- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Enzyme Engineering Market Forecast 2034 | CAGR 10.3%

Global Enzyme Engineering Market Size, Share, Growth & Industry Analysis By Enzyme Type (Oxidoreductases, Hydrolases, Transferases, Lyases, Isomerases, Ligases), By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Biofuels, Animal Nutrition, Specialty Chemicals, Textiles), By Technology Platform (Directed Evolution, Computational Design, Rational Design) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

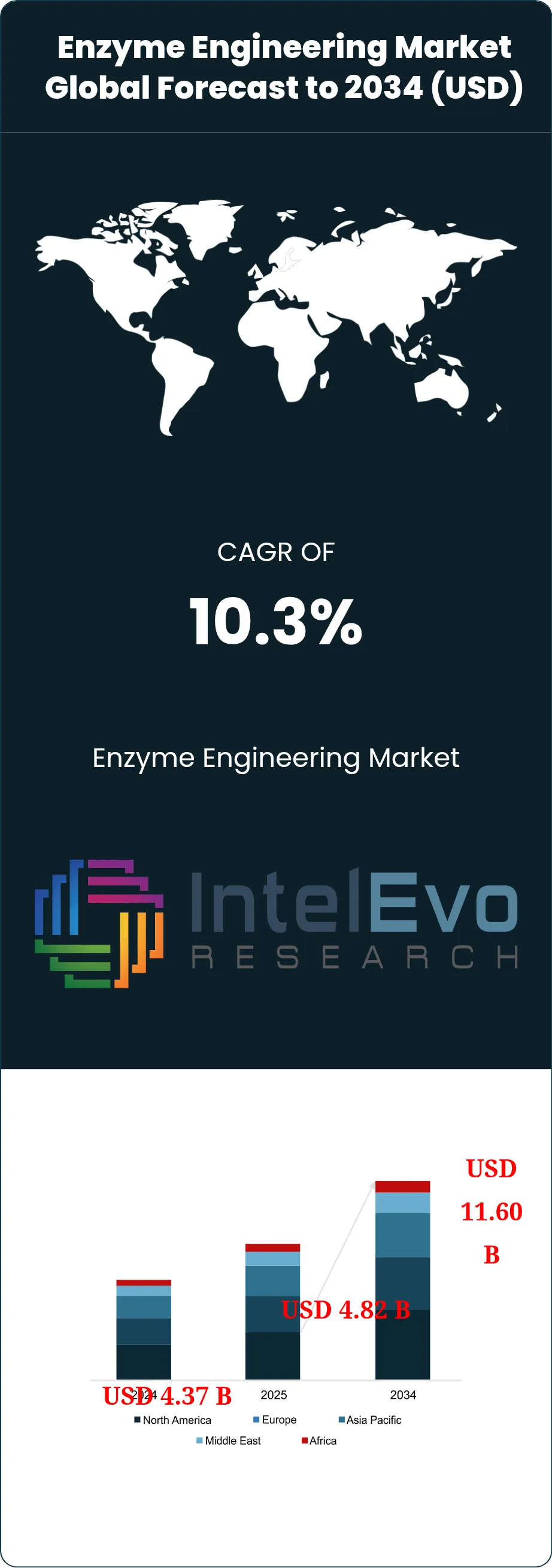

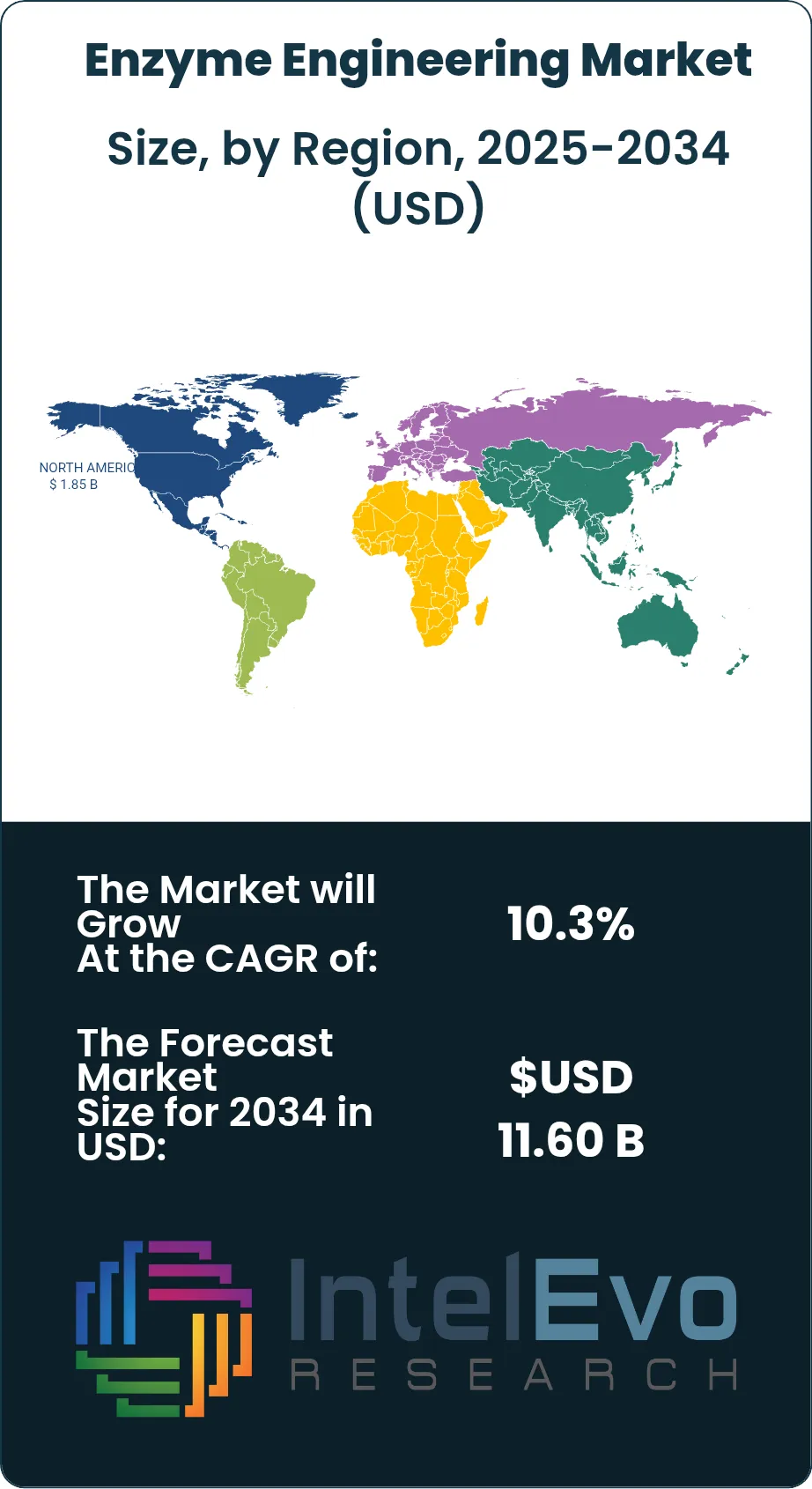

| USD 4.82 Billion | USD 11.60 Billion | 10.3% | North America, 38.4% |

The Enzyme Engineering Market was valued at approximately USD 4.37 Billion in 2024 and reached USD 4.82 Billion in 2025. The market is projected to grow to USD 11.60 Billion by 2034, expanding at a CAGR of 10.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.78 Billion over the analysis period, driven by accelerating demand across pharmaceuticals, food and beverage processing, biofuel production, and specialty chemical manufacturing.

Get More Information about this report -

Request Free Sample ReportEnzyme engineering encompasses the rational design, directed evolution, and computational optimization of enzymes to enhance catalytic efficiency, substrate specificity, thermal stability, and operational longevity. As industrial biotechnology matures, biocatalysts engineered for non-native substrates and extreme process conditions have become essential assets in sustainable manufacturing. The enzyme engineering market is gaining commercial ground as companies replace energy-intensive chemical synthesis routes with enzymatic pathways that operate at ambient temperatures and produce minimal waste byproducts.

