- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Fill-Finish Manufacturing Market Size & Forecast | CAGR 10.9%

Global Fill-Finish Manufacturing Market Size, Share, Growth & Industry Analysis By Primary Container Format (Vials Glass & Polymer, Pre-Filled Syringes, Cartridges, Ampoules, Flexible Bags), By Drug Type (Biologics & Biosimilars, Sterile Injectables, Vaccines, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Government Manufacturing) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 14.62 Billion | USD 37.04 Billion | 10.9% | North America, 39.4% |

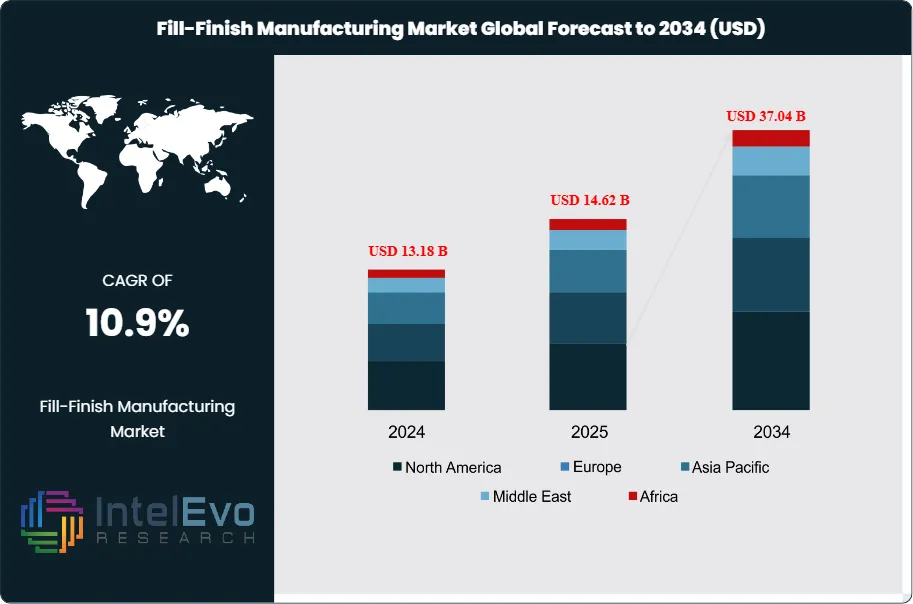

The Fill-Finish Manufacturing Market was valued at approximately USD 13.18 Billion in 2024 and reached USD 14.62 Billion in 2025. The market is projected to grow to USD 37.04 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 22.42 Billion over the analysis period, driven by accelerating demand for sterile injectable biologics, mRNA-based therapeutics, biosimilars, and pre-filled syringe presentations across global pharmaceutical markets.

Get More Information about this report -

Request Free Sample ReportFill-finish manufacturing encompasses the final production stages of pharmaceutical drug product manufacturing: aseptic filling of drug substance into primary containers, stoppering, sealing, inspection, and labeling. The primary container formats served include vials, pre-filled syringes, cartridges, ampoules, and flexible bags. Fill-finish is one of the most capital-intensive and technically demanding segments of pharmaceutical manufacturing, operating under Grade A (ISO Class 5) aseptic conditions within isolator or RABS-based environments, with all operations governed by FDA 21 CFR Part 211, EU GMP Annex 1, and WHO Technical Report Series requirements for sterile drug products.

Demand within the fill-finish manufacturing market is fundamentally linked to the biologics pipeline. More than 40% of novel FDA drug approvals in 2024 were biologics, and the vast majority of approved and pipeline biologic drug products are administered as sterile injectables requiring aseptic fill-finish processing. The biosimilar wave is adding incremental volume demand, with over 40 biosimilar products approved in the United States alone by 2025 and additional approvals expected at an accelerating rate as originator biologic patents expire. The mRNA platform, commercialized at unprecedented scale during the COVID-19 vaccine programs, has expanded into oncology, infectious disease, and rare disease therapeutic areas — each requiring aseptic fill-finish capacity for lipid nanoparticle formulations.

