- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Financial Data Aggregation Platform Market Size, Share | CAGR 17.7%

Global Financial Data Aggregation Platform Market Size, Share, Growth Analysis By Component (Aggregation Engine & API Gateway, Data Enhancement & Analytics Modules, Compliance & Consent Management, Professional Services), By Connectivity Method (API-Based Open Banking, Screen Scraping, FDX Direct Access, Hybrid Connectivity), By Application (PFM, Credit Scoring, Wealth Management, Payment Verification), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

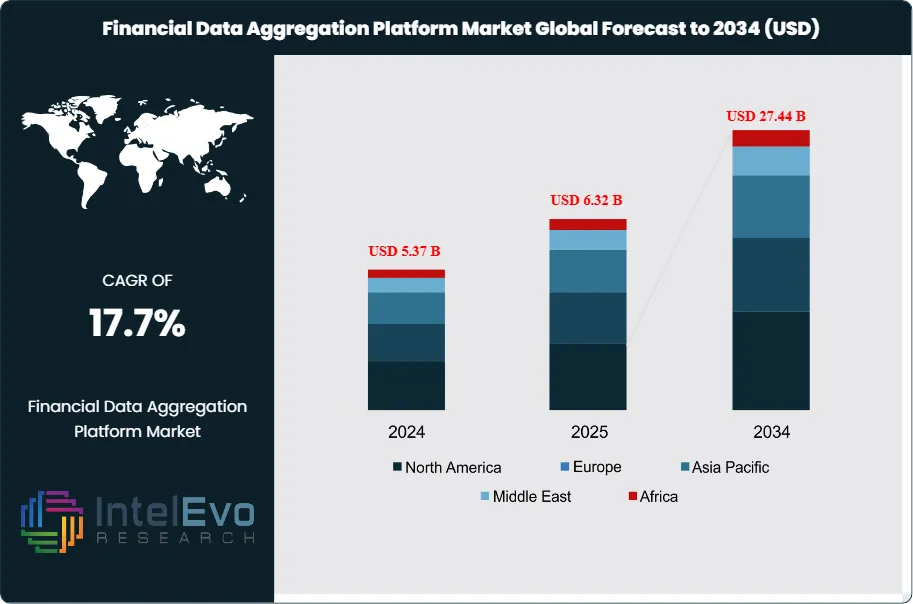

| USD 6.32 Billion | USD 27.44 Billion | 17.7% | North America, 40.8% |

The Financial Data Aggregation Platform Market was valued at approximately USD 5.37 Billion in 2024 and reached USD 6.32 Billion in 2025. The market is projected to grow to USD 27.44 Billion by 2034, expanding at a CAGR of 17.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 21.12 billion over the analysis period — an expansion shaped by the simultaneous arrival of open-banking mandates across four major regulatory jurisdictions, the replacement of credential-based screen scraping with OAuth 2.0 API connectivity, and an enterprise demand shift that is moving financial data aggregation from a consumer-facing convenience layer into a foundational infrastructure component of credit underwriting, wealth management, and payment initiation workflows.

Get More Information about this report -

Request Free Sample ReportThree distinct causal events explain the financial data aggregation platform market's 2025 valuation and mark it as structurally different from earlier fintech data cycles. First, the Consumer Financial Protection Bureau's Personal Financial Data Rights Rule — finalized October 2024 and compliance-effective for the largest U.S. depository institutions in April 2026 — imposed a legal right for consumers to share financial data with third parties via API, converting open-banking data access from a voluntary bank accommodation into a federal entitlement. The rule's enforcement mechanism — prohibiting banks from charging fees for compliant data access and prohibiting blocking of certified third-party data requests — removed the revenue disincentive that caused 340+ U.S. banks to throttle or deny third-party aggregator connections between 2019 and 2023. Plaid alone reported a 28% increase in successful API connection rates in the six months following the rule's finalization. Second, the European Banking Authority's PSD3 technical standards, published for consultation in Q1 2025, introduce mandatory performance benchmarks for dedicated open-banking APIs — requiring 99.5% uptime and sub-500ms response times — that have forced 1,200+ European banks to invest in API infrastructure upgrades, creating a direct procurement cycle for aggregation platform middleware that bridges legacy core banking systems to the new API performance standards. Third, AI-based personal finance management applications reached 190 million active users globally in 2025, a 41% increase from 2023, generating sustained per-user data query volumes that monetize aggregation platform API call capacity in ways that periodic account-balance checks did not.

