- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global EV Battery Recycling Market Size, Share & Forecast | CAGR 20.2%

Global EV Battery Recycling Market Size, Share, Growth Analysis By Recycling Process (Hydrometallurgical Processing, Pyrometallurgical Processing, Direct Recycling), By Battery Chemistry (NMC, LFP, NCA, LCO), By Material Recovered (Lithium, Cobalt, Nickel, Graphite, Copper, Aluminum), By Source (Manufacturing Scrap, End-of-Life Batteries, Second-Life Repurposing), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

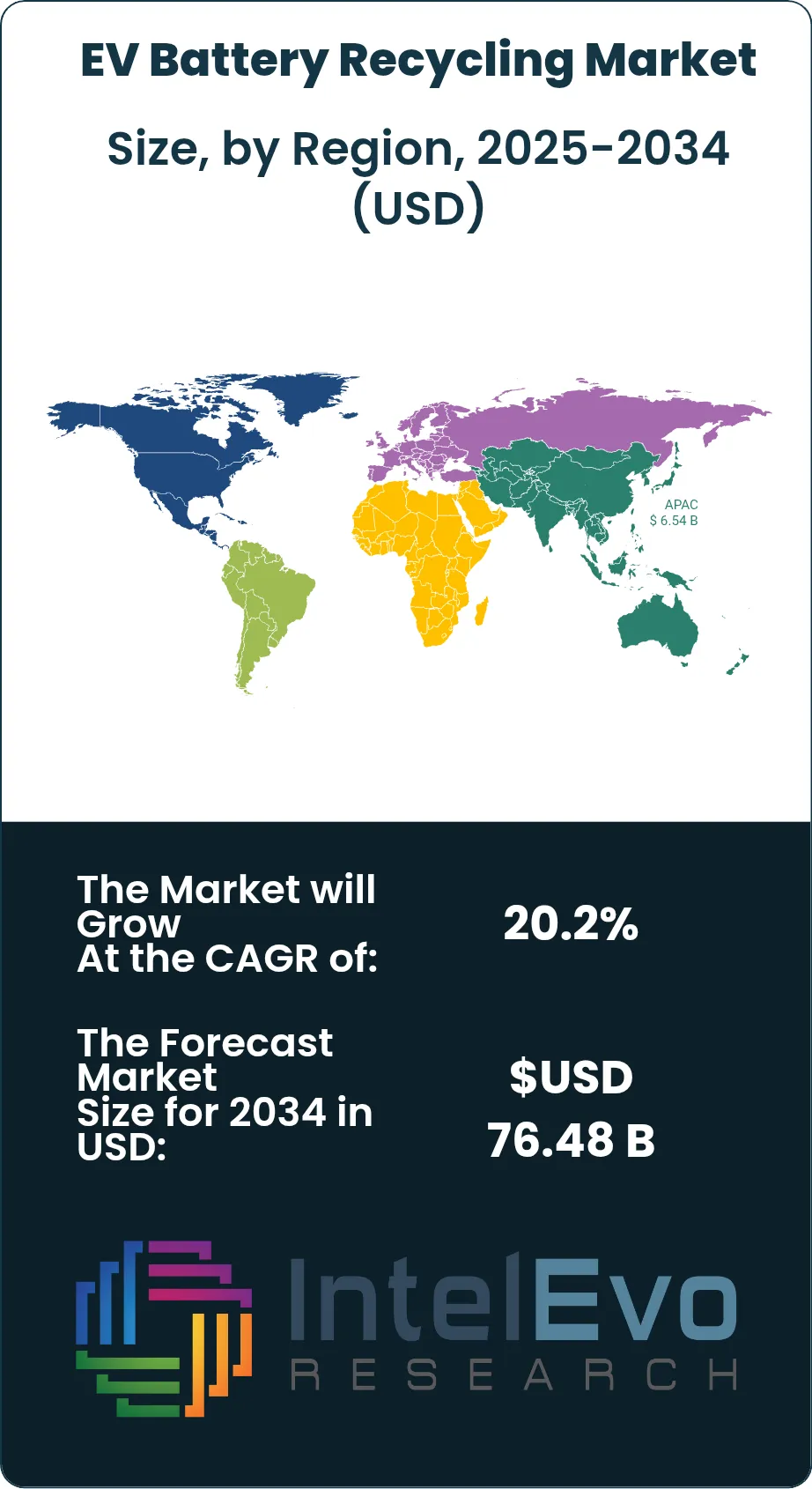