Several macroeconomic and structural forces are reshaping the enzyme engineering market. The EU Green Deal and US Inflation Reduction Act have accelerated adoption of bio-based process chemistry, creating regulatory-driven demand for custom biocatalysts. Pharmaceutical contract manufacturers are integrating engineered enzymes into active pharmaceutical ingredient (API) synthesis, where biocatalytic steps now represent an estimated 35% of new molecular entity manufacturing workflows as of 2025. Food manufacturers are deploying lactases, lipases, and proteases engineered for pH and temperature tolerance to extend shelf life and reduce additive use, responding to clean-label consumer trends.

In the biofuel sector, thermostable cellulases and hemicellulases engineered to hydrolyze lignocellulosic feedstocks are enabling next-generation cellulosic ethanol plants to achieve conversion efficiencies above 85%, compared to 60-65% for legacy enzyme formulations. The IEA estimates that second-generation biofuels could displace 450 billion liters of fossil fuel annually by 2034, a trajectory that directly stimulates demand for high-performance enzyme engineering.

AI-guided protein engineering platforms are compressing enzyme discovery timelines from years to months. Machine learning models trained on protein structure databases now predict beneficial mutations with accuracy exceeding 70%, reducing wet-lab screening cycles by an estimated 60%. North America held the largest enzyme engineering market share at 38.4% in 2025, anchored by established synthetic biology firms, NIH-funded academic pipelines, and extensive pharmaceutical manufacturing infrastructure. Asia Pacific is the fastest-growing region, expanding at a projected CAGR of 12.1% through 2034 as Chinese and Indian bioprocessing capacity scales.

, By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Biofuels, Animal Nutrition, Specialty Chemicals, Textiles), By Technology Platform (Directed Evolution, Computational Design, Rational Design) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global enzyme engineering market was valued at USD 4.82 Billion in 2025 and is forecast to reach USD 11.60 Billion by 2034, registering a CAGR of 10.3% during 2026-2034.

- Segment Dominance: By enzyme type, the oxidoreductases segment held the largest share at 34.2% of the enzyme engineering market in 2025, driven by its central role in pharmaceutical biosynthesis and green chemistry oxidation pathways.

- Segment Dominance: By end-use industry, the pharmaceuticals and biotechnology segment accounted for 38.7% of total enzyme engineering market revenue in 2025, reflecting surging demand for enantioselective biocatalysts in API manufacturing.

- Driver: Rapid adoption of AI-assisted directed evolution platforms is accelerating enzyme optimization cycles by up to 60%, reducing development costs and enabling commercialization of previously inaccessible biocatalytic reactions.

- Restraint: High upfront R&D expenditure associated with enzyme protein engineering, averaging USD 2-8 Million per engineered enzyme project, limits participation by smaller biotechnology firms and constrains market entry rates.

- Opportunity: The expanding biosimilar and biologic manufacturing sector, projected to represent USD 580 Billion in global revenues by 2034, creates a sizeable addressable market for custom-engineered enzymes used in glycosylation, conjugation, and bioprocessing steps.

- Trend: Immobilized enzyme systems are gaining traction in continuous manufacturing, with adoption rates growing at approximately 14.8% annually in 2025, as pharmaceutical manufacturers pursue process intensification and enzyme reusability.

- Regional Analysis: North America led the enzyme engineering market with a 38.4% share, equivalent to USD 1.85 Billion in 2025, supported by dense pharmaceutical manufacturing clusters, leading synthetic biology firms, and sustained federal R&D investment.

