- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Electronic Lab Notebook Market Size & Share Forecast 2025–2034 | 7.6% CAGR

Global Electronic Lab Notebook Market Size, Share, Analysis By Product Type (Cross-Disciplinary ELN Platforms, Specific/Discipline-Focused ELN Systems), By License Type (Proprietary Software, Open-Source ELN Solutions), By Delivery Mode (On-Premise Deployment, Cloud-Based ELN Platforms), By End-User (Life Sciences, Pharmaceutical Companies, CROs, Academic Research Institutions, Food & Beverage & Agriculture Industries, Other End-Users) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Digital Lab Transformation Trends & Forecast 2025–2034

Report Overview

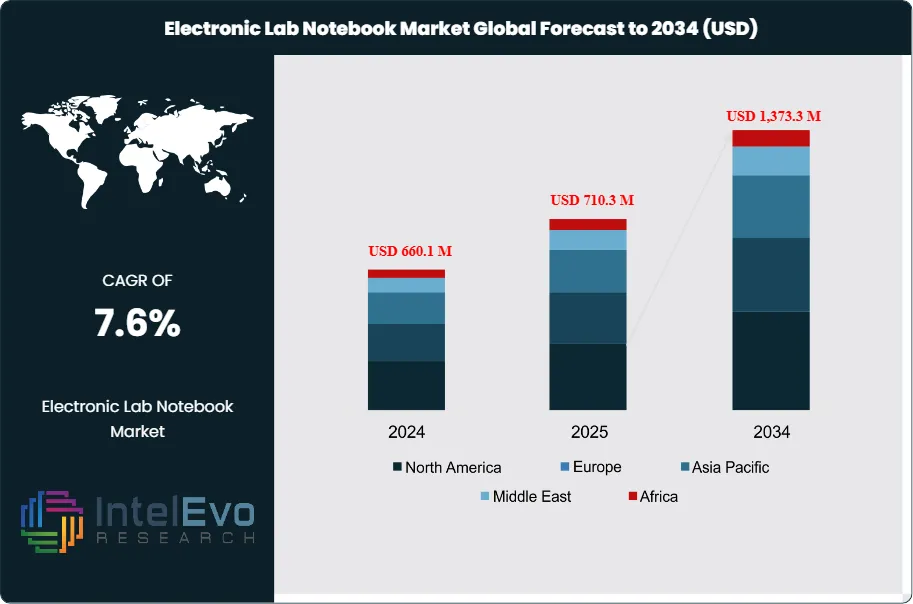

The Electronic Lab Notebook Market was valued at USD 660.1 Million in 2024 and is estimated to reach approximately USD 710.3 Million in 2025. Driven by increasing digitization of laboratory workflows, growing demand for secure research data management, and rising adoption across pharmaceutical, biotechnology, and academic research institutions, the market is projected to grow from about USD 764.3 Million in 2026 to nearly USD 1,373.3 Million by 2034, registering a compound annual growth rate (CAGR) of around 7.6% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportElectronic lab notebooks (ELNs) replace paper notebooks by digitizing experimental documentation, data capture, and collaboration. ELNs allow teams to store structured text, images, graphs, and instrument outputs in a single record. This shift supports faster retrieval and stronger traceability across research phases, which elevates productivity and improves confidence in results.

Demand remains strongest in regulated and data-intensive settings. Pharmaceuticals and biotechnology are estimated to account for about 45% of 2024 revenue, driven by discovery throughput needs and audit-ready documentation requirements across R&D and quality functions. Contract research organizations and academic institutes add scale through multi-site studies and shared workspaces. On the supply side, competition focuses on interoperability with LIMS and SDMS, configurable templates, and validated deployment options. Cloud-based ELNs represent an estimated 55% of 2024 spending and should approach ~70% by 2034 as subscription procurement and remote collaboration become standard.

Regulation shapes both purchasing criteria and product design. FDA 21 CFR Part 11 expectations, GxP controls, and ISO-aligned procedures push laboratories toward electronic signatures, tamper-evident audit logs, role-based permissions, and retention policies with complete change histories. These requirements raise the value of ELNs, but they also increase implementation burden. Key risks include cybersecurity incidents, inconsistent data standards across teams, integration failures, and vendor lock-in that can widen total program cost and delay return on investment.

Technology advances continue to expand ELN utility beyond record-keeping. AI-driven search and classification, automated metadata capture, and workflow automation reduce manual logging and improve reproducibility. Vendors are adding analytics connectors and automation layers to support near real-time review and exception detection. A 2024 Technology Networks report noted that 77% of laboratory leaders said the COVID-19 period accelerated digital transformation plans, which supports sustained funding for ELN modernization.

Regionally, North America leads with an estimated 38% share in 2024 due to high R&D intensity and compliance-driven spending. Europe follows at roughly 28%, supported by life sciences manufacturing depth and mature governance practices. Asia-Pacific is the fastest-growing region, projected near 9% CAGR, with investment hotspots in China, India, Singapore, and South Korea as biopharma capacity and clinical research activity expand.

