- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Enteric Softgel Capsules Market Size, Share & Forecast 2034 | CAGR 3.6%

Global Enteric Softgel Capsules Market Size, Share, Analysis By Product Type (Gelatin Type-A & Type-B, Fish Bone Gelatin, Starch Material, Cellulose Derivatives), By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-User (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034

Report Overview

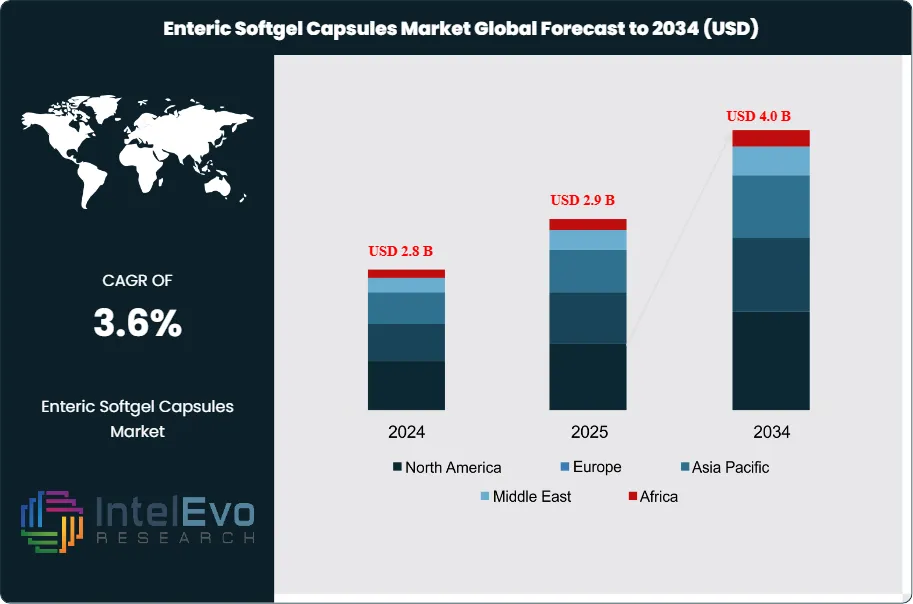

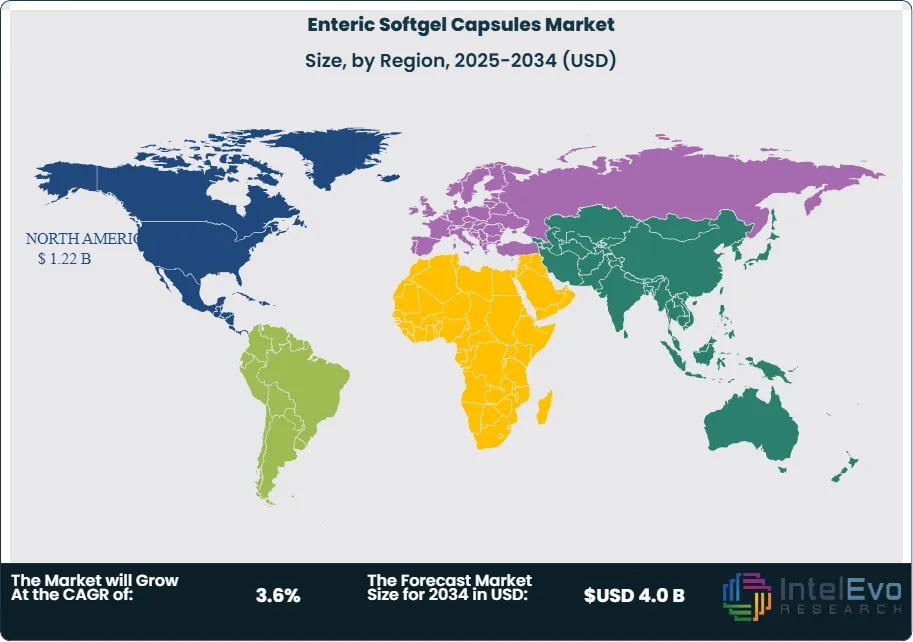

The Enteric Softgel Capsules Market was valued at USD 2.8 billion in 2024 and is projected to reach approximately USD 2.9 billion in 2025. The market is further expected to expand to nearly USD 4.0 billion by 2034, registering a compound annual growth rate (CAGR) of about 3.6% during the forecast period from 2026 to 2034. Growth in the market is driven by the increasing demand for targeted drug delivery systems and improved oral dosage formulations in the pharmaceutical and nutraceutical industries. Enteric softgel capsules help protect active ingredients from stomach acid and ensure release in the intestine, improving drug stability, absorption efficiency, and patient compliance.

