- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Energy Trading & Risk Management Market Forecast 2034 | CAGR 8.6%

Global Energy Trading and Risk Management (ETRM) Software Market Size, Share, Growth & Industry Analysis By Offering (Software Solutions, Professional Services), By Deployment Mode (On-Premise, Cloud-Based), By Commodity Type (Power & Electricity, Natural Gas & LNG, Crude Oil & Refined Products, Environmental Commodities, Others), By End-User (Energy Companies, Financial Institutions, Trading Firms) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 18.42 Billion | USD 38.65 Billion | 8.6% | North America, 38.6% |

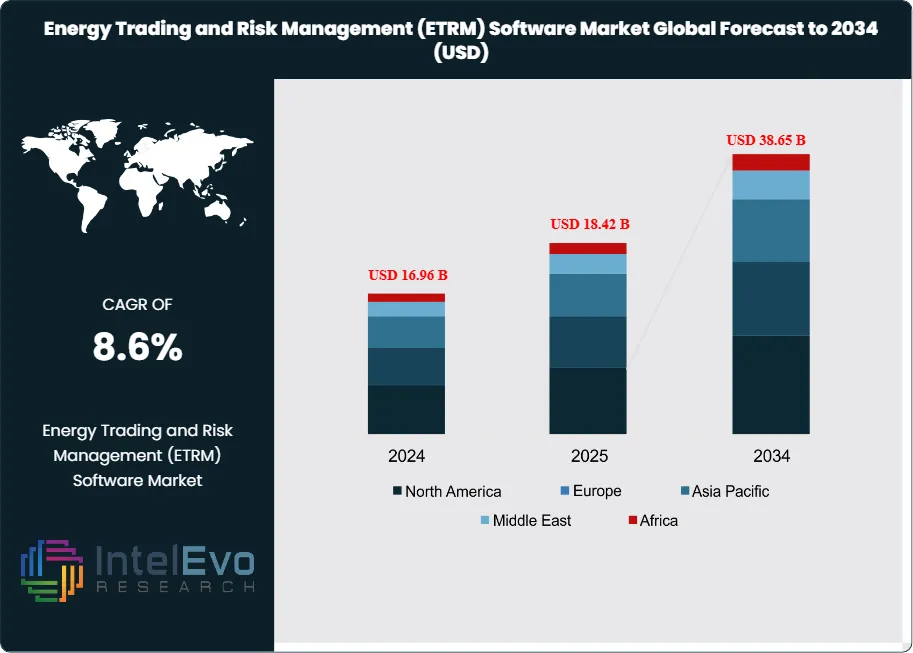

The Energy Trading and Risk Management (ETRM) Software Market was valued at approximately USD 16.96 Billion in 2024 and reached USD 18.42 Billion in 2025. The market is projected to grow to USD 38.65 Billion by 2034, expanding at a CAGR of 8.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.23 billion over the analysis period. The energy trading and risk management software market encompasses platforms that enable commodity trading organizations, utilities, energy producers, and financial institutions to execute trades, manage physical and financial positions, quantify market exposures, and maintain regulatory compliance across power, natural gas, crude oil, refined products, LNG, and environmental commodities.

Get More Information about this report -

Request Free Sample ReportDemand for ETRM software accelerates as energy markets face increasing volatility and complexity. The energy transition has introduced new tradable instruments including renewable energy certificates, carbon credits, and battery storage rights that require sophisticated position management capabilities. Power market liberalization in Europe and Asia creates new trading opportunities while expanding compliance requirements under regulations including REMIT, MiFID II, and Dodd-Frank. The integration of renewable generation assets with variable output profiles demands advanced forecasting and scheduling tools embedded within ETRM platforms. Natural gas markets have globalized through LNG spot trading, creating basis risks between regional hubs that traders must manage through robust portfolio analytics.

The energy trading and risk management software market benefits from regulatory requirements that mandate position reporting, trade surveillance, and risk quantification. CFTC position limits for energy commodities require real-time monitoring capabilities that legacy spreadsheet-based approaches cannot provide. FERC reporting requirements for physical power and gas transactions drive adoption of integrated trade capture and settlement systems. European utilities face ACER REMIT transaction reporting obligations that necessitate automated trade reporting functionality. These regulatory drivers create non-discretionary software spending regardless of commodity price cycles.