Regulatory forces are simultaneously driving equipment modernization and capacity expansion. The revised EU GMP Annex 1 (effective August 2023) has reset global sterility assurance standards, requiring isolator-based Grade A environments, automated container handling, and continuous environmental monitoring at fill-finish lines. Compliance with Annex 1 has triggered a capital expenditure wave among European and multi-regional pharmaceutical manufacturers, with fill-finish facility upgrades and new builds estimated at USD 3.8 Billion in cumulative investment between 2023 and 2026.

On the supply side, CDMOs now account for approximately 38.6% of global fill-finish capacity in 2025, a share that has grown steadily as pharmaceutical companies choose to outsource capital-intensive sterile manufacturing operations. Major CDMO groups have invested aggressively in fill-finish infrastructure across the United States, Europe, and Asia Pacific, creating an increasingly competitive outsourcing supply base. Technology suppliers are delivering integrated fill-finish platforms combining vial filling, stoppering, lyophilizer loading, inspection, and packaging within isolator-enclosed systems that reduce contamination risk and simplify regulatory validation.

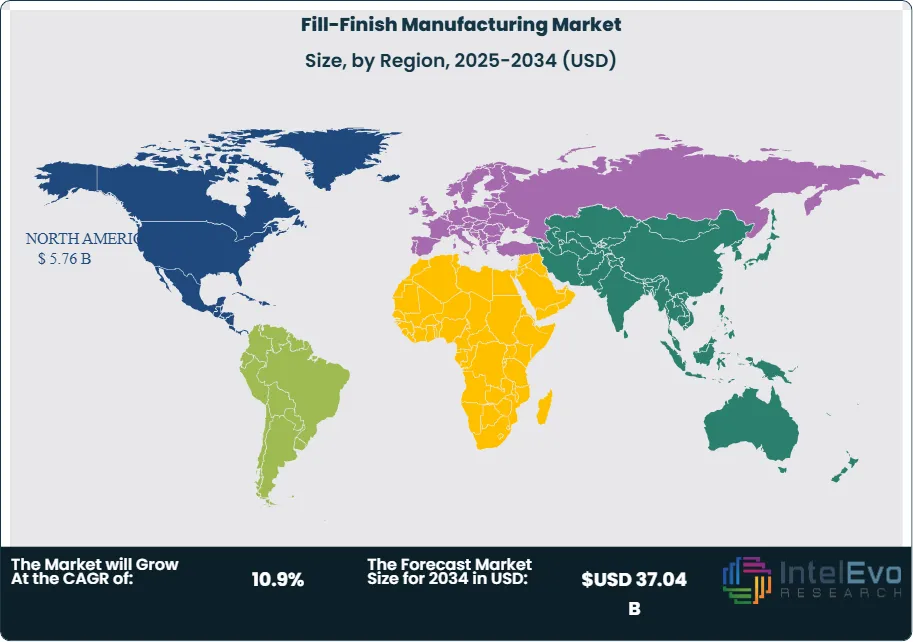

North America leads the global fill-finish manufacturing market with a 39.4% share in 2025, generating approximately USD 5.76 Billion. Europe holds 28.8%, anchored by Germany, Ireland, Switzerland, and Italy. Asia Pacific represents 22.4% and is the fastest-growing region, with China, India, and South Korea all investing materially in GMP fill-finish capacity. The fill-finish manufacturing market across all regions benefits from the structural shift toward prefilled syringe presentations, which now account for the fastest-growing primary container format and are expected to represent the largest format segment by 2029.

, By Drug Type (Biologics & Biosimilars, Sterile Injectables, Vaccines, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Government Manufacturing) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global fill-finish manufacturing market was valued at USD 14.62 Billion in 2025 and is projected to reach USD 37.04 Billion by 2034, expanding at a CAGR of 10.9% over the forecast period 2026–2034.

