- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Fetal Bovine Serum Replacement Market Forecast 2034 | CAGR 13.6%

Global Fetal Bovine Serum Replacement Market Size, Share, Growth & Industry Analysis By Product Type (Chemically Defined Media, Serum-Free Basal Media, Protein-Free Media, Plant-Derived Hydrolysates, Recombinant Growth Factors), By End-Use Application (Biopharma Manufacturing, Cell & Gene Therapy, Research, Cultivated Meat, Diagnostics), By Cell Type (CHO Cells, T Cells, iPSCs, Primary Cells) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

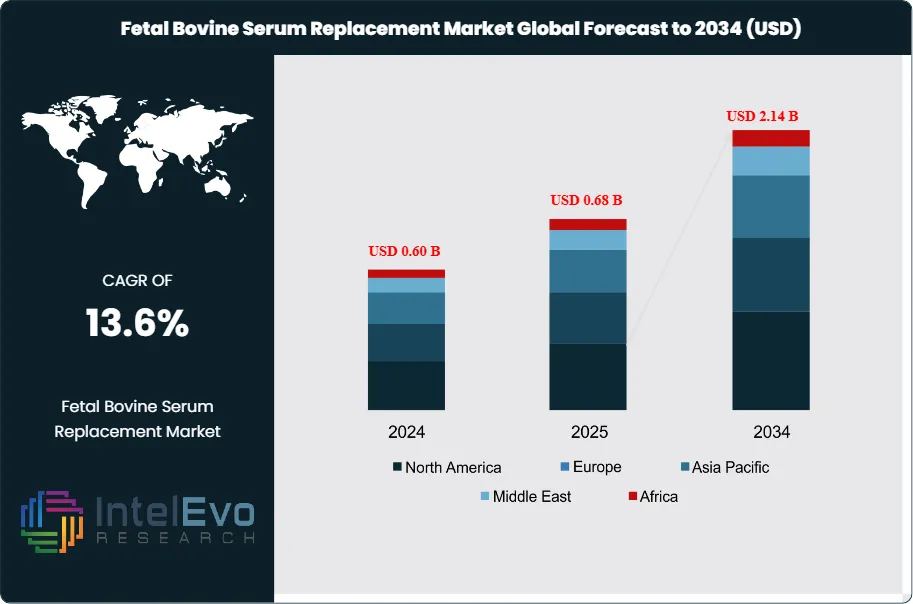

| USD 0.68 Billion | USD 2.14 Billion | 13.6% | North America, 39.7% |

The Fetal Bovine Serum Replacement Market was valued at approximately USD 0.60 Billion in 2024 and reached USD 0.68 Billion in 2025. The market is projected to grow to USD 2.14 Billion by 2034, expanding at a CAGR of 13.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.46 Billion over the analysis period, driven by stringent regulatory pressure to eliminate animal-derived components from biopharmaceutical manufacturing, rapid expansion of cell and gene therapy clinical pipelines, and intensifying ethical scrutiny over the use of fetal bovine serum in cell culture applications.

Get More Information about this report -

Request Free Sample ReportFetal bovine serum (FBS) has served as the standard supplement for mammalian cell culture since the 1950s, providing a complex mixture of growth factors, hormones, and attachment proteins that support cell proliferation and viability. Despite its widespread adoption, FBS presents significant disadvantages for commercial biopharmaceutical manufacturing, including lot-to-lot variability, risk of adventitious agent contamination, inconsistent regulatory approval documentation, and ethical concerns related to collection practices. The fetal bovine serum replacement market encompasses serum-free media formulations, chemically defined media, protein-free media, recombinant growth factor supplements, and plant-derived hydrolysate systems that replicate or exceed FBS performance across diverse cell culture applications without reliance on animal components.

