- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Fiberglass Pipes Market Size & Growth Outlook | CAGR 5.8%

Global Fiberglass Pipes Market Size, Share & Analysis By Product Type, (GRP Pipes, GRE Pipes, Other Product Types), By Fiber Type, (T/ S/ R Glass, E-glass, Other Fiber Types), By End-User Industry, Corrosion Resistance Benefits, Regional Demand & Forecast 2025–2034

Report Overview

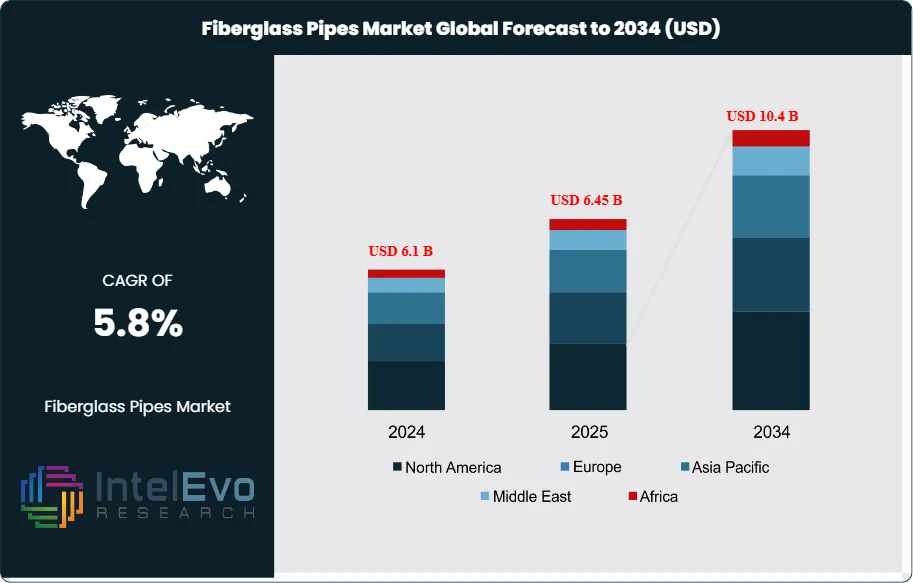

The Fiberglass Pipes Market is valued at approximately USD 6.1 billion in 2024 and is projected to reach nearly USD 10.4 billion by 2034, expanding at a CAGR of around 5.8% from 2025 to 2034. Growing demand for corrosion-resistant, high-efficiency piping systems across oil & gas, water treatment, and chemical industries is accelerating global adoption. Infrastructure modernization, energy transition in emerging markets, and advancements in composite materials are poised to reshape competitive dynamics through the next decade.

Get More Information about this report -

Request Free Sample ReportThis steady growth trajectory reflects the increasing preference for fiberglass pipes as an advanced alternative to conventional materials such as steel, concrete, and PVC. Historically, the market has benefitted from the expansion of industrial infrastructure, particularly in oil and gas and chemical processing, where reliability, corrosion resistance, and durability are paramount. More recently, rising investments in water and wastewater management projects, coupled with stricter environmental standards, have further supported adoption.

Key demand drivers include the pipes’ lightweight structure, ease of installation, and low lifecycle costs, which make them attractive for large-scale projects requiring long service lives and minimal maintenance. In oil and gas, glass-reinforced epoxy (GRE) pipes have emerged as a dominant product segment, widely deployed in both offshore and onshore exploration activities due to their high pressure-handling capacity and resistance to harsh environments. Similarly, sectors such as irrigation, sewage, and chemicals increasingly turn to fiberglass pipes to ensure operational efficiency and regulatory compliance. On the supply side, however, fluctuating raw material costs and the relatively high upfront capital requirements remain challenges that could temper near-term expansion.

Technological innovation is playing a decisive role in reshaping the market. Advances in resin formulations, automated winding processes, and AI-assisted design are improving the strength-to-weight ratio, enabling customized solutions and driving down installation timelines. Digital monitoring systems integrated with pipeline networks are also enhancing predictive maintenance, further amplifying cost savings and operational resilience.

Regionally, Asia-Pacific dominates global consumption, underpinned by government-backed infrastructure programs in China, India, and Southeast Asia, where water management and energy transportation are critical priorities. North America and the Middle East are also key investment hotspots, with oil and gas projects fueling demand for high-performance pipe systems. Europe’s emphasis on sustainable infrastructure and stringent environmental regulations provides additional growth avenues, particularly in wastewater treatment and industrial applications. Collectively, these dynamics position fiberglass pipes as a strategically important material for industries seeking efficiency, durability, and compliance, making the sector an increasingly attractive domain for long-term investment.

