- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Enhanced Oil Recovery Chemical Market Size, Share & Growth | CAGR 9.6%

Global Enhanced Oil Recovery Chemical Market Size, Share, Analysis By Chemical Type (Polymers including Hydrolyzed Polyacrylamide and Biopolymers, Surfactants including Anionic, Non-ionic and Amphoteric, Alkaline Chemicals, Specialty Support Chemicals), By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore Oilfields, Offshore Fields), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 4.8 Billion, 2025 | USD 10.9 Billion, 2034 | 9.6%, 2026–2034 | Middle East and Africa, 31.2%, 2025 |

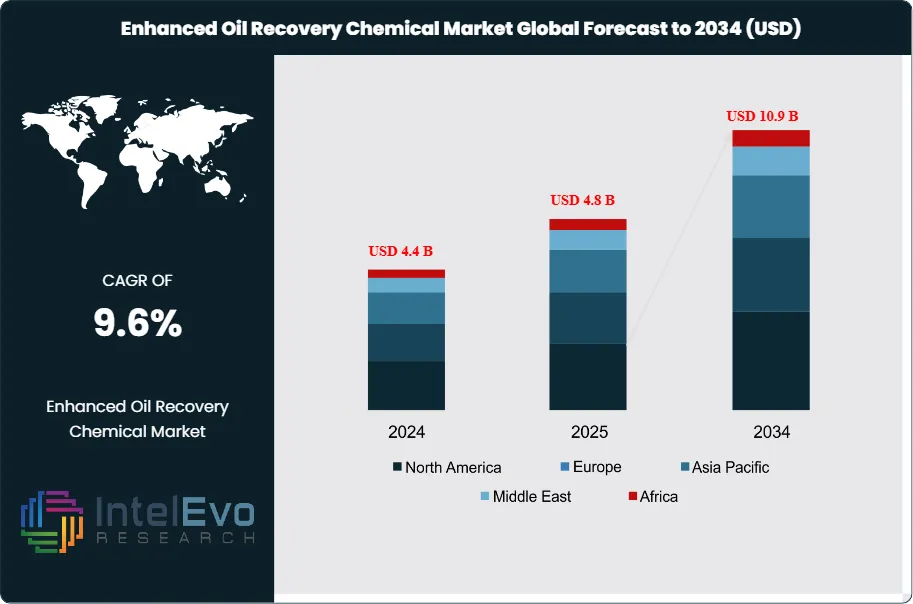

The Enhanced Oil Recovery Chemical Market was valued at approximately USD 4.4 Billion in 2024 and increased to USD 4.8 Billion in 2025. The market is projected to reach nearly USD 10.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 9.6% during the forecast period from 2026 to 2034. The enhanced oil recovery chemical market is experiencing broad-based growth driven by the imperative for operators to extract maximum value from maturing conventional oilfields, rising demand for chemical EOR programs that improve sweep efficiency in waterflooded reservoirs, and sustained investment in polymer flooding, surfactant injection, and alkaline-surfactant-polymer programs across high-value mature basins. Enhanced oil recovery chemicals, encompassing polymers, surfactants, alkaline chemicals, and specialty chemical systems, serve as the primary technical tools that operators deploy to access the two-thirds of original oil in place that primary and secondary recovery methods leave behind.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the enhanced oil recovery chemical market include the global maturation of prolific conventional reservoirs in the Middle East, North America, and the Former Soviet Union that have entered declining production phases amenable to chemical EOR intervention. Operators are increasingly recognizing that chemical EOR programs can add 5–15% incremental recovery to mature waterflooded fields at costs per barrel that are competitive with greenfield development in many price environments. Supply-side dynamics reflect growing competition among specialty chemical manufacturers including SNF Group, BASF, Solvay, and Stepan Company, which are expanding their EOR-grade polymer and surfactant production capacities in response to rising operator program commitments. The enhanced oil recovery chemical market benefits from the long program duration of chemical EOR projects, which typically run for 5–15 years once initiated, creating sustained chemical supply demand and recurring revenue for established vendors.

Regulatory frameworks are influencing the enhanced oil recovery chemical market primarily through produced water management and environmental compliance requirements. Chemical EOR programs generate produced fluids containing injected chemicals that require treatment before disposal or reinjection, adding operational cost and complexity to program management. The U.S. Environmental Protection Agency's Underground Injection Control program regulates the use of chemical injection wells, while in China the Ministry of Ecology and Environment has established chemical EOR environmental impact assessment requirements for large-scale polymer flooding projects. Norway's offshore chemical regulation framework imposes rigorous ecotoxicological screening for all chemicals used in offshore EOR programs, driving demand for biodegradable polymer and surfactant formulations.