- Segment Dominance: By primary container format, vials remain the leading container type at approximately 44.8% of fill-finish manufacturing market revenue in 2025, driven by their established use across lyophilized biologics, vaccines, and multi-dose injectable drug products.

- Segment Dominance: By end-user, CDMOs account for 38.6% of fill-finish manufacturing market revenue in 2025, reflecting the industry-wide structural shift toward outsourced sterile manufacturing at specialized GMP fill-finish facilities.

- Driver: The global injectable biologics market exceeded USD 320 Billion in 2025, with biologics representing more than 40% of all novel FDA drug approvals in 2024, generating sustained capital expenditure for aseptic fill-finish capacity at both integrated pharmaceutical manufacturers and CDMO operators.

- Restraint: High capital expenditure requirements for GMP fill-finish facility construction — averaging USD 80–150 Million for a new greenfield aseptic vial filling suite with isolator technology — constrain entry for smaller operators and limit capacity addition timelines to 3–5 years from investment decision to commercial readiness.

- Opportunity: The pre-filled syringe segment is the fastest-growing primary container format in fill-finish manufacturing at a projected CAGR of 13.6% through 2034, representing an incremental addressable revenue opportunity exceeding USD 8.2 Billion over the forecast period as GLP-1 receptor agonist and biologic self-injection products drive format conversion.

- Trend: Integration of robotic container handling, automated visual inspection, and isolator-coupled aseptic filling within unified fill-finish platform architectures is present in approximately 46.8% of new fill-finish line installations in 2025, up from 21.3% in 2019, as EU GMP Annex 1 mandates elimination of manual Grade A zone interventions.

- Regional Analysis: North America leads the global fill-finish manufacturing market with a 39.4% share in 2025, generating approximately USD 5.76 Billion in revenue, anchored by the United States' dominant biologics manufacturing base and the world's highest concentration of licensed aseptic fill-finish CDMO capacity.

Competitive Landscape Overview

The fill-finish manufacturing market is moderately consolidated at the CDMO service level, with the top four CDMO operators — Lonza Group, Baxter BioPharma Solutions, Recipharm, and Vetter Pharma — collectively holding approximately 31.4% of global outsourced fill-finish revenue in 2025. On the equipment supply side, the market is similarly moderately consolidated, with Syntegon Technology, IMA Life, Bausch+Stroebel, and Groninger & Co. leading commercial line installations. Competition is technology- and regulatory-capability-driven, with Annex 1 compliance expertise, container format breadth, and geographic diversification serving as primary differentiators. M&A activity among CDMOs has increased substantially since 2022 as groups seek to add fill-finish capacity, container format coverage, and geographic distribution of aseptic manufacturing risk.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Service | Geo Strength | Recent Strategic Move (2024–2026) |

| Lonza Group | Switzerland | Leader | Lonza Sterile Fill-Finish CDMO Services | Europe / North America | Feb 2025: Expanded aseptic vial and pre-filled syringe fill-finish capacity at its Visp, Switzerland site by adding two new isolator-coupled filling lines targeting biologics CDMO demand. |

| Baxter BioPharma Solutions | USA | Leader | Baxter Aseptic Fill-Finish CDMO | North America / Europe | Apr 2025: Entered a multi-year fill-finish CDMO partnership with a top-10 global pharmaceutical company for pre-filled syringe filling of a high-volume biologic product. |

| Recipharm | Sweden | Leader | Recipharm Sterile Injectable Services | Europe / Global | Jan 2026: Completed acquisition of a US-based aseptic fill-finish CDMO site, adding vial and cartridge filling capacity to its North American manufacturing network. |

| Vetter Pharma | Germany | Leader | Vetter Prefillable Syringe Filling | Europe / North America | Sep 2025: Commissioned a new pre-filled syringe manufacturing suite at its Ravensburg facility, adding 30 Million syringe units per year of annual fill-finish capacity. |

| Syntegon Technology | Germany | Challenger | Versynta microBatch Fill-Finish System | Europe / Global | Mar 2025: Launched Versynta microBatch — a flexible, small-batch aseptic filling platform targeting clinical-stage and orphan drug fill-finish for CDMOs and emerging biotech manufacturers. |

