- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Europe CAR-T Cell Therapy Market Forecast 2034 | CAGR 17.2%

Europe CAR-T Cell Therapy Market Size, Share, Growth & Industry Analysis By Product Type (Autologous CAR-T Therapies, Allogeneic Off-the-Shelf CAR-T Therapies), By Therapeutic Indication (DLBCL, Multiple Myeloma, B-Cell ALL, Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours), By End-User (Academic Medical Centres, Private Oncology Hospitals, Specialised Clinics), By Antigen Target (CD19, BCMA, CD22, Multi-Antigen) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Country (2025) |

| USD 1.24 Billion | USD 5.18 Billion | 17.2% | Germany, 22.6% |

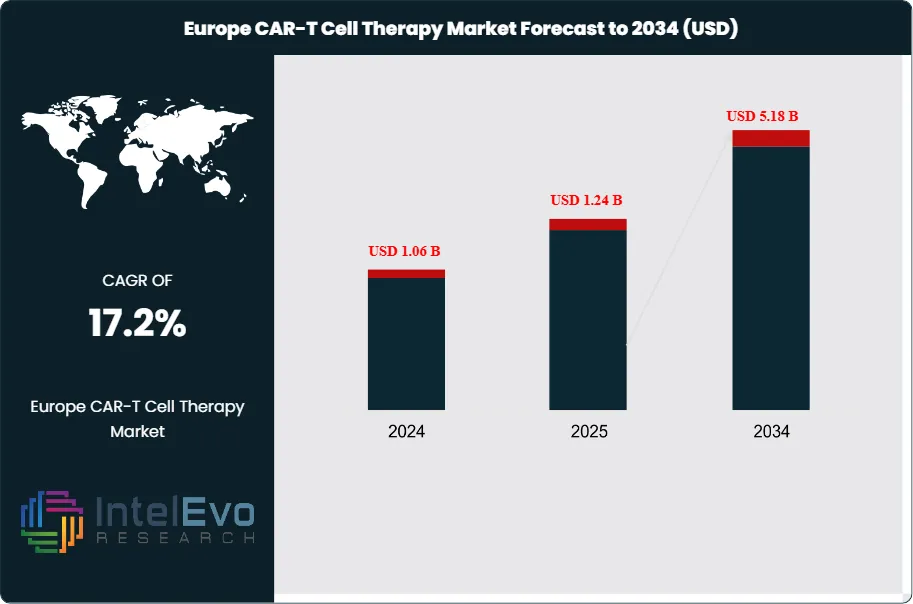

The Europe CAR-T Cell Therapy Market was valued at approximately USD 1.06 Billion in 2024 and reached USD 1.24 Billion in 2025. The market is projected to grow to USD 5.18 Billion by 2034, expanding at a CAGR of 17.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.94 Billion over the analysis period, reflecting accelerating clinical adoption, expanding reimbursement frameworks, and a rapidly maturing manufacturing infrastructure for chimeric antigen receptor T-cell therapies across the continent.

Get More Information about this report -

Request Free Sample ReportThe Europe CAR-T cell therapy market encompasses commercially approved autologous and allogeneic CAR-T products, the clinical trial pipeline across all development stages, and the ancillary manufacturing and logistics services that support therapy delivery. Four CAR-T products held EMA marketing authorisation in 2025: Kymriah, Yescarta, Breyanzi, and Carvykti, with Autolus Therapeutics' obecabtagene autoleucel receiving conditional marketing authorisation in late 2025. The approved products collectively generated USD 1.24 Billion across European markets in 2025, with haematological oncology representing 94.8% of all commercial revenue. Germany led national market performance with a 22.6% share, driven by the highest density of EMA-authorised CAR-T treatment centres of any EU member state and a statutory health insurance framework that has embedded outcomes-based payment models for advanced therapy medicinal products (ATMPs).

Regulatory architecture is a primary force in shaping the European CAR-T cell therapy market. The EMA Committee for Advanced Therapies (CAT) operates a dedicated ATMP review pathway that granted four commercial authorisations between 2018 and 2025 and has 11 additional CAR-T applications in active review as of 2025. The Hospital Exemption clause under Regulation (EC) No 1394/2007 allows EU member states to authorise hospital-manufactured CAR-T products outside the centralised EMA process, a pathway that activated at least 28 academic programmes in Germany, France, Spain, Italy, and the Netherlands by 2025. These hospital programmes represent a parallel supply channel that adds approximately 12% to 15% to effective market volumes not captured in commercial product revenue figures.

