- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Exoskeleton Market Size, Growth & Forecast 2025–2034 | CAGR 18.1%

Global Exoskeleton Market Size, Share & Analysis By Mobility (Fixed/Stationary, Mobile), By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton), Injury Reduction Benefits, Technology Advancements, Key Players & Forecast 2025–2034

Report Overview

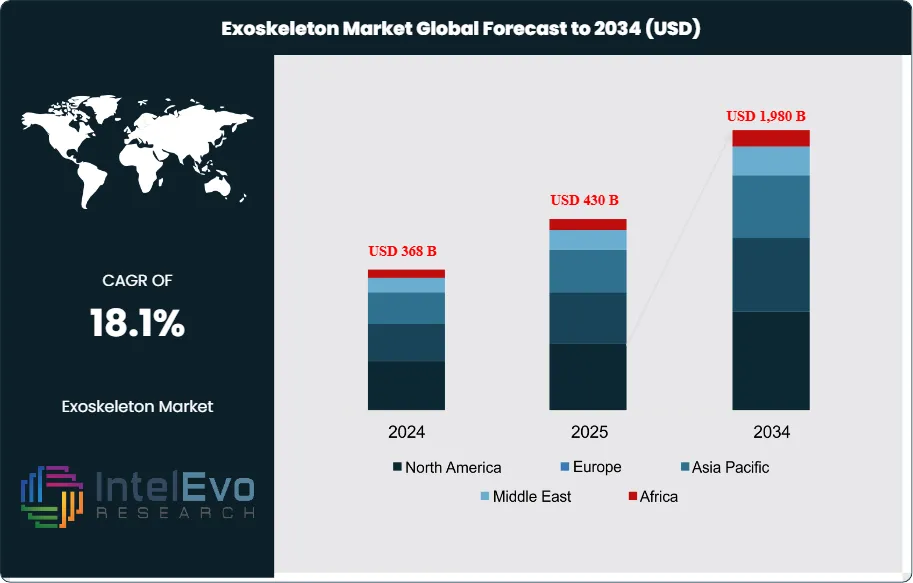

The Exoskeleton Market is estimated at approximately USD 430 billion in 2025 and is projected to reach around USD 1,980 billion by 2034, registering a strong compound annual growth rate (CAGR) of about 18.1% during 2026–2034. This growth is being fueled by rising adoption of powered exoskeletons across healthcare rehabilitation, industrial worker safety, military load-bearing systems, and elderly mobility assistance. Accelerating investments in human augmentation technologies, coupled with advances in AI-enabled motion control, lightweight materials, and wearable robotics, are positioning exoskeletons as a core component of future workforce and healthcare infrastructure. As regulatory approvals expand and unit costs decline, market penetration is expected to broaden rapidly across both developed and emerging economies, supporting sustained long-term demand.

Get More Information about this report -

Request Free Sample ReportMarket momentum reflects a transition from research pilots to scaled deployment across healthcare, industrial, defense, and construction settings. Over the past five years, installed bases have expanded rapidly as rehabilitation centers and trauma hospitals formalized exoskeleton protocols, while automotive and logistics operators adopted occupational exosuits to reduce musculoskeletal injuries. Medical use remains the largest revenue pool—driven by aging demographics, post-stroke mobility therapies, and rising spinal cord injury (SCI) prevalence—while non-medical segments are the fastest-growing as productivity and safety ROI become measurable. In the U.S. alone, new SCI incidence is typically in the 17,000–18,000 range annually, underlining the sustained clinical need; globally, stroke recovery and neurorehabilitation cohorts continue to expand, supporting multi-year demand visibility.

Growth is propelled by converging drivers on both the demand and supply sides. Providers and employers seek to cut injury-related downtime and worker compensation costs, with early adopters reporting double-digit reductions in back and shoulder strain claims. On the supply side, falling system weights (often 20–30% lighter per product generation), improved ergonomics, and modularity are widening addressable applications. Nevertheless, high upfront costs, uneven reimbursement frameworks, safety/liability considerations, and integration complexity remain gating factors, particularly for smaller health systems and mid-market manufacturers. Regulatory clarity is improving: in the U.S., most therapeutic devices route through Class II pathways, and EU MDR requirements are accelerating quality system maturity, but compliance timelines can elongate commercialization.