Several converging regulatory and commercial forces are reshaping the fetal bovine serum replacement market. The FDA's Guidance for Industry on cell therapy manufacturing and the EMA's guidelines on Good Manufacturing Practice for Advanced Therapy Medicinal Products both explicitly recommend elimination of animal-derived components from manufacturing processes where technically feasible, citing adventitious agent risk and batch reproducibility requirements. The International Council for Harmonisation ICH Q5A guideline on viral safety of biotechnology products further reinforces this imperative for biologics manufacturers. In the cell and gene therapy sector, CAR-T cell manufacturing platforms, NK cell expansion systems, and iPSC derivation protocols require serum-free, xeno-free culture conditions to meet FDA CBER requirements for clinical-grade material production.

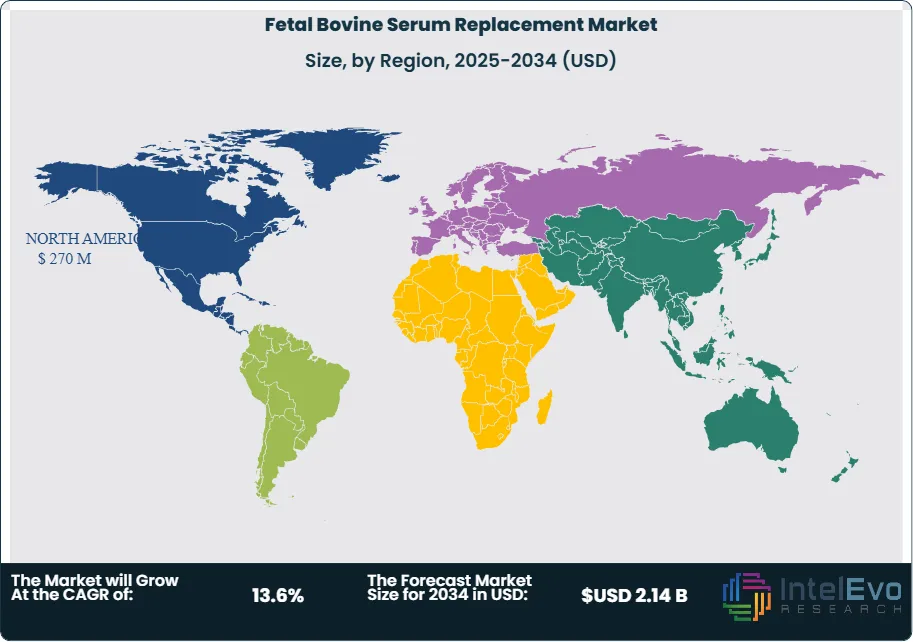

The cultivated meat sector represents an emerging high-volume demand driver for the fetal bovine serum replacement market, as food technology companies must eliminate FBS from cell-based meat production to achieve regulatory approval for human food products. The FDA and USDA jointly regulate cultivated meat in the US under a framework that requires demonstration of food-safety-compliant culture media, directly accelerating serum-free media adoption in this new application segment. North America dominated the fetal bovine serum replacement market with a 39.7% share in 2025, equivalent to USD 270 Million, supported by the world's largest biopharmaceutical manufacturing base and extensive NIH and BARDA funding for cell and gene therapy development. Asia Pacific is the fastest-growing regional market, expanding at a projected CAGR of 15.8% through 2034.

, By End-Use Application (Biopharma Manufacturing, Cell & Gene Therapy, Research, Cultivated Meat, Diagnostics), By Cell Type (CHO Cells, T Cells, iPSCs, Primary Cells) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global fetal bovine serum replacement market was valued at USD 0.68 Billion in 2025 and is forecast to reach USD 2.14 Billion by 2034, registering a CAGR of 13.6% during the 2026-2034 forecast period.

- Segment Dominance: By product type, chemically defined media held the largest share at 42.3% of the fetal bovine serum replacement market in 2025, reflecting its critical role in biopharmaceutical GMP manufacturing where batch reproducibility and regulatory compliance are non-negotiable.

- Segment Dominance: By end-use application, biopharmaceutical manufacturing accounted for 46.8% of fetal bovine serum replacement market revenues in 2025, driven by monoclonal antibody production, CAR-T cell manufacturing, and viral vector biomanufacturing protocols requiring animal-component-free culture systems.