Manufacturing capacity constraints eased between 2023 and 2025 as Novartis, Kite Pharma, and BMS expanded their European vector production and cell processing facilities, reducing median vein-to-vein time for autologous products from 32 days in 2021 to 21 days in 2025. The transition to decentralised and automated manufacturing, supported by platforms such as Miltenyi Biotec's CliniMACS Prodigy, is compressing production costs and enabling smaller academic medical centres to qualify as authorised treatment sites. Allogeneic CAR-T therapies, which eliminate patient-specific manufacturing, are projected to capture an 18.5% share of European commercial revenue by 2034, introducing a fundamentally different cost and logistics profile that will attract new entrants and intensify competition from 2027 onward.

, By Therapeutic Indication (DLBCL, Multiple Myeloma, B-Cell ALL, Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours), By End-User (Academic Medical Centres, Private Oncology Hospitals, Specialised Clinics), By Antigen Target (CD19, BCMA, CD22, Multi-Antigen) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Europe CAR-T cell therapy market was valued at USD 1.24 Billion in 2025 and is forecast to reach USD 5.18 Billion by 2034, at a CAGR of 17.2% during the 2026–2034 forecast period.

- Segment Dominance: Autologous CAR-T therapies held an 81.5% product-type share in 2025, generating USD 1.01 Billion in revenue, driven by four commercially approved products from Novartis, Kite, BMS, and Janssen.

- Segment Dominance: Diffuse large B-cell lymphoma (DLBCL) was the leading indication segment at 42.3% of European CAR-T revenue in 2025, representing USD 0.52 Billion, underpinned by Yescarta and Breyanzi second-line approvals.

- Driver: Expanding reimbursement coverage across EU member states drove a 38% increase in patient access to approved CAR-T therapies between 2022 and 2025, adding an estimated USD 320 Million to annual market revenue.

- Restraint: Per-treatment costs averaging USD 370,000 to USD 430,000 for approved autologous products in 2025 limit accessible patient populations and are the primary barrier cited in 67% of payer reimbursement negotiations across EU member states.

- Opportunity: Allogeneic CAR-T therapies represent an addressable European market opportunity of USD 820 Million by 2034, with at least six allogeneic products expected to enter commercial readiness between 2027 and 2030.

- Trend: Automated and decentralised CAR-T manufacturing adoption reached 31.4% of European authorised treatment centres in 2025, reducing average vein-to-vein time by 34% versus manual batch processes.

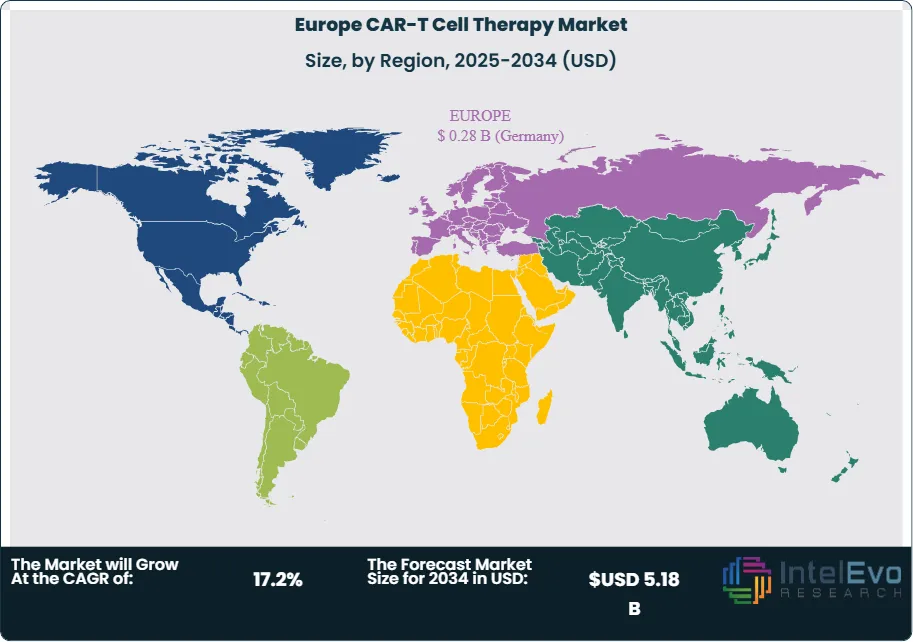

- Regional Analysis: Germany led the Europe CAR-T cell therapy market with a 22.6% share in 2025, generating USD 0.28 Billion, supported by IQWIG outcomes assessment frameworks and statutory insurer outcomes-based contracting mechanisms.