| IMA Life | Italy | Challenger | IMA BFT Vial Filling Line | Europe / North America | Jun 2025: Launched an integrated vial fill-finish line with direct isolator coupling and robotic tray loading, meeting EU GMP Annex 1 critical zone automation requirements. |

| Bausch+Stroebel | Germany | Challenger | Bausch+Stroebel VarioSys Filling Platform | Europe / North America | Nov 2024: Introduced an upgraded VarioSys flexible filling platform supporting vials, syringes, and cartridges within a single, isolator-compatible aseptic processing system. |

| Groninger & Co. | Germany | Challenger | groninger DOSYS Filling System | Europe | May 2025: Secured a multi-line supply contract with a major European CDMO for DOSYS vial and pre-filled syringe filling systems for a new aseptic manufacturing expansion. |

| WuXi Biologics (WuXi AppTec) | China | Niche Player | WuXi Biologics Fill-Finish CDMO | Asia Pacific / Global | Aug 2025: Opened a new GMP fill-finish facility in Wuxi, China with 12 filling lines supporting vials, pre-filled syringes, and lyophilization for global pharmaceutical clients. |

| Catalent | USA | Niche Player | Catalent Biologics Fill-Finish Services | North America / Europe | Jan 2025: Completed integration of its Bloomington, Indiana fill-finish site into the Novo Holdings acquisition structure, adding significant pre-filled syringe and vial fill-finish capacity. |

By Primary Container Format

The fill-finish manufacturing market by primary container format is led by vials, which account for approximately 44.8% of total market revenue in 2025, valued at USD 6.55 Billion. Vials remain the dominant fill-finish container format for lyophilized biologics, vaccines, cytotoxic injectables, and multi-dose parenteral products. The standard pharmaceutical vial, available in glass and increasingly in polymer configurations, accommodates fill volumes from 0.5 mL to 100 mL and is compatible with both liquid and freeze-dried drug product presentations. The lyophilized vial sub-format is particularly active, as the commercial expansion of monoclonal antibodies, ADCs, and protein therapeutics that require lyophilization for stability drives investment in vial fill-finish capacity with integrated lyophilizer loading. The vial segment is expected to grow at a 9.8% CAGR through 2034, slightly below the overall market rate, as pre-filled syringe formats gain share in self-injection biologic and GLP-1 receptor agonist product categories. Vial fill-finish line speeds range from 6,000 vials per hour for small-molecule injectables to 3,000 vials per hour for high-viscosity biologics, with commercial scale assets valued at USD 5–15 Million per integrated line.

Pre-filled syringes represent 31.6% of fill-finish manufacturing market revenue in 2025 at USD 4.62 Billion and are the fastest-growing primary container format with a projected CAGR of 13.6% through 2034. The shift from vial-and-needle to prefilled syringe presentation is driven by patient convenience, dose accuracy, and needle-stick injury reduction, but the most powerful commercial force in 2025 is the GLP-1 receptor agonist market. Products including semaglutide (Novo Nordisk's Ozempic and Wegovy) and tirzepatide (Eli Lilly's Mounjaro and Zepbound) are filled primarily in pre-filled auto-injector formats, and their extraordinary commercial success has created acute demand for pre-filled syringe fill-finish capacity globally. The pre-filled syringe format is also the preferred container for subcutaneous biologic biologics including adalimumab biosimilars, etanercept biosimilars, and emerging checkpoint inhibitor products formulated for patient self-administration. Cartridges account for 10.8% of market revenue, primarily serving pen injector presentations for insulin and GLP-1 products. Ampoules and flexible bags together account for the remaining 12.8%.