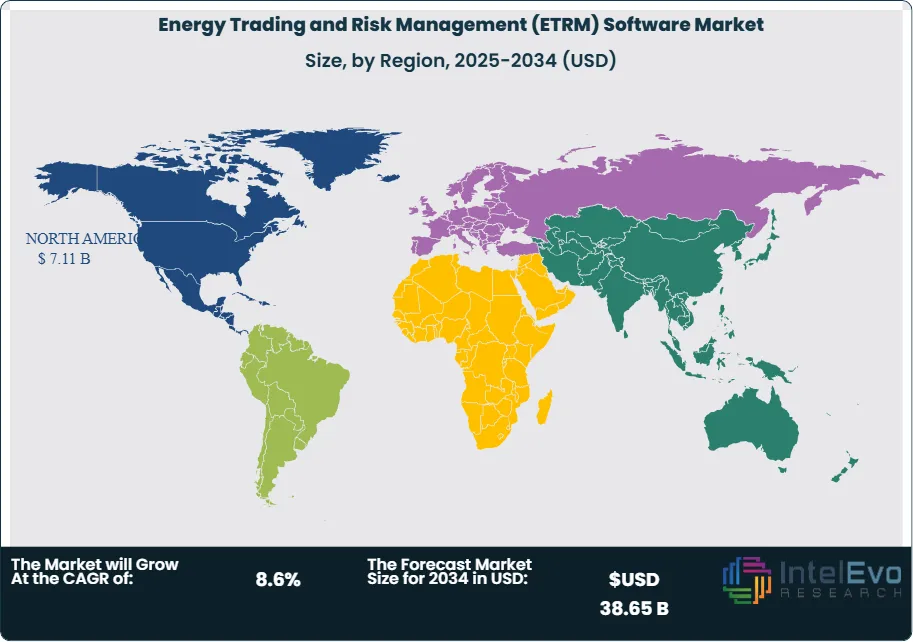

Cloud deployment models are transforming the ETRM software market. Cloud-based solutions represent 44.8% of new implementations in 2025, up from 22% in 2020. The shift reflects end-user preferences for reduced IT infrastructure requirements, faster deployment timelines, and automatic software updates that maintain regulatory compliance. Molecule, Eka Software, and newer entrants have built cloud-native platforms that compete with established vendors transitioning legacy architectures. North America leads the market with 38.6% share, generating USD 7.11 billion in 2025. Europe follows at 32.4% share driven by power market integration and gas hub development. Asia Pacific accounts for 16.8% with growth driven by power sector deregulation in Japan, India, and Southeast Asian markets.

Software Market Size, Share, Growth & Industry Analysis By Offering (Software Solutions, Professional Services), By Deployment Mode (On-Premise, Cloud-Based), By Commodity Type (Power & Electricity, Natural Gas & LNG, Crude Oil & Refined Products, Environmental Commodities, Others), By End-User (Energy Companies, Financial Institutions, Trading Firms) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The energy trading and risk management software market is projected to expand from USD 18.42 billion in 2025 to USD 38.65 billion by 2034, achieving a CAGR of 8.6% during the 2025-2034 forecast period.

- Segment Dominance (By Offering): Software solutions command 72.4% market share in 2025, generating USD 13.34 billion, as organizations invest in integrated platforms for trade capture, position management, and risk analytics.

- Segment Dominance (By End-User): Energy companies account for 48.6% of market revenue in 2025, valued at USD 8.95 billion, as utilities, oil majors, and independent power producers upgrade trading and risk systems.

- Driver: Energy market volatility has intensified ETRM investment, with European gas price swings exceeding 400% in 2022 driving 28% increase in risk management software spending through 2025.

- Restraint: Implementation complexity and integration challenges extend project timelines, with 42% of large ETRM deployments exceeding initial schedules by more than six months.

- Opportunity: Carbon trading and environmental commodities present a USD 3.2 billion incremental opportunity by 2034, as emissions trading schemes expand globally and carbon border adjustment mechanisms take effect.

- Trend: AI and machine learning adoption within ETRM platforms has reached 35% of enterprise installations in 2025, enabling predictive analytics for price forecasting, demand estimation, and anomaly detection.

- Regional Analysis: North America maintains market leadership with 38.6% share and USD 7.11 billion revenue in 2025, driven by commodity trading concentration in Houston and financial trading operations in New York and Chicago.