- Driver: FDA and EMA regulatory pressure to eliminate animal-derived components from biopharmaceutical manufacturing processes is compelling manufacturers to transition to serum-free alternatives, with ICH Q5A viral safety requirements reducing FBS-using processes among cGMP cell culture operations by an estimated 22% between 2022 and 2025.

- Restraint: Performance gaps in serum-free media for certain primary cell types and suspension culture applications constrain adoption, with an estimated 35% of academic and research laboratories reporting incomplete substitutability of chemically defined alternatives for complex primary cell culture as of 2025.

- Opportunity: The cultivated meat industry, projected to represent USD 6.0 Billion in global revenues by 2034, requires food-grade serum-free cell culture media for skeletal muscle cell expansion, creating a new high-volume addressable market for fetal bovine serum replacement suppliers.

- Trend: Adoption of recombinant albumin and recombinant insulin as functional serum-free media components grew at approximately 19.4% annually in 2025, reflecting the shift toward fully chemically defined, lot-consistent media formulations in pharmaceutical manufacturing.

- Regional Analysis: North America led the fetal bovine serum replacement market with a 39.7% share, equivalent to USD 270 Million in 2025, supported by a dense biopharmaceutical manufacturing base, robust cell and gene therapy clinical activity, and FDA regulatory guidance favoring animal-component-free manufacturing.

Competitive Landscape Overview

The fetal bovine serum replacement market is moderately fragmented, with the top four suppliers — Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), Sartorius AG, and Corning Inc. — collectively accounting for approximately 52% of global market revenues in 2025. Competition is primarily technology-driven, centered on proprietary serum-free media formulation depth, the ability to offer chemically defined alternatives for a broad range of cell types, and speed of regulatory documentation support for cGMP manufacturing transitions. M&A activity accelerated in 2024-2025 as large life science tools companies acquired specialty media formulators to expand their animal-component-free portfolios. Nucleus Biologics and FUJIFILM Irvine Scientific are the most prominent challengers, competing on rapid customization speed and supply chain reliability for emerging biotech clients.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Thermo Fisher Scientific | USA | Leader | StemPro-34 SFM / Gibco Serum-Free Media | North America & Europe | Launched expanded xeno-free, serum-free media portfolio for CAR-T cell manufacturing in Q1 2025. |

| Merck KGaA (MilliporeSigma) | Germany | Leader | EX-CELL Advanced Serum-Free Media | Europe & North America | Expanded EX-CELL line with new suspension CHO media targeting monoclonal antibody production; March 2025. |

| Sartorius AG | Germany | Leader | BioOsmoShock-Free & PM-CHO Media | Europe & Asia Pacific | Acquired a specialty cell culture media developer to strengthen serum-free formulation portfolio; Q2 2025. |

| Corning Inc. | USA | Leader | BioCoat & Synthecon Serum-Free Media | North America | Launched a chemically defined, animal-component-free media line for viral vector manufacturing; June 2025. |

| FUJIFILM Irvine Scientific | USA | Challenger | IS CHO-CD & SFM4CHO Serum-Free Media | North America & Asia Pacific | Signed CDMO supply agreement with a South Korean biologics manufacturer for serum-free media supply; 2025. |

| Nucleus Biologics | USA | Challenger | Triton Serum-Free Media Platform | North America | Raised USD 55M Series C in February 2025 to expand rapid, personalized serum-free media formulation services. |

| PromoCell GmbH | Germany | Niche Player | Serum-Free Cell Culture Media Range | Europe | Expanded serum-free endothelial and smooth muscle cell culture lines for cardiovascular research; Q3 2025. |

| Pan-Biotech GmbH | Germany | Niche Player | Cell-Evo Serum-Free Media | Europe | Launched Cell-Evo animal-component-free media for iPSC and organoid research applications; 2025. |

| ScienCell Research Laboratories | USA | Niche Player | ScienCell Serum-Free Specialty Media | North America | Extended specialty serum-free media catalog to 18 new primary cell types for immuno-oncology research; 2025. |

| Ajinomoto Co. | Japan | Challenger | CDM-HD Chemically Defined Media | Asia Pacific | Partnered with a leading Japanese cell therapy company to supply CDM-HD for allogeneic NK cell manufacturing; Jan 2026. |