By Drug Type

By drug type, biologics and biosimilars dominate the fill-finish manufacturing market, accounting for 52.4% of revenue in 2025 at USD 7.66 Billion. This segment encompasses fill-finish processing for monoclonal antibodies, recombinant proteins, bispecific antibodies, ADCs, fusion proteins, cell and gene therapy products, and mRNA-based therapeutics. The consistent growth of the biologics category is the primary force expanding fill-finish manufacturing capacity requirements globally, as each new biologic product launch requires dedicated or shared aseptic fill-finish capacity for clinical supply and commercial production. Biosimilar market entry, while generating lower per-unit revenue than originator biologics, adds significant volume demand for fill-finish services at CDMOs as biosimilar developers outsource sterile manufacturing to control capital costs. Small-molecule sterile injectables account for 30.8% of fill-finish market revenue in 2025 at USD 4.50 Billion, encompassing chemotherapy agents, antifungals, analgesics, antibiotics, and contrast media. Vaccines represent 11.6% of market revenue at USD 1.70 Billion, with demand shaped by routine immunization programs and pandemic preparedness investments. Cell and gene therapy fill-finish constitutes the remaining 5.2%, a small but rapidly growing share driven by commercial CGT product launches and the unique fill-finish requirements of viral vector and patient-specific cell therapy products.

By End-User

By end-user, integrated pharmaceutical and biopharmaceutical manufacturers represent the largest revenue category within the fill-finish manufacturing market at 52.2% of revenue in 2025, or USD 7.63 Billion. These manufacturers operate proprietary fill-finish suites for internally developed products, investing in GMP-grade aseptic lines to maintain control over commercial drug product quality, supply security, and regulatory submissions. Large integrated companies including Pfizer, Eli Lilly, AstraZeneca, Novartis, Roche, and Sanofi each operate multiple fill-finish sites globally, with combined investments in fill-finish infrastructure running into billions of dollars over the 2020–2025 period. CDMOs account for 38.6% of market revenue at USD 5.64 Billion, serving the fill-finish needs of biotechnology companies, specialty pharma developers, and large pharmaceutical companies that have chosen to outsource sterile drug product manufacturing. Government and public health manufacturing organizations, including national vaccine institutes and public health emergency preparedness entities, account for approximately 6.4% of market revenue. Academic and research use makes up the remaining 2.8%.

Regional Analysis

North America Fill-Finish Manufacturing Market

North America holds a commanding 39.4% share of the global fill-finish manufacturing market in 2025, generating approximately USD 5.76 Billion in revenue. The United States is the world's largest single fill-finish manufacturing market, benefiting from the highest concentration of FDA-approved biologic drug products, the most extensive CDMO fill-finish infrastructure globally, and FDA's institutional framework for aseptic manufacturing compliance. Major CDMO campuses offering fill-finish services are concentrated in New Jersey, Indiana, North Carolina, and Massachusetts, with additional capacity in Pennsylvania and California. US pharmaceutical companies including Pfizer, Eli Lilly, Amgen, and Regeneron have each invested over USD 500 Million in fill-finish manufacturing capacity since 2020, driven by the commercial launches of high-volume biologics and mRNA products. The FDA's current Good Manufacturing Practice (cGMP) enforcement environment — evidenced by a sustained cadence of Form 483 observations and Warning Letters related to aseptic process failures — is compelling manufacturers to upgrade older fill-finish lines and adopt isolator-based aseptic systems. Canada contributes to regional demand through federal biomanufacturing strategy investments, while Mexico's pharmaceutical sector adds incremental capacity oriented toward CDMO services for North American markets. North America's fill-finish manufacturing market is projected to grow at a 10.2% CAGR through 2034.