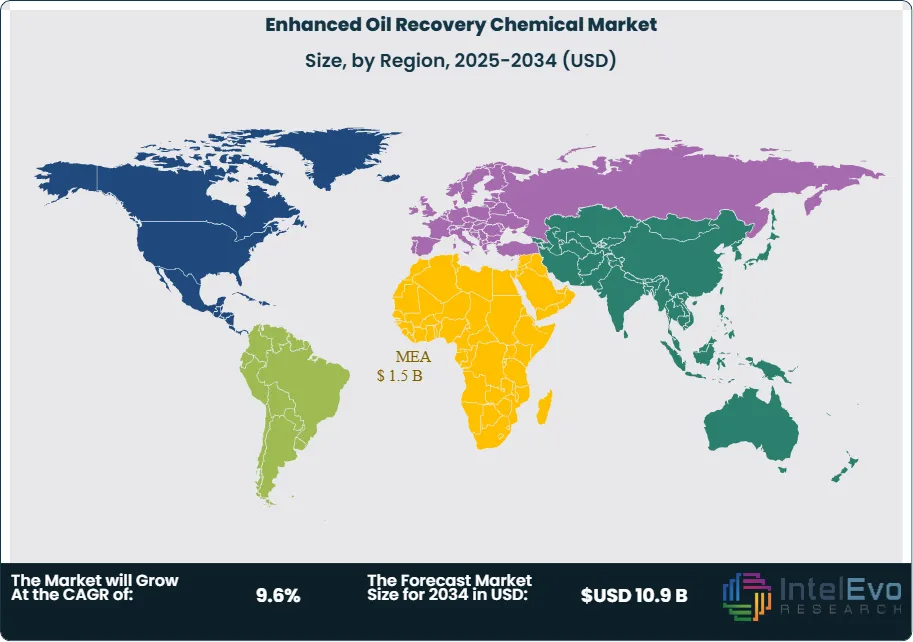

Risk factors in the enhanced oil recovery chemical market include oil price sensitivity that affects the economic viability of chemical EOR programs, technical failure risk from inadequate reservoir characterization that leads to poor chemical sweep efficiency, and the long capital payback periods of chemical EOR programs that make project economics sensitive to sustained oil price assumptions. The market is also navigating the energy transition, with operators evaluating chemical EOR investments against competing capital allocation opportunities in renewables and carbon capture. The Middle East and Africa region holds the largest share of the enhanced oil recovery chemical market at 31.2% in 2025 at USD 1.5 Billion, driven by Arabian Peninsula mature field programs. Asia Pacific follows at 28.6% at USD 1.4 Billion, anchored by China's world-leading polymer flooding program. By 2034, bio-based and low-environmental-impact chemical EOR formulations are projected to define a significant portion of new program specifications, reshaping the competitive landscape of the enhanced oil recovery chemical market.

, By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore Oilfields, Offshore Fields), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global enhanced oil recovery chemical market was valued at USD 4.8 Billion in 2025 and is projected to reach USD 10.9 Billion by 2034, registering a CAGR of 9.6% during the forecast period 2025–2034, supported by expanding polymer flooding programs and rising mature field chemical EOR investment globally.

- Segment Dominance (By Chemical Type): Polymers are the dominant chemical type in the enhanced oil recovery chemical market with a 48.2% share in 2025 at USD 2.3 Billion, driven by the widespread deployment of hydrolyzed polyacrylamide polymer flooding programs across Chinese, Middle Eastern, and North American mature reservoirs.

- Segment Dominance (By Application): Onshore EOR applications lead the market with a 72.4% share in 2025 at USD 3.5 Billion, as the majority of global chemical EOR program activity is concentrated in continental mature oilfields including China's Daqing, Shengli, and Xinjiang fields and Middle Eastern carbonate reservoirs.

- Driver: The accelerating maturation of global conventional oil reservoirs, with the International Energy Agency estimating that over 70% of producing fields globally have passed their production peak, is compelling operators to deploy chemical EOR programs that can add 5–15% incremental recovery factor to reservoirs where primary and secondary methods have been exhausted.