Get More Information about this report -

Request Free Sample ReportAdditionally, rising investments in advanced encapsulation technologies, growing consumption of dietary supplements, and the expansion of contract manufacturing services in the pharmaceutical sector are expected to further support market growth during the forecast period.

North America leads in 2024 with 41.9% share, equivalent to about US$ 1.2 Billion, supported by high nutraceutical penetration, steady prescription volumes, and sizable CDMO capacity. Demand rises as manufacturers prioritize targeted intestinal release to protect acid-sensitive actives from gastric degradation and improve downstream absorption. This preference strengthens adoption across probiotics, where brands seek higher microbial viability through gastrointestinal transit, and across omega-3 supplements, where enteric shells help reduce reflux while protecting oxidation-sensitive lipids.

Supply-side competition centers on shell chemistry, fill compatibility, and manufacturing efficiency. Between 2024 and 2025, Sirio Pharma introduced a clean-label approach that embeds enteric functionality directly into gelatin and plant-based shells, removing the need for a separate enteric coating step. The approach reduces process steps and limits heat and moisture exposure, which supports stability for sensitive ingredients such as probiotics and omega-3 oils. Capacity expansion across Asia and Europe improves lead times for these coating-free formats and increases supply responsiveness for high-volume supplement programs. In parallel, developers advance plant-based enteric softgels for vegan positioning, and multi-chamber architectures that separate incompatible fills to enable combination regimens for metabolic and digestive health.

Regulatory and quality requirements shape both cost and time to market. Manufacturers operate under cGMP expectations and tighter scrutiny of supplement substantiation and labeling, alongside more stringent microbiological specifications for live microbial products. These controls expand validation requirements for pH-responsive polymers, hybrid gelatin-pectin matrices, and complex designs that must deliver consistent dissolution in the intestine. Risk concentrates in raw material volatility for gelatin and specialty polymers, stability losses in humid supply chains, and batch failures driven by dissolution variability or microbial limits. Technology offsets part of this exposure. Producers deploy automation in shell preparation, in-line viscosity and moisture control, and high-speed inspection, while AI-assisted formulation screening and digital batch records improve process control and shorten development cycles. Europe remains a high-compliance market at an estimated ~27% of 2024 revenue, while Asia-Pacific posts the fastest growth, with investment clustering in China, India, and Southeast Asia as export-oriented CDMOs scale enteric formats for probiotics, enzymes, and “burp-reduced” omega-3 portfolios.

, By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-User (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market generates 2.8 billion USD, 2024 and reaches 4.0 billion USD, 2034, at 3.6%, 2026-2034.

- Segment Dominance: Gelatin (Type-A & Type-B) leads the product mix at 58.6%, 2024.

- Segment Dominance: Health supplements lead applications at 42.4%, 2024.

- Driver: Pharmaceutical companies drive demand through scale adoption at 47.8%, 2024.

- Restraint: Regulatory and compliance costs constrain expansion at estimated: 0.3 billion USD, 2024.

- Opportunity: Alternative materials beyond gelatin expand growth potential at estimated: 0.5 billion USD, 2034.

- Trend: Portfolio shifts toward non-gelatin formats accelerate at estimated: 18.0%, 2024.

- Regional Analysis: North America leads with 41.9%, 2024.

By Type

Gelatin based enteric softgel capsules continue to anchor the market structure in 2025, with Type A and Type B gelatin together accounting for about 58.6 percent of total product demand in the latest measured year. Manufacturers favor gelatin for its consistent film formation, predictable dissolution at intestinal pH levels, and compatibility with high speed rotary die equipment. These attributes allow precise shell thickness control, which improves resistance to gastric acid and supports repeatable delayed release performance at scale.

Pharmaceutical grade gelatin also enables secure encapsulation of oils and semi solid fills without leakage. Longstanding regulatory familiarity shortens approval timelines for reformulated and line extension products. Cost efficiency relative to synthetic polymers reinforces its position across prescription and non-prescription categories. Global sourcing from bovine and porcine inputs sustains supply continuity, while ongoing refinement in purity and cross linking control reduces variability risk and enhances batch consistency.

Alternative materials, including fish bone gelatin, starch based systems, and cellulose derivatives, are gaining attention as niche solutions. These formats address dietary restrictions, allergen concerns, and specific stability requirements. Adoption remains lower than gelatin but is expanding in premium and specialty portfolios where differentiated positioning offsets higher production costs.