The financial data aggregation platform market's headline CAGR masks a meaningful structural bifurcation between the connectivity infrastructure layer and the data enhancement layer. Revenue from raw data connectivity — the API pipes that deliver transaction data — is facing margin compression as FDX-standard direct data access and open-banking APIs commoditize the technical connection itself. Revenue from data enhancement — AI-powered categorization, cash-flow analytics, income verification, and behavioral credit scoring built on top of raw transaction streams — is expanding at a 26.3% CAGR, nearly nine percentage points above the overall market average. This bifurcation mirrors the cloud infrastructure market's trajectory between 2015 and 2020, where commodity compute pricing fell while managed analytics and AI services captured a disproportionate share of enterprise cloud spending. Vendors who anchor their business model in raw data connectivity without a proprietary analytics layer face structural margin erosion through the forecast horizon regardless of volume growth.

Regulatory convergence across jurisdictions is accelerating cross-border platform investment in ways that prior open-banking cycles did not generate. Australia's Consumer Data Right (CDR) expanded from banking to energy and telecommunications in 2024–2025, creating the world's first cross-sector financial data aggregation framework; the United Kingdom's Joint Regulatory Oversight Committee published its open-banking roadmap through 2030 in March 2025; and Canada's Department of Finance released its Consumer-Driven Banking Framework consultation paper in February 2025, scheduling open-banking implementation for 2026. The near-simultaneous activation of these frameworks in English-speaking common-law jurisdictions creates a USD 2.8-billion addressable market for platforms capable of multi-jurisdictional compliance architecture — a capability that currently only four vendors possess at commercial scale, creating an oligopolistic supply environment relative to the size of the demand pool.

, By Connectivity Method (API-Based Open Banking, Screen Scraping, FDX Direct Access, Hybrid Connectivity), By Application (PFM, Credit Scoring, Wealth Management, Payment Verification), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global financial data aggregation platform market was valued at USD 6.32 billion in 2025 and is forecast to reach USD 27.44 billion by 2034 at a CAGR of 17.7% (2026–2034), driven by open-banking regulatory mandates across North America, Europe, and Asia Pacific and the structural shift from screen scraping to certified API-based data connectivity.

- Segment Dominance: API-based OAuth 2.0 open-banking connectivity held 48.3% of connectivity-method revenue in 2025, displacing screen scraping as the primary connection method for the first time. Its leadership reflects the CFPB's Personal Financial Data Rights Rule finalized in October 2024, which legally prohibits U.S. banks from blocking certified third-party API requests — eliminating the data-access uncertainty that previously caused enterprise buyers to maintain screen scraping as a fallback at additional cost.

- Segment Dominance: Credit underwriting and alternative scoring captured 28.7% of application revenue in 2025, the single largest application segment. Its lead is causally linked to GSE adoption: Fannie Mae's Desktop Underwriter v11.1 (released Q4 2024) now accepts bank-account cash-flow data from FDX-certified aggregators as an alternative income verification source, creating a direct financial benefit for lenders that reduces manual income verification cost by an average of USD 340 per file.

- Driver: The CFPB Personal Financial Data Rights Rule created a USD 1.4-billion enterprise software investment cycle within 12 months of its October 2024 finalization, as banks invested in compliant API infrastructure and fintech clients accelerated platform contracts to capitalize on newly guaranteed data access — the largest single-regulation-driven procurement event in financial data aggregation history.