- Restraint: Oil price sensitivity constrains the enhanced oil recovery chemical market, as chemical EOR program economics require sustained oil prices above USD 45–60 per barrel to justify capital commitment. Price volatility in the 2025 environment, with Brent crude fluctuating between USD 68 and USD 88 per barrel, creates investment hesitancy that delays program final investment decisions by 12–24 months for price-sensitive operators.

- Opportunity: Offshore chemical EOR programs represent a USD 2.1 Billion addressable opportunity within the enhanced oil recovery chemical market by 2034. Current offshore chemical EOR deployments account for less than 8% of global chemical EOR program activity as of 2025, with the majority of technically viable offshore candidates remaining on conventional waterflooding without chemical augmentation.

- Trend: Bio-based and environmentally acceptable polymer and surfactant formulations for EOR applications are growing at 24.6% annually in 2025, driven by offshore regulatory requirements in Norway and the United Kingdom and corporate sustainability commitments from major international oil companies that are mandating reduced-toxicity chemical sourcing across their EOR programs.

- Regional Analysis: The Middle East and Africa region leads the global enhanced oil recovery chemical market with a 31.2% share in 2025, equivalent to USD 1.5 Billion, anchored by large-scale polymer and surfactant flooding programs in Saudi Arabia, Kuwait, Oman, and the UAE targeting incremental recovery from aging carbonate reservoirs.

Competitive Landscape

The Global Enhanced Oil Recovery (EOR) Chemical Market is moderately consolidated, with the top four companies accounting for an estimated 39.0% of total market revenue in 2025. Competition is primarily technology-driven, focusing on polymer flooding, surfactant flooding, alkaline–surfactant–polymer (ASP) systems, and customized reservoir chemistry solutions rather than pure commodity chemical supply. Major chemical producers and oilfield service companies are expanding collaborations with national oil companies and offshore operators to deploy advanced chemical flooding solutions in mature reservoirs. Competitive intensity increased in 2025–2026 as operators in China, the Middle East, and Latin America accelerated EOR programs to extend the life of aging oilfields and improve recovery factors.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| BASF | Germany | Leader | Polymer flooding and surfactant EOR chemical systems | Europe, Middle East, Asia-Pacific | Expanded EOR chemical production capacity and technical partnerships with Middle East operators in 2025. |

| DOW | US | Leader | Surfactants and advanced polymer formulations for EOR | North America, Latin America, Asia-Pacific | Strengthened collaboration with oil companies to deploy surfactant flooding solutions for mature reservoirs in 2025. |

| SOLVAY | Belgium | Leader | Specialty surfactants and chemical flooding technologies | Europe, Middle East, Africa | Expanded specialty chemical portfolio targeting enhanced oil recovery and reservoir optimization in 2025. |

| SNF | France | Leader | High-performance polyacrylamide polymers for EOR flooding | China, Middle East, North America | Expanded polymer production and supply agreements for large-scale polymer flooding projects in China in 2025. |

| CLARIANT | Switzerland | Challenger | Specialty surfactants and tailored EOR chemical systems | Middle East, Europe, Asia-Pacific | Launched new chemical formulations for improved oil displacement efficiency in carbonate reservoirs in 2025. |

| CHAMPIONX | US | Challenger | Production chemicals and chemical EOR solutions | North America, Middle East, Latin America | Expanded EOR chemical services portfolio integrated with digital production monitoring in 2025. |

| STEPPAN COMPANY | US | Challenger | Surfactants for chemical flooding and enhanced recovery | North America, Asia-Pacific | Expanded specialty surfactant supply for upstream chemical flooding programs in 2025. |

| INNOSPEC | US | Niche Player | Oilfield specialty chemicals including EOR additives | North America, Middle East | Strengthened oilfield chemical distribution partnerships across Middle East EOR projects in 2025. |

| CRODA INTERNATIONAL | UK | Niche Player | Specialty surfactants and reservoir chemistry solutions | Europe, Middle East, Asia-Pacific | Expanded specialty surfactant offerings for upstream energy applications in 2025. |

| HUNTSMAN | US | Niche Player | Advanced chemical formulations for reservoir treatment | North America, Europe | Expanded specialty chemical R&D programs targeting improved EOR recovery efficiency in 2025. |

Segmentation Analysis

The enhanced oil recovery chemical market segmentation analysis covers four key dimensions: By Chemical Type, By EOR Method, By Application, and By End-User. Each dimension reveals distinct demand concentrations, technology requirements, and competitive structures that characterize the global enhanced oil recovery chemical market through 2034.