Competitive Landscape Overview

The energy trading and risk management software market exhibits moderate consolidation, with the top four vendors capturing approximately 52% of global revenue in 2025. Competition centers on functional depth, commodity coverage, and integration capabilities with market data providers and settlement systems. ION Group's December 2024 acquisition of OpenLink for USD 1.8 billion created the dominant industry platform combining Allegro and Endur solutions. SAP maintains strong positions among large utilities and oil majors through SAP Commodity Management integration with core ERP systems. Established vendors face pressure from cloud-native challengers including Molecule and Eka Software that offer faster implementation and lower total cost of ownership. Vendor consolidation continues as private equity sponsors seek scale in a market characterized by high switching costs and recurring maintenance revenue.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| OpenLink | US | Leader | Endur ETRM Platform | North America | Acquired by ION Group for USD 1.8B (Dec 2024) |

| ION Group | Ireland | Leader | Allegro ETRM Suite | Global | Completed OpenLink acquisition (Dec 2024) |

| SAP | Germany | Leader | SAP Commodity Management | Europe | Launched AI-powered risk analytics (Mar 2025) |

| Openlink (Brady) | UK | Leader | Brady Trinity ETRM | Europe | Expanded renewable trading modules (Jan 2026) |

| FIS | US | Challenger | Energy Risk Manager | North America | Partnered with Enverus for data (Apr 2025) |

| Eka Software | US | Challenger | Eka Cloud CTRM | Asia Pacific | Raised USD 125M Series D (Jun 2025) |

| Murex | France | Challenger | MX.3 Commodities | Europe | Added carbon credits module (Aug 2025) |

| Aspect Enterprise | UK | Niche Player | AspectCTRM | Europe | Launched SaaS platform (Sep 2025) |

| Molecule | US | Niche Player | Molecule Cloud ETRM | North America | Secured USD 65M funding (Feb 2025) |

| Pioneer Solutions | US | Niche Player | TRMTracker | North America | Released mobile trading app (Nov 2024) |

By Offering

The energy trading and risk management software market segments by offering into software solutions and professional services. Software solutions dominate with 72.4% market share in 2025, generating USD 13.34 billion in revenue. This segment encompasses trade capture and execution platforms, position management systems, risk analytics engines, settlement and accounting modules, and regulatory reporting tools. License and subscription revenues comprise the core software segment, with perpetual licenses declining as vendors transition to SaaS delivery models. The average enterprise ETRM software contract generates USD 2-8 million in annual recurring revenue depending on commodity scope and user count. OpenLink Endur, ION Allegro, and SAP Commodity Management represent leading software platforms serving large enterprise customers.

Professional services hold 27.6% share at USD 5.08 billion in 2025. This segment includes implementation consulting, system integration, customization development, training, and managed services. ETRM implementations typically require 12-24 months for enterprise deployments, with professional services fees often exceeding initial software license costs. Accenture, Capgemini, and specialized boutiques including Opportune and Capco provide implementation capacity. Ongoing support and enhancement services generate recurring revenue as organizations adapt systems to changing market structures and regulatory requirements.

By Deployment Mode

On-premise deployment retains 55.2% market share in 2025, generating USD 10.17 billion. Large energy companies and trading houses with significant IT infrastructure continue to prefer on-premise installations that provide complete control over sensitive trading algorithms, position data, and risk models. Security concerns regarding cloud access to proprietary trading strategies reinforce on-premise preferences among sophisticated trading operations. Major oil companies, investment banks, and large utilities predominantly operate on-premise ETRM environments. Cloud-based deployment accounts for 44.8% share at USD 8.25 billion in 2025. This segment has grown rapidly from 22% share in 2020 as vendors developed secure, compliant cloud architectures. Molecule pioneered cloud-native ETRM for commodity markets, while established vendors including ION and OpenLink have migrated platforms to AWS and Azure. Mid-market energy companies, renewable developers, and newer trading operations prefer cloud deployment for reduced IT overhead and faster implementation.

By Commodity Type

Power and electricity trading represents the largest commodity segment at 34.2% share in 2025, generating USD 6.30 billion. Power markets require sophisticated real-time trading capabilities, unit commitment modeling, transmission scheduling, and settlement processes that differ fundamentally from other commodities. European power market coupling, U.S. ISO participation, and emerging Asian markets drive software demand. Natural gas and LNG holds 28.4% share at USD 5.23 billion. The globalization of gas markets through LNG spot trading creates complex basis management requirements spanning Henry Hub, TTF, JKM, and emerging Asian benchmarks. Pipeline scheduling, storage optimization, and balancing functionality represent critical capabilities. Crude oil and refined products captures 22.6% share, valued at USD 4.16 billion. Physical crude trading, refinery margin optimization, and product distribution require integration with logistics and supply chain systems. Environmental commodities including carbon credits, renewable energy certificates, and emissions allowances account for 8.4% share at USD 1.55 billion, representing the fastest-growing segment at 14% annual growth. Other commodities including coal, metals, and agricultural products comprise 6.4% at USD 1.18 billion.