, By Fiber Type, (T/ S/ R Glass, E-glass, Other Fiber Types), By End-User Industry, Corrosion Resistance Benefits, Regional Demand & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global fiberglass pipes market is projected to expand from USD 6.1 billion in 2024 to approximately USD 10.4 billion by 2034, reflecting a CAGR of 5.8% over 2025–2034. Growth is fueled by rising demand for lightweight, corrosion-resistant, and cost-efficient piping solutions across industrial and infrastructure sectors.

- Product Type: Glass Reinforced Epoxy (GRE) pipes accounted for 47.9% of total revenues in 2024, driven by their superior performance in high-pressure and high-temperature environments, particularly in oil and gas exploration and production.

- Fiber Type: E-glass fiber held over 55% market share in 2024 due to its excellent resistance to acidic corrosion, making it the preferred choice in chemical processing and wastewater treatment applications.

- Driver: Expanding oil and gas infrastructure is a key demand catalyst, as fiberglass pipes reduce operating costs through low maintenance and extended service life. Offshore drilling projects in the Middle East and shale gas development in North America are particularly accelerating adoption.

- Restraint: High raw material costs, especially resins and specialty glass fibers, continue to constrain profitability. Price volatility can inflate project budgets by 8–12%, limiting uptake in cost-sensitive developing markets.

- Opportunity: China’s transition from coal to natural gas is expected to significantly boost demand for fiberglass pipelines, with potential multi-billion-dollar investments in gas transmission infrastructure creating long-term growth prospects.

- Trend: Technological advancements in automated filament winding and AI-driven pipe design are enhancing efficiency and customization. Digital monitoring systems embedded in pipelines are emerging as a disruptive innovation, enabling predictive maintenance and reducing lifecycle costs by up to 20%.

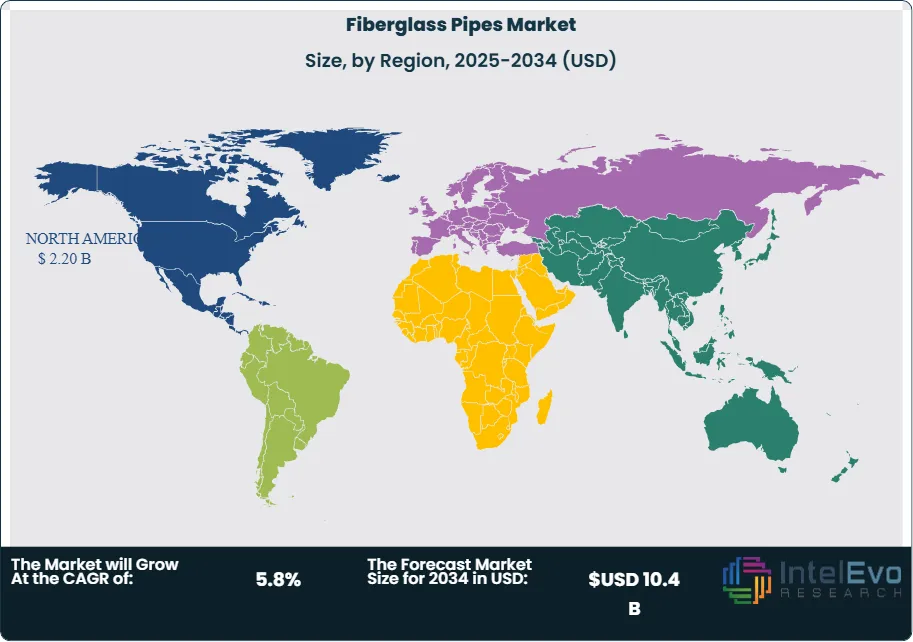

- Regional Analysis: North America led the market in 2024 with a 36% revenue share, valued at USD 1.6 billion, supported by large-scale energy and municipal infrastructure projects. Meanwhile, Asia-Pacific is poised for the fastest growth, with government-backed water and wastewater initiatives in India, China, and Southeast Asia expected to elevate regional CAGR above the global average.