Competitive Landscape Overview

The enzyme engineering market is moderately consolidated, with the top four players — Novozymes (Novonesis), DuPont (IFF), DSM-Firmenich, and BASF — collectively accounting for approximately 48% of global market revenue in 2025. Competition centers on proprietary protein engineering platforms, depth of industrial application portfolios, and speed of customization. M&A activity intensified between 2023 and 2025, most notably the Novozymes-Chr. Hansen merger forming Novonesis, which reinforced scale advantages in food ingredient and pharmaceutical enzyme segments. Emerging challengers such as Codexis and c-LEcta compete through best-in-class platform technology for pharmaceutical biocatalysis, attracting significant partnership interest from global API manufacturers.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Novozymes A/S | Denmark | Leader | Saphera Lactase Platform | Europe & North America | Completed merger with Chr. Hansen to form Novonesis; January 2025 integration accelerating enzyme pipeline commercialization. |

| DuPont (IFF) | USA | Leader | Danisco Enzyme Suite | North America & Europe | Launched next-generation protease series for industrial bioprocessing in Q1 2025, targeting USD 200M incremental revenue by 2027. |

| DSM-Firmenich | Netherlands | Leader | Maxilact & NIMO Enzyme Range | Europe & Asia Pacific | Established enzyme innovation hub in Singapore in March 2025 to expand Asia Pacific biocatalysis capacity. |

| BASF SE | Germany | Leader | Natuphos E Phytase | Europe & North America | Signed strategic R&D collaboration with Ginkgo Bioworks in February 2025 for AI-guided enzyme evolution platform. |

| Codexis Inc. | USA | Challenger | CodeEvolver Platform | North America | Secured USD 45M partnership with a global API manufacturer in June 2025 to engineer novel biocatalysts for pharmaceutical synthesis. |

| Amano Enzyme Inc. | Japan | Challenger | Lipase PS & Protease M | Asia Pacific | Expanded production capacity in Nagoya facility by 30% in Q2 2025 to meet rising Asian food ingredient demand. |

| Novonesis (Chr. Hansen/Novozymes JV) | Denmark | Leader | HMO Biosynthesis Enzymes | Global | Launched dedicated HMO enzyme platform for infant nutrition sector in September 2025, targeting premium biomanufacturing. |

| AB Enzymes | Germany | Niche Player | Rohalase & Rohament Range | Europe | Formed distribution partnership with Indian agrochemical firm for cellulase penetration in South Asian animal feed market, 2025. |

| Verenium (BP) | USA | Niche Player | Fuelzyme Alpha-Amylase | North America | Piloted high-temperature variant of Fuelzyme for next-gen cellulosic ethanol plants in Q3 2025. |

| c-LEcta GmbH | Germany | Niche Player | Immobilized Enzyme Platforms | Europe | Raised EUR 22M Series B in January 2026 to scale pharmaceutical-grade immobilized enzyme manufacturing. |

By Enzyme Type

The enzyme engineering market by enzyme type spans oxidoreductases, transferases, hydrolases, lyases, isomerases, and ligases, each finding distinct industrial application niches. Oxidoreductases commanded the largest share at 34.2% of the enzyme engineering market in 2025, equivalent to approximately USD 1.65 Billion. These enzymes catalyze critical oxidation-reduction reactions in pharmaceutical synthesis, specialty chemical production, and biofuel upgrading. Engineered laccases and peroxidases are replacing toxic chemical oxidants in organic synthesis, while P450 monooxygenase variants are increasingly applied to asymmetric hydroxylation of pharmaceutical precursors. The oxidoreductase segment is growing at approximately 11.1% CAGR through 2034, sustained by pharmaceutical process chemistry demand.

Hydrolases represent the second-largest enzyme type segment with a 29.8% market share in 2025. Lipases, proteases, amylases, and cellulases engineered for enhanced substrate range and stability anchor this segment. The food and beverage industry accounts for the majority of hydrolase demand, deploying engineered lactases for lactose-free dairy production, engineered proteases for meat tenderization and cheese ripening, and engineered amylases for starch liquefaction in ethanol and sweetener manufacturing. Transferases held an 18.3% share in 2025, led by glycosyltransferases used in drug conjugation and glycoprotein biomanufacturing. Lyases, isomerases, and ligases collectively accounted for approximately 17.7% of the enzyme engineering market in 2025, with growing application in biosynthetic pathway construction for specialty chemical and nutraceutical manufacturing.