| USD 14.62 Billion | USD 76.48 Billion | 20.2% | Asia Pacific, 44.7% |

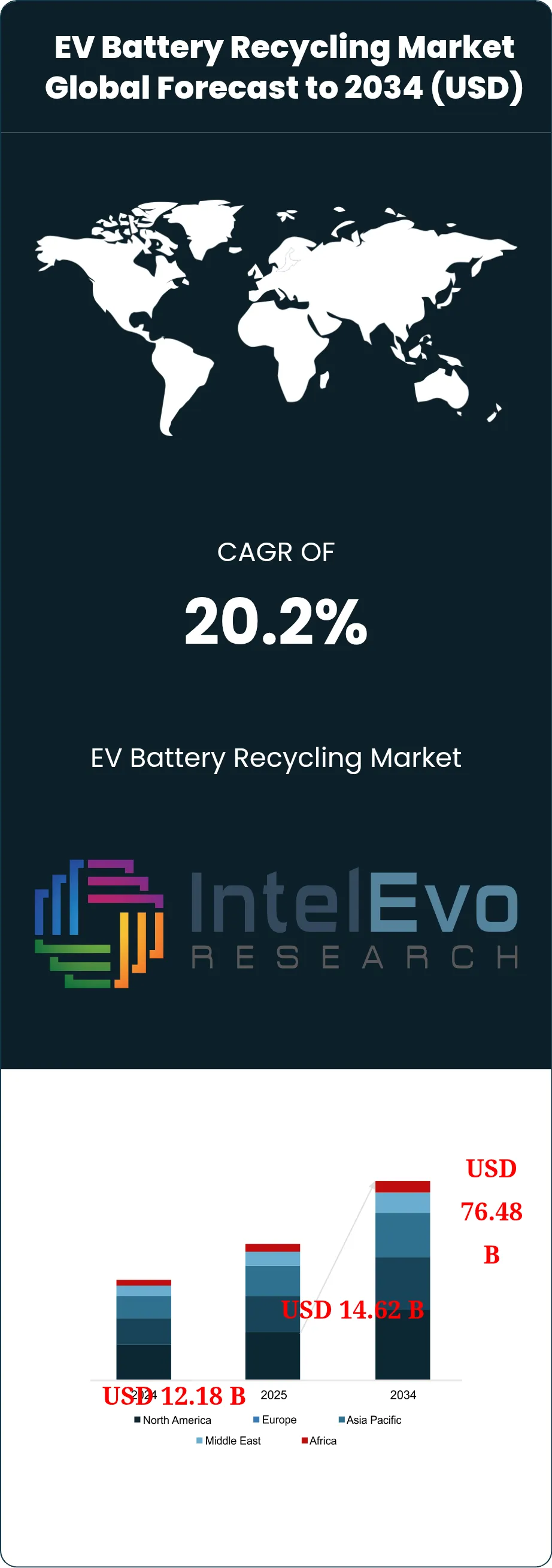

The EV Battery Recycling Market was valued at approximately USD 12.18 Billion in 2024 and reached USD 14.62 Billion in 2025. The market is projected to grow to USD 76.48 Billion by 2034, expanding at a CAGR of 20.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 61.86 Billion over the analysis period, positioning EV battery recycling as one of the most capital-intensive and strategically consequential growth markets within the global circular economy and critical materials supply chain.