By End-User

Energy companies represent the largest end-user segment at 48.6% share in 2025, generating USD 8.95 billion. This category includes integrated oil companies, independent producers, utilities, and renewable energy developers that trade physical commodities and financial derivatives to hedge production or consumption. Shell, BP, ExxonMobil, and TotalEnergies operate extensive trading operations that require multi-commodity ETRM platforms. Financial institutions hold 32.8% share at USD 6.04 billion. Investment banks, hedge funds, and proprietary trading firms deploy ETRM software for commodities trading desks that take speculative positions and provide market-making services. Goldman Sachs, Morgan Stanley, and Citadel represent major consumers of ETRM solutions. Trading companies and merchants capture 18.6% share, valued at USD 3.43 billion. Physical commodity merchants including Vitol, Trafigura, Gunvor, and Glencore require platforms supporting global logistics, storage, and trading operations across multiple commodity classes.

Regional Analysis

North America

North America commands 38.6% of the global energy trading and risk management software market in 2025, generating USD 7.11 billion in revenue. The United States accounts for 88% of regional revenue, driven by the concentration of commodity trading operations in Houston, financial trading in New York and Chicago, and technology vendors in major metro areas. Houston serves as the global center for physical energy trading, hosting trading operations of major oil companies, independent producers, and physical commodity merchants. CME Group and ICE trading activity drives demand for derivatives-focused ETRM functionality. CFTC position limit monitoring and FERC reporting requirements create compliance-driven software spending. PJM, ERCOT, CAISO, and other ISO markets require sophisticated power trading and scheduling capabilities. Canada contributes 9% of regional revenue with natural gas marketing operations in Calgary and power trading across provincial markets. Mexico accounts for 3% as energy reform has attracted international participants requiring ETRM infrastructure.

Europe

Europe holds 32.4% market share in 2025, valued at USD 5.97 billion. The United Kingdom leads with 28% of regional revenue as London maintains its position as a global commodity trading hub despite Brexit. Major oil companies, trading houses, and financial institutions operate extensive trading desks requiring sophisticated ETRM platforms. Germany contributes 22% driven by utility trading operations, industrial consumers hedging energy costs, and RWE and E.ON trading activities. The Netherlands accounts for 16% as TTF gas hub development and Amsterdam/Rotterdam commodity trading generate software demand. Switzerland contributes 12% with commodity trading houses in Geneva and Zug including Vitol, Trafigura, and Gunvor operating multi-commodity platforms. France adds 10% through EDF trading operations and financial institution activities. Nordic markets comprise 8% with active power trading across Nord Pool. REMIT compliance requirements, MiFID II reporting obligations, and EU ETS carbon trading create regulatory-driven demand across the region.

Asia Pacific

Asia Pacific represents 16.8% of the global market in 2025, generating USD 3.09 billion in revenue, while achieving the fastest regional growth at 11.2% CAGR through 2034. Japan leads with 32% of regional revenue as power market deregulation since 2016 has created wholesale trading opportunities requiring ETRM infrastructure. JEPX trading activity continues to expand as retail competition intensifies. Singapore accounts for 24% as the Asian commodity trading hub hosting oil trading operations for major international traders and regional players. China contributes 22% as national oil companies expand trading activities and power market reform creates wholesale electricity trading. India represents 12% with power exchange development and gas market reforms driving ETRM adoption among utilities and industrial consumers. Australia adds 6% with NEM power trading and LNG export operations. South Korea captures 4% with KEPCO and independent generators requiring risk management capabilities.

Middle East and Africa

The Middle East and Africa region represents 7.8% of the global market in 2025, generating USD 1.44 billion in revenue. The UAE leads with 42% of regional revenue as Dubai develops as a commodities trading hub through DMCC and various commodity exchanges. ENOC, ADNOC, and international trading houses operate regional desks requiring ETRM capabilities. Saudi Arabia accounts for 28% as Aramco's trading arm expands and domestic market development creates new requirements. The Kingdom's Vision 2030 includes financial market development that will expand derivatives trading. South Africa contributes 12% with Eskom and independent power producers managing power market positions. African LNG exporters including Nigeria and Egypt comprise 10% as national oil companies develop trading sophistication. Other GCC markets including Qatar and Kuwait account for 8% with national oil company trading operations.