By Product Type

The fetal bovine serum replacement market by product type encompasses chemically defined media, serum-free basal media with defined supplements, protein-free media, plant-derived hydrolysate supplements, and recombinant protein supplements. Chemically defined media held the dominant share at 42.3% of the fetal bovine serum replacement market in 2025, equivalent to approximately USD 288 Million. These formulations specify the identity and concentration of every component, eliminating biological variation and enabling precise regulatory documentation. Pharmaceutical manufacturers adopting continuous biomanufacturing platforms are particularly dependent on chemically defined media to meet FDA process analytical technology (PAT) requirements, as lot-to-lot variation in serum-containing media would invalidate process control strategies. Leading chemically defined media products include the EX-CELL Advanced series from Merck KGaA and the CD OptiCHO system from Thermo Fisher Scientific, both of which are validated for licensed monoclonal antibody manufacturing processes.

Serum-free basal media with defined supplements held a 28.7% share of the fetal bovine serum replacement market in 2025. These formulations replace FBS with purified recombinant proteins, transferrin, insulin, selenium, and lipid supplements, offering improved batch consistency over conventional serum-containing media while avoiding full chemical definition. They serve research-grade cell culture and early-stage clinical manufacturing where full chemical definition is not yet required. Protein-free media, which eliminates all protein components to facilitate downstream purification of recombinant proteins, accounted for 14.2% of the fetal bovine serum replacement market in 2025. Plant-derived hydrolysates and peptone supplements represented 9.6% of the market, serving microbial fermentation and some mammalian cell culture applications. Recombinant growth factor and cytokine supplements for serum-free media formulation, including recombinant albumin, recombinant transferrin, and recombinant insulin analogs, held the remaining 5.2% of the fetal bovine serum replacement product market in 2025 and are the fastest-growing sub-segment.

By End-Use Application

The fetal bovine serum replacement market by end-use application reveals biopharmaceutical manufacturing as the revenue leader with a 46.8% share in 2025, equivalent to approximately USD 318 Million. Within this segment, monoclonal antibody production via CHO cell culture represents the largest single application, where chemically defined serum-free media are now standard practice across cGMP manufacturing facilities operated by large biopharmaceutical companies. Viral vector manufacturing for gene therapy, including adeno-associated virus (AAV) and lentiviral vector production, is the fastest-growing sub-application within biopharmaceutical manufacturing, requiring specialized serum-free HEK293 and HeLa cell culture media validated to CBER standards. CAR-T cell manufacturing protocols at companies including Novartis and Bristol-Myers Squibb have transitioned entirely to xeno-free, serum-free T-cell expansion media to satisfy FDA CBER GTP compliance requirements.

Cell and gene therapy research accounted for 22.4% of the fetal bovine serum replacement market in 2025. iPSC derivation and differentiation, organoid culture, and ex vivo cell expansion for adoptive cell therapy trials all require serum-free conditions to meet regulatory expectations for clinical-grade material. Academic and basic research institutions represented 16.3% of the market, driven by university policies in the EU and UK mandating phaseout of FBS from non-essential research applications under the 3Rs framework for animal use reduction. The cultivated meat and food technology sector held a 7.2% share in 2025 but represents the highest-growth application segment at an estimated CAGR of 24.8% through 2034. Diagnostics, biosensor development, and other specialty applications accounted for the remaining 7.3% of the fetal bovine serum replacement market in 2025.

By Cell Type

The fetal bovine serum replacement market by cell type served spans CHO and other recombinant mammalian cell lines, T cells and other immune cell types, iPSCs and pluripotent stem cells, primary cells, and microbial and insect cell systems. CHO cell culture, the workhorse of monoclonal antibody and recombinant protein biomanufacturing, represented the largest cell-type segment at 38.4% of the fetal bovine serum replacement market in 2025. CHO-compatible serum-free and chemically defined media have achieved the highest technology maturity in the market, with multiple commercially validated formulations offering performance parity with serum-containing counterparts in terms of cell growth, viability, and protein productivity. T-cell expansion media for CAR-T and TCR therapy manufacturing accounted for 19.7% of the cell-type segment, reflecting the rapid growth of the cell therapy clinical pipeline.

