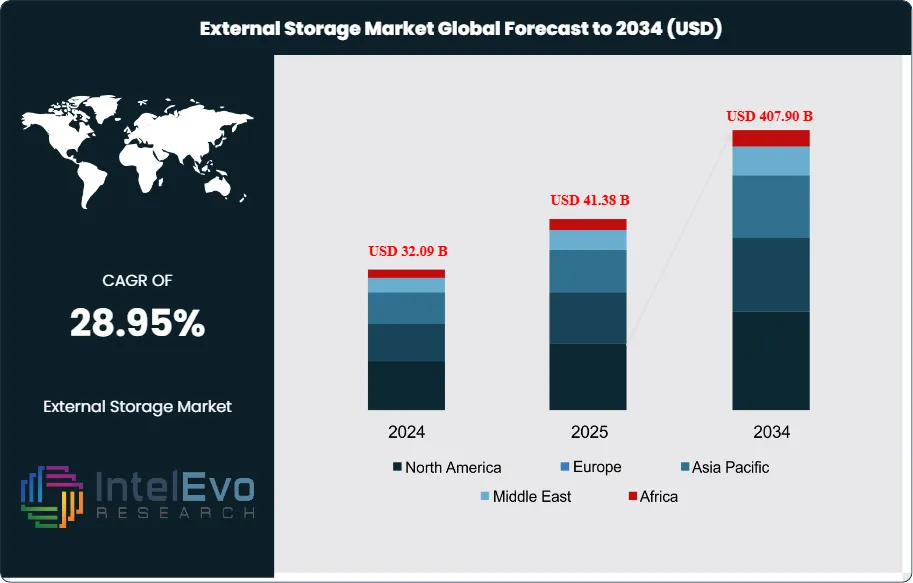

The External Storage Market size is expected to be worth around USD 407.90 Billion by 2034, from USD 32.09 Billion in 2024, growing at a CAGR of 28.95% during the forecast period from 2024 to 2034. The External Storage Market encompasses devices and solutions designed to store data externally, separate from the internal storage systems of computers, smartphones, and other electronic devices.

This market includes a comprehensive range of storage technologies such as external hard drives, solid-state drives (SSDs), optical storage devices, network-attached storage (NAS), flash storage devices, and cloud storage solutions. These technologies serve both consumer and enterprise segments, providing scalable, portable, and secure data storage capabilities that extend beyond built-in device limitations.

The market is experiencing robust expansion driven by exponential data generation across industries, increasing digitization of business processes, and the growing adoption of remote work and cloud computing paradigms. The proliferation of content creation, multimedia consumption, and data-intensive applications has created unprecedented demand for external storage solutions. Enterprise digital transformation initiatives, combined with regulatory compliance requirements for data retention and backup, are further accelerating market growth. The integration of artificial intelligence and machine learning technologies into storage systems is enhancing data management capabilities and driving innovation across the sector.