By Chemical Type

Polymers represent the dominant chemical type in the enhanced oil recovery chemical market, commanding a 48.2% share in 2025 at USD 2.3 Billion. Hydrolyzed polyacrylamide is the most widely deployed polymer EOR chemical globally, used in polymer flooding programs to increase the viscosity of injected water and improve mobility ratio, thereby enhancing sweep efficiency in heterogeneous reservoirs. China's Daqing oilfield has the world's largest polymer flooding operation, consuming over 300,000 metric tons of polyacrylamide annually and demonstrating incremental recovery factors of 12–15% above conventional waterflooding. SNF Group and BASF are the dominant polymer suppliers globally, with SNF holding an estimated 35% of global EOR polymer supply capacity. Biopolymers including xanthan gum are gaining adoption in reservoirs where synthetic polymer degradation is a concern, particularly in high-temperature carbonate reservoirs above 90 degrees Celsius where polyacrylamide thermal stability becomes limiting.

Surfactants hold a 28.4% share of the enhanced oil recovery chemical market in 2025 at USD 1.4 Billion. Surfactants reduce interfacial tension between oil and water phases, mobilizing trapped residual oil that remains immobile after waterflooding. Anionic surfactants including alpha-olefin sulfonates and internal olefin sulfonates are the most commercially deployed categories, with Stepan Company, Shell Chemicals, and Huntsman Corporation as primary suppliers. Surfactant-polymer co-injection programs, which combine viscosity improvement with interfacial tension reduction, represent the fastest-growing application within the surfactant segment. Alkaline chemicals account for 14.6% of the market at USD 701 Million in 2025, used as saponification agents that generate in-situ surfactants from reservoir crude oil acids. Specialty chemicals including scale inhibitors, biocides, and oxygen scavengers for EOR program support represent the remaining 8.8% at USD 422 Million in 2025.

By EOR Method

Polymer flooding is the dominant EOR method driving enhanced oil recovery chemical market demand, accounting for 44.8% of method-based revenue in 2025 at USD 2.2 Billion. Polymer flooding is the most commercially mature chemical EOR technique, with field applications spanning five decades and a well-documented performance database across sandstone and carbonate reservoir types globally. China accounts for approximately 65% of global polymer flooding chemical consumption in 2025, with PetroChina's large-scale polymer flooding programs at Daqing, Shengli, and Liaohe fields representing the world's most extensive continuous polymer EOR operations. The Middle East is the most rapidly expanding polymer flooding market, with Aramco, ADNOC, and Kuwait Oil Company evaluating and deploying polymer flooding in carbonate reservoirs that present unique technical challenges requiring specialized polymer formulations with high-salinity and high-temperature resistance.

Surfactant-polymer flooding represents 26.4% of the EOR method segment in 2025 at USD 1.3 Billion, combining the mobility control benefits of polymer flooding with the interfacial tension reduction of surfactant injection to achieve greater incremental recovery than either technique alone. Alkaline-surfactant-polymer flooding, the most chemically complex commercial EOR method, holds 16.8% of market revenue at USD 807 Million in 2025, achieving incremental recovery factors of 15–22% above conventional waterflooding in technically successful field applications. Microbial EOR applications using specialty microbial cultures and nutrient chemicals represent 12.0% of the method segment at USD 576 Million in 2025, growing from niche applications in specific reservoir types toward broader commercial deployment as microbial strain performance data accumulates from field trials across North America and China.

By Application

Onshore applications dominate the enhanced oil recovery chemical market with a 72.4% share in 2025 at USD 3.5 Billion. The onshore segment encompasses the full spectrum of chemical EOR program activity globally, concentrated in China's mature sandstone oil provinces, Middle Eastern carbonate reservoirs, the U.S. Permian and Midcontinent basins, and the Former Soviet Union's Western Siberian fields. Onshore chemical EOR programs benefit from infrastructure accessibility that allows large-volume chemical injection at economically viable cost structures, continuous monitoring and adjustment of injection parameters based on production response, and the ability to conduct comprehensive reservoir characterization studies that inform chemical system selection and performance prediction. The onshore segment is mature in China and the Middle East but expanding rapidly in the Former Soviet Union as Rosneft, Lukoil, and Gazprom Neft evaluate large-scale polymer flooding for their declining West Siberian sandstone fields.