iPSC and pluripotent stem cell culture media represented 16.2% of the fetal bovine serum replacement market in 2025. These applications demand the most stringent xeno-free and feeder-free conditions, as any animal-derived contamination in iPSC-derived cell therapies or their differentiation products creates regulatory rejection risk at the FDA and EMA. Primary cell culture, encompassing endothelial cells, smooth muscle cells, neurons, hepatocytes, and myosatellite cells, held a 14.3% share of the cell-type segment in 2025. Primary cells present the greatest technical challenge for serum-free media developers because of their sensitivity to growth factor composition and attachment factor requirements. Insect cell systems (Sf9, Sf21, Hi5) used for baculovirus-expressed recombinant protein production and microbial fermentation applications accounted for the remaining 11.4% of the fetal bovine serum replacement market by cell type in 2025.

By End-User

The fetal bovine serum replacement market by end-user segments into biopharmaceutical and biotechnology companies, academic research institutions, contract development and manufacturing organizations (CDMOs), food and cultivated meat companies, and diagnostic and medical device manufacturers. Biopharmaceutical and biotechnology companies held the largest end-user share at 48.6% of the fetal bovine serum replacement market in 2025. These organizations drive demand for validated, regulatory-compliant chemically defined media across monoclonal antibody, bispecific antibody, ADC, and cell therapy manufacturing platforms. CDMOs representing organizations such as Lonza, Samsung Biologics, and Catalent held a 18.4% market share in 2025, as CDMO clients increasingly specify serum-free process conditions as a mandatory requirement in manufacturing service agreements. Academic and government research institutions accounted for 19.7% of the end-user market, while food and cultivated meat companies and diagnostic manufacturers represented the remaining 13.3% of the fetal bovine serum replacement market by end-user in 2025.

Regional Analysis

North America

North America fetal bovine serum replacement market held a 39.7% share in 2025, generating approximately USD 270 Million in revenue. The United States is the dominant national market, accounting for over 90% of the regional total, driven by the world's largest concentration of biopharmaceutical manufacturing facilities, a high density of cell and gene therapy clinical programs, and FDA regulatory guidance explicitly favoring animal-component-free manufacturing. The FDA's Center for Biologics Evaluation and Research has published guidance documents that effectively make serum-free, chemically defined media a preferred standard for BLA submissions involving cell-based drug products, viral vectors, and advanced therapy medicinal products. BARDA's investments in domestic biomanufacturing resilience, exceeding USD 3 Billion since 2022, are accelerating adoption of standardized serum-free media platforms across federally supported manufacturing preparedness programs. Canada contributes through a growing cell therapy manufacturing sector in Toronto and Vancouver, where provincial biotech investment programs support serum-free process development. Mexico is an emerging consumer of serum-free media as its pharmaceutical contract manufacturing sector scales.

Europe

Europe fetal bovine serum replacement market represented 28.4% of global revenues in 2025, equivalent to USD 193 Million. Germany leads the European market, hosting major serum-free media producers including Merck KGaA and PromoCell, alongside a large biopharmaceutical manufacturing base at companies such as Bayer, Boehringer Ingelheim, and BioNTech. The EMA's GMP guidelines for Advanced Therapy Medicinal Products under Regulation (EC) No 1394/2007 require elimination of animal-derived components where technically feasible, creating binding regulatory pressure on cell and gene therapy manufacturers across EU member states. The UK's Medicines and Healthcare products Regulatory Agency has adopted aligned requirements under its post-Brexit regulatory framework, sustaining serum-free media demand in a significant European market. Denmark benefits from proximity to Novonesis's biotechnology infrastructure and hosts a growing number of cell therapy startups transitioning to animal-component-free culture systems. France and the Netherlands each represent substantial demand centers, driven by vaccine manufacturing and monoclonal antibody production facilities that have completed FBS phaseout programs. The 3Rs framework on animal use reduction in research, enforced across EU member states through Directive 2010/63/EU, is mandating FBS reduction in academic cell culture applications, broadening demand beyond commercial manufacturing.