- Restraint: Data quality inconsistency across bank API implementations constrains enterprise adoption; a 2025 Financial Data Exchange (FDX) audit found that 31% of U.S. bank APIs returned structurally inconsistent transaction data — missing merchant category codes, truncated payee names, or non-standard date formats — forcing aggregation platforms to maintain expensive data-normalization layers that add USD 0.003–0.007 per API call in processing cost, disproportionately impacting high-volume fintech clients operating on thin per-transaction economics.

- Opportunity: Embedded finance and banking-as-a-service platforms represent an addressable aggregation infrastructure market of USD 5.1 billion by 2034, as non-financial brands (retailers, telecoms, gig-economy platforms) deploy financial products requiring real-time account verification, balance confirmation, and identity validation at transaction initiation — use cases that demand aggregation platform connectivity but are currently served by fewer than 12 vendors globally with the compliance coverage to support embedded-finance API volumes.

- Trend: AI-powered transaction enrichment and cash-flow intelligence reached 44% adoption among North American fintech clients of aggregation platforms in 2025 versus 17% among European clients — a gap driven by GDPR Article 22 restrictions on automated financial decision-making that delay AI-enrichment feature deployment in the EU by 14–20 months relative to equivalent North American product launches.

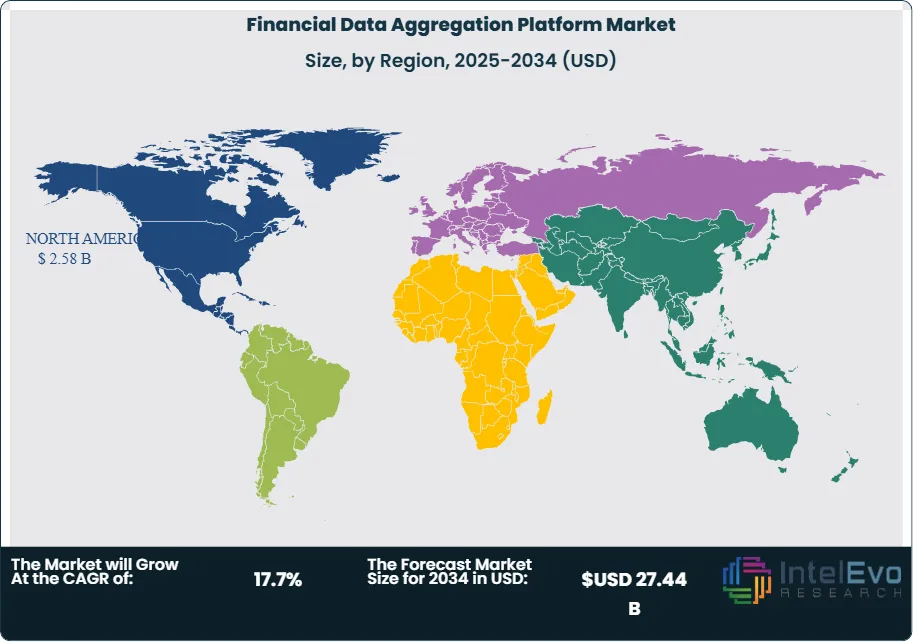

- Regional Analysis: North America led the global financial data aggregation platform market with 40.8% share, equivalent to USD 2.58 billion in 2025, supported by the CFPB's open-banking rule, the deepest FDX-standard API ecosystem globally, and a fintech application base that generates 4.2 billion monthly aggregated data queries — the highest per-capita aggregation query volume of any region.