Get More Information about this report -

Request Free Sample ReportEV battery recycling encompasses the collection, dismantling, and processing of end-of-life lithium-ion battery packs from electric vehicles to recover high-value materials including lithium, cobalt, nickel, manganese, and graphite for reintroduction into new battery cell manufacturing. The market sits at the convergence of three structural forces: the accelerating global EV adoption trajectory that is generating rapidly expanding battery end-of-life volumes, the geopolitical imperative to reduce dependence on primary critical mineral supply chains concentrated in the Democratic Republic of Congo for cobalt and China for processed lithium and graphite, and tightening environmental regulations that prohibit landfill disposal of lithium-ion batteries and mandate minimum recycled content in new battery production.

Regulatory frameworks across major EV markets are creating enforceable demand for recycled battery materials. The European Union Battery Regulation, which entered into force in 2023 with phased implementation through 2031, mandates minimum recycled content thresholds of 16% for cobalt, 85% for lead, 6% for lithium, and 6% for nickel in new batteries sold within the EU by 2031, rising to 26% for cobalt and 12% for lithium by 2036. These legally binding thresholds create structural offtake demand for recycled battery materials that provides revenue visibility for recycling infrastructure investment. The U.S. Inflation Reduction Act’s battery material sourcing requirements for EV tax credit eligibility have incentivized domestic recycling capacity investment, with the Department of Energy allocating over USD 3 Billion in recycling and remanufacturing grants between 2022 and 2025 through its Battery Materials Processing and Manufacturing program.

Three principal recycling process technologies compete in the EV battery recycling market: hydrometallurgical processing, which uses aqueous chemical leaching to selectively dissolve and recover battery materials with high purity and recovery rates; pyrometallurgical processing, which uses high-temperature smelting to recover metals including cobalt, nickel, and copper but sacrifices lithium and graphite recovery; and direct recycling, an emerging technology that recovers cathode active materials in their functional form to avoid the energy-intensive chemical reformation required in hydrometallurgical routes. Hydrometallurgy has emerged as the dominant commercial technology by volume in 2025, with direct recycling advancing through pilot-scale validation at facilities operated by companies including Li-Cycle, Redwood Materials, and Battery Resources.

Asia Pacific leads the global EV battery recycling market with a 44.7% share in 2025 at USD 6.54 Billion, anchored by China’s dominant position in both EV sales and battery manufacturing that has generated the world’s largest existing pool of end-of-life battery materials. Europe holds 23.8% of global market share, driven by the EU Battery Regulation’s phased recycled content mandates and the geographic concentration of battery gigafactory investment. North America accounts for 19.4% of the market in 2025, with substantial capacity expansion underway supported by Inflation Reduction Act funding and automotive OEM strategic recycling partnerships.

, By Battery Chemistry (NMC, LFP, NCA, LCO), By Material Recovered (Lithium, Cobalt, Nickel, Graphite, Copper, Aluminum), By Source (Manufacturing Scrap, End-of-Life Batteries, Second-Life Repurposing), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global EV battery recycling market was valued at USD 14.62 Billion in 2025 and is forecast to reach USD 76.48 Billion by 2034, expanding at a CAGR of 20.2% over the 2026–2034 forecast period.

- Segment Dominance: By recycling process, hydrometallurgical processing holds the largest share at 52.4% of the EV battery recycling market in 2025, favored for its high material recovery purity, commercial scalability, and compatibility with the lithium recovery mandates under the EU Battery Regulation.

- Segment Dominance: By material recovered, lithium-ion cathode materials including lithium, cobalt, and nickel collectively represent the dominant recovered material category at 61.8% of market revenue in 2025, reflecting the high commodity value of these critical minerals and the concentrated demand from battery cell manufacturers seeking to secure recycled feedstock.

- Driver: The EU Battery Regulation’s legally binding recycled content thresholds, requiring 16% recycled cobalt and 6% recycled lithium in new batteries by 2031, are creating enforceable structural demand for recycled battery materials that underpins long-term capital investment in European recycling infrastructure by both dedicated recyclers and automotive OEMs.