By End-Use Industry

The enzyme engineering market by end-use industry reveals a clear dominance of pharmaceuticals and biotechnology, which held 38.7% of total market revenues in 2025, equivalent to USD 1.87 Billion. Biocatalytic synthesis is now embedded in the manufacturing of over 40% of new chemical entities approved by the FDA, where engineered ketoreductases, transaminases, and lipases deliver superior enantioselectivity compared to chemical asymmetric synthesis. Outsourcing of enzyme engineering work to CDMOs and specialist biocatalysis firms is also growing, with firms like Codexis capturing multi-million-dollar platform licensing agreements with top-20 pharmaceutical companies.

Food and beverage processing represented 26.4% of the enzyme engineering market in 2025. Engineering efforts focus on pH stability (for acid-stable lactases operating in yogurt fermentation), thermostability (for amylases in high-temperature starch conversion), and substrate selectivity (for lipases targeting specific fatty acid profiles in structured lipid manufacturing). The biofuel sector accounted for 14.6% of market revenue in 2025, with demand concentrated in engineered cellulase cocktails for lignocellulosic biomass conversion. Animal nutrition held an 8.9% share, driven by phytases and carbohydrases engineered to improve feed conversion ratios in poultry and swine operations. Specialty chemicals, textiles, pulp and paper, and other industries collectively represented the remaining 11.4% of the enzyme engineering market in 2025.

By Technology Platform

The enzyme engineering market by technology platform is segmented into directed evolution, rational design, semi-rational design, and computational enzyme design. Directed evolution remains the dominant methodology, representing 42.3% of the enzyme engineering market in 2025. This approach generates diverse enzyme variants through iterative rounds of random mutagenesis and high-throughput functional screening, enabling discovery of mutations that improve catalytic activity, thermostability, or organic solvent tolerance. High-throughput screening infrastructure, including robotic liquid handling and microfluidic droplet platforms, has reduced screening costs by approximately 55% over the past decade, making directed evolution accessible to mid-sized biotech firms.

Computational enzyme design, which integrates molecular dynamics simulation, machine learning-based fitness prediction, and deep learning protein structure tools such as AlphaFold derivatives, held a 22.7% technology share in 2025. Adoption is accelerating rapidly, and this sub-segment is projected to grow at a CAGR of 15.3% through 2034 as AI models become more accurate and accessible. Rational design, guided by mechanistic understanding of enzyme active sites and structure-activity relationships, held 19.8% of the enzyme engineering market in 2025 and remains the preferred approach for pharmaceutical applications requiring precise molecular specificity. Semi-rational design, which combines limited mutagenesis of selected active-site residues with high-throughput screening, represented 15.2% of the technology market in 2025 and serves as a practical middle ground for many industrial enzyme development programs.

By Application Format

The enzyme engineering market by application format covers free-enzyme formulations, immobilized enzyme systems, and whole-cell biocatalysis. Free-enzyme formulations held the largest share at 54.6% in 2025, widely adopted in food processing and pharmaceutical single-use batch operations where enzyme recovery is economically secondary. Immobilized enzyme systems, in which the engineered enzyme is covalently or physically attached to a solid carrier to enable reuse and continuous operation, accounted for 31.7% of the enzyme engineering market in 2025. These systems are growing rapidly in pharmaceutical continuous manufacturing environments where enzyme longevity directly reduces per-unit API synthesis cost. Whole-cell biocatalysis, where the host organism expresses the engineered enzyme in situ, represented 13.7% in 2025 and is favored for multi-step cascade reactions where cofactor regeneration is required intracellularly.

Regional Analysis

North America

North America accounted for 38.4% of the global enzyme engineering market in 2025, generating approximately USD 1.85 Billion in revenue. The United States is the dominant contributor, driven by a dense pharmaceutical manufacturing base, deep venture capital funding for synthetic biology startups, and sustained NIH investment in protein engineering research. The Biomanufacturing USA initiative and the National Biotechnology and Biomanufacturing Initiative have both channeled federal resources into enzyme and biocatalysis infrastructure. Canada contributes meaningfully through agricultural bioprocessing and biofuel enzyme demand, while Mexico is emerging as a food processing enzyme consumer as its agricultural export sector modernizes. The FDA's progressive stance on biocatalytic process chemistry in NDA manufacturing documentation has further encouraged pharmaceutical producers to adopt engineered enzyme workflows. The US enzyme engineering ecosystem also benefits from a concentration of world-class academic programs producing protein engineering talent at MIT, Caltech, and University of California Berkeley.

