due to restrictions on travel and gatherings. However, it also underscored the necessity for innovative transport solutions that enhance public health safety and alleviate congestion. As cities seek to recover and adapt to post-pandemic realities, there is renewed interest in eVTOLs as clean and efficient alternatives to traditional transportation. This shift in public perception could further accelerate market growth in the coming years.

, Technology (Multirotor, Vectored Thrust, Lift + Cruise), Propulsion Type (Battery Electric, Hybrid Electric, Hydrogen Electric), MTOW (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Historical Data and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The Electric Vertical Take-off and Landing (eVTOL) aircraft market is expected to reach USD 53.6 billion by 2034, growing at a robust CAGR of 15.2%, indicating strong market expansion.

- Technology Segment Analysis: The multirotor technology segment is anticipated to dominate the eVTOL market due to its operational versatility and efficiency in urban environments, catering to both passenger and cargo applications.

- Propulsion Type Analysis: The battery electric propulsion type is likely to hold the largest market share, driven by advancements in battery technology and increasing focus on sustainable aviation solutions.

- Driver: Urban congestion is a primary driver for eVTOL market growth, as cities seek efficient alternatives to traditional ground transport to improve mobility and reduce traffic-related issues

- Restraint: Regulatory challenges and certification processes for eVTOL aircraft remain significant restraints, as achieving compliance with aviation safety standards can be lengthy and complex.

- Opportunity: The increasing investment in urban air mobility infrastructure presents significant opportunities for market players, as governments and private sectors collaborate to enhance eVTOL adoption and operational feasibility.

- Trend: The trend towards sustainable and efficient transportation solutions is gaining momentum, with eVTOLs positioned as key players in the future of urban mobility.

- Regional Analysis: North America is currently the leading region for eVTOL development, but the Asia-Pacific region is projected to experience the fastest growth due to rapid urbanization and supportive government initiatives.

Technology:

The technology segment of the eVTOL market comprises three main types: multirotor, vectored thrust, and lift + cruise designs. Multirotor aircraft utilize multiple rotors to achieve vertical lift and are popular for their simplicity and versatility, making them ideal for urban environments. Vectored thrust designs use tilt-rotor technology to transition between vertical and horizontal flight, offering increased speed and efficiency. Lift + cruise eVTOLs combine fixed-wing designs with separate rotors, providing optimal lift during take-off and efficient cruising capabilities. As cities increasingly seek sustainable transportation solutions, the demand for advanced eVTOL technologies is anticipated to rise, spurring innovation and competition among manufacturers.

Propulsion Type:

The propulsion type segment plays a crucial role in the eVTOL market, categorized into battery electric, hybrid electric, and hydrogen electric systems. Battery electric propulsion is currently the most prevalent, driven by advancements in energy density and charging technology that enhance operational range and reduce emissions. Hybrid electric systems combine traditional fuel engines with electric propulsion, offering extended range and flexibility, making them suitable for longer urban routes. Hydrogen electric systems, though still in the early stages of development, present a promising alternative for zero-emission flight, appealing to environmental concerns. As battery technology continues to evolve, the market will likely see a shift towards cleaner and more efficient propulsion methods.

Maximum Take-off Weight (MTOW):

The maximum take-off weight (MTOW) segment categorizes eVTOLs into three groups: below 2,000 lbs, 2,000 to 5,000 lbs, and above 5,000 lbs. eVTOLs weighing less than 2,000 lbs are generally designed for short-range air taxi services and are more agile in urban environments. The 2,000 to 5,000 lbs category typically includes larger passenger aircraft capable of carrying multiple individuals or cargo over longer distances, making them ideal for regional transport. Aircraft exceeding 5,000 lbs usually target specialized markets, such as emergency services or freight transport. As urban air mobility grows, understanding the MTOW capabilities will be essential for aligning aircraft designs with market demands.

Application:

The application segment of the eVTOL market includes air taxi services, cargo transport, emergency medical services (EMS), and military applications. Air taxis represent the most prominent application, targeting urban commuters seeking efficient and time-saving transport options. Cargo transport is also gaining traction, particularly for last-mile deliveries, as eVTOLs can bypass congested roadways. EMS applications leverage eVTOLs for rapid patient transport in emergency situations, significantly improving response times. Additionally, military applications utilize eVTOL technology for logistics, surveillance, and search and rescue missions. Each application is driving innovations in eVTOL design and technology, catering to specific operational needs and enhancing overall market growth.