Competitive Landscape Overview

The Europe CAR-T cell therapy market is highly consolidated among approved commercial product holders, with Novartis, Kite Pharma (Gilead), Bristol Myers Squibb, and Janssen (J&J) collectively commanding approximately 89% of commercial revenue in 2025. Competition is principally technology-driven and regulatory-access-driven, centred on EMA authorisation breadth, payer reimbursement agreements, and authorised treatment centre network size. Competitive intensity is accelerating as Autolus Therapeutics and allogeneic-platform companies including Cellectis and Celyad Oncology enter the commercial phase, adding three to five new competitive entrants by 2028.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Novartis | Switzerland | Leader | Kymriah (tisagenlecleucel) | Pan-European | Received EMA label expansion for Kymriah in follicular lymphoma; launched EU outcomes-based payment framework (Feb 2025) |

| Kite Pharma (Gilead) | USA | Leader | Yescarta (axicabtagene ciloleucel) | Germany, France, UK | Launched Tecartus REMS programme across 8 EU markets and expanded authorised treatment centre network by 34% (Apr 2025) |

| Bristol Myers Squibb | USA | Leader | Breyanzi (lisocabtagene maraleucel) | UK, Germany, Netherlands | Completed EMA submission for Breyanzi in chronic lymphocytic leukaemia; partnered with Lonza Basel for EU vein-to-vein expansion (Jan 2026) |

| Janssen (J&J) | Belgium | Challenger | Carvykti (ciltacabtagene autoleucel) | Spain, Italy, Germany | Secured EUR 210M reimbursement agreements across 5 EU member states for Carvykti in myeloma (Sep 2025) |

| Autolus Therapeutics | UK | Challenger | Obecabtagene Autoleucel (obe-cel) | UK, Germany | EMA conditional marketing authorisation granted for obe-cel in adult ALL; raised USD 150M to scale UK manufacturing (Nov 2025) |

| Celyad Oncology | Belgium | Niche Player | CYAD-101 (allogeneic NKG2D) | Belgium, Netherlands | Presented Phase I data for CYAD-211 at ASH 2025; partnership with UCB for combination immunotherapy (Jun 2025) |

| Cellectis | France | Niche Player | UCART19, UCART22 (allogeneic) | France | Completed USD 60M Series C to fund EU allogeneic CAR-T manufacturing scale-up (Mar 2025) |

| Miltenyi Biotec | Germany | Niche Player | CliniMACS Prodigy (mfg platform) | Germany, Austria | Launched ProdigyPlus automated CAR-T manufacturing system; signed 5 CDO agreements with EU academic centres (Aug 2025) |

By Product Type

Autologous CAR-T therapies dominate the Europe CAR-T cell therapy market, holding an 81.5% product-type share in 2025 and generating USD 1.01 Billion in revenue. Autologous therapies use the patient's own T-cells, extracted via leukapheresis, genetically engineered ex vivo to express a chimeric antigen receptor, and reinfused following lymphodepletion conditioning. This patient-specific manufacturing process is the commercial standard for the four EMA-approved products and delivers complete response rates of 40% to 70% across the approved indications, which include relapsed or refractory DLBCL, follicular lymphoma, mantle cell lymphoma, B-cell ALL, and multiple myeloma. The segment faces cost and manufacturing time constraints, but remains the dominant revenue source through 2034 given the depth of clinical evidence and the established ATMP reimbursement frameworks across Germany, France, the UK, and Spain. Autologous product revenue is projected to reach USD 4.22 Billion by 2034 as label expansions into earlier therapy lines, additional lymphoma subtypes, and solid tumour indications broaden the addressable patient population.

Allogeneic CAR-T therapies held an 18.5% share in 2025, representing USD 0.23 Billion in revenue, a figure driven primarily by compassionate access programmes and hospital exemption manufacturing rather than commercially approved allogeneic products. Allogeneic therapies use T-cells from healthy donors, manufactured in centralised batches that can be stored and shipped off-the-shelf, eliminating the patient-specific manufacturing cycle. This structural advantage reduces vein-to-vein time from 21 days (autologous average) to fewer than 72 hours and opens a cost-reduction pathway estimated at 40% to 60% per treatment relative to autologous products at commercial manufacturing scale. European allogeneic development is led by Cellectis, Celyad Oncology, and international entrants including Precision BioSciences, with the first EU commercial allogeneic approvals anticipated between 2027 and 2029. The allogeneic segment is projected to grow at 26.4% CAGR through 2034, outpacing the overall market growth rate by more than nine percentage points.