Technology is reshaping performance and economics. Soft exosuits, energy-recapture knee/hip modules, and high-torque lightweight actuators are enhancing mobility while reducing fatigue. Embedded sensors fused with AI/ML enable intent detection and adaptive gait tuning; cloud analytics are beginning to quantify therapy outcomes and workplace risk reductions in real time. Battery energy density gains and hot-swappable packs are extending duty cycles toward full-shift usage.

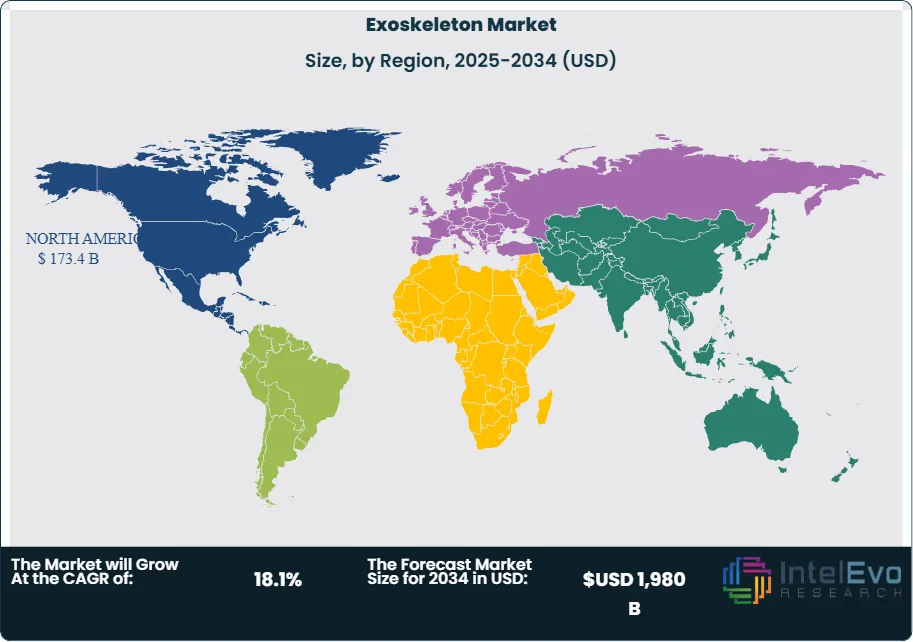

Regionally, North America leads with an estimated 35–40% share on account of reimbursement progress and enterprise safety programs, while Europe (≈30% share) benefits from strong rehabilitation networks. Asia Pacific is the principal investment hotspot, projected to outpace the global average with >18% CAGR through 2033 as Japan, South Korea, and China scale industrial exosuits and elder-care solutions. For investors, near-term opportunities center on clinically validated rehab platforms, modular industrial exosuits with demonstrable ROI, and AI-enabled software layers that lock in recurring revenue.

, By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton), Injury Reduction Benefits, Technology Advancements, Key Players & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global exoskeleton market was 430 billion in 2025 and is projected to reach USD 1,980 billion by 2034 (18.1% CAGR), propelled by aging demographics, rising stroke/SCI rehabilitation demand, and enterprise investments in industrial ergonomics.

- Product Type: Mobile exoskeletons held 63.56% share in 2023, favored for versatility across rehab clinics, automotive, and logistics, while stationary systems remain niche in inpatient settings.

- Technology: Powered exoskeletons captured 76.1% revenue share in 2023 as higher torque, multi-joint control, and gait-training features command premiums; passive/soft exosuits are poised to grow fastest (>18–20% CAGR) on cost and comfort advantages.

- Driver: Clinical need is expanding, with the U.S. recording ~17–18k new SCI cases annually and a rising global stroke cohort; formalized hospital protocols and growing insurer pilots are accelerating adoption of exoskeleton-assisted neurorehabilitation.