Product Type Analysis

The fiberglass pipes market continues to be led by Glass Reinforced Epoxy (GRE) pipes, which accounted for nearly 48% of global revenues in 2024 and are expected to maintain dominance through 2030. GRE pipes are widely adopted in oil and gas exploration, offshore platforms, and industrial applications due to their ability to withstand extreme pressure, high temperatures, and corrosive environments. Their approval by international regulatory bodies such as the International Maritime Organization (IMO) for marine fire endurance applications has further enhanced credibility, boosting uptake in critical infrastructure projects. By 2025, demand is projected to accelerate, particularly across offshore oil and gas developments in the Middle East and subsea projects in Asia.

Glass Reinforced Plastic (GRP) pipes, including epoxy, polyester, and vinyl ester resin systems, are also experiencing robust growth. Epoxy-based GRP, in particular, has gained traction owing to its superior chemical resistance, making it a preferred solution in hydrocarbon transport and chemical processing. Market consolidation and expansion strategies, such as NOV’s acquisition of Denali Incorporated and the establishment of advanced fiberglass manufacturing plants in Saudi Arabia, highlight the segment’s strategic significance. These developments underscore how manufacturers are scaling capacity to meet rising demand from industrial, water treatment, and resource transport applications.

The broader adoption of GRE and GRP pipes reflects their competitive advantage over conventional steel and concrete systems. Lighter weight, ease of installation, dimensional stability, and immunity to corrosion make them attractive for wastewater management, desalination plants, and potable water projects. With the global water demand expected to rise by 30% by 2035, GRE and GRP pipes are positioned as critical enablers of sustainable water infrastructure.

Fiber Type Analysis

E-glass fiber dominated the market with more than 55% share in 2024 and remains the most widely used reinforcement material in fiberglass pipes. Its alumino-borosilicate composition provides high strength-to-weight performance and exceptional resistance to acidic corrosion, making it suitable for applications ranging from municipal sewer systems to chemical processing pipelines. E-glass reinforced pipes also excel in trenchless installations, micro-tunneling, and relining projects, where smooth internal surfaces and structural reliability reduce operational costs.

The increasing scale of chemical production is a key driver for E-glass adoption. With China and India expanding their petrochemical capacities and Europe modernizing plants, the need for durable, corrosion-resistant piping continues to rise. According to the European Chemical Industry Council, global chemical output is expected to grow at 3% annually through 2030, supporting demand for E-glass–reinforced pipes across process industries. Major producers such as PPG Industries, Saint-Gobain Vetrotex, and Nippon Electric Glass are investing in R&D to enhance fiber performance and extend its use in high-pressure and environmentally sensitive applications.

Other fiber types, including S-glass and T-glass, are gaining traction in niche, high-performance environments. Their enhanced thermal stability and tensile strength make them suitable for aerospace-grade composites and specialized industrial pipelines. While their share remains smaller compared to E-glass, the increasing demand for tailored solutions in energy and infrastructure projects suggests incremental growth opportunities over the next decade.

End-Use Analysis

The oil and gas sector remains the leading consumer of fiberglass pipes, accounting for over 40% of global revenues in 2024. This dominance is expected to persist as major energy-producing regions invest heavily in exploration, transportation, and refinery upgrades. Fiberglass pipes provide critical advantages over metal counterparts—chiefly their resistance to corrosion in saline and hydrocarbon-rich environments and their lighter weight, which reduces logistical costs for offshore rigs and remote installations. With global offshore oil production projected to increase by 15% by 2030, demand for GRE and GRP pipes in this sector is set to accelerate.

The chemical industry represents another significant growth vertical, particularly in Europe, North America, and Asia Pacific. Favorable feedstock pricing, especially from natural gas in the U.S., has spurred investments in petrochemical facilities, creating rising demand for fiberglass pipes in chemical transport and processing systems. Additionally, the increasing focus on environmental compliance is driving industries toward corrosion-resistant solutions that lower risks of leakage and contamination.

Sewage and water management applications are emerging as high-potential end uses, propelled by urbanization and climate-driven investments in water security. With global wastewater treatment capacity expected to expand by 25% by 2035, fiberglass pipes are becoming indispensable for sewer networks, desalination plants, and potable water distribution. The combination of low maintenance, longevity, and cost-efficiency positions fiberglass as a preferred solution for municipalities and private water utilities worldwide.