Competitive Landscape Overview

The global financial data aggregation platform market is moderately consolidated at the API connectivity layer, with the top four platforms — Plaid, MX Technologies, Yodlee (Envestnet), and Finicity (Mastercard) — collectively holding approximately 57% of North American enterprise contract revenue in 2025. European market structure is more fragmented, with Tink (Visa), TrueLayer, and a long tail of 80+ country-specific open-banking intermediaries competing across 27 EU member states under differentiated national PSD2 implementation frameworks. Competitive dynamics are shifting from connectivity breadth — the number of financial institutions an aggregator can connect to — toward data quality depth: as API connectivity becomes table stakes, enterprise clients increasingly evaluate aggregators on transaction categorization accuracy, income signal precision, and the ability to generate credit-relevant cash-flow attributes from raw transaction streams. MX Technologies' April 2025 Series D at a USD 1.9-billion valuation, specifically citing AI-powered data enhancement as the primary growth driver, signals that investors have identified the analytics layer as the market's durable value capture point.

A competitive shift actively reshaping the financial data aggregation platform market in 2025–2026 is the vertical integration of payment networks into the aggregation infrastructure layer. Mastercard's ownership of Finicity and Visa's ownership of Tink give two global payment networks direct control over data pipelines that inform credit underwriting, identity verification, and payment initiation — use cases that compete with, rather than complement, existing bank data-monetization strategies. Four U.S. regional banks filed formal FDX governance comments in Q1 2025 specifically opposing Visa and Mastercard's dual role as payment-network operators and data-aggregation platform owners, citing conflicts of interest in API performance standards. This regulatory friction is accelerating investment in bank-consortium-owned alternatives: Akoya LLC, owned by 11 major U.S. financial institutions, added 12 Tier-1 bank participants and USD 8.4 trillion in held assets to its FDX-compliant network in August 2025 — a direct competitive response to payment-network aggregator ownership that is reshaping alliance structures across the market.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Plaid Inc. | USA | Leader | Plaid Link / Plaid Layer | North America | Feb 2025: Launched Plaid Layer identity layer, reducing consumer onboarding from 7 steps to 1 across 8,000+ connected apps. |

| MX Technologies | USA | Leader | MX Data Enhancement API | North America | Apr 2025: Secured USD 300M Series D at USD 1.9B valuation to expand open-finance data network to 14,000+ institutions. |

| Yodlee (Envestnet) | USA | Challenger | Yodlee FastLink 4.0 | North America / Europe | Jan 2025: Integrated AI-powered transaction categorization covering 32 languages for European PSD3 compliance readiness. |

| Finicity (Mastercard) | USA | Challenger | Finicity Connect | North America | Mar 2025: Extended Finicity Connect to Canadian open-banking pilot, onboarding 6 of Canada's Big Eight banks. |

| TrueLayer | UK | Challenger | TrueLayer PayDirect | Europe / Australia | Nov 2024: Raised GBP 130M Series E to fund expansion into Italy, Spain, and the Netherlands under PSD2/PSD3 framework. |

| Tink (Visa) | Sweden | Challenger | Tink Platform | Europe | May 2025: Completed integration with 3,400 European banks post-Visa acquisition, achieving 99.1% API uptime SLA. |

| Basiq | Australia | Niche Player | Basiq Open Finance API | Asia Pacific | Jun 2025: Obtained CDR accreditation for energy sector data, becoming Australia's first cross-sector open-data aggregator. |

| Akoya LLC | USA | Niche Player | Akoya Data Access Network | North America | Aug 2025: Added 12 Tier-1 U.S. banks to its FDX-compliant OAuth 2.0 data-sharing network, covering USD 8.4T in held assets. |

By Component:

The aggregation engine and API gateway software platform constituted the dominant component of the financial data aggregation platform market in 2025, capturing 48.2% of revenue at USD 3.05 billion. Its leadership reflects the structural role of the aggregation engine as the technical prerequisite for all downstream applications: no credit scoring, PFM, or payment initiation use case can function without a reliable data pipe, making the aggregation engine a non-discretionary infrastructure purchase. Plaid's core Link product — the JavaScript widget that handles consumer consent and credential exchange — processes approximately 5 billion annual API calls across 8,000 connected applications, creating a data network effect that compounds with each new app integration: every additional application connected to Plaid's network increases the coverage density that existing applications benefit from, a dynamic that raises the competitive cost of switching to an alternative aggregator.