Europe

Europe held a 28.7% share of the enzyme engineering market in 2025, equivalent to USD 1.38 Billion. Denmark stands as the nerve center of the European market, home to Novonesis, the world's largest industrial enzyme company formed from the merger of Novozymes and Chr. Hansen. Germany contributes significantly through BASF's industrial biotechnology division and a cluster of specialized enzyme engineering firms including AB Enzymes and c-LEcta. The Netherlands hosts DSM-Firmenich's bioprocessing innovation centers. The EU's Chemical Strategy for Sustainability actively incentivizes replacement of hazardous chemical processes with biocatalytic alternatives, creating regulatory tailwinds for enzyme engineering adoption across specialty chemicals and agrochemicals. France and the UK each represent mature demand markets for pharmaceutical and food processing enzymes, with UK enzyme engineering activity supported by the Medicines and Healthcare products Regulatory Agency's engagement with bioprocess technology development. REACH regulation compliance is also driving enzyme-based substitution for restricted chemical substances.

Asia Pacific

Asia Pacific represented 21.4% of the global enzyme engineering market in 2025, generating approximately USD 1.03 Billion, and is the fastest-growing regional market with a projected CAGR of 12.1% through 2034. China is the largest national market in the region, where domestic enzyme producers including Sunson Industry Group are scaling up engineered enzyme production capacity for the textile, paper, and food industries. The Chinese government's 14th Five-Year Plan explicitly targets biomanufacturing as a strategic sector, allocating state funding to enzyme protein engineering research and fermentation infrastructure. Japan maintains a sophisticated enzyme engineering sector centered on Amano Enzyme and Shin Nihon Chemical, with particular strength in food-grade and pharmaceutical-grade biocatalysts. India is the region's most rapidly expanding market, where enzyme engineering companies support growing pharmaceutical API manufacturing and animal nutrition sectors. South Korea is emerging as a significant player through its biosimilar manufacturing industry, which requires engineered glycosylation enzymes and post-translational modification catalysts.

Latin America

Latin America accounted for approximately 6.8% of the enzyme engineering market in 2025, equivalent to USD 328 Million. Brazil is the dominant regional market, where sugarcane bioethanol production drives substantial demand for engineered cellulases and ligninases capable of converting agricultural residues to fermentable sugars. Brazil's Renovabio program mandates increasing renewable fuel content, directly stimulating biocatalyst demand at cellulosic ethanol facilities. Argentina represents the second-largest enzyme engineering market in Latin America, with food processing applications for engineered proteases and lipases in soybean and animal protein processing industries. Mexico serves as both a food manufacturing and pharmaceutical manufacturing base, creating dual-sector enzyme demand. The region faces infrastructure constraints including limited fermentation manufacturing capacity and reliance on imported enzyme formulations, but government incentives for domestic biotechnology capacity building are beginning to attract regional investment.

Middle East & Africa

The Middle East and Africa region held approximately 4.7% of the enzyme engineering market in 2025, generating USD 227 Million. The UAE and Saudi Arabia represent the primary demand centers in the Middle East, where diversification strategies under Vision 2030 and UAE National Innovation Strategy are driving investment in biotechnology and industrial fermentation. Saudi Aramco's downstream diversification includes exploration of biocatalytic upgrading of petrochemical streams. South Africa leads the African enzyme engineering market, with enzyme applications in food processing, mining bioleaching, and paper manufacturing. The region's pharmaceutical manufacturing base is expanding under the African Continental Free Trade Agreement, creating longer-term demand for pharmaceutical-grade engineered enzymes. Infrastructure gaps and limited domestic enzyme manufacturing capacity represent near-term constraints, but increasing technology transfer arrangements with European and Asian enzyme producers are beginning to address these barriers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Enzyme Type