- Restraint: The variable chemistry and structural heterogeneity of end-of-life EV battery packs, spanning NMC, LFP, NCA, and LCO chemistries with differing cell form factors and pack configurations, increases sorting, dismantling, and process adaptation costs that constrain per-unit recycling economics and limit the degree to which recyclers can standardize processing workflows.

- Opportunity: The North American EV battery recycling market, projected to grow at a CAGR of 23.1% through 2034 under Inflation Reduction Act incentives, presents a first-mover investment window of approximately USD 18.4 Billion in cumulative recycling infrastructure capital between 2025 and 2030 for companies establishing domestic critical mineral recovery capacity.

- Trend: Automotive OEM vertical integration into battery recycling, through direct ownership or exclusive offtake agreements with dedicated recyclers, is reshaping the competitive structure of the market, with 14 major OEMs having announced proprietary recycling programs or strategic recycling partnerships by the end of 2025.

- Regional Analysis: Asia Pacific leads the global EV battery recycling market with a 44.7% share in 2025, representing USD 6.54 Billion, driven by China’s dominant EV installed base generating the world’s largest end-of-life battery volume and its integrated battery material processing infrastructure.

Competitive Landscape Overview

The EV battery recycling market exhibits moderate fragmentation in 2025, with the top four players accounting for approximately 43% of global revenue. The competitive environment features three distinct player archetypes: pure-play dedicated battery recyclers that have built proprietary processing technologies and are scaling commercial capacity, chemical and mining companies that have extended downstream into battery recycling as a critical mineral supply strategy, and automotive OEMs developing captive or partnership recycling programs to secure recycled material feedstock for their battery supply chains. Competition is driven by material recovery rates, processing cost per kilowatt-hour of battery processed, offtake contract relationships with battery manufacturers and OEMs, and geographic proximity to end-of-life battery collection networks. Strategic capital intensity is high, with commercial-scale hydrometallurgical recycling facilities requiring USD 200 Million to USD 500 Million in construction capital, creating significant barriers to entry that are concentrating capacity among well-capitalized players.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Technology / Plant | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Umicore | Belgium | Leader | Val'Eas hydromet recycling | Europe, Asia Pacific | Commissioned expanded Val'Eas Phase 3 recycling capacity in 2025, targeting 150,000 tonnes annual battery processing; signed multi-year offtake with a European automotive OEM. |

| Redwood Materials | USA | Leader | Integrated hydromet + anode/cathode | North America | Opened 100 GWh annual capacity campus in Nevada in 2025; signed recycling agreements with Toyota, Volkswagen, and Panasonic covering end-of-life and scrap battery flows. |

| Li-Cycle | Canada | Challenger | Spoke & Hub hydromet process | North America, Europe | Advanced Rochester Hub commissioning timeline in 2025 following DOE loan finalization; signed new spoke agreements with three North American battery cell manufacturers. |

| Ganfeng Lithium | China | Leader (APAC) | Integrated lithium recovery | Asia Pacific | Expanded recycling processing capacity by 40,000 tonnes in 2025; deepened integration with CATL battery scrap supply agreements for direct cathode material recovery. |

| GEM Co. | China | Challenger | Wet-process cobalt/nickel recovery | Asia Pacific | Processed over 200,000 tonnes of end-of-life batteries in 2024; expanded Southeast Asia collection network into Indonesia and Vietnam in 2025. |

| Fortum Battery Recycling | Finland | Niche Player | Hydromet black mass processing | Europe | Commissioned Harjavalta Phase 2 expansion in Finland in 2025, raising annual capacity to 30,000 tonnes; signed supply agreements with Northvolt and ACC. |

| Battery Resources (Aqua Metals) | USA | Niche Player | AquaRefining electrochemical | North America | Demonstrated commercial-scale lead-free electrochemical lithium recovery process in 2025; entered licensing discussions with two Asian battery manufacturers. |

| Retriev Technologies | USA | Niche Player | Mechanical + hydromet hybrid | North America | Expanded Ohio and British Columbia facilities in 2025 to address growing EV battery collection volumes; signed agreements with three U.S. automotive dealers for end-of-life collection. |