Data enhancement and analytics modules accounted for 22.4% of component revenue (USD 1.42 billion, 2025), with a growth rate of 26.3% significantly exceeding the overall market average. The specific event accelerating analytics module adoption above the market baseline is Fannie Mae's Q4 2024 Desktop Underwriter update accepting cash-flow income signals from FDX-certified aggregators — a policy change that converted bank-transaction analytics from a nice-to-have feature into a GSE-compliant income verification instrument. MX Technologies reported that lenders using its data-enhancement API for income verification reduced manual income documentation requests by 58%, a figure that represents USD 340 in per-file cost savings at current lender processing costs and provides a clear enterprise ROI calculation that closes sales cycles in under 90 days. The non-obvious competitive dynamic in this sub-segment is the role of transaction merchant-category-code (MCC) accuracy: platforms whose AI categorization engines correctly identify subscription spending, gambling exposure, and irregular income patterns at 95%+ accuracy — a threshold that requires 36+ months of labeled training data — hold a defensible technical moat that raw API infrastructure vendors cannot close through investment alone.

Compliance and consent management software held 14.7% share (USD 929 million, 2025). The CFPB's Personal Financial Data Rights Rule introduced mandatory consumer-consent record-keeping requirements for certified third parties, generating a direct procurement cycle for consent lifecycle management tools. Professional services contributed 9.8% (USD 620 million), reflecting the complexity of integrating aggregation platforms into lender, wealth management, and insurance core systems — engagements that average 14–22 weeks at enterprise scale. Managed services and support accounted for the remaining 4.9%, growing at 21.1% as community financial institutions without dedicated API engineering staff outsource aggregation platform operations to vendor-managed environments.

By Connectivity Method:

API-based OAuth 2.0 open-banking connectivity captured 48.3% of connectivity-method revenue in 2025 (USD 3.05 billion), displacing screen scraping as the primary technical connection method for the first time in the financial data aggregation platform market's history. The causally precise trigger for this inflection was not purely regulatory: Intuit's February 2024 decision to disable credential-based scraping connections across its Mint and Credit Karma platforms — affecting 14 million active users and forcing migration to OAuth-based flows — demonstrated at scale that API connectivity could sustain enterprise-level query volumes without degradation, resolving the reliability skepticism that had caused many enterprise clients to maintain scraping as a primary or parallel channel.

Screen scraping and credential-based connectivity retained 29.4% share (USD 1.86 billion, 2025), concentrated in markets and financial institutions where open-banking API infrastructure remains immature — specifically smaller U.S. credit unions below USD 2 billion in assets, most Latin American banks, and Southeast Asian institutions outside Singapore and Australia. The scraping segment's CAGR of 3.8% over the forecast period is the lowest within the connectivity category, driven by progressive regulatory displacement (the CFPB rule effectively sets a sunset timeline for credential-based access at covered institutions) and by bank security teams upgrading authentication infrastructure to block automated credential submission as part of broader fraud prevention programs. FDX-standard direct data access held 12.6% share, with its adoption concentrated among Tier-1 U.S. banks that have invested in FDX-compliant API infrastructure specifically to satisfy the CFPB rule's data-access requirements. Hybrid connectivity (API primary, scraping fallback) accounted for 9.7% and is expected to decline as API coverage reaches sufficient institutional breadth to eliminate fallback requirements for the top 500 U.S. financial institutions by 2027.

By Application:

Credit underwriting and alternative scoring captured 28.7% of application revenue (USD 1.81 billion, 2025), the single largest application segment in the financial data aggregation platform market. Its leadership is causally explained by the intersection of two simultaneous developments: Fannie Mae's DU v11.1 acceptance of cash-flow income verification and the CFPB's parallel July 2024 guidance clarifying that cash-flow data used in credit decisioning is subject to Equal Credit Opportunity Act (ECOA) fairness requirements — a guidance that increased compliance complexity but simultaneously validated cash-flow underwriting as a legitimate regulated practice, giving bank credit risk committees the legal cover to approve its adoption. Nova Credit's partnership with American Express to underwrite cross-border credit files using international bank transaction data, operational across 12 countries by Q2 2025, exemplifies the credit scoring application's expansion beyond domestic income verification into international credit portability.

