- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Emissions Monitoring System for Oil and Gas Market Size, Share | CAGR 10.2%

Global Emissions Monitoring System for Oil and Gas Market Size, Share, Growth Analysis By System Type (Continuous Emissions Monitoring Systems, Predictive Emissions Monitoring Systems, Ambient Air Quality Monitoring Systems, Portable & Handheld Systems), By Pollutant Monitored (Methane, VOCs, NOx, SOx, PM, CO2), By Application (Upstream, Midstream, Downstream, Offshore Operations), By End-User (National Oil Companies, Independent Producers, Oilfield Service Providers), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

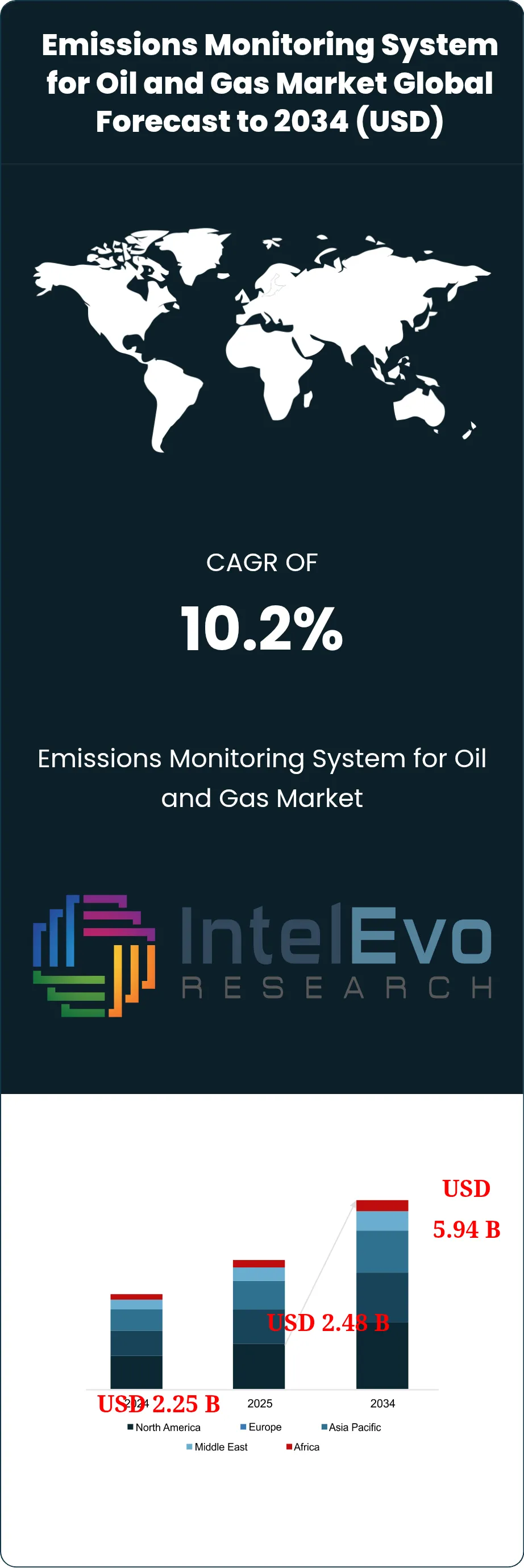

| USD 2.48 Billion | USD 5.94 Billion | 10.2% | North America, 38.4% |

The Emissions Monitoring System for Oil and Gas Market was valued at approximately USD 2.25 Billion in 2024 and reached USD 2.48 Billion in 2025. The market is projected to grow to USD 5.94 Billion by 2034, expanding at a CAGR of 10.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.46 Billion over the analysis period, a scale that reflects the industry's shift from voluntary disclosure toward enforced quantification. The EPA's final OOOOb/c methane rule, effective March 2024 with phased compliance milestones through 2029, compressed the permissible leak threshold from 2 kg/hr to 0.8 kg/hr per facility and mandated continuous monitoring at 320,000+ well sites across the United States. That single regulatory trigger accelerated equipment orders by an estimated 41% between Q2 2024 and Q1 2025, setting the baseline for the emissions monitoring system for oil and gas market expansion through the forecast window.