By Recycling Process

The EV battery recycling market by recycling process is led by hydrometallurgical processing, which captured 52.4% of global revenue in 2025 at approximately USD 7.66 Billion. Hydrometallurgical recycling uses aqueous acid or alkaline leaching solutions to selectively dissolve battery materials from shredded black mass, followed by solvent extraction, precipitation, and electrochemical refining steps to produce battery-grade lithium carbonate, cobalt sulfate, nickel sulfate, and manganese sulfate. The process achieves lithium recovery rates of 85 to 95% and cobalt and nickel recovery rates exceeding 98%, meeting the purity specifications required by cathode active material manufacturers for direct reintroduction into battery cell production. Hydrometallurgy’s commercial dominance reflects its compatibility with the EU Battery Regulation’s specific recovery rate targets and its capacity to recover lithium, which pyrometallurgy cannot achieve economically. Pyrometallurgical processing represents 30.8% of the market in 2025 at USD 4.50 Billion, relying on high-temperature smelting to recover cobalt, nickel, and copper in a mixed metal alloy while sacrificing lithium and graphite in the slag and off-gas streams. Legacy smelting infrastructure operated by Umicore, Glencore, and specialized base metal smelters continues to process significant volumes, particularly for batteries with complex chemistries not yet optimized for hydrometallurgical routes. Direct recycling, which preserves cathode active material crystal structure to avoid energy-intensive chemical reconstruction, represents 16.8% of the market at USD 2.46 Billion in 2025. This emerging technology offers the potential for the lowest processing cost per unit of recovered material but requires tight battery chemistry sorting to maintain output quality and is advancing through pilot-to-commercial scale transitions at multiple facilities.

By Battery Chemistry

The EV battery recycling market by battery chemistry is structured by the composition of incoming battery packs, which determines the material recovery value profile and processing pathway requirements for each recycling stream. Nickel Manganese Cobalt (NMC) battery chemistry accounts for the largest share of recycled volume in 2025 at 44.2% of market revenue at USD 6.46 Billion, reflecting its dominant position in premium EV battery packs from European and Korean manufacturers including BMW, Mercedes-Benz, Hyundai, and LG Energy Solution. NMC batteries offer the highest recovered material value per unit weight due to their cobalt and nickel content, making them the most economically attractive feedstock for hydrometallurgical recyclers. Lithium Iron Phosphate (LFP) chemistry represents 28.6% of the recycled volume market in 2025 at USD 4.18 Billion, and is growing fastest as Chinese EV manufacturers’ LFP-dominant production translates into end-of-life volumes entering recycling streams. LFP batteries contain no cobalt or nickel, reducing recovered material value but benefiting from the high intrinsic value of lithium recovery and iron phosphate cathode material that can be directly recycled. Nickel Cobalt Aluminum (NCA) chemistry, used primarily by Tesla and Panasonic, accounts for 16.4% of the market at USD 2.40 Billion. Lithium Cobalt Oxide (LCO) and other chemistries represent the remaining 10.8%.

By Material Recovered

The EV battery recycling market by material recovered reflects the commodity value hierarchy of critical minerals contained within lithium-ion battery cells. Cathode active materials including lithium, cobalt, nickel, and manganese collectively represent 61.8% of market revenue in 2025 at USD 9.03 Billion, reflecting the high spot market prices for battery-grade cobalt sulfate and nickel sulfate that make cathode material recovery the primary economic driver of recycling operations. Lithium recovery specifically represents 18.4% of total market revenue at USD 2.69 Billion, growing disproportionately as hydrometallurgical technology improvements raise lithium recovery rates and regulatory mandates create enforceable demand for recycled lithium content in new batteries. Graphite anode material recovery represents 14.7% of the market at USD 2.15 Billion, an underutilized recovery stream in many existing operations that is gaining commercial attention as China’s dominance of natural and synthetic graphite supply creates strategic motivation for Western recyclers to develop domestic graphite recovery capabilities. Copper and aluminum current collector recovery accounts for 13.6% at USD 1.99 Billion, providing reliable baseline revenue that partially offsets processing costs even in periods of cathode material price weakness. Other recovered materials represent the remaining 9.9%.