Personal finance management held 23.4% of application revenue (USD 1.48 billion, 2025). Despite consumer PFM's role as the original driver of financial data aggregation adoption, its revenue share has declined from 31.2% in 2022 as higher-margin B2B credit and payment applications have grown faster. Payment initiation and account verification captured 19.8%, accelerating sharply after the CFPB's confirmation that Real-Time Payments (RTP) and FedNow instant-transfer initiation fall within the Personal Financial Data Rights Rule's scope — bringing account verification for instant payment initiation into the regulated open-banking framework. Wealth management and investment advisory contributed 16.3%, with Schwab, Fidelity, and Vanguard all expanding API-based account aggregation for held-away asset visibility in their advisor platforms during 2025. Regulatory reporting and compliance analytics accounted for 11.8%, primarily from bank compliance departments using aggregated transaction data to generate Community Reinvestment Act (CRA) assessment reports and Bank Secrecy Act (BSA) transaction pattern analysis.

By End-User:

Fintech applications and neobanks constituted the largest end-user segment of the financial data aggregation platform market in 2025, capturing 36.4% of revenue at USD 2.30 billion. Their leading position reflects the founding architecture of modern fintech: nearly every consumer financial application built since 2016 — from neobanks (Chime, Dave, Current) to investment apps (Robinhood, Acorns) to BNPL platforms (Affirm, Klarna) — is built on aggregation platform APIs rather than direct bank data agreements, creating a structural dependency that makes aggregation platform fees a non-negotiable cost of goods sold for fintech business models. Chime alone processes an estimated 280 million monthly aggregated data queries through Plaid's infrastructure, a volume scale that makes the per-query economics of the aggregation layer a board-level concern rather than a procurement afterthought.

Banks and credit unions held 27.8% share (USD 1.76 billion, 2025). The CFPB rule converted banks from passive data providers into active aggregation platform clients: to comply with the rule's consumer-permissioned data-sharing requirements, banks must deploy their own certified third-party data-access APIs, creating a new category of platform procurement in which banks are simultaneously data source and data consumer. Wealth management and robo-advisory firms captured 18.6% (USD 1.18 billion), with growth driven by SEC guidance encouraging advisor platforms to aggregate held-away accounts for fiduciary completeness assessments. Insurance and lending platforms held 11.4%, growing at 23.8% as property and casualty insurers adopt bank-transaction data for telematics-equivalent behavioral risk scoring — using spending pattern analysis as a proxy for life-stage and financial-stability risk factors. Enterprise corporate treasury accounted for 5.8%, a nascent segment gaining traction as multinationals deploy aggregation platforms for real-time global cash visibility across 40–120 banking relationships.

Regional Analysis

North America:

Backed by the CFPB's Personal Financial Data Rights Rule — the most consequential open-banking regulation enacted in the region's history — and the Financial Data Exchange's FDX API standard now adopted by institutions holding over USD 14 trillion in consumer financial assets, North America's financial data aggregation platform market captured 40.8% of global revenue at USD 2.58 billion in 2025. The United States generates 94% of the North American figure, with San Francisco-headquartered Plaid and Salt Lake City-based MX Technologies operating the two largest independent aggregation networks. New York's concentration of wealth management firms and investment banks produces a disproportionate share of high-value API query revenue: Goldman Sachs' Marcus platform and Morgan Stanley's Wealth Management digital tools both rely on aggregation platform infrastructure for account-held-away visibility, generating enterprise contract values 8–12x higher than equivalent retail fintech agreements. Canada's Financial Consumer Agency completed its Consumer-Driven Banking Framework consultation in February 2025, scheduling formal open-banking legislation for the 2026 Parliamentary session — a regulatory timeline that is generating anticipatory infrastructure investment from Canada's Big Eight banks in Toronto's Bay Street financial district. Mexico contributes through CNBV-regulated fintech lenders in Monterrey and Mexico City, whose credit-underwriting applications use aggregated SPEI transaction data as an alternative income signal for the 60% of Mexican adults lacking formal credit bureau records.