, By License Type (Proprietary Software, Open-Source ELN Solutions), By Delivery Mode (On-Premise Deployment, Cloud-Based ELN Platforms), By End-User (Life Sciences, Pharmaceutical Companies, CROs, Academic Research Institutions, Food & Beverage & Agriculture Industries, Other End-Users) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Digital Lab Transformation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Electronic Lab Notebook Market grows from 0.6 billion USD, 2023 to 1.3 billion USD, 2033 at 7.6%, 2026-2034.

- Segment Dominance: Cross-disciplinary products lead with 53.8%, 2023 due to broad applicability across research domains.

- Segment Dominance: Cloud-based delivery leads with 62.0%, 2023, reflecting scalability and remote accessibility needs.

- Driver: Pharmaceuticals drive adoption with 38.5%, 2023 as digital documentation supports compliant drug development cycles.

- Restraint: Proprietary licensing leads with estimated: 55.0%, 2023, which can elevate switching costs and limit interoperability.

- Opportunity: Vendors can target modernization programs with estimated: 0.7 billion USD, 2024 as labs accelerate digital transformation spending.

- Trend: Adoption shifts toward SaaS with estimated: 65.0%, 2024 as automation and AI-assisted capture improve workflow speed.

- Regional Analysis: North America leads with 35.0%, 2024, supported by advanced research infrastructure and higher compliance spend.

By Product

Cross-disciplinary electronic lab notebooks remain the largest product category in the ELN market, accounting for approximately 53.8 percent of total revenue as of the latest benchmark year. Their adoption continues to expand through 2025 as research organizations prioritize standardization across departments. These platforms support multiple scientific workflows within a single environment, allowing chemistry, biology, materials science, and analytical teams to operate on a shared system. This approach reduces software fragmentation and improves data continuity across research stages.

Integration capability is a central factor behind this dominance. Cross-disciplinary ELNs connect with laboratory instruments, LIMS, and scientific data management systems, enabling automated data capture and reducing manual entry errors. Large pharmaceutical firms and multinational research centers increasingly mandate these platforms to support multi-site collaboration and regulatory documentation. Specific ELNs, designed for niche domains such as synthetic chemistry or molecular biology, continue to serve specialized users. However, their limited interoperability restricts broader enterprise deployment, keeping their market share structurally lower despite strong adoption in focused research environments.

By License

Proprietary licenses continue to represent the majority of ELN deployments, supported by enterprise demand for vendor-backed updates, security assurance, and regulatory alignment. In 2025, proprietary models are estimated to account for over 60 percent of active installations globally. Vendors provide validated software releases, audit trails, and electronic signature frameworks that align with FDA 21 CFR Part 11 and GxP requirements, which remain critical purchasing criteria in regulated industries.

Open-license ELNs retain relevance in academic and publicly funded research settings where budget constraints and customization needs shape procurement decisions. These platforms allow direct code modification and flexible deployment. Adoption remains limited among large enterprises due to the absence of guaranteed technical support and higher internal maintenance demands. As compliance scrutiny intensifies, open systems face slower uptake outside universities and small research groups.

By Delivery Mode

Cloud-based ELNs continue to lead delivery preferences, holding roughly 62 percent of market share. Adoption accelerates as laboratories expand remote collaboration and decentralized research models. Cloud deployment supports rapid scaling, centralized updates, and predictable subscription costs, which appeal to contract research organizations and mid-sized laboratories managing fluctuating project volumes.

On-premise systems maintain a presence in environments with strict data residency or internal security policies. Defense-linked research centers and select pharmaceutical manufacturers continue to invest in local infrastructure. However, higher capital expenditure and ongoing maintenance requirements limit broader expansion. Market data suggests cloud-based ELNs will exceed 70 percent adoption by the early 2030s as compliance-certified hosting options mature.

By End-User

Pharmaceutical companies remain the leading end-user group, representing approximately 38.5 percent of total demand. ELNs support clinical documentation, formulation development, and intellectual property protection across long research cycles. Rapid audit access and data traceability directly reduce regulatory risk and shorten review timelines.

Life sciences firms and CROs follow closely, driven by outsourced research growth and sponsor reporting requirements. Academic institutions emphasize collaboration and data retention, while food, beverage, and agriculture research increasingly adopts ELNs to support quality testing and regulatory documentation. Adoption across non-pharma sectors continues to rise as digital recordkeeping becomes standard practice.