By Source

The EV battery recycling market by source is currently divided between manufacturing scrap and process waste, which dominates current volumes, and end-of-life vehicle batteries, which will become the primary source as the global EV fleet ages. Manufacturing scrap from battery gigafactories represents 58.3% of recycled battery input volumes in 2025 at USD 8.52 Billion, as yield losses of 5 to 15% during electrode coating, cell assembly, and formation processes generate substantial quantities of off-specification cells, electrode scrap, and electrolyte-contaminated material that require specialized recycling. This scrap stream is geographically concentrated near gigafactory clusters in China, South Korea, Europe, and North America, enabling efficient collection logistics. End-of-life vehicle batteries represent 35.4% of input volumes in 2025 at USD 5.18 Billion, a share that will grow substantially as the first wave of mass-market EVs sold between 2017 and 2021 approach end-of-battery-life at 8 to 12 years. Second-life battery repurposing for stationary energy storage, representing 6.3% of the market at USD 921 Million, diverts batteries with remaining capacity from immediate recycling into energy storage applications before eventual end-of-life processing.

Regional Analysis

Asia Pacific

Asia Pacific accounts for 44.7% of the global EV battery recycling market in 2025, representing USD 6.54 Billion, and is the world’s dominant region by both recycling volume and processing infrastructure. China is the commanding national market, driven by its position as the world’s largest EV market, with over 30 million EVs on Chinese roads as of 2025 generating the largest end-of-life battery volume globally. China’s Ministry of Industry and Information Technology has implemented a producer responsibility framework requiring battery manufacturers to establish collection and recycling networks, and the standardized battery traceability system tracks individual battery packs from manufacture through end-of-life. Major Chinese recyclers including GEM Co., Brunp Recycling (CATL subsidiary), Ganfeng Lithium, and Huayou Cobalt have built integrated processing capacity that spans collection, hydrometallurgical processing, and cathode material precursor production. South Korea’s market is driven by LG Energy Solution, Samsung SDI, and SK Innovation’s battery scrap generation and the Korean government’s K-Battery initiative supporting domestic recycling infrastructure. Japan’s Battery Recycling Promotion Council has established collection frameworks, with Sumitomo Metal Mining and Honda operating joint recycling programs. The Asia Pacific EV battery recycling market’s growth through 2034 is expected to accelerate as the 2017 to 2022 Chinese EV boom cohort reaches battery end-of-life, generating a step-change increase in end-of-life pack volumes entering recycling streams.

Europe

Europe represents 23.8% of the global EV battery recycling market in 2025 at USD 3.48 Billion, and is the most regulatory-driven regional market in the world. The EU Battery Regulation’s recycled content mandates, extended producer responsibility requirements, and collection rate targets are creating the most comprehensive legal framework for battery circular economy globally, and European recycling infrastructure investment is responding accordingly. Germany hosts the highest concentration of European EV battery recycling capacity, with BASF, Volkswagen Group Components, and specialty recyclers operating facilities supported by federal funding under Germany’s National Battery Initiative. Belgium’s Umicore operates the Val’Eas facility, the largest single-site battery recycling plant in Europe, which is expanding through phased capacity additions. Finland’s Fortum Battery Recycling and Nornickel’s Harjavalta refinery complex represent the Nordic cluster’s contribution to European critical mineral recovery. France’s Eramet and Suez have established joint recycling ventures supported by France Relance funding. The Northvolt gigafactory network in Sweden and Germany generates significant manufacturing scrap volumes that are contracted to regional recyclers. European recycling investment through 2030 is estimated at EUR 6 to 8 Billion, driven primarily by the regulatory certainty of the EU Battery Regulation’s phased requirements.