Regional Analysis

North America held a commanding 36% share of the fiberglass pipes market in 2024, valued at USD 1.6 billion, and continues to benefit from stringent environmental regulations and modernization of municipal infrastructure. U.S. policy initiatives, such as long-term water infrastructure programs under the Water Resources Development Act, are encouraging the adoption of corrosion-resistant piping in both public utilities and energy projects. The oil and gas shale boom also provides steady momentum for GRE pipe installations in upstream and midstream networks.

Asia Pacific is anticipated to record the fastest CAGR through 2034, fueled by rapid urbanization, rising water demand, and energy diversification policies. China’s pivot toward natural gas and reduction of coal dependency is expected to drive substantial investment in fiberglass pipeline networks. The country’s dominant chemical sector, accounting for over 40% of global sales, further cements its role as a critical growth hub. Meanwhile, India’s diversified chemical processing industry, projected to reach USD 300 billion by 2025, is generating robust demand for fiberglass piping in both industrial and municipal applications.

The Middle East and Africa (MEA) are also emerging as strategic markets, underpinned by large-scale investments in desalination and oil infrastructure. Countries such as Saudi Arabia and the UAE are expanding fiberglass manufacturing bases to reduce import reliance and strengthen supply security. In Europe and Latin America, stricter environmental regulations and renewable energy expansion are accelerating adoption in wastewater treatment and industrial facilities. Collectively, these regional trends underscore the global shift toward fiberglass as a material of choice for critical infrastructure modernization.

Get More Information about this report -

Request Free Sample ReportМаrkеt Кеу Ѕеgmеntѕ

By Product Type

- GRP Pipes

- GRE Pipes

- Other Product Types

By Fiber Type

- T/ S/ R Glass

- E-glass

- Other Fiber Types

By End-Use

- Oil & Gas

- Chemicals

- Sewage

- Other End-Uses

Regions

- North America

- Western Europe

- Eastern Europe

- APAC

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 6.1 B |

| Forecast Revenue (2034) | USD 10.4 B |

| CAGR (2024-2034) | 5.8% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, GRP Pipes, GRE Pipes, Other Product Types, By Fiber Type, T/ S/ R Glass, E-glass, Other Fiber Types, By End-Use, Oil & Gas, Chemicals, Sewage, Other End-Uses |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Saudi Arabian AMIANTIT Company, Fibrex Corporation, HOBAS International GmbH, Chemical Process Piping Pvt. Ltd. (CPP), Andronaco Industries, Amiblu Holding GmbH, Graphite India Limited, Future Pipe Industries, National Oilwell Varco Inc., FCX Performance, Sarplast SA, PPG Fiberglass Industries, Other Key Players, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Fiber Type, (T/ S/ R Glass, E-glass, Other Fiber Types), By End-User Industry, Corrosion Resistance Benefits, Regional Demand & Forecast 2025–2034")

, By Fiber Type, (T/ S/ R Glass, E-glass, Other Fiber Types), By End-User Industry, Corrosion Resistance Benefits, Regional Demand & Forecast 2025–2034")

, By Fiber Type, (T/ S/ R Glass, E-glass, Other Fiber Types), By End-User Industry, Corrosion Resistance Benefits, Regional Demand & Forecast 2025–2034")

Frequently Asked Questions

How big is the Fiberglass Pipes Market?

The Fiberglass Pipes Market is projected to grow from USD 6.1 billion in 2024 to USD 10.4 billion by 2034, at a CAGR of 5.8% during 2025–2034. Rising demand for corrosion-resistant piping, expanding oil & gas and water treatment infrastructure, and advancements in composite manufacturing are driving global market expansion. Emerging economies and sustainability-focused projects will further accelerate growth over the next decade.

Who are the major players in the Fiberglass Pipes Market?

Saudi Arabian AMIANTIT Company, Fibrex Corporation, HOBAS International GmbH, Chemical Process Piping Pvt. Ltd. (CPP), Andronaco Industries, Amiblu Holding GmbH, Graphite India Limited, Future Pipe Industries, National Oilwell Varco Inc., FCX Performance, Sarplast SA, PPG Fiberglass Industries, Other Key Players,

Which segments covered the Fiberglass Pipes Market?

By Product Type, GRP Pipes, GRE Pipes, Other Product Types, By Fiber Type, T/ S/ R Glass, E-glass, Other Fiber Types, By End-Use, Oil & Gas, Chemicals, Sewage, Other End-Uses

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date