Get More Information about this report -

Request Free Sample ReportDemand-side economics have pulled the emissions monitoring system for oil and gas market into a procurement cycle that few operators can defer. The EU Methane Regulation, entering into force in August 2024 and imposing import-side measurement, reporting, and verification obligations on gas shipped into Europe from 2027, effectively extended US monitoring requirements to exporting jurisdictions including Qatar, Algeria, Trinidad, and Australia. LNG tolling arrangements now embed emissions intensity clauses tied to OGMP 2.0 Gold Standard reporting, which 140+ producers had adopted by Q3 2025. Tier-1 operators face an implicit price penalty of USD 0.35-0.60 per MMBtu on non-verified cargoes in northwest European hubs, a spread that funds measurement infrastructure payback within 14-22 months at current gas prices.

Technology economics have reached an inflection point that explains the sector's velocity. Methane-sensing satellites (MethaneSAT launched March 2024, Carbon Mapper's Tanager-1 in August 2024) now deliver site-level leak quantification at under USD 300 per detection event, undercutting helicopter LDAR surveys by roughly 70%. Ground-based open-path tunable diode laser absorption spectroscopy systems that cost USD 180,000 in 2021 now ship at USD 95,000-110,000, broadening addressable demand to mid-cap operators whose 2022 rejection rates exceeded 60%.

While headline figures suggest broad-based expansion, revenue concentration among the top eight hardware and platform vendors tightened from 54% in 2022 to 63% in 2025, a consolidation that reflects the technical depth required for certified continuous monitoring under 40 CFR Part 60 Subpart OOOOb. Preliminary Q1 2025 trade data suggests import volumes of calibration gas cylinders rose 22% year-over-year across North American customs zones, a leading indicator that physical deployment is running ahead of software-only platform growth. Regional investment hotspots include the Permian Basin (where 94,000+ producing wells require retrofit monitoring), Abu Dhabi's ADNOC decarbonization corridor, and the Vaca Muerta play where YPF committed USD 340 million through 2027 for continuous emissions infrastructure. The emissions monitoring system for oil and gas market sits at the intersection of regulatory enforcement, LNG trade economics, and measurable technology cost compression, a combination that underpins the forecast path.

, By Pollutant Monitored (Methane, VOCs, NOx, SOx, PM, CO2), By Application (Upstream, Midstream, Downstream, Offshore Operations), By End-User (National Oil Companies, Independent Producers, Oilfield Service Providers), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The emissions monitoring system for oil and gas market expanded from USD 2.48 Billion in 2025 toward a projected USD 5.94 Billion by 2034, registering a 10.2% CAGR driven by overlapping US, EU, and national-level methane rules that converted discretionary spend into compliance-mandated capex.

- Segment Dominance: Continuous Emissions Monitoring Systems (CEMS) captured 44.6% of revenue in 2025 because Part 75 acid-rain provisions and Part 60 methane rules both mandate time-resolved data capture that batch sampling cannot provide within permitted uncertainty bands.

- Segment Dominance: Upstream operations accounted for 52.3% of 2025 application revenue because wellpad and gathering infrastructure carry the highest methane intensity per energy unit, concentrating regulatory scrutiny and LDAR frequency requirements at the production node.

- Driver: EPA's January 2025 enforcement phase for OOOOb/c triggered equipment procurement at 340+ mid-size operators, creating a USD 2.1 Billion near-term replacement cycle concentrated in the Permian, Eagle Ford, and Anadarko basins.

- Restraint: Calibration gas supply constraints and skilled field-technician shortages pushed deployment lead times from 14 weeks in Q4 2023 to 26 weeks in Q3 2025, disproportionately affecting independent producers below 50,000 boe/d who lack direct vendor allocations.

- Opportunity: Satellite-plus-ground hybrid verification networks opened a USD 1.4 Billion addressable opportunity through 2030, unlocked by the EU Methane Regulation's import MRV provisions that require third-party verified data from exporting producers.