Region Analysis:

North America Leads With 40% Market Share In eVTOL Aircraft Market: North America is poised to dominate the eVTOL aircraft market, accounting for approximately 40% of the total market share. This leadership position is primarily due to the region's robust aerospace and aviation industry, supported by substantial investments in research and development from both private and public sectors. Major players, including established aerospace firms and numerous startups, are actively engaged in advancing eVTOL technology. Furthermore, favorable regulatory frameworks, such as the Federal Aviation Administration's (FAA) support for urban air mobility initiatives, foster innovation and expedite certification processes. The high demand for air taxi services in congested urban areas, coupled with increasing investments in related infrastructure, is also contributing to North America's market dominance. This combination of factors makes the region a global hub for eVTOL development.

In contrast, the Asia-Pacific region is emerging as the fastest-growing market for eVTOL aircraft, projected to witness significant growth driven by rapid urbanization and rising demand for innovative transportation solutions. Countries like China, Japan, and Singapore are investing heavily in urban air mobility initiatives, creating favorable conditions for eVTOL adoption. Government support, particularly in regulatory advancements and infrastructure development, is pivotal in accelerating market growth. The increasing population density in major cities is compelling governments and private companies to seek alternatives to traditional ground transportation, enhancing the appeal of eVTOLs. Partnerships between local startups and global aerospace firms are fostering technological advancements and driving market penetration. As a result, the Asia-Pacific region presents immense growth potential, positioning itself as a key player in the evolving eVTOL landscape.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Lift Technology

- Multirotor

- Lift Plus Cruise

- Vectored Thrust

By Mode of Operation

- Piloted

- Autonomous

By Range

- <50 km

- 50–200 km

- >200 km

By Maximum Take-off Weight (MTOW)

- Below 2,000 lbs

- 2,000 to 5,000 lbs

- Above 5,000 lbs

By Application

- Air Taxis

- Cargo Transport

- Military and Defense

- Emergency Medical Services

- Private and Recreational

By Propulsion Type

- Fully Electric

- Hybrid Electric

- Hydrogen Fuel Cell

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 17.16 B |

| Forecast Revenue (2034) | USD 53.6 B |

| CAGR (2025-2034) | 15.2% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Lift Technology (Multirotor, Lift Plus Cruise, Vectored Thrust), By Mode of Operation (Piloted, Autonomous), By Range (<50 km, 50–200 km, >200 km), By Maximum Take-off Weight (MTOW) (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), By Application (Air Taxis, Cargo Transport, Military and Defense, Emergency Medical Services, Private and Recreational), By Propulsion Type (Fully Electric, Hybrid Electric, Hydrogen Fuel Cell) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Joby Aviation, Volocopter, Lilium, Archer Aviation, EHang, Bell Textron, Airbus, Hyundai, Karem Aircraft, Pipistrel, Aurora Flight Sciences (a Boeing subsidiary), Vertical Aerospace, Nexter Aerospace, Urban Aeronautics, Electra Aero, Beta Technologies, Zunum Aero, Pipistrel Aircraft, Skydrive, Wisk Aero |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Technology (Multirotor, Vectored Thrust, Lift + Cruise), Propulsion Type (Battery Electric, Hybrid Electric, Hydrogen Electric), MTOW (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Historical Data and Forecast 2025-2034")

, Technology (Multirotor, Vectored Thrust, Lift + Cruise), Propulsion Type (Battery Electric, Hybrid Electric, Hydrogen Electric), MTOW (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Historical Data and Forecast 2025-2034")

, Technology (Multirotor, Vectored Thrust, Lift + Cruise), Propulsion Type (Battery Electric, Hybrid Electric, Hydrogen Electric), MTOW (Below 2,000 lbs, 2,000 to 5,000 lbs, Above 5,000 lbs), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Historical Data and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Electric Vertical Take-off and Landing Aircraft Market

Published Date : 06 Jan 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date