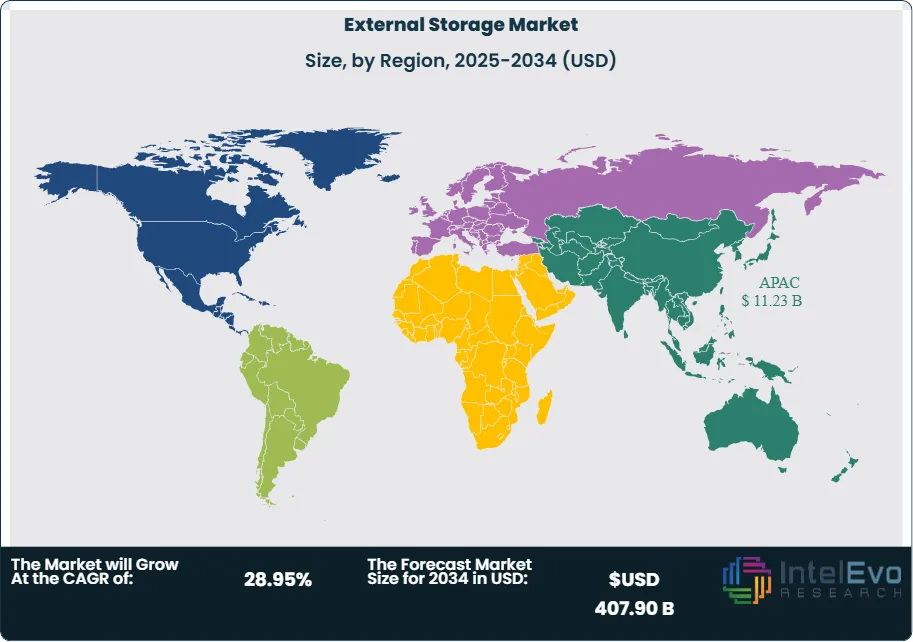

Asia-Pacific emerges as the dominant regional market, benefiting from strong manufacturing capabilities, extensive consumer electronics adoption, and rapid digital transformation across emerging economies. The region's leadership is reinforced by the presence of major technology manufacturers, cost-effective production capabilities, and growing enterprise IT infrastructure investments. North America maintains significant market presence through advanced technology adoption, substantial enterprise spending on data storage solutions, and strong demand for high-performance storage systems in sectors such as healthcare, finance, and media entertainment.

The pandemic significantly accelerated external storage market growth as organizations rapidly transitioned to remote work models, requiring enhanced data accessibility and backup solutions. Educational institutions, healthcare providers, and businesses across industries invested heavily in external storage infrastructure to support distributed workforces and ensure business continuity. The shift toward digital-first operations, increased content creation, and growing reliance on cloud-based collaboration tools created sustained demand for both consumer and enterprise external storage solutions.

Ongoing trade tensions, particularly between major economies, have influenced supply chain dynamics and pricing strategies within the external storage market. Tariff implementations on electronic components and finished storage products have prompted manufacturers to diversify production locations and adjust pricing models. Geopolitical concerns regarding data sovereignty and security have increased demand for locally-manufactured storage solutions and influenced enterprise procurement decisions, particularly in government and critical infrastructure sectors.

Key Takeaways

Market Growth: The External Storage Market is expected to reach USD 407.90 Billion by 2034, propelled by massive data proliferation, widespread business digitalization, and the surge in remote work coupled with cloud adoption.

Storage Type Dominance: External Hard Drives lead the market due to cost-effectiveness and high storage capacity.

Application Dominance: Consumer Electronics holds the largest share, owing to widespread personal device adoption.

Drivers: Key drivers accelerating growth include exponential data generation and digital transformation, which boost market expansion through increased storage requirements and technology adoption.

Restraints: Growth is hindered by cloud storage competition and security concerns, which create challenges such as market saturation and data privacy issues.

Opportunities: The market is poised for expansion due to opportunities like IoT proliferation and 5G deployment, which enable enhanced connectivity and data processing capabilities.

Trends: Emerging trends including SSD adoption and AI-powered storage management are reshaping the market by improving performance and intelligent data handling.

Regional Leader: Asia-Pacific leads owing to manufacturing capabilities and consumer electronics demand. North America and Europe show high promise due to enterprise digitization and advanced technology adoption.

Storage Type Analysis:

The Storage Type segment represents the fundamental technology categories that define external storage capabilities and performance characteristics. External Hard Drives maintain market leadership through their optimal combination of high storage capacity, cost-effectiveness, and proven reliability for both consumer and enterprise applications. These devices excel in scenarios requiring large-capacity storage at affordable price points, making them ideal for data backup, media archiving, and bulk file storage. Solid-State Storage Devices are experiencing rapid growth due to superior performance, durability, and decreasing costs, particularly appealing to professionals requiring fast data access and transfer speeds. Flash Storage Devices continue to gain traction in portable applications, while Optical Storage maintains relevance in specific archival and distribution use cases.

Application Analysis:

Consumer Electronics Leads With more than 30% Market Share In External Storage Market: Consumer Electronics applications drive the largest market share through personal data storage needs, multimedia content management, and device capacity expansion requirements. This segment benefits from growing content creation, digital photography, gaming, and entertainment consumption trends. Enterprise applications represent a rapidly growing segment, driven by data backup requirements, regulatory compliance mandates, and digital transformation initiatives. Healthcare, Education, and Government sectors contribute specialized demand patterns, often requiring enhanced security features, compliance certifications, and specialized data management capabilities tailored to their unique operational requirements and regulatory environments.