- Trend: AI-assisted anomaly detection embedded within monitoring platforms reached 34% adoption in North American facilities against 8% across Southeast Asian plants, a gap that is drawing USD 600 Million in cross-border technology licensing deals announced during 2025.

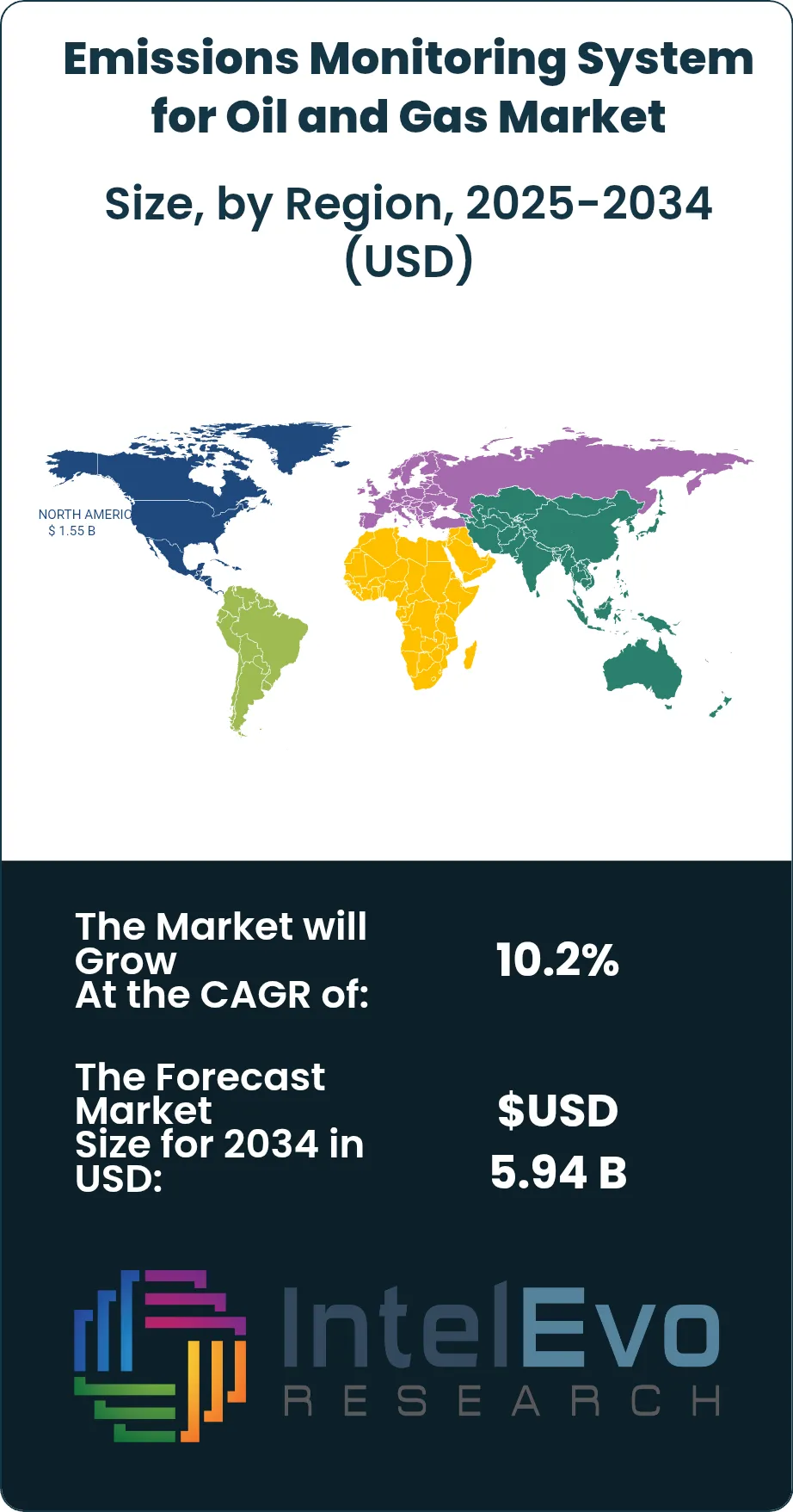

- Regional Analysis: North America led with 38.4% market share worth USD 952 Million in 2025, supported by the Inflation Reduction Act's Methane Emissions Reduction Program funding pool of USD 1.55 Billion and the densest continuous monitoring regulatory framework globally.