By Therapeutic Indication

Diffuse large B-cell lymphoma (DLBCL) represented the leading therapeutic indication segment of the Europe CAR-T cell therapy market at 42.3% of revenue and USD 0.52 Billion in 2025. DLBCL was the first indication granted EMA authorisation for CAR-T therapy and benefits from the broadest treatment centre infrastructure, the most extensive real-world evidence dataset, and outcomes-based reimbursement models in Germany, France, and the UK. Second-line approvals for both Yescarta and Breyanzi, secured in 2022 and 2023 respectively, expanded the eligible patient population by approximately 2.4-fold versus third-line-only authorisations, directly driving revenue growth between 2023 and 2025. Multiple myeloma held a 24.7% share in 2025, generating USD 0.31 Billion, anchored by Carvykti's commercial expansion across Spain, Italy, and Germany following favourable CHMP opinion. B-cell acute lymphoblastic leukaemia (ALL) in paediatric and young adult populations contributed 14.8% of revenue, supported by Kymriah's longstanding approval and NHS England commissioning. Follicular lymphoma, mantle cell lymphoma, and emerging solid tumour programmes accounted for the remaining 18.2%, with this diversification segment projected to capture 24.5% of European market revenue by 2034 as label expansion programmes mature.

By End-User

Academic medical centres and university hospitals constituted the dominant end-user segment of the Europe CAR-T cell therapy market, commanding a 68.4% share in 2025 and generating USD 0.85 Billion. These institutions hold the majority of EMA-authorised treatment centre certifications, maintain the multidisciplinary haemato-oncology infrastructure required for CAR-T patient management, and operate the hospital exemption manufacturing programmes that produce academic CAR-T constructs outside the commercial approval pathway. Germany's university hospital network, comprising 22 EMA-certified CAR-T treatment centres as of 2025, handled an estimated 31% of total European commercial CAR-T patient treatments. Private oncology hospital networks held a 21.8% share in 2025, a proportion expanding as reimbursement clarity improves and commercial operators such as Quironsalud in Spain and Humanitas in Italy qualify additional sites. Outpatient and specialised oncology clinic settings accounted for 9.8%, a nascent but growing channel enabled by improved toxicity management protocols that reduce mandatory inpatient monitoring from 14 days to 7 days under revised EBMT guidelines published in 2024.

Regional Analysis

The Europe CAR-T cell therapy market is a geographically complex market segmented by national reimbursement decisions, treatment centre certification status, and country-level payer willingness-to-pay frameworks rather than broad regional dynamics.

| Country/Sub-Region | Share (2025) | Revenue (USD B) | Key Demand Driver |

| Germany | 22.6% | 0.28 | Highest ATMP-approved treatment centre density in Europe |

| France | 18.4% | 0.23 | ATU/AAP compassionate access schemes; CAR-T national plan |

| United Kingdom | 17.2% | 0.21 | NHS England CAR-T commissioning; MHRA post-Brexit approvals |

| Spain | 12.1% | 0.15 | RedCAR national network; increasing public reimbursement |

| Italy | 10.8% | 0.13 | AIFA regulatory acceleration; academic hospital programmes |

| Rest of Europe | 18.9% | 0.24 | Benelux, Nordics, CEE expanding authorised centre networks |

Germany

Germany led the Europe CAR-T cell therapy market with a 22.6% share and USD 0.28 Billion in revenue in 2025. The German statutory health insurance system processes CAR-T reimbursement through the NUB (neue Untersuchungs- und Behandlungsmethoden) mechanism, which granted interim reimbursement to Kymriah, Yescarta, Breyanzi, and Carvykti under NUB Status 1 designations, enabling immediate hospital cost recovery while formal IQWIG assessments proceed. The country's 22 EMA-authorised treatment centres span major academic networks including Charite Berlin, University Hospital Frankfurt, and LMU Munich, providing geographic coverage that served an estimated 680 commercial CAR-T patients in 2025. Germany also hosts the largest concentration of CAR-T manufacturing infrastructure in Europe, with Miltenyi Biotec and multiple academic GMP facilities providing domestic vector production and cell processing capacity. The German government's ATMP Action Plan, published in 2024, commits EUR 180 Million in funding for ATMP manufacturing scale-up and clinical research through 2028, reinforcing Germany's position as the continental reference market.