- Restraint: High acquisition costs—often USD 30,000–100,000+ for medical-grade powered units—plus uneven reimbursement and safety certification for uneven/outdoor terrain elongate payback periods and slow SME and smaller hospital uptake.

- Opportunity: Asia Pacific is the principal growth pocket, expected to outpace the global average with >18% CAGR through 2033 as Japan, South Korea, and China scale industrial exosuits and elder-care deployments, potentially adding 5–7 percentage points to the region’s global share.

- Trend: Integration of AI/ML for intent detection and adaptive control, lighter actuators (≈20–30% weight reduction per product cycle), and connected analytics platforms (e.g., Ekso Bionics, CYBERDYNE, German Bionic, Ottobock) are enabling fleet-scale rollouts and full-shift duty cycles with hot-swappable batteries.

- Regional Analysis: North America led with ~44.8% share (≈USD 173.4 billion in 2023) on reimbursement progress and enterprise safety programs; Europe (≈30% share) benefits from mature rehab networks, while Asia Pacific delivers the fastest growth and represents the key investment hotspot for industrial applications.

Mobility Analysis

Mobile exoskeletons remain the center of gravity for market expansion in 2025, building on their 2023 baseline of roughly 63.6% revenue share. Their advantage stems from task versatility—spanning gait therapy in rehabilitation, load-handling in manufacturing and logistics, and endurance support in defense—combined with steady improvements in weight, ergonomics, and duty cycles. As battery density, hot-swappable packs, and modular frames mature, mobile units are increasingly viable for full-shift industrial use and community-based clinical care.

Key growth drivers include aging populations, rising stroke and spinal cord injury prevalence, and employer programs targeting musculoskeletal injury reduction. Challenges persist around outdoor/uneven-terrain safety certification, worker acceptance, and total cost of ownership, particularly for small clinics and SMEs. Fixed/stationary systems, while a smaller niche, deliver high-precision gait training and balance control in inpatient and outpatient facilities, benefiting from expanding neurorehabilitation infrastructure and objective outcome tracking.

Looking ahead, mobile platforms are positioned for high-teens CAGR through 2030–2033 as unit economics improve and fleet analytics quantify ROI. Fixed/stationary solutions should post steady low-double-digit growth, supported by hospital capital cycles and reimbursement pilots that prioritize measurable functional gains and therapist productivity.

Technology Analysis

Powered systems accounted for about 76.1% of revenues in 2023 and will continue to dominate through 2025+, driven by multi-joint control, higher torque, and AI-enabled intent detection that personalizes assistance in real time. These capabilities command premium pricing in post-acute care and high-value industrial use cases, though acquisition costs (often USD 30,000–100,000+) and maintenance remain gating factors for budget-constrained buyers.

Non-powered and soft exosuits are scaling rapidly in warehousing, automotive, and construction due to lower price points, minimal training needs, and compatibility with existing PPE. Mechanical energy-storage designs targeting back/shoulder support help reduce strain exposure and fatigue, improving near-term ROI without batteries or motors. As standards and validation studies proliferate, purchasing committees increasingly treat passive solutions as preventive ergonomics investments rather than experimental pilots.

Through the forecast window, powered systems should grow at a solid mid-teens pace as vendors (e.g., Ekso Bionics, CYBERDYNE, Ottobock, ReWalk) shift toward software subscriptions, remote telemetry, and service contracts. Passive/soft categories are expected to outpace the market—often >18–20% CAGR—on comfort, cost, and ease of deployment across multi-site operations.

Extremity Analysis

Lower-body platforms led the market with ~43.6% share in 2023 and remain the workhorse segment in 2025, addressing mobility impairment, gait retraining, and leg/lumbar assistance for material handling. Their impact is most visible in stroke and SCI rehabilitation and in jobs requiring prolonged standing, lifting, and walking.