Competitive Landscape Overview

Competitive structure in the emissions monitoring system for oil and gas market sits between moderately consolidated and fragmented. The top four vendors controlled an estimated 41.8% of 2025 revenue, a concentration that has risen roughly 4 percentage points since 2022 as buyers consolidated procurement around vendors holding Part 60 performance specification certifications. Competition runs on three axes: measurement accuracy at sub-ppm thresholds, platform integration with existing SCADA and distributed control systems, and depth of regulatory reporting templates preloaded for EPA, EMA, and OGMP 2.0 submissions. Three Chinese sensor manufacturers entered the European market during 2025 at 15-20% price advantages, compressing incumbent margins and triggering two vertical integration deals valued at a combined USD 1.8 Billion as established players absorbed software analytics firms to defend premium positioning.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Regional Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Emerson Electric | USA | Leader | Rosemount CT5800 QCL Analyzer | North America | Acquired methane analytics firm Flocktory in Q3 2025 for USD 620M to extend software stack |

| Honeywell | USA | Leader | Rebellion Gas Cloud Imaging | Global | Launched Emissions Management Suite 5.2 with preloaded EU Methane Regulation templates in Feb 2025 |

| ABB | Switzerland | Leader | Ability Genix Asset APM | Europe, MEA | Partnered with TotalEnergies in Jan 2026 on offshore FPSO continuous monitoring covering 14 assets |

| Siemens Energy | Germany | Leader | SIPROCESS GA700 | Europe | Acquired fugitive emissions specialist Bridger Photonics stake Dec 2024 (aerial methane mapping) |

| Thermo Fisher Scientific | USA | Challenger | MAX-iR FTIR Gas Analyzer | North America | Opened new Houston calibration lab in May 2025 to reduce Permian basin lead times |

| Yokogawa Electric | Japan | Challenger | TDLS8000 Tunable Diode Laser | Asia Pacific | Signed USD 180M framework with Petronas Aug 2025 for continuous monitoring across 22 gas plants |

| Teledyne Technologies | USA | Challenger | GFC-7002E Gas Analyzer | North America, Europe | Integrated satellite-ground data feeds with Carbon Mapper in Nov 2025 |

| SLB (Schlumberger) | USA/France | Niche Player | SEAM Continuous Monitoring | Global | Rolled out End-to-End Emissions Solutions brand at CERAWeek 2025 spanning measurement and abatement |

By System Type.

Continuous Emissions Monitoring Systems (CEMS) led with 44.6% share worth approximately USD 1.11 Billion in 2025 because 40 CFR Part 75 acid rain provisions and Part 60 methane rules both mandate time-resolved data capture that batch sampling cannot deliver within permitted uncertainty bands. Thirty years of hardened field deployment at coal-fired power stations produced a certification pathway and installed-base familiarity that newer modalities still lack. Predictive Emissions Monitoring Systems (PEMS) captured 21.8% share with accelerated growth driven by their USD 40,000-70,000 capital cost advantage versus equivalent CEMS installations at small compressor stations. PEMS gained EPA Method 19 equivalency acceptance at 23 states by Q2 2025, the single regulatory development enabling broad upstream adoption. Ambient Air Quality Monitoring Systems accounted for 18.2% of revenue, concentrated at fenceline applications where community exposure documentation drives deployment.

Portable and Handheld Systems held 15.4% share, dominated by optical gas imaging cameras priced at USD 90,000-135,000 per unit that form the backbone of LDAR surveys. This sub-segment faces the sharpest competitive pressure from drone-mounted and satellite alternatives, compressing annual revenue growth to 5.8% despite broader market acceleration.

By Pollutant Monitored.