Europe Fill-Finish Manufacturing Market

Europe represents 28.8% of the global fill-finish manufacturing market in 2025 at USD 4.21 Billion. Germany, Ireland, Switzerland, and Italy are the primary manufacturing hubs, each hosting major fill-finish operations for multinational pharmaceutical companies and growing CDMO sectors. The EU GMP Annex 1 revision (effective August 2023) has been the definitive regulatory catalyst for capital investment in European fill-finish manufacturing, requiring isolator-based Grade A environments, automated container handling in critical zones, and continuous environmental monitoring at fill-finish lines. Industry estimates place cumulative Annex 1 compliance investment in European fill-finish infrastructure at USD 3.8 Billion between 2023 and 2026. Ireland has attracted particularly significant investment from US pharmaceutical companies seeking EU manufacturing presence, with multiple new fill-finish facilities commissioned in Cork and Dublin. Germany's Vetter Pharma, a specialist pre-filled syringe fill-finish CDMO headquartered in Ravensburg, is one of Europe's most advanced commercial fill-finish operators and a direct beneficiary of the GLP-1 agonist pre-filled syringe demand surge. Switzerland's fill-finish manufacturing base, anchored by Lonza's operations in Visp and the operations of Novartis and Roche, contributes significant aseptic processing capacity. Europe's fill-finish manufacturing market is projected to grow at a 10.6% CAGR through 2034.

Asia Pacific Fill-Finish Manufacturing Market

Asia Pacific accounts for 22.4% of the global fill-finish manufacturing market in 2025 at USD 3.27 Billion and is the fastest-growing region with a projected CAGR of 13.9% through 2034. China is the largest and fastest-growing national market in the region, with domestic pharmaceutical manufacturers and CDMOs — including WuXi Biologics, Zhangjiang Biotech, and Tianyuan Gene — investing aggressively in GMP-grade fill-finish capacity to serve both domestic biologic markets and global pharmaceutical outsourcing clients. NMPA's progressive GMP alignment with FDA and EU standards has elevated quality expectations and driven equipment modernization among Chinese fill-finish operators. India's pharmaceutical sector, the world's largest generic drug producer, is rapidly expanding sterile injectables fill-finish capacity through PLI scheme-incentivized facility investments, with multiple greenfield aseptic fill-finish plants under construction to serve FDA and EMA export markets. South Korea's Samsung Biologics and Celltrion operate globally significant fill-finish capacity and are actively expanding to serve growing biosimilar and CDMO demand. Japan's domestic fill-finish sector, serving a high-value domestic market, is investing in Annex 1-equivalent GMP upgrades and pre-filled syringe format expansion. The Asia Pacific fill-finish manufacturing market is the primary geographic growth opportunity for equipment suppliers and CDMO services through 2034.

Latin America Fill-Finish Manufacturing Market

Latin America holds a 5.8% share of the fill-finish manufacturing market in 2025 at approximately USD 0.85 Billion. Brazil is the dominant regional market, anchored by ANVISA-regulated pharmaceutical manufacturing and public health institutions including Fiocruz and Instituto Butantan, which operate fill-finish capacity for vaccine and biologic drug products serving domestic and regional public health programs. Fiocruz's technology transfer programs with global vaccine manufacturers have included fill-finish technology transfer components, gradually building domestic fill-finish technical capability. Mexico's pharmaceutical manufacturing sector, oriented partly toward supplying North American markets, is adding GMP fill-finish capacity to support CDMO service offerings. Argentina's domestic pharmaceutical industry contributes fill-finish capacity for the domestic market. The Latin American fill-finish manufacturing market is constrained by imported equipment costs, limited local qualified engineering resources, and foreign exchange risks affecting capital expenditure planning for US dollar-denominated equipment. International CDMO groups are selectively establishing regional fill-finish capacity to serve Latin American pharmaceutical markets. The region's fill-finish manufacturing market is projected to grow at a 9.4% CAGR through 2034.