North America

North America accounts for 19.4% of the global EV battery recycling market in 2025 at USD 2.84 Billion and is the fastest-growing major regional market, projected to expand at a CAGR of 23.1% through 2034. The United States’ Inflation Reduction Act has been the primary catalyst for North American recycling investment, providing investment tax credits, production tax credits for qualifying critical mineral production, and direct grants through the Department of Energy’s Battery Materials Processing and Manufacturing program that collectively de-risk the capital formation required for commercial-scale recycling facilities. Redwood Materials’ Nevada campus, operational at 100 GWh annual processing capacity in 2025, is the most significant single-site investment in North American battery recycling history. Li-Cycle’s Rochester Hub, supported by a USD 375 Million DOE loan guarantee, is advancing toward commercial commissioning. General Motors’ strategic investment in Li-Cycle and Ford’s partnership with Redwood Materials reflect automotive OEM commitment to domestic recycled material supply. Canada’s market benefits from its lithium processing refinery investment, with Lithion Recycling and Electra Battery Materials building Quebec-based hydrometallurgical capacity supported by the Canada Infrastructure Bank. Mexico is an emerging market driven by growing battery manufacturing activity from LG Energy Solution and Samsung SDI that generates scrap recycling demand.

Latin America

Latin America represents 7.3% of the global EV battery recycling market in 2025 at USD 1.07 Billion, a disproportionately large share relative to EV penetration rates that reflects the region’s strategic position in primary lithium supply and growing interest in capturing value from lithium recycling. Chile and Argentina, holding the majority of the Lithium Triangle’s brine resources, are developing national battery recycling strategies that leverage existing lithium processing infrastructure. Brazil’s EV market is accelerating under the Mover Program’s electrification incentives, generating a nascent end-of-life battery stream and motivating recycling infrastructure investment. The Latin American recycling market is constrained by relatively underdeveloped EV collection infrastructure and the absence of comprehensive producer responsibility regulation comparable to the EU Battery Regulation, which limits the certainty of battery supply available to recycling investors. International recyclers including Umicore and Glencore have established collection agreements in Chile and Argentina that route end-of-life battery material to European or Asian processing facilities pending the development of domestic processing capacity.

Middle East & Africa

Middle East & Africa accounts for 4.8% of the global EV battery recycling market in 2025 at USD 702 Million, a share that substantially reflects South Africa’s industrial recycling infrastructure and the UAE’s emerging position as a regional hub for critical mineral processing and trading. South Africa’s established base metal smelting industry, particularly the Bushveld Complex’s platinum group metal processing infrastructure, provides technical adjacencies applicable to battery metal recovery. The UAE’s Khalifa Industrial Zone Abu Dhabi is developing battery recycling facilities targeting the Gulf Cooperation Council’s growing EV fleet, supported by Abu Dhabi government industrial diversification investment. Saudi Arabia’s NEOM project and Vision 2030’s electric mobility targets are creating forward-looking demand for recycling infrastructure. The Democratic Republic of Congo’s position as the source of approximately 70% of global primary cobalt creates potential strategic interest in establishing domestic battery recycling to capture value from secondary cobalt alongside its primary mining operations, though infrastructure and governance constraints limit near-term development.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Recycling Process

- Hydrometallurgical Processing

- Pyrometallurgical Processing

- Direct Recycling

By Battery Chemistry

- Nickel Manganese Cobalt (NMC)

- Lithium Iron Phosphate (LFP)

- Nickel Cobalt Aluminum (NCA)

- Lithium Cobalt Oxide (LCO) and Others

By Material Recovered

- Cathode Active Materials (Lithium, Cobalt, Nickel, Manganese)