Regional Analysis:

Asia-Pacific Leads With over 35% Market Share In External Storage Market: Asia-Pacific dominates the global external storage market through its comprehensive ecosystem encompassing manufacturing excellence, technological innovation, and substantial consumer demand. The region benefits from the presence of major storage device manufacturers, cost-effective production capabilities, and rapidly expanding consumer electronics markets across countries like China, Japan, South Korea, and India. Strong government initiatives supporting digital transformation, smart city development, and Industry 4.0 adoption create favorable conditions for sustained market growth. The region's leadership is reinforced by its role as a global manufacturing hub for electronic components and finished storage devices.

North America represents a mature but technologically advanced market characterized by high per-capita technology adoption, substantial enterprise IT spending, and strong demand for high-performance storage solutions. The region's market dynamics are driven by established technology companies, advanced data center infrastructure, and sophisticated enterprise requirements for data management and security. Strong regulatory frameworks governing data protection and privacy create additional demand for compliant storage solutions, particularly in healthcare, finance, and government sectors.

Europe demonstrates steady growth supported by stringent data protection regulations, advanced manufacturing capabilities, and growing emphasis on data sovereignty. The region's market is characterized by strong demand for security-focused storage solutions, compliance with GDPR requirements, and increasing adoption of cloud-hybrid storage architectures. European enterprises prioritize data protection, privacy, and local storage capabilities, creating opportunities for specialized storage solutions and services.

Storage Type (Flash Memory Devices, Professional Optical Storage, Solid State Storage, External Hard Drives); Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Western Digital Corporation, Infortrend Technology Inc., Seagate Technology, Oracle Corporation, Toshiba Corporation, Samsung Electronics Co., Ltd., Lenovo Group Limited, Synology Inc., NetApp Inc.sss, Micron Technology Inc., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), IBM Corporation, Kingston Technology Company Inc., Fujitsu Ltd., Hitachi Vantara, Pure Storage Inc., ADATA Technology Co., Ltd., LaCie (Seagate subsidiary), G-Technology (Western Digital subsidiary), Quantum Corporation, Transcend Information Inc., Promise Technology Inc., Thecus Technology Corp., QNAP Systems, Inc.

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 MARKET SCOPE

1.3 RESEARCH METHODOLOGY

1.3.1 SECONDARY DATA

1.3.2 PRIMARY DATA

1.3.3 MARKET SIZE ESTIMATION

1.3.4 BOTTOM-UP APPROACH

1.3.5 TOP-DOWN APPROACH

1.4 RESEARCH ASSUMPTION

1.5 STAKEHOLDERS

1.6 CURRENCY

1.7 YEARS CONSIDERED

1.8 LIMITATION

2 EXECUTIVE SUMMARY

3 MARKET OUTLOOK

3.1 INTRODUCTION

3.2 DROC MATRIX

3.3 MARKET CHALLENGES

3.4 MARKET SHARE ANALYSIS

3.5 COST STRUCTURE ANALYSIS

3.6 VALUE CHAIN ANALYSIS

3.7 COVID-19 IMPACT ANALYSES

3.8 TARIFF IMPACT ANALYSIS

4 INDUSTRY TRENDS

4.1 INTRODUCTION

4.2 PESTEL ANALYSIS

4.3 PORTER’S FIVE FORCES MODEL

4.3.1 DEGREE OF COMPETITION

4.3.2 BARGAINING POWER OF BUYERS

4.3.3 BARGAINING POWER OF SUPPLIERS

4.3.4 THREAT FROM SUBSTITUTES

4.3.5 THREAT FROM NEW ENTRANTS

5 EXTERNAL STORAGE STORAGE TYPE ANALYSIS

5.1 INTRODUCTION

5.2 HISTORICAL MARKET STORAGE TYPE ANALYSIS, 2019-2023

5.3 CURRENT AND FUTURE MARKET VALUE (MILLION) PROJECTIONS, 2024–2034

FIGURE 19 NORTH AMERICA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 20 NORTH AMERICA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 21 U.S. EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 22 U.S. EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 23 CANADA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 24 CANADA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 25 MEXICO EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 26 MEXICO EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 27 MARKET SHARE BY COUNTRY

FIGURE 28 APAC EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 29 APAC EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 30 CHINA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 31 CHINA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 32 JAPAN EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 33 JAPAN EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 34 KOREA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 35 KOREA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 36 INDIA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 37 INDIA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 38 SOUTHEAST ASIA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 39 SOUTHEAST ASIA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 40 MARKET SHARE BY COUNTRY