By Application

Health supplements remain the largest application segment, representing approximately 42.4 percent of market demand in 2024 and maintaining momentum into 2025. Enteric softgels protect probiotics, enzymes, omega fatty acids, and botanical extracts from gastric degradation, improving intestinal absorption and consumer tolerance. Brands use delayed release positioning to justify premium pricing and strengthen differentiation in crowded supplement categories.

Demand benefits from rising focus on digestive health, preventive nutrition, and aging populations with daily supplementation routines. Enteric formats reduce gastrointestinal discomfort and taste issues, which supports compliance and repeat purchases. Digital retail channels and specialty nutrition stores amplify reach, while clinical substantiation of absorption claims strengthens credibility.

Pharmaceutical applications such as anti-inflammatory, antibiotic, and antibacterial therapies also contribute steady volumes. Enteric softgels reduce gastric irritation and improve therapeutic consistency, particularly for chronic use products. Combined formulations with targeted release profiles continue to expand across both supplement and drug portfolios.

By End-Use

Pharmaceutical companies account for the largest end-use share at roughly 47.8 percent, reflecting strong reliance on enteric softgels for acid sensitive active ingredients. These dosage forms enable intestinal release, which improves efficacy and reduces adverse gastric effects. Developers also use enteric softgels to reformulate mature drugs, extending lifecycle value and supporting differentiation in competitive therapy areas.

Rising emphasis on patient adherence drives selection of smooth, easy to swallow capsules. Well established quality systems and regulatory pathways align closely with gelatin based enteric softgel production. Contract development and manufacturing organizations play a central role, allowing faster scale up and global distribution.

Nutraceutical, cosmeceutical, and food industry users represent a growing secondary base. These sectors apply enteric softgels to functional ingredients and beauty from within products where stability and sensory acceptance remain critical.

By Region

North America remains the leading regional market with about 41.9 percent share in 2024, supported by strong supplement consumption, high prescription volumes, and advanced manufacturing capacity. Demand centers on digestive health supplements, omega-3 products, and non-steroidal anti-inflammatory drugs. Regulatory emphasis on bioavailability and safety continues to favor enteric delivery systems. In 2024, the U.S. Food and Drug Administration approved 50 new drugs, several of which relied on advanced oral capsule technologies.

Europe follows with stable growth driven by compliance focused pharmaceutical production and premium nutraceutical brands. Asia Pacific is projected to record the highest growth rate through the forecast period, supported by expanding middle class populations, government incentives for local drug manufacturing, and rising demand for vitamins, minerals, and herbal supplements. China alone approved 83 new drugs in 2024, highlighting the region’s accelerating pharmaceutical output. Latin America and the Middle East and Africa show gradual adoption, led by urban wellness markets and improving access to regulated supplements and medicines.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Gelatin (Type-A & Type-B)

- Fish Bone Gelatin

- Starch Material

- Cellulose Derivatives

By Application

- Health Supplements

- Anti-inflammatory Drugs

- Vitamin and Dietary Supplements

- Antibiotic & Antibacterial Drugs

- Others

By End-user

- Pharmaceutical Companies

- Cosmeceutical Companies

- Nutraceutical Companies

- Food Industry

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.9 B |

| Forecast Revenue (2034) | USD 4.0 B |

| CAGR (2025-2034) | 3.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Gelatin (Type-A & Type-B), Fish Bone Gelatin, Starch Material, Cellulose Derivatives), By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-user (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Sirio Pharma, EuroCaps, Catalent Inc., Soft Gel Technologies, HealthCaps India, Procaps Group, Aenova Group, Fuji Capsule, Strides Pharma Science, Lonza Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-User (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-User (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-User (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Enteric Softgel Capsules Market?

Global Enteric Softgel Capsules Market was valued at USD 2.8 billion in 2024 and is projected to reach USD 4.0 billion by 2034, growing at a CAGR of 3.6%. Explore key trends, pharmaceutical demand, and growth opportunities.

Who are the major players in the Enteric Softgel Capsules Market?

Sirio Pharma, EuroCaps, Catalent Inc., Soft Gel Technologies, HealthCaps India, Procaps Group, Aenova Group, Fuji Capsule, Strides Pharma Science, Lonza Group

Which segments covered the Enteric Softgel Capsules Market?

By Product Type (Gelatin (Type-A & Type-B), Fish Bone Gelatin, Starch Material, Cellulose Derivatives), By Application (Health Supplements, Anti-inflammatory Drugs, Vitamin and Dietary Supplements, Antibiotic & Antibacterial Drugs, Others), By End-user (Pharmaceutical Companies, Cosmeceutical Companies, Nutraceutical Companies, Food Industry)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Enteric Softgel Capsules Market

Published Date : 10 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date