Asia Pacific

Asia Pacific fetal bovine serum replacement market held approximately 22.6% of global revenues in 2025, generating USD 154 Million, and represents the fastest-growing regional market at a projected CAGR of 15.8% through 2034. Japan is the most technically advanced national market within the region, with the Act on the Safety of Regenerative Medicine creating a structured regulatory framework for cell therapy manufacturing that actively incentivizes serum-free and xeno-free culture conditions. Ajinomoto Co. is the most significant domestic serum-free media supplier in Japan, serving cell therapy and vaccine manufacturing clients across the country. China is the largest Asia Pacific market by revenue, where rapid biosimilar and monoclonal antibody manufacturing capacity expansion is driving demand for chemically defined serum-free media validated to China NMPA cGMP standards. South Korea's large and technically sophisticated biosimilar manufacturing industry, led by Samsung Biologics and Celltrion, has substantially completed FBS phaseout for CHO cell-based manufacturing processes, sustaining ongoing demand for serum-free media. India represents the fastest-growing individual national market within the region, driven by pharmaceutical API manufacturing modernization and cell-based vaccine manufacturing programs funded by the government's National Biotechnology Development Strategy.

Latin America

Latin America held approximately 5.8% of the fetal bovine serum replacement market in 2025, generating approximately USD 39 Million. Brazil is the dominant regional market, where ANVISA's cGMP requirements for biopharmaceutical manufacturing are progressively aligning with ICH guidelines, compelling manufacturers producing biologics for domestic or export markets to document and justify animal-derived component use. FIOCRUZ, Brazil's largest public health and biomedical research institution, has implemented institutional policies to phase out FBS from research applications under 3Rs principles, creating academic sector demand for serum-free alternatives. Argentina represents the second-largest Latin American fetal bovine serum replacement market, with pharmaceutical manufacturing companies supplying both domestic and regional export markets adopting chemically defined media to meet quality requirements. Mexico contributes through pharmaceutical contract manufacturing operations affiliated with global biopharmaceutical companies that mandate serum-free manufacturing standards under their supplier qualification requirements. Infrastructure constraints including limited cold-chain logistics for sensitive serum-free media formulations and lower awareness of serum-free alternatives among small academic institutions constrain regional growth relative to North America and Europe.

Middle East & Africa

The Middle East and Africa region represented approximately 3.5% of the fetal bovine serum replacement market in 2025, generating USD 24 Million. The UAE and Saudi Arabia are the primary demand centers within the region, where government healthcare investment programs including Saudi Vision 2030 are building domestic biopharmaceutical manufacturing capacity that increasingly references ICH guidelines and FDA/EMA GMP standards. Saudi Arabia's King Abdulaziz City for Science and Technology (KACST) has funded cell therapy research programs at King Faisal Specialist Hospital that require serum-free culture conditions, contributing to specialized demand. South Africa leads the African fetal bovine serum replacement market through vaccine manufacturing operations at the Biovac Institute and other facilities that are transitioning production processes toward animal-component-free standards to satisfy WHO prequalification requirements for vaccine supply to international health programs. The region remains heavily dependent on imported serum-free media formulations from North American and European suppliers, with limited domestic manufacturing capacity for serum-free media, presenting both a supply chain vulnerability and a long-term investment opportunity.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Chemically Defined Media

- Serum-Free Basal Media with Defined Supplements

- Protein-Free Media

- Plant-Derived Hydrolysate Supplements

- Recombinant Growth Factor & Cytokine Supplements

By End-Use Application

- Biopharmaceutical Manufacturing

- Cell & Gene Therapy Research

- Academic & Basic Research

- Cultivated Meat & Food Technology

- Diagnostics & Other Specialty Applications

By Cell Type

- CHO & Recombinant Mammalian Cell Lines

- T Cells & Immune Cell Types

- iPSCs & Pluripotent Stem Cells

- Primary Cells

- Insect & Microbial Cell Systems

By End-User

- Biopharmaceutical & Biotechnology Companies

- Academic & Government Research Institutions

- Contract Development & Manufacturing Organizations (CDMOs)