France

France held an 18.4% share of the Europe CAR-T cell therapy market in 2025, generating USD 0.23 Billion. The French market operates through the Autorisation Temporaire d'Utilisation (ATU), succeeded by the Accès Précoce (AAP) mechanism since 2021, which provides reimbursed early access to CAR-T therapies before formal HAS assessment completion, accelerating commercial uptake relative to EU peers. France's national CAR-T programme, coordinated through the Institut National du Cancer (INCa), designated 26 authorised treatment centres and established a national patient registry that generated real-world evidence supporting formulary listing decisions. The country treated an estimated 540 commercial CAR-T patients in 2025, a number expected to grow at 19.4% annually through 2034 as second-line indications and new product approvals expand the eligible pool. French academic institutions including Hôpital Saint-Louis and CHU Bordeaux operate hospital exemption CAR-T manufacturing programmes, accounting for an additional 80 to 100 academic CAR-T administrations annually that supplement commercial product volumes.

United Kingdom

The UK accounted for a 17.2% share of the Europe CAR-T cell therapy market in 2025 with USD 0.21 Billion in revenue, operating as a distinct regulatory and reimbursement market since Brexit. The MHRA independently reviewed and authorised Kymriah, Yescarta, Breyanzi, and Carvykti under UK procedures, while NHS England commissions CAR-T therapies through a centralised Cancer Drugs Fund mechanism that applies strict cost-effectiveness thresholds evaluated by NICE. NHS England authorised 14 CAR-T treatment centres across England, Scotland, and Wales in 2025, treating approximately 420 patients with commercially approved products. The UK's Cell and Gene Therapy Catapult, a government-backed manufacturing and innovation centre in Stevenage, supports domestic autologous and allogeneic manufacturing scale-up and houses GMP production facilities for academic and early commercial-stage programmes. Autolus Therapeutics' obe-cel approval by MHRA in 2025 added the first UK-headquartered commercial CAR-T product to the national formulary, representing a significant milestone in domestic biotech commercialisation.

Spain and Italy

Spain held a 12.1% share and Italy a 10.8% share of the Europe CAR-T cell therapy market in 2025, generating USD 0.15 Billion and USD 0.13 Billion respectively. Spain operates the RedCAR national CAR-T network, a collaboration of 22 haematology centres coordinated under the Spanish Society of Haematology (SEHH) with standardised patient management protocols and centralised data collection. The Spanish Agency of Medicines and Medical Devices (AEMPS) operates a compassionate use programme that provided access to Carvykti and obe-cel ahead of national formulary decisions, driving above-average early adoption. Italy's AIFA (Agenzia Italiana del Farmaco) completed reimbursement negotiations for all four approved CAR-T products by mid-2025, with treatments channelled through 18 certified haemato-oncology centres. Italy's hospital exemption manufacturing at centres including San Raffaele in Milan and Istituto Nazionale Tumori contributed an estimated 60 academic CAR-T administrations annually in 2025.

Rest of Europe

The Rest of Europe segment, encompassing the Benelux countries, the Nordic region, Austria, Switzerland, and Central and Eastern Europe, collectively held an 18.9% share in 2025 and generated USD 0.24 Billion. The Netherlands, Belgium, and Switzerland are the most advanced markets within this grouping, each hosting two to five EMA-certified treatment centres and national reimbursement decisions for at least three approved CAR-T products by 2025. The Nordic markets (Sweden, Denmark, Norway) present high per-patient treatment cost acceptance but limited eligible patient volumes given smaller total population bases, translating to moderate absolute revenue contribution. Central and Eastern European markets, including Poland, the Czech Republic, and Hungary, are at earlier access stages; reimbursement negotiations for first CAR-T products were underway in Poland and Czechia in 2025, with commercial access expected to open for at least two products in these markets before 2027. This sub-region represents an estimated USD 160 Million incremental revenue opportunity through 2034 as CEE health system ATMP reimbursement frameworks mature.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Autologous CAR-T Therapies

- Allogeneic (Off-the-Shelf) CAR-T Therapies

By Therapeutic Indication

- Diffuse Large B-Cell Lymphoma (DLBCL)

- Multiple Myeloma

- B-Cell Acute Lymphoblastic Leukaemia (ALL)

- Follicular Lymphoma

- Mantle Cell Lymphoma

- Solid Tumours (Investigational)