By Region

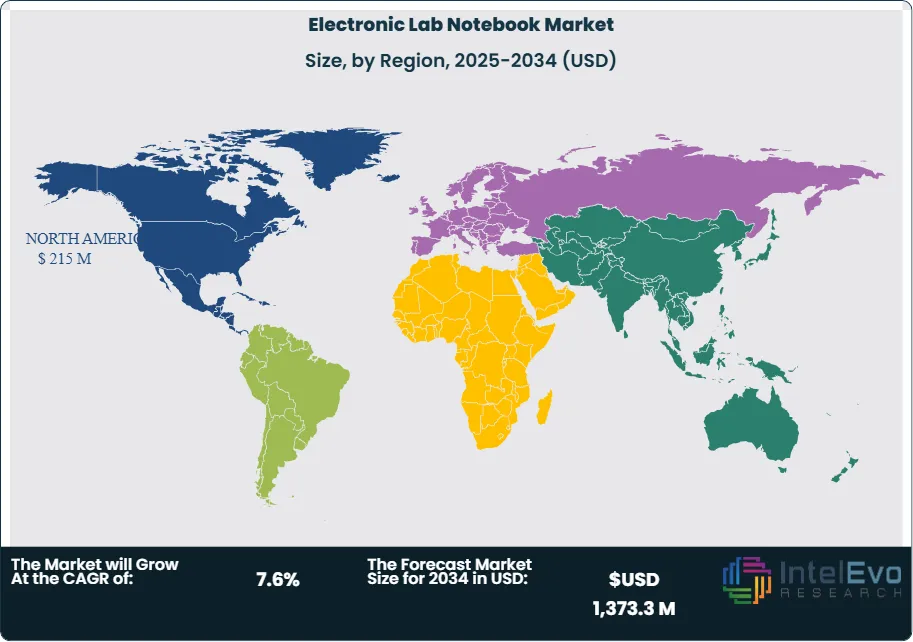

North America remains the largest regional market, holding about 35.0 percent share with an estimated value exceeding USD 215 million. Strong research funding, established pharmaceutical clusters, and early adoption of digital lab infrastructure support continued expansion. Regulatory enforcement and data governance expectations further reinforce ELN demand.

Europe follows with steady adoption across life sciences and chemical research, supported by harmonized compliance standards. Asia Pacific records the fastest growth rate, exceeding 8 percent CAGR, driven by expanding pharmaceutical manufacturing and government-backed research programs in China, India, South Korea, and Singapore. Latin America and the Middle East and Africa remain smaller markets but show rising interest as laboratory modernization initiatives progress.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Cross-disciplinary

- Specific

By License

- Proprietary

- Open

By Delivery Mode

- On-Premise

- Cloud-based

By End-User

- Lifesciences

- Food and Beverages & Agriculture Industries

- CRO’s

- Academic Research

- Pharmaceutical

- Other End-Users

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 710.3 M |

| Forecast Revenue (2034) | USD 1,373.3 M |

| CAGR (2025-2034) | 7.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Cross-disciplinary, Specific), By License (Proprietary, Open), By Delivery Mode (On-Premise, Cloud-based), By End-User (Lifesciences, Food and Beverages & Agriculture Industries, CRO’s, Academic Research, Pharmaceutical, Other End-Users) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Thermo Fisher Scientific Inc., LabWare, Bruker Corporation, Danaher Corporation, Accelrys, Inc., Waters Corporation, Abbott, Agilent Technologies, Inc., Core Informatics, LLC, PerkinElmer, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By License Type (Proprietary Software, Open-Source ELN Solutions), By Delivery Mode (On-Premise Deployment, Cloud-Based ELN Platforms), By End-User (Life Sciences, Pharmaceutical Companies, CROs, Academic Research Institutions, Food & Beverage & Agriculture Industries, Other End-Users) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Digital Lab Transformation Trends & Forecast 2025–2034")

, By License Type (Proprietary Software, Open-Source ELN Solutions), By Delivery Mode (On-Premise Deployment, Cloud-Based ELN Platforms), By End-User (Life Sciences, Pharmaceutical Companies, CROs, Academic Research Institutions, Food & Beverage & Agriculture Industries, Other End-Users) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Digital Lab Transformation Trends & Forecast 2025–2034")

, By License Type (Proprietary Software, Open-Source ELN Solutions), By Delivery Mode (On-Premise Deployment, Cloud-Based ELN Platforms), By End-User (Life Sciences, Pharmaceutical Companies, CROs, Academic Research Institutions, Food & Beverage & Agriculture Industries, Other End-Users) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Digital Lab Transformation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Electronic Lab Notebook Market?

The Global Electronic Lab Notebook Market was valued at USD 660.1 Million in 2024 and is projected to reach USD 1,373.3 Million by 2034, growing at a CAGR of 7.6% from 2026–2034. Explore key trends, drivers, digital lab transformation, secure data management solutions, and opportunities across pharma, biotech, and research institutions.

Who are the major players in the Electronic Lab Notebook Market?

Thermo Fisher Scientific Inc., LabWare, Bruker Corporation, Danaher Corporation, Accelrys, Inc., Waters Corporation, Abbott, Agilent Technologies, Inc., Core Informatics, LLC, PerkinElmer, Inc.

Which segments covered the Electronic Lab Notebook Market?

By Product (Cross-disciplinary, Specific), By License (Proprietary, Open), By Delivery Mode (On-Premise, Cloud-based), By End-User (Lifesciences, Food and Beverages & Agriculture Industries, CRO’s, Academic Research, Pharmaceutical, Other End-Users)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Electronic Lab Notebook Market

Published Date : 05 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date