FIGURE 41 MIDDLE EAST AND AFRICA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 42 MIDDLE EAST AND AFRICA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 43 SAUDI ARABIA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 44 SAUDI ARABIA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 45 UAE EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 46 UAE EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 47 EGYPT EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 48 EGYPT EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 49 NIGERIA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 50 NIGERIA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 51 SOUTH AFRICA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 52 SOUTH AFRICA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 53 MARKET SHARE BY COUNTRY

FIGURE 54 EUROPE EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 55 EUROPE EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 56 GERMANY EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 57 GERMANY EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 58 FRANCE EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 59 FRANCE EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 60 UK EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 61 UK EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 62 SPAIN EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 63 SPAIN EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 64 ITALY EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 65 ITALY EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 66 MARKET SHARE BY COUNTRY

FIGURE 67 SOUTH AMERICA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 68 SOUTH AMERICA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 69 BRAZIL EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 70 BRAZIL EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 71 ARGENTINA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 72 ARGENTINA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 73 COLUMBIA EXTERNAL STORAGE CURRENT AND FUTURE STORAGE TYPE ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 74 COLUMBIA EXTERNAL STORAGE CURRENT AND FUTURE APPLICATION ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 75 FINANCIAL OVERVIEW:

Key Players Analysis

Western Digital Corporation: Western Digital maintains a dominant position in the external storage market with comprehensive product portfolios spanning consumer and enterprise segments. The company's competitive edge stems from vertical integration across the storage value chain, including hard drive manufacturing, SSD technology development, and storage system design capabilities. Western Digital's strategic advantages include strong brand recognition, extensive distribution networks, and continuous innovation in storage technologies. The company's expansion strategy focuses on developing next-generation storage solutions, strengthening partnerships with cloud service providers, and expanding market presence in emerging economies through localized product offerings and competitive pricing strategies.

Seagate Technology PLC: Seagate leverages its position as a leading storage technology innovator to deliver high-capacity, reliable external storage solutions across consumer and enterprise markets. The company's competitive differentiators include advanced magnetic recording technologies, specialized storage solutions for data centers, and strong relationships with original equipment manufacturers. Seagate's strategic initiatives emphasize developing cutting-edge storage technologies, expanding cloud storage partnerships, and creating integrated storage ecosystems that combine hardware, software, and services to deliver comprehensive data management solutions.

Samsung Electronics Co., Ltd.: Samsung utilizes its semiconductor manufacturing expertise and consumer electronics market leadership to deliver innovative external storage products featuring advanced SSD technologies and mobile-optimized solutions. The company's market advantages include cutting-edge memory and storage technologies, strong brand recognition in consumer markets, and integrated product ecosystems that enhance user experience across Samsung devices. Samsung's strategic focus involves advancing next-generation storage technologies, expanding market reach through competitive pricing, and developing specialized storage solutions for emerging applications such as gaming, content creation, and mobile computing.

Toshiba Corporation: Toshiba combines decades of storage technology expertise with innovative product development to serve both consumer and enterprise external storage markets. The company's competitive strengths include advanced flash memory technologies, reliable mechanical storage solutions, and strong presence in Asian markets. Toshiba's strategic direction emphasizes developing high-capacity storage solutions, strengthening partnerships with system integrators, and expanding market presence through technology licensing agreements and joint ventures with regional manufacturers.

Dell Technologies Inc.: Dell leverages its enterprise infrastructure expertise and customer relationships to deliver comprehensive external storage solutions tailored to business requirements. The company's competitive advantages include deep understanding of enterprise storage needs, integrated solutions combining hardware and software, and strong support services that ensure successful implementation and ongoing operation. Dell's strategic approach focuses on developing software-defined storage solutions, expanding cloud integration capabilities, and creating industry-specific storage offerings that address unique vertical market requirements.

Market Key Players

Western Digital Corporation

Infortrend Technology Inc.

Seagate Technology

Oracle Corporation

Toshiba Corporation

Samsung Electronics Co., Ltd.

Lenovo Group Limited

Synology Inc.

NetApp Inc.sss

Micron Technology Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise (HPE)

IBM Corporation

Kingston Technology Company Inc.

Fujitsu Ltd.

Hitachi Vantara

Pure Storage Inc.

ADATA Technology Co., Ltd.

LaCie (Seagate subsidiary)

G-Technology (Western Digital subsidiary)

Quantum Corporation

Transcend Information Inc.

Promise Technology Inc.

Thecus Technology Corp.

QNAP Systems, Inc.