Offshore chemical EOR applications account for 27.6% of the enhanced oil recovery chemical market in 2025 at USD 1.3 Billion. Offshore chemical EOR programs are technically more complex than onshore deployments due to limited topside space for chemical handling and injection equipment, the need to manage produced chemical-laden fluids in environmentally sensitive marine environments, and the higher cost of intervention when injection parameters require adjustment. The North Sea has the most active offshore chemical EOR portfolio, with Equinor, Aker BP, and Shell deploying polymer flooding at several Norwegian Continental Shelf fields including Dalia, Brage, and Snorre. Brazil's Petrobras is evaluating offshore polymer flooding for specific pre-salt carbonate field applications, representing a significant potential market expansion for offshore EOR chemical vendors. The offshore segment is growing at above-average rates within the enhanced oil recovery chemical market as operator experience accumulates and offshore-specific chemical formulations improve.

By End-User

National oil companies are the largest end-user segment in the enhanced oil recovery chemical market, representing 52.6% of revenue in 2025 at USD 2.5 Billion. PetroChina and CNOOC are the single largest consumers of EOR chemicals globally, with PetroChina's polymer flooding operations at Daqing alone consuming chemical volumes that represent a measurable share of global polyacrylamide production capacity. Saudi Aramco, Kuwait Oil Company, Petroleum Development Oman, and ADNOC collectively represent the second-largest national oil company EOR chemical demand cluster, with combined annual program expenditure estimated at over USD 600 Million in 2025. These operators are increasingly pursuing domestic chemical supply chains to reduce import dependency and satisfy local content requirements.

International oil companies represent 28.4% of the enhanced oil recovery chemical market in 2025 at USD 1.4 Billion. Shell, ExxonMobil, TotalEnergies, and BP operate chemical EOR programs across their global mature field portfolios, with Shell's Minas field polymer flooding program in Indonesia and ExxonMobil's alkaline-surfactant-polymer programs in the Permian Basin among the most extensively documented commercial operations. Independent oil companies account for 19.0% of market revenue at USD 912 Million in 2025, primarily deploying smaller-scale polymer and surfactant EOR programs in North American and North Sea mature fields where incremental recovery economics are supported by established production infrastructure.

Regional Analysis

Middle East & Africa Enhanced Oil Recovery Chemical Market

The Middle East and Africa region leads the global enhanced oil recovery chemical market with a 31.2% share in 2025, equivalent to USD 1.5 Billion. Saudi Arabia is the dominant country market, with Saudi Aramco operating one of the world's most advanced EOR chemical evaluation and deployment programs targeting incremental recovery from its super-giant carbonate reservoirs including Abqaiq, Ghawar, and Safaniya. Saudi Aramco's EOR program includes large-scale surfactant flooding pilots, polymer flooding evaluation in specific reservoir intervals, and alkaline-surfactant-polymer field trials, with chemical procurement commitments estimated at over USD 350 Million annually in 2025. The Kingdom's Vision 2030 initiative mandates maintaining oil production capacity at 12 Million barrels per day, creating policy imperative for EOR program investment to offset natural field decline.

Kuwait is the second-largest Middle East market, with Kuwait Oil Company deploying polymer flooding across its Burgan field, the world's second-largest oilfield, where polymer injection is targeting incremental recovery from the producing Upper Burgan sandstone reservoir. Oman contributes through Petroleum Development Oman's Marmul polymer flooding program, one of the longest continuously operating polymer EOR programs in the Middle East, which has demonstrated sustained incremental production since its initiation in the 1990s. The United Arab Emirates is an emerging EOR chemical market, with ADNOC accelerating chemical EOR evaluation across its onshore and offshore carbonate fields as part of its program to maintain 4 Million barrel per day production capacity. The Middle East and Africa region is projected to grow at a CAGR of 10.4% through 2034, supported by sustained national oil company EOR investment mandates.

Asia Pacific Enhanced Oil Recovery Chemical Market

Asia Pacific holds a 28.6% share of the global enhanced oil recovery chemical market in 2025, generating USD 1.4 Billion in revenue. China is the overwhelmingly dominant country market within the region and globally, accounting for approximately 78% of Asia Pacific market revenue. PetroChina's polymer flooding operations at Daqing, the world's original large-scale polymer EOR field, consume over 300,000 metric tons of polyacrylamide annually, making China the single largest national market for EOR chemicals globally. The Daqing field's polymer flooding program, operational since 1995, has added over 1.2 Billion barrels of incremental oil recovery compared to conventional waterflooding projections, providing the world's most comprehensive field-scale validation of polymer EOR economics.