- Cultivated Meat & Food Companies

- Diagnostic & Medical Device Manufacturers

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.68 B |

| Forecast Revenue (2034) | USD 2.14 B |

| CAGR (2025-2034) | 13.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Chemically Defined Media, Serum-Free Basal Media with Defined Supplements, Protein-Free Media, Plant-Derived Hydrolysate Supplements, Recombinant Growth Factor & Cytokine Supplements), By End-Use Application, (Biopharmaceutical Manufacturing, Cell & Gene Therapy Research, Academic & Basic Research, Cultivated Meat & Food Technology, Diagnostics & Other Specialty Applications), By Cell Type, (CHO & Recombinant Mammalian Cell Lines, T Cells & Immune Cell Types, iPSCs & Pluripotent Stem Cells, Primary Cells, Insect & Microbial Cell Systems), By End-User, (Biopharmaceutical & Biotechnology Companies, Academic & Government Research Institutions, Contract Development & Manufacturing Organizations (CDMOs), Cultivated Meat & Food Companies, Diagnostic & Medical Device Manufacturers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, CORNING INC., FUJIFILM IRVINE SCIENTIFIC, NUCLEUS BIOLOGICS, AJINOMOTO CO., PROMOCELL GMBH, PAN-BIOTECH GMBH, SCIENCELL RESEARCH LABORATORIES, LONZA GROUP AG, CYTIVA (DANAHER), CELLERO (NOVATEK INTERNATIONAL), HIMEDIA LABORATORIES, BIOLOGICAL INDUSTRIES (SARTORIUS), BIOWEST SAS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use Application (Biopharma Manufacturing, Cell & Gene Therapy, Research, Cultivated Meat, Diagnostics), By Cell Type (CHO Cells, T Cells, iPSCs, Primary Cells) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Biopharma Manufacturing, Cell & Gene Therapy, Research, Cultivated Meat, Diagnostics), By Cell Type (CHO Cells, T Cells, iPSCs, Primary Cells) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Biopharma Manufacturing, Cell & Gene Therapy, Research, Cultivated Meat, Diagnostics), By Cell Type (CHO Cells, T Cells, iPSCs, Primary Cells) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Fetal Bovine Serum Replacement Market?

Global FBS replacement market valued at USD 0.60B in 2024, reaching USD 2.14B by 2034, growing at a CAGR of 13.6% from 2026–2034.

Who are the major players in the Fetal Bovine Serum Replacement Market?

THERMO FISHER SCIENTIFIC, MERCK KGAA (MILLIPORESIGMA), SARTORIUS AG, CORNING INC., FUJIFILM IRVINE SCIENTIFIC, NUCLEUS BIOLOGICS, AJINOMOTO CO., PROMOCELL GMBH, PAN-BIOTECH GMBH, SCIENCELL RESEARCH LABORATORIES, LONZA GROUP AG, CYTIVA (DANAHER), CELLERO (NOVATEK INTERNATIONAL), HIMEDIA LABORATORIES, BIOLOGICAL INDUSTRIES (SARTORIUS), BIOWEST SAS, OTHERS

Which segments covered the Fetal Bovine Serum Replacement Market?

By Product Type, (Chemically Defined Media, Serum-Free Basal Media with Defined Supplements, Protein-Free Media, Plant-Derived Hydrolysate Supplements, Recombinant Growth Factor & Cytokine Supplements), By End-Use Application, (Biopharmaceutical Manufacturing, Cell & Gene Therapy Research, Academic & Basic Research, Cultivated Meat & Food Technology, Diagnostics & Other Specialty Applications), By Cell Type, (CHO & Recombinant Mammalian Cell Lines, T Cells & Immune Cell Types, iPSCs & Pluripotent Stem Cells, Primary Cells, Insect & Microbial Cell Systems), By End-User, (Biopharmaceutical & Biotechnology Companies, Academic & Government Research Institutions, Contract Development & Manufacturing Organizations (CDMOs), Cultivated Meat & Food Companies, Diagnostic & Medical Device Manufacturers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Fetal Bovine Serum Replacement Market

Published Date : 17 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date