Drivers:

Exponential Data Generation and Digital Content Creation:

The unprecedented explosion in data generation across consumer and enterprise segments serves as the primary catalyst for external storage market expansion. Digital transformation initiatives, remote work adoption, and content creation proliferation have created insatiable demand for scalable storage solutions. Social media platforms, streaming services, gaming applications, and professional content creation tools generate massive amounts of data requiring reliable, accessible storage infrastructure. Enterprise applications including IoT devices, artificial intelligence systems, and business analytics platforms contribute to exponential data growth rates that consistently outpace internal storage capabilities. This driver manifests through increased storage capacity requirements, demand for high-performance storage solutions, and growing need for data backup and archival systems. Organizations implementing data-driven strategies report significant improvements in operational efficiency, customer insights, and competitive positioning when supported by robust external storage infrastructure.

Enterprise Digital Transformation and Compliance Requirements:

The accelerating pace of enterprise digital transformation is driving substantial investments in external storage infrastructure to support cloud migration, data analytics, and hybrid work environments. Modern businesses require flexible, scalable storage solutions that can adapt to changing operational requirements while maintaining data accessibility and security standards. Regulatory compliance mandates across industries such as healthcare (HIPAA), finance (SOX), and data protection (GDPR) create mandatory requirements for comprehensive data backup, retention, and archival systems. This driver gains momentum through evolving regulatory frameworks, increasing data governance requirements, and growing recognition of data as a strategic business asset. The timeline for compliance implementation typically spans 18-36 months, with strategic outcomes including improved regulatory adherence, enhanced data security postures, and reduced operational risks associated with data loss or breach incidents.

Restraints:

Cloud Storage Competition and Service Integration:

The rapid expansion and sophistication of cloud storage services presents significant competitive pressure on traditional external storage solutions, particularly in consumer and small business segments. Cloud providers offer seamless integration with applications, automatic backup capabilities, and access from multiple devices without physical hardware requirements. This competitive landscape creates pricing pressure on external storage devices and reduces market appeal for users prioritizing convenience over ownership. The financial impact extends beyond direct competition to include changing user preferences toward subscription-based storage models and integrated cloud services. Organizations often find cloud solutions more attractive due to reduced maintenance overhead, automatic updates, and scalable pricing models. Mitigation strategies include developing hybrid storage solutions that combine local and cloud capabilities, focusing on specific use cases where physical storage provides advantages, and creating value-added services that differentiate external storage products from commodity cloud offerings.

Data Security and Privacy Concerns:

Growing awareness of data security vulnerabilities and privacy risks associated with external storage devices creates market hesitation, particularly among enterprise and government customers. High-profile data breaches involving lost or stolen external storage devices have heightened organizational concerns about data protection and regulatory compliance. Technical challenges include ensuring robust encryption, managing access controls, and maintaining data integrity across diverse storage platforms and use cases. These concerns are amplified by sophisticated cyber threats, evolving regulatory requirements, and increasing penalties for data protection failures. Historical incidents involving external storage security compromises have led to restrictive corporate policies and procurement guidelines that limit market adoption. Cross-regional impacts vary based on regulatory environments, with markets having stringent data protection laws showing greater sensitivity to security concerns. Organizations must invest in advanced security features, employee training programs, and comprehensive data governance frameworks to address these challenges effectively.

Opportunities:

Internet of Things (IoT) and Edge Computing Integration:

The proliferation of IoT devices and edge computing architectures creates substantial opportunities for specialized external storage solutions designed to handle distributed data processing and local storage requirements. IoT deployments generate massive amounts of sensor data, video surveillance content, and operational telemetry that require local storage capabilities before cloud transmission or processing. Edge computing implementations demand high-performance, reliable storage systems that can operate in challenging environmental conditions while providing real-time data access for critical applications. This opportunity encompasses developing ruggedized storage devices optimized for industrial environments, creating intelligent storage management systems that can prioritize data based on business value, and establishing partnerships with IoT platform providers to deliver integrated solutions. Market sectors affected include smart cities, industrial automation, autonomous vehicles, and healthcare monitoring systems. The growth potential extends to specialized storage architectures, real-time analytics capabilities, and hybrid cloud-edge storage management platforms.