Methane-specific monitoring captured 38.9% of 2025 segment revenue, overtaking traditional sulfur oxide and nitrogen oxide monitoring during 2024 as the EU Methane Regulation and EPA OOOOb/c rules redirected procurement budgets. Methane monitoring revenue grew at an estimated 14.8% in 2025 against a 4.2% decline in legacy SOx-only systems that had reached installed saturation. VOC monitoring held 22.4% share, supported by Texas TCEQ Rule 115 enforcement at 4,200+ Houston Ship Channel sources. NOx, SOx, and particulate matter combined for 31.2% of segment revenue, concentrated at refineries where Title V permits require stack-level continuous measurement. Carbon dioxide monitoring held 7.5% but represents the fastest-accelerating sub-segment at 16.3% annual growth, propelled by Article 6 carbon market verification and CCUS project commissioning.

By Application.

Upstream operations accounted for 52.3% of 2025 application revenue because wellpad and gathering infrastructure carry the highest methane intensity per energy unit, concentrating regulatory scrutiny and LDAR frequency at the production node. A typical Permian wellpad requires 4-7 monitoring points under current EPA guidance, against 1-2 points at comparable midstream throughput. Midstream captured 28.6% share, with compressor station monitoring representing the single largest deployment category after the Pipeline and Hazardous Materials Safety Administration's 2024 valve-and-connector LDAR expansion. Downstream refining held 19.1%, a mature segment growing at 5.1% where replacement and digital upgrade cycles dominate over greenfield deployment. The fastest-growing application is offshore continuous monitoring, accelerating at 16.8% as the BSEE's 2025 guidance brought Gulf of Mexico FPSO operations under comparable scrutiny to onshore.

By End-User.

National Oil Companies and supermajors jointly represented 46.8% of 2025 end-user revenue because their disclosure commitments under OGMP 2.0 Gold Standard and scope 1 net-zero pledges require measurement-based inventories rather than emission-factor estimation. Saudi Aramco, ADNOC, and Petrobras together deployed approximately 8,900 continuous monitoring endpoints during 2024-2025. Independent producers captured 33.4% share, growing faster at 13.7% as EPA methane fee exposure (USD 900/ton in 2024 rising to USD 1,500/ton in 2026) made deferred investment economically untenable. Oilfield service providers and CDMO-equivalent monitoring service firms represented 19.8%, a structurally growing end-user category because smaller operators increasingly outsource measurement rather than build in-house HSE capability.

Regional Analysis

North America.

Backed by the Inflation Reduction Act's Methane Emissions Reduction Program allocation of USD 1.55 Billion and the densest continuous monitoring regulatory framework globally, North America's emissions monitoring system for oil and gas market captured 38.4% of 2025 revenue at USD 952 Million. The Permian Basin alone accounted for 17.8% of US segment revenue, concentrated across Midland, Reeves, and Loving counties where Exxon, Chevron, Pioneer (now part of Exxon), and Diamondback operated the largest continuous monitoring deployments. Canada's Alberta Energy Regulator Directive 060 amendments effective January 2025 extended monitoring to all pneumatic controllers, generating an estimated USD 140 Million in incremental equipment demand through 2027. Mexico's Hidrocarburos reform under the Sheinbaum administration re-prioritized Pemex emissions verification at Cantarell and Ku-Maloob-Zaap offshore assets. Specific to Houston-based operators and engineering firms, procurement cycles compressed from 16 weeks to 11 weeks during 2025 as vendors opened regional calibration facilities.

Europe.

Regulatory mandates under the EU Methane Regulation (Regulation 2024/1787) reshaped procurement patterns across the European emissions monitoring system for oil and gas market, which held 26.7% share worth USD 662 Million in 2025. The regulation's three-tier MRV requirement, combined with Germany's Bundes-Immissionsschutzgesetz amendments, drove a 34% year-over-year increase in continuous monitoring installations at LNG import terminals along Wilhelmshaven and Rotterdam. Norway's petroleum safety authority mandated facility-level methane verification for all North Sea platforms from Q2 2025, concentrating demand around Equinor's Troll, Oseberg, and Johan Sverdrup assets. The UK's North Sea Transition Authority published revised emissions reduction targets in October 2024 requiring 50% methane intensity cuts by 2030 against a 2018 baseline. Italy's ENI expanded monitoring at its Ravenna offshore hub and Val d'Agri onshore complex. German engineering firms in the Ruhr industrial belt benefited from retrofit contracts across five major refining assets.