Latin America

Latin America accounts for 4.4% of the global market in 2025, valued at USD 810 million. Brazil dominates with 52% of regional revenue as power market reform and pre-salt oil production create trading requirements. Petrobras trading operations and independent power producers drive ETRM demand. The expanding free power market enables bilateral trading that requires position management capabilities. Mexico contributes 24% following energy reform that attracted international traders and created wholesale electricity market trading. Chile accounts for 14% with copper mining power requirements and renewable energy development creating hedging needs. Argentina represents 10% with YPF and Vaca Muerta development generating oil and gas trading requirements. Colombia and other Andean markets capture the remaining share as energy markets develop and international investment expands trading sophistication requirements.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software Solutions

- Professional Services

By Deployment Mode

- On-Premise

- Cloud-Based

By Commodity Type

- Power and Electricity

- Natural Gas and LNG

- Crude Oil and Refined Products

- Environmental Commodities

- Others

By End-User

- Energy Companies

- Financial Institutions

- Trading Companies and Merchants

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.42 B |

| Forecast Revenue (2034) | USD 38.65 B |

| CAGR (2025-2034) | 8.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software Solutions, Professional Services), By Deployment Mode, (On-Premise, Cloud-Based), By Commodity Type, (Power and Electricity, Natural Gas and LNG, Crude Oil and Refined Products, Environmental Commodities, Others), By End-User, (Energy Companies, Financial Institutions, Trading Companies and Merchants) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ION GROUP (ALLEGRO), OPENLINK (ION GROUP), SAP, BRADY TECHNOLOGIES, EKA SOFTWARE, FIS, MUREX, MOLECULE, ASPECT ENTERPRISE SOLUTIONS, PIONEER SOLUTIONS, ENVERUS, ORACLE, AMPHORA, AXPO SOLUTIONS, AGIBOO, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Software Market Size, Share, Growth & Industry Analysis By Offering (Software Solutions, Professional Services), By Deployment Mode (On-Premise, Cloud-Based), By Commodity Type (Power & Electricity, Natural Gas & LNG, Crude Oil & Refined Products, Environmental Commodities, Others), By End-User (Energy Companies, Financial Institutions, Trading Firms) Industry Trends & Forecast 2026–2034")

Software Market Size, Share, Growth & Industry Analysis By Offering (Software Solutions, Professional Services), By Deployment Mode (On-Premise, Cloud-Based), By Commodity Type (Power & Electricity, Natural Gas & LNG, Crude Oil & Refined Products, Environmental Commodities, Others), By End-User (Energy Companies, Financial Institutions, Trading Firms) Industry Trends & Forecast 2026–2034")

Software Market Size, Share, Growth & Industry Analysis By Offering (Software Solutions, Professional Services), By Deployment Mode (On-Premise, Cloud-Based), By Commodity Type (Power & Electricity, Natural Gas & LNG, Crude Oil & Refined Products, Environmental Commodities, Others), By End-User (Energy Companies, Financial Institutions, Trading Firms) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Energy Trading and Risk Management (ETRM) Software Market?

Global Energy trading & risk management software market valued at USD 16.96B in 2024, reaching USD 38.65B by 2034, growing at a CAGR of 8.6% from 2026–2034.

Who are the major players in the Energy Trading and Risk Management (ETRM) Software Market?

ION GROUP (ALLEGRO), OPENLINK (ION GROUP), SAP, BRADY TECHNOLOGIES, EKA SOFTWARE, FIS, MUREX, MOLECULE, ASPECT ENTERPRISE SOLUTIONS, PIONEER SOLUTIONS, ENVERUS, ORACLE, AMPHORA, AXPO SOLUTIONS, AGIBOO, Others

Which segments covered the Energy Trading and Risk Management (ETRM) Software Market?

By Offering, (Software Solutions, Professional Services), By Deployment Mode, (On-Premise, Cloud-Based), By Commodity Type, (Power and Electricity, Natural Gas and LNG, Crude Oil and Refined Products, Environmental Commodities, Others), By End-User, (Energy Companies, Financial Institutions, Trading Companies and Merchants)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Energy Trading and Risk Management (ETRM) Software Market

Published Date : 03 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date