By End-User

- Academic Medical Centres & University Hospitals

- Private Oncology Hospital Networks

- Outpatient Oncology & Specialised Clinics

By Antigen Target

- CD19-Targeted CAR-T

- BCMA-Targeted CAR-T

- CD22-Targeted CAR-T

- Other/Multi-Antigen Targeted

Regional Analysis and Coverage

- Germany:

- France:

- United Kingdom:

- Spain:

- Italy:

- Rest of Europe:

| Report Attribute | Details |

| Market size (2025) | USD 1.24 B |

| Forecast Revenue (2034) | USD 5.18 B |

| CAGR (2025-2034) | 17.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Autologous CAR-T Therapies, Allogeneic (Off-the-Shelf) CAR-T Therapies), By Therapeutic Indication, (Diffuse Large B-Cell Lymphoma (DLBCL), Multiple Myeloma, B-Cell Acute Lymphoblastic Leukaemia (ALL), Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours (Investigational)), By End-User, (Academic Medical Centres & University Hospitals, Private Oncology Hospital Networks, Outpatient Oncology & Specialised Clinics), By Antigen Target, (CD19-Targeted CAR-T, BCMA-Targeted CAR-T, CD22-Targeted CAR-T, Other/Multi-Antigen Targeted) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVARTIS AG, KITE PHARMA (GILEAD SCIENCES), BRISTOL MYERS SQUIBB, JANSSEN (JOHNSON & JOHNSON), AUTOLUS THERAPEUTICS, CELYAD ONCOLOGY, CELLECTIS SA, MILTENYI BIOTEC, ALLOGENE THERAPEUTICS, PRECISION BIOSCIENCES, TMUNITY THERAPEUTICS, IOVANCE BIOTHERAPEUTICS, ORI BIOTECH, LONZA GROUP (CDMO), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Therapeutic Indication (DLBCL, Multiple Myeloma, B-Cell ALL, Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours), By End-User (Academic Medical Centres, Private Oncology Hospitals, Specialised Clinics), By Antigen Target (CD19, BCMA, CD22, Multi-Antigen) Industry Trends & Forecast 2026–2034")

, By Therapeutic Indication (DLBCL, Multiple Myeloma, B-Cell ALL, Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours), By End-User (Academic Medical Centres, Private Oncology Hospitals, Specialised Clinics), By Antigen Target (CD19, BCMA, CD22, Multi-Antigen) Industry Trends & Forecast 2026–2034")

, By Therapeutic Indication (DLBCL, Multiple Myeloma, B-Cell ALL, Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours), By End-User (Academic Medical Centres, Private Oncology Hospitals, Specialised Clinics), By Antigen Target (CD19, BCMA, CD22, Multi-Antigen) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Europe CAR-T Cell Therapy Market?

Europe CAR-T cell therapy market valued at USD 1.06B in 2024, reaching USD 5.18B by 2034, growing at a CAGR of 17.2% from 2026–2034.

Who are the major players in the Europe CAR-T Cell Therapy Market?

NOVARTIS AG, KITE PHARMA (GILEAD SCIENCES), BRISTOL MYERS SQUIBB, JANSSEN (JOHNSON & JOHNSON), AUTOLUS THERAPEUTICS, CELYAD ONCOLOGY, CELLECTIS SA, MILTENYI BIOTEC, ALLOGENE THERAPEUTICS, PRECISION BIOSCIENCES, TMUNITY THERAPEUTICS, IOVANCE BIOTHERAPEUTICS, ORI BIOTECH, LONZA GROUP (CDMO), OTHERS

Which segments covered the Europe CAR-T Cell Therapy Market?

By Product Type, (Autologous CAR-T Therapies, Allogeneic (Off-the-Shelf) CAR-T Therapies), By Therapeutic Indication, (Diffuse Large B-Cell Lymphoma (DLBCL), Multiple Myeloma, B-Cell Acute Lymphoblastic Leukaemia (ALL), Follicular Lymphoma, Mantle Cell Lymphoma, Solid Tumours (Investigational)), By End-User, (Academic Medical Centres & University Hospitals, Private Oncology Hospital Networks, Outpatient Oncology & Specialised Clinics), By Antigen Target, (CD19-Targeted CAR-T, BCMA-Targeted CAR-T, CD22-Targeted CAR-T, Other/Multi-Antigen Targeted)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Europe CAR-T Cell Therapy Market

Published Date : 14 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date