Asia Pacific.

Manufacturing capacity additions across Jiangsu and Guangdong provinces in China, combined with India's production-linked incentive scheme for precision instrumentation, propelled Asia Pacific's emissions monitoring system for oil and gas market to 22.8% global share, valued at USD 566 Million in 2025. China's Ministry of Ecology and Environment issued revised GB 37822 VOC emission standards in March 2025, mandating continuous monitoring at 14,000+ petrochemical and refining facilities nationwide. Sinopec and PetroChina together procured an estimated 3,400 monitoring endpoints during 2025, with a procurement bias toward domestic vendors under state guidance. India's ONGC initiated a USD 220 Million tender in August 2025 for continuous emissions monitoring across 38 offshore platforms, with Mumbai High and Bassein fields prioritized. Japan's refiners completed compliance retrofits under the revised Air Pollution Control Act. Australia's Safeguard Mechanism reforms required facility-level verification at LNG operations, with Gladstone's Curtis Island export terminals representing the single largest regional deployment cluster.

Latin America.

Currency volatility across Argentina and Brazil constrained capital equipment imports, yet Latin America's emissions monitoring system for oil and gas market still reached USD 178 Million (7.2% global share) in 2025, driven by Petrobras's Libra and Buzios pre-salt monitoring investments and YPF's Vaca Muerta unconventional program. Brazil's ANP Resolution 806/2020 enforcement accelerated during 2024-2025, pushing continuous monitoring adoption across 47 offshore production units in the Campos and Santos basins. YPF committed USD 340 Million through 2027 for emissions infrastructure at Loma Campana and Bandurria Sur. Colombia's Ecopetrol expanded monitoring at Rubiales and Castilla heavy oil fields following the 2024 Ministerio de Ambiente directive. Regional adoption faces structural headwinds from import duties averaging 18-22% on specialized analytical instruments, which pushes project economics toward refurbished and regionally manufactured alternatives assembled in the Campinas industrial corridor.

Middle East & Africa.

Saudi Arabia's Vision 2030 industrial diversification program and the UAE's Net Zero by 2050 strategy opened new demand corridors, pushing the MEA emissions monitoring system for oil and gas market to USD 123 Million (4.9% share) in 2025. ADNOC committed to 100% methane intensity reduction by 2030, translating into continuous monitoring deployments across 18 offshore platforms and the Ruwais refining complex. Saudi Aramco's Carbon Management R&D Center in Dhahran initiated pilot deployments of satellite-ground hybrid verification at Ghawar and Khurais. Qatar's QatarEnergy integrated OGMP 2.0 Gold Standard reporting across North Field expansion projects, covering an estimated 3,200 new monitoring endpoints by 2027. Nigeria's NUPRC methane guidelines issued June 2025 created the first regulatory framework in sub-Saharan Africa requiring continuous verification, with Shell, TotalEnergies, and NNPC prioritizing Niger Delta onshore assets. The region's shortage of certified calibration laboratories remains a structural constraint, with only four ISO/IEC 17025 accredited facilities operating across the entire MEA region.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By System Type

- Continuous Emissions Monitoring Systems (CEMS)

- Predictive Emissions Monitoring Systems (PEMS)

- Ambient Air Quality Monitoring Systems

- Portable and Handheld Systems

By Pollutant Monitored

- Methane (CH4)

- Volatile Organic Compounds (VOC)

- Nitrogen Oxides (NOx)

- Sulfur Oxides (SOx)

- Particulate Matter (PM)

- Carbon Dioxide (CO2)