China's Shengli and Xinjiang oilfields host substantial secondary polymer flooding programs managed by Sinopec, representing additional chemical consumption volumes that collectively position China's domestic EOR chemical demand at approximately 55% of global polymer EOR chemical consumption in 2025. Domestic Chinese chemical manufacturers including CNPC's chemical subsidiaries and Hengju Chemical have developed competitive EOR polymer production capabilities that reduce dependence on international suppliers, shaping the competitive landscape for foreign chemical companies seeking Chinese market access. India is the second-largest Asia Pacific market, with ONGC deploying polymer flooding in specific sandstone reservoirs in Assam and Gujarat provinces. Indonesia represents a growing EOR chemical market as Pertamina evaluates chemical flooding for its Sumatran and Kalimantan mature fields. Asia Pacific is projected to grow at a CAGR of 9.8% through 2034.

North America Enhanced Oil Recovery Chemical Market

North America accounts for 22.4% of the global enhanced oil recovery chemical market in 2025, equivalent to USD 1.1 Billion. The United States is the dominant country market, with chemical EOR program activity concentrated in the Permian Basin, Midcontinent, and Gulf Coast regions where mature waterflooded reservoirs are candidates for polymer and alkaline-surfactant-polymer flooding. ExxonMobil operates one of the most technically advanced commercial alkaline-surfactant-polymer flooding programs in the Permian Basin, targeting residual oil in mature Clearfork formation reservoirs. The U.S. Department of Energy's Carbon Utilization and Storage program has historically supported chemical EOR research and field demonstration projects, providing co-funding that reduces operator risk for early commercial deployments.

Canada contributes approximately 18% of North American enhanced oil recovery chemical market revenue in 2025, with chemical EOR activity primarily in Alberta's heavy oil deposits where surfactant-based solvent-assisted steam flooding programs augment conventional thermal EOR operations. Mexico's Pemex is evaluating chemical EOR for its mature Chicontepec and Southern Region fields, representing a longer-term market expansion opportunity as regulatory frameworks and technical capabilities mature. The United States market benefits from a mature chemical supply chain and strong oilfield chemical research infrastructure concentrated at universities in Texas, Oklahoma, and Colorado. North America is projected to grow at a CAGR of 8.6% through 2034, with growth driven by expanding Permian Basin chemical EOR programs and Canadian heavy oil surfactant applications.

Europe Enhanced Oil Recovery Chemical Market

Europe holds a 10.8% share of the global enhanced oil recovery chemical market in 2025, valued at USD 518 Million. Norway leads the European segment, with the Norwegian Continental Shelf hosting the most technically advanced offshore chemical EOR portfolio globally. Equinor's polymer flooding programs at the Snorre and Brage fields, and its broader offshore EOR research program conducted through the Norwegian Enhanced Oil Recovery Centre, represent the primary demand drivers for EOR chemicals in Norway. The Norwegian petroleum directorate actively supports chemical EOR deployment as a mechanism for improving recovery from the North Sea's maturing production base, with national recovery rate targets influencing operator EOR investment decisions.

The United Kingdom contributes through North Sea chemical EOR pilots and small-scale surfactant flooding programs managed by independent operators in mature fields including Forties, Nelson, and Captain. The Captain field polymer flooding project operated by Chevron on the UK Continental Shelf is one of the few commercially operating offshore polymer flooding programs globally, providing operational data that informs broader offshore EOR chemical market development. Germany contributes modest chemical EOR activity through Wintershall Dea's onshore mature field programs in Lower Saxony. The Netherlands hosts Shell's European EOR technology development activities, with Shell's laboratory and pilot programs in the Netherlands contributing to its global chemical EOR portfolio management. Europe is projected to grow at a CAGR of 8.2% through 2034, with offshore EOR program expansion providing the primary growth catalyst.

Latin America Enhanced Oil Recovery Chemical Market

Latin America accounts for 7.0% of the global enhanced oil recovery chemical market in 2025, totaling USD 336 Million. Brazil is the dominant country market within the region, with Petrobras deploying chemical EOR technologies in specific onshore and offshore field applications. Petrobras's Marmul-analogous carbonate reservoir EOR evaluations in the Campos Basin and onshore Recôncavo Basin polymer flooding pilots represent active chemical procurement programs. However, Petrobras's capital allocation priority for pre-salt greenfield development has historically limited chemical EOR investment in its mature field portfolio, with EOR chemical budgets representing a smaller proportion of total upstream expenditure than in comparable mature-basin-focused operators.