- Graphite Anode Material

- Copper and Aluminum Current Collectors

- Other Recovered Materials

By Source

- Manufacturing Scrap and Process Waste

- End-of-Life Vehicle Batteries

- Second-Life Battery Repurposing

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.62 B |

| Forecast Revenue (2034) | USD 76.48 B |

| CAGR (2025-2034) | 20.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Recycling Process, (Hydrometallurgical Processing, Pyrometallurgical Processing, Direct Recycling), By Battery Chemistry, (Nickel Manganese Cobalt (NMC), Lithium Iron Phosphate (LFP), Nickel Cobalt Aluminum (NCA), Lithium Cobalt Oxide (LCO) and Others), By Material Recovered, (Cathode Active Materials (Lithium, Cobalt, Nickel, Manganese), Graphite Anode Material, Copper and Aluminum Current Collectors, Other Recovered Materials), By Source, (Manufacturing Scrap and Process Waste, End-of-Life Vehicle Batteries, Second-Life Battery Repurposing) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | UMICORE, REDWOOD MATERIALS, LI-CYCLE, GEM CO., GANFENG LITHIUM, HUAYOU COBALT, BRUNP RECYCLING (CATL SUBSIDIARY), FORTUM BATTERY RECYCLING, RETRIEV TECHNOLOGIES, BATTERY RESOURCES (AQUA METALS), GLENCORE, LITHION RECYCLING, ELECTRA BATTERY MATERIALS, ERAMET, SUMITOMO METAL MINING, VOLKSWAGEN GROUP COMPONENTS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Battery Chemistry (NMC, LFP, NCA, LCO), By Material Recovered (Lithium, Cobalt, Nickel, Graphite, Copper, Aluminum), By Source (Manufacturing Scrap, End-of-Life Batteries, Second-Life Repurposing), Industry Trends & Forecast 2026-2034")

, By Battery Chemistry (NMC, LFP, NCA, LCO), By Material Recovered (Lithium, Cobalt, Nickel, Graphite, Copper, Aluminum), By Source (Manufacturing Scrap, End-of-Life Batteries, Second-Life Repurposing), Industry Trends & Forecast 2026-2034")

, By Battery Chemistry (NMC, LFP, NCA, LCO), By Material Recovered (Lithium, Cobalt, Nickel, Graphite, Copper, Aluminum), By Source (Manufacturing Scrap, End-of-Life Batteries, Second-Life Repurposing), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the EV Battery Recycling Market?

The Global EV Battery Recycling Market was valued at USD 12.18 Billion in 2024 and is projected to reach USD 76.48 Billion by 2034, growing at a CAGR of 20.2% from 2026 to 2034, driven by rising electric vehicle adoption, increasing demand for sustainable battery material recovery, advancements in lithium-ion battery recycling technologies, and growing government focus on circular economy initiatives and critical mineral supply chain security worldwide.

Who are the major players in the EV Battery Recycling Market?

UMICORE, REDWOOD MATERIALS, LI-CYCLE, GEM CO., GANFENG LITHIUM, HUAYOU COBALT, BRUNP RECYCLING (CATL SUBSIDIARY), FORTUM BATTERY RECYCLING, RETRIEV TECHNOLOGIES, BATTERY RESOURCES (AQUA METALS), GLENCORE, LITHION RECYCLING, ELECTRA BATTERY MATERIALS, ERAMET, SUMITOMO METAL MINING, VOLKSWAGEN GROUP COMPONENTS, Others

Which segments covered the EV Battery Recycling Market?

By Recycling Process, (Hydrometallurgical Processing, Pyrometallurgical Processing, Direct Recycling), By Battery Chemistry, (Nickel Manganese Cobalt (NMC), Lithium Iron Phosphate (LFP), Nickel Cobalt Aluminum (NCA), Lithium Cobalt Oxide (LCO) and Others), By Material Recovered, (Cathode Active Materials (Lithium, Cobalt, Nickel, Manganese), Graphite Anode Material, Copper and Aluminum Current Collectors, Other Recovered Materials), By Source, (Manufacturing Scrap and Process Waste, End-of-Life Vehicle Batteries, Second-Life Battery Repurposing)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date