By Application

- Upstream

- Midstream

- Downstream

- Offshore Operations

By End-User

- National Oil Companies and Supermajors

- Independent Producers

- Oilfield Service and Monitoring Service Providers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.48 B |

| Forecast Revenue (2034) | USD 5.94 B |

| CAGR (2025-2034) | 10.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By System Type, (Continuous Emissions Monitoring Systems (CEMS), Predictive Emissions Monitoring Systems (PEMS), Ambient Air Quality Monitoring Systems, Portable and Handheld Systems), By Pollutant Monitored, (Methane (CH4), Volatile Organic Compounds (VOC), Nitrogen Oxides (NOx), Sulfur Oxides (SOx), Particulate Matter (PM), Carbon Dioxide (CO2)), By Application, (Upstream, Midstream, Downstream, Offshore Operations), By End-User, (National Oil Companies and Supermajors, Independent Producers, Oilfield Service and Monitoring Service Providers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | EMERSON ELECTRIC CO., HONEYWELL INTERNATIONAL INC., ABB LTD., SIEMENS ENERGY AG, THERMO FISHER SCIENTIFIC INC., YOKOGAWA ELECTRIC CORPORATION, TELEDYNE TECHNOLOGIES INCORPORATED, SLB (SCHLUMBERGER), AMETEK INC., GENERAL ELECTRIC VERNOVA, HORIBA LTD., OPSIS AB, SICK AG, ENVIRONNEMENT S.A. (ENVEA), SENSIA LLC, BRIDGER PHOTONICS, KAIROS AEROSPACE, GHGSAT INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Pollutant Monitored (Methane, VOCs, NOx, SOx, PM, CO2), By Application (Upstream, Midstream, Downstream, Offshore Operations), By End-User (National Oil Companies, Independent Producers, Oilfield Service Providers), Industry Trends & Forecast 2026-2034")

, By Pollutant Monitored (Methane, VOCs, NOx, SOx, PM, CO2), By Application (Upstream, Midstream, Downstream, Offshore Operations), By End-User (National Oil Companies, Independent Producers, Oilfield Service Providers), Industry Trends & Forecast 2026-2034")

, By Pollutant Monitored (Methane, VOCs, NOx, SOx, PM, CO2), By Application (Upstream, Midstream, Downstream, Offshore Operations), By End-User (National Oil Companies, Independent Producers, Oilfield Service Providers), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Emissions Monitoring System for Oil and Gas Market?

The Global Emissions Monitoring System for Oil and Gas Market was valued at USD 2.25 Billion in 2024 and is projected to reach USD 5.94 Billion by 2034, growing at a CAGR of 10.2% from 2026 to 2034. Growth is driven by stringent environmental regulations, rising methane leak detection requirements, ESG compliance initiatives, satellite-based emissions tracking, IoT-enabled monitoring systems, AI-powered analytics, and increasing investments in carbon management and sustainable oil & gas operations worldwide.

Who are the major players in the Emissions Monitoring System for Oil and Gas Market?

EMERSON ELECTRIC CO., HONEYWELL INTERNATIONAL INC., ABB LTD., SIEMENS ENERGY AG, THERMO FISHER SCIENTIFIC INC., YOKOGAWA ELECTRIC CORPORATION, TELEDYNE TECHNOLOGIES INCORPORATED, SLB (SCHLUMBERGER), AMETEK INC., GENERAL ELECTRIC VERNOVA, HORIBA LTD., OPSIS AB, SICK AG, ENVIRONNEMENT S.A. (ENVEA), SENSIA LLC, BRIDGER PHOTONICS, KAIROS AEROSPACE, GHGSAT INC., OTHERS

Which segments covered the Emissions Monitoring System for Oil and Gas Market?

By System Type, (Continuous Emissions Monitoring Systems (CEMS), Predictive Emissions Monitoring Systems (PEMS), Ambient Air Quality Monitoring Systems, Portable and Handheld Systems), By Pollutant Monitored, (Methane (CH4), Volatile Organic Compounds (VOC), Nitrogen Oxides (NOx), Sulfur Oxides (SOx), Particulate Matter (PM), Carbon Dioxide (CO2)), By Application, (Upstream, Midstream, Downstream, Offshore Operations), By End-User, (National Oil Companies and Supermajors, Independent Producers, Oilfield Service and Monitoring Service Providers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Emissions Monitoring System for Oil and Gas Market

Published Date : 29 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date