Upper-body solutions are gaining traction in overhead and repetitive tasks across automotive, aerospace, and parcel logistics, where early adopters report double-digit reductions in shoulder and back strain events. They also support upper-limb neurorehabilitation, expanding the eligible patient pool beyond traditional gait programs. Full-body systems—while still niche due to weight and complexity—serve defense and heavy industry missions requiring comprehensive augmentation and hazard protection.

Outlook favors continued leadership for lower-body devices, faster growth in upper-body wearables as textile-based designs improve comfort, and selective uptake of full-body suits in mission-critical environments. Notably, partial-body configurations are projected to post robust mid-teens growth (≈16–17% CAGR) as buyers prioritize targeted risk reduction over all-encompassing augmentation.

End-Use Analysis

Healthcare remains the single largest end-use, holding about 51.7% share in 2023 and sustaining momentum into 2025 as rehabilitation networks formalize exoskeleton protocols and payers expand pilots for post-stroke and SCI care. Leading vendors—Ekso Bionics, CYBERDYNE, ReWalk, DIH/Hocoma, Ottobock/SuitX—are bundling evidence-based training programs with cloud analytics to document functional gains and therapy efficiency.

Military adoption, though smaller, is strategically important. Programs from BAE Systems, Lockheed Martin, Raytheon, SRI International, and others focus on dismounted soldier endurance and load carriage, with lower-body platforms historically representing a large share of fielded systems. Procurement hinges on ruggedization, power management, and interoperability with body armor and comms gear.

Industry is the fastest-growing end-use as manufacturers, logistics providers, and construction firms deploy exosuits to cut musculoskeletal injuries and improve throughput. Companies such as German Bionic, Ottobock, Honda, and Ekso Bionics target high-incidence tasks (lifting, sustained flexion, overhead work), with multi-site rollouts increasingly justified by measurable reductions in strain exposure and lost-time incidents, alongside improved worker retention.

By Region

North America leads the revenue pool (≈44.8% share; ~USD 173.4 billion in 2023) and retains a 2025 edge on the back of reimbursement pilots, enterprise safety programs, and a dense ecosystem of clinical partners and integrators. Europe follows with a strong share near 30%, supported by mature rehabilitation pathways and MDR-driven quality standards that favor clinically validated platforms.

Asia Pacific is the primary growth engine through 2030–2033, with many markets tracking above the global CAGR (often >18%) as Japan, South Korea, and China scale industrial exosuits and elder-care technologies and as India expands rehabilitation capacity. Government incentives for advanced manufacturing and robotics, plus local component supply chains, are accelerating commercialization.

Latin America and the Middle East & Africa are earlier in adoption but show rising demand tied to new rehab centers and heavy-industry applications (mining, oil & gas, shipyards). Partnerships between teaching hospitals and global vendors, along with donor and public-health funding for neurorehabilitation, are laying the groundwork for multi-year uptake, particularly in tier-1 cities and export-oriented industrial zones.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Mobility

- Fixed/Stationary

- Mobile

Technology

- Non-Powered

- Powered

Extremity

- Lower Body

- Upper Body

- Full Body

End-use

- Healthcare

- Industry

- Military

Type

- Soft Exoskeleton

- Rigid Exoskeleton

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 368 B |

| Forecast Revenue (2034) | USD 1,980 B |

| CAGR (2024-2034) | 18.1% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Mobility (Fixed/Stationary, Mobile), By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Cyberdyne Inc., Wearable Robotics Srl, ActiveLink (Panasonic Corporation), ReWalk Robotics Ltd., Rex Bionics Plc., Ekso Bionics, RB3D, Bionik Laboratories Corp., Suit X (U.S. Bionics Inc.), Hocoma, Lockheed Martin Corporation, Atoun Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton), Injury Reduction Benefits, Technology Advancements, Key Players & Forecast 2025–2034")

, By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton), Injury Reduction Benefits, Technology Advancements, Key Players & Forecast 2025–2034")

, By Technology (Non-Powered, Powered), By Extremity (Lower Body, Upper Body, Full Body), By End-use (Healthcare, Industry, Military), By Type (Soft Exoskeleton, Rigid Exoskeleton), Injury Reduction Benefits, Technology Advancements, Key Players & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date