Colombia represents the second-largest Latin American market, with Ecopetrol deploying polymer flooding in specific Llanos Basin sandstone reservoirs and evaluating alkaline-surfactant-polymer programs for its heavier oil fields in the Magdalena Valley. Colombia's national hydrocarbon agency has established mature field recovery improvement targets that provide policy incentive for chemical EOR program investment. Mexico's Pemex is evaluating chemical EOR for its declining Southern Region fields, with technical studies underway for polymer flooding feasibility in Tertiary sandstone formations. Venezuela's mature Orinoco belt and Lake Maracaibo fields present large theoretical chemical EOR opportunities, but economic and operational constraints limit near-term market realization. Latin America is projected to grow at a CAGR of 9.2% through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Chemical Type

- Polymers (Hydrolyzed Polyacrylamide, Biopolymers)

- Surfactants (Anionic, Non-ionic, Amphoteric)

- Alkaline Chemicals

- Specialty Support Chemicals

By EOR Method

- Polymer Flooding

- Surfactant-Polymer Flooding

- Alkaline-Surfactant-Polymer Flooding

- Microbial EOR

By Application

- Onshore

- Offshore

By End-User

- National Oil Companies

- International Oil Companies

- Independent Oil Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.8 B |

| Forecast Revenue (2034) | USD 10.9 B |

| CAGR (2025-2034) | 9.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Chemical Type (Polymers (Hydrolyzed Polyacrylamide, Biopolymers), Surfactants (Anionic, Non-ionic, Amphoteric), Alkaline Chemicals, Specialty Support Chemicals), By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore, Offshore), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SNF GROUP, BASF SE, STEPAN COMPANY, SOLVAY SA, HUNTSMAN CORPORATION, NALCO WATER (ECOLAB INC.), CLARIANT AG, SCHLUMBERGER (SLB) CHEMICAL SERVICES, HALLIBURTON CHEMICAL SOLUTIONS, BAKER HUGHES CHEMICALS, KEMIRA OYJ, AKZO NOBEL N.V., CRODA INTERNATIONAL PLC, NOURYON (FORMERLY AKZO NOBEL SPECIALTY CHEMICALS), HENGJU CHEMICAL GROUP CO., LTD., CNPC BOHAI DRILLING ENGINEERING CO., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore Oilfields, Offshore Fields), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

, By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore Oilfields, Offshore Fields), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

, By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore Oilfields, Offshore Fields), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Enhanced Oil Recovery Chemical Market?

The Global Enhanced Oil Recovery Chemical Market was valued at USD 4.8 Billion in 2025, projected to reach USD 10.9 Billion by 2034 at a CAGR of 9.6% from 2026–2034. Growth is driven by increasing adoption of polymer, surfactant, and alkaline flooding technologies to improve recovery from mature oilfields and maximize hydrocarbon production.

Who are the major players in the Enhanced Oil Recovery Chemical Market?

SNF GROUP, BASF SE, STEPAN COMPANY, SOLVAY SA, HUNTSMAN CORPORATION, NALCO WATER (ECOLAB INC.), CLARIANT AG, SCHLUMBERGER (SLB) CHEMICAL SERVICES, HALLIBURTON CHEMICAL SOLUTIONS, BAKER HUGHES CHEMICALS, KEMIRA OYJ, AKZO NOBEL N.V., CRODA INTERNATIONAL PLC, NOURYON (FORMERLY AKZO NOBEL SPECIALTY CHEMICALS), HENGJU CHEMICAL GROUP CO., LTD., CNPC BOHAI DRILLING ENGINEERING CO., Others

Which segments covered the Enhanced Oil Recovery Chemical Market?

By Chemical Type (Polymers (Hydrolyzed Polyacrylamide, Biopolymers), Surfactants (Anionic, Non-ionic, Amphoteric), Alkaline Chemicals, Specialty Support Chemicals), By EOR Method (Polymer Flooding, Surfactant-Polymer Flooding, Alkaline-Surfactant-Polymer Flooding, Microbial EOR), By Application (Onshore, Offshore), By End-User (National Oil Companies, International Oil Companies, Independent Oil Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Enhanced Oil Recovery Chemical Market

Published Date : 16 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date