- Oxidoreductases

- Hydrolases

- Transferases

- Lyases

- Isomerases

- Ligases

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Food & Beverage Processing

- Biofuels & Renewable Energy

- Animal Nutrition

- Specialty Chemicals

- Textiles, Pulp & Paper

- Others

By Technology Platform

- Directed Evolution

- Computational Enzyme Design

- Rational Design

- Semi-Rational Design

By Application Format

- Free-Enzyme Formulations

- Immobilized Enzyme Systems

- Whole-Cell Biocatalysis

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.82 B |

| Forecast Revenue (2034) | USD 11.60 B |

| CAGR (2025-2034) | 10.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Enzyme Type, (Oxidoreductases, Hydrolases, Transferases, Lyases, Isomerases, Ligases), By End-Use Industry, (Pharmaceuticals & Biotechnology, Food & Beverage Processing, Biofuels & Renewable Energy, Animal Nutrition, Specialty Chemicals, Textiles, Pulp & Paper, Others), By Technology Platform, (Directed Evolution, Computational Enzyme Design, Rational Design, Semi-Rational Design), By Application Format, (Free-Enzyme Formulations, Immobilized Enzyme Systems, Whole-Cell Biocatalysis) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVOZYMES A/S (NOVONESIS), DUPONT (IFF) - DANISCO ENZYMES, DSM-FIRMENICH, BASF SE, CODEXIS INC., AMANO ENZYME INC., AB ENZYMES, VERENIUM (BP BIOFUELS), C-LECTA GMBH, ENZYME DEVELOPMENT CORPORATION, ADVANCED ENZYME TECHNOLOGIES LTD., BIOCATALYSTS LTD., ENMEX S.A. DE C.V., SHIN NIHON CHEMICAL CO., DIREVO INDUSTRIAL BIOTECHNOLOGY GMBH, SUNSON INDUSTRY GROUP CO., LTD., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Biofuels, Animal Nutrition, Specialty Chemicals, Textiles), By Technology Platform (Directed Evolution, Computational Design, Rational Design) Industry Trends & Forecast 2026–2034")

, By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Biofuels, Animal Nutrition, Specialty Chemicals, Textiles), By Technology Platform (Directed Evolution, Computational Design, Rational Design) Industry Trends & Forecast 2026–2034")

, By End-Use Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Biofuels, Animal Nutrition, Specialty Chemicals, Textiles), By Technology Platform (Directed Evolution, Computational Design, Rational Design) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Enzyme Engineering Market?

Global Enzyme engineering market valued at USD 4.37B in 2024, reaching USD 11.6B by 2034, growing at a CAGR of 10.3% from 2026–2034.

Who are the major players in the Enzyme Engineering Market?

NOVOZYMES A/S (NOVONESIS), DUPONT (IFF) - DANISCO ENZYMES, DSM-FIRMENICH, BASF SE, CODEXIS INC., AMANO ENZYME INC., AB ENZYMES, VERENIUM (BP BIOFUELS), C-LECTA GMBH, ENZYME DEVELOPMENT CORPORATION, ADVANCED ENZYME TECHNOLOGIES LTD., BIOCATALYSTS LTD., ENMEX S.A. DE C.V., SHIN NIHON CHEMICAL CO., DIREVO INDUSTRIAL BIOTECHNOLOGY GMBH, SUNSON INDUSTRY GROUP CO., LTD., OTHERS

Which segments covered the Enzyme Engineering Market?

By Enzyme Type, (Oxidoreductases, Hydrolases, Transferases, Lyases, Isomerases, Ligases), By End-Use Industry, (Pharmaceuticals & Biotechnology, Food & Beverage Processing, Biofuels & Renewable Energy, Animal Nutrition, Specialty Chemicals, Textiles, Pulp & Paper, Others), By Technology Platform, (Directed Evolution, Computational Enzyme Design, Rational Design, Semi-Rational Design), By Application Format, (Free-Enzyme Formulations, Immobilized Enzyme Systems, Whole-Cell Biocatalysis)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date