Middle East & Africa Fill-Finish Manufacturing Market

The Middle East and Africa region accounts for 3.6% of global fill-finish manufacturing market revenue in 2025 at approximately USD 0.53 Billion. Saudi Arabia and the UAE are the primary demand centers within the GCC, where Vision 2030 and equivalent national strategies are channeling investment into domestic sterile pharmaceutical manufacturing. Saudi Arabia's SFDA has implemented GMP standards aligned with WHO and ICH requirements, providing the regulatory foundation for commercial GMP fill-finish operations. The UAE's pharmaceutical manufacturing sector, while smaller in absolute scale, is growing through free zone-based manufacturing investments and government-sponsored pharmaceutical self-sufficiency programs. South Africa's pharmaceutical manufacturing base, the most developed in sub-Saharan Africa, contributes fill-finish capacity through established injectable drug manufacturers serving domestic and export markets. The MEA region's fill-finish manufacturing market is in an early but accelerating growth phase, with significant investment catalysts including the African Union's pharmaceutical manufacturing agenda, GAVI-supported vaccine fill-finish programs, and bilateral technology transfer agreements between GCC nations and global pharmaceutical companies. MEA's fill-finish manufacturing market is projected to grow at a 11.2% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Primary Container Format

- Vials (Glass & Polymer)

- Pre-Filled Syringes

- Cartridges

- Ampoules

- Flexible Bags & Other Formats

By Drug Type

- Biologics & Biosimilars

- Small-Molecule Sterile Injectables

- Vaccines

- Cell & Gene Therapy Products

By End-User

- Integrated Pharmaceutical & Biopharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Government & Public Health Manufacturing Organizations

- Academic & Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.62 B |

| Forecast Revenue (2034) | USD 37.04 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Primary Container Format, (Vials (Glass & Polymer), Pre-Filled Syringes, Cartridges, Ampoules, Flexible Bags & Other Formats), By Drug Type, (Biologics & Biosimilars, Small-Molecule Sterile Injectables, Vaccines, Cell & Gene Therapy Products), By End-User, (Integrated Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Government & Public Health Manufacturing Organizations, Academic & Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LONZA GROUP, BAXTER BIOPHARMA SOLUTIONS, RECIPHARM, VETTER PHARMA, SYNTEGON TECHNOLOGY, IMA LIFE, BAUSCH+STROEBEL, GRONINGER & CO., WUXI BIOLOGICS (WUXI APPTEC), CATALENT, PFIZER CENTREONE, FAREVA, AESICA PHARMACEUTICALS (RECIPHARM), BIOMEVA (MERCK KGAA), BOEHRINGER INGELHEIM BIOPHARMACEUTICALS, SAMSUNG BIOLOGICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Drug Type (Biologics & Biosimilars, Sterile Injectables, Vaccines, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Government Manufacturing) Industry Trends & Forecast 2026–2034")

, By Drug Type (Biologics & Biosimilars, Sterile Injectables, Vaccines, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Government Manufacturing) Industry Trends & Forecast 2026–2034")

, By Drug Type (Biologics & Biosimilars, Sterile Injectables, Vaccines, Cell & Gene Therapy), By End-User (Pharma, CDMOs, Government Manufacturing) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Fill-Finish Manufacturing Market?

Global Fill-finish manufacturing market valued at USD 13.18B in 2024, reaching USD 37.04B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Fill-Finish Manufacturing Market?

LONZA GROUP, BAXTER BIOPHARMA SOLUTIONS, RECIPHARM, VETTER PHARMA, SYNTEGON TECHNOLOGY, IMA LIFE, BAUSCH+STROEBEL, GRONINGER & CO., WUXI BIOLOGICS (WUXI APPTEC), CATALENT, PFIZER CENTREONE, FAREVA, AESICA PHARMACEUTICALS (RECIPHARM), BIOMEVA (MERCK KGAA), BOEHRINGER INGELHEIM BIOPHARMACEUTICALS, SAMSUNG BIOLOGICS, Others

Which segments covered the Fill-Finish Manufacturing Market?

By Primary Container Format, (Vials (Glass & Polymer), Pre-Filled Syringes, Cartridges, Ampoules, Flexible Bags & Other Formats), By Drug Type, (Biologics & Biosimilars, Small-Molecule Sterile Injectables, Vaccines, Cell & Gene Therapy Products), By End-User, (Integrated Pharmaceutical & Biopharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Government & Public Health Manufacturing Organizations, Academic & Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Fill-Finish Manufacturing Market

Published Date : 04 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date