Professional Content Creation and Media Production:

The explosive growth in professional content creation, video production, and digital media consumption creates significant opportunities for high-performance external storage solutions tailored to creative workflows and media production requirements. Content creators, video editors, photographers, and media production companies require storage systems that can handle large file sizes, provide fast data transfer speeds, and offer reliable backup capabilities for valuable creative assets. This niche market demands specialized features including high-capacity storage, professional-grade reliability, seamless integration with creative software applications, and collaborative access capabilities for distributed production teams. Success enablers include partnerships with content creation software providers, development of industry-specific storage solutions, and creation of comprehensive media asset management platforms that integrate with existing creative workflows. The opportunity extends to cloud-hybrid storage solutions that enable collaborative editing, automated backup systems for creative assets, and specialized storage architectures optimized for media production environments.

Trends:

Solid-State Drive (SSD) Technology Adoption and Performance Enhancement:

The external storage industry is experiencing a fundamental shift toward solid-state drive technology, driven by dramatically improved performance characteristics, enhanced durability, and rapidly declining cost structures. SSDs offer superior data transfer speeds, lower power consumption, increased resistance to physical shock, and silent operation compared to traditional mechanical hard drives. This transformation affects both consumer and enterprise segments, with consumers seeking faster boot times and application loading while enterprises prioritize improved system responsiveness and reduced maintenance requirements. Advanced SSD technologies including NVMe interfaces, 3D NAND flash memory, and intelligent controller algorithms continue to push performance boundaries while maintaining reliability standards. The trend encompasses development of specialized SSD solutions for specific applications, integration of AI-powered storage optimization, and creation of hybrid storage architectures that combine SSD performance with traditional HDD capacity for cost-effective storage tiers.

Artificial Intelligence and Intelligent Storage Management:

The integration of artificial intelligence and machine learning technologies into storage systems represents a transformative trend that enhances data management efficiency, predictive maintenance capabilities, and automated optimization functions. AI-powered storage solutions can analyze usage patterns, predict hardware failures, optimize data placement for performance, and automate backup and archival processes based on content analysis and business priorities. This trend responds to growing data complexity, increasing storage management overhead, and demand for proactive maintenance approaches that minimize downtime and data loss risks. Behavioral shifts toward intelligent automation and regulatory changes supporting AI-driven data governance create favorable conditions for widespread adoption. The transformation includes development of self-managing storage systems, integration with business intelligence platforms, and creation of predictive analytics capabilities that enable proactive storage capacity planning and performance optimization across diverse enterprise environments.

Recent Development

In May 2025: Silicon Motion Technology Corporation, a recognized innovator in NAND-flash controller design, has unveiled its newest solid-state drive breakthroughs. Center stage were two next-generation chips: the SM2504XT PCIe Gen5 SSD controller and the SM2324 USB4 portable SSD controller. Both solutions are engineered to deliver substantial gains in speed and power efficiency, addressing surging demand for ultra-high-performance storage devices.

In January 2025: CORSAIR has launched the EX400U USB4 External SSD, establishing new benchmarks for portable storage through remarkable transfer performance and compact design. Harnessing USB4's advanced bandwidth capabilities, this external drive achieves impressive sequential read rates reaching 4,000MB/sec and write speeds up to 3,600MB/sec. From high-definition video editing to large-scale project management and bulk file transfers, the EX400U dramatically minimizes processing delays, enabling users to concentrate on their core productivity tasks.

Frequently Asked Questions

How big is the External Storage Market?

Global External Storage Market to reach USD 407.90B by 2034, growing at a CAGR of 28.95%. Explore key trends, drivers, and growth opportunities in the sector.

Who are the major players in the External Storage Market?

Western Digital Corporation, Infortrend Technology Inc., Seagate Technology, Oracle Corporation, Toshiba Corporation, Samsung Electronics Co., Ltd., Lenovo Group Limited, Synology Inc., NetApp Inc.sss, Micron Technology Inc., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), IBM Corporation, Kingston Technology Company Inc., Fujitsu Ltd., Hitachi Vantara, Pure Storage Inc., ADATA Technology Co., Ltd., LaCie (Seagate subsidiary), G-Technology (Western Digital subsidiary), Quantum Corporation, Transcend Information Inc., Promise Technology Inc., Thecus Technology Corp., QNAP Systems, Inc.

Which segments covered the External Storage Market?

Storage Type (Flash Memory Devices, Professional Optical Storage, Solid State Storage, External Hard Drives); Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

; Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

; Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

; Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

; Application(Enterprise Storage, Consumer Electronics, Industrial Applications, Healthcare Devices, Automotive Applications, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")