Europe:

Regulatory mandates under PSD2 — enforced since 2019 — and the PSD3 technical standards published for consultation in Q1 2025 requiring 99.5% API uptime and sub-500ms response times have progressively deepened open-banking infrastructure across the European financial data aggregation platform market, which held 29.3% share worth USD 1.85 billion in 2025. The UK leads European adoption despite operating outside the EU's PSD2 framework post-Brexit: the Joint Regulatory Oversight Committee's 2025 open-banking roadmap, committing to variable recurring payments and cross-sector data portability through 2030, provides the long-term regulatory certainty that enterprise clients require before committing multi-year platform contracts. Germany's stringent Schufa credit-bureau data protections and BaFin's interpretive caution around Article 22 automated-decisioning restrictions have slowed AI-enrichment adoption in Frankfurt's banking center, but Deutsche Bank's March 2025 pilot of MX-powered cash-flow underwriting for digital SME lending marks the first Tier-1 German bank deployment of AI-enriched aggregation data in a credit application. Sweden contributes disproportionately through Tink, now a Visa subsidiary, whose headquarters in Stockholm and engineering operations in Barcelona serve as the technical backbone for Visa's European open-banking strategy across 3,400 connected institutions. The Netherlands, where Amsterdam's ABN AMRO and ING operate among Europe's most advanced open-banking API implementations, functions as the EU's de facto aggregation platform proving ground for new product features before broader continental rollout.

Asia Pacific:

Australia's Consumer Data Right framework, which expanded from banking to energy and telecommunications sectors in 2024–2025 — making it the world's first cross-sector open-data aggregation regime — positioned Asia Pacific's financial data aggregation platform market at 18.4% global share, valued at USD 1.16 billion in 2025. Sydney and Melbourne-based CDR-accredited data recipients, including Frollo, WeMoney, and Basiq, are building the infrastructure that will eventually support energy bill consolidation alongside bank-account aggregation in a single consumer data interface — a product capability with no parallel in any other jurisdiction. Singapore's Monetary Authority of Singapore (MAS) financial data exchange (SGFinDex), operational since 2020 and expanded to insurance data in 2024, serves as the model for government-orchestrated aggregation infrastructure that India's Account Aggregator (AA) framework — administered from Mumbai's Bandra-Kurla Complex financial district — is scaling to reach 800 million potential users through the NBFC-AA network of nine licensed account aggregators including CAMSFinServ, Perfios, and OneMoney. Japan's Financial Services Agency March 2025 guidance mandating API connectivity for all registered electronic settlement agency service providers created compliance-driven procurement at Mizuho's digital banking subsidiary and NTT Data's financial services division, generating the first meaningful enterprise aggregation platform contract activity in Japan since the Banking Act amendments of 2017.

Latin America:

Credit market formalization across Brazil and Mexico — where 48% and 55% of adults respectively lack sufficient formal credit history for traditional scoring — has created the financial data aggregation platform market's most compelling credit-underwriting use case globally: alternative income and cash-flow scoring derived from mobile-money and PIX transaction data. Latin America's market reached USD 440 million (7.0% global share) in 2025, primarily concentrated in Sao Paulo, where Brazil's Banco Central's open-finance implementation (Fase 4, completed 2024) now covers insurance, pension, and investment data alongside banking — a regulatory completeness that positions Brazil as the most developed open-finance ecosystem in the Southern Hemisphere. Nubank's 100-million-customer base in Brazil and Mexico generates an estimated 420 million monthly aggregated data queries, making Nubank the single largest end-user of financial data aggregation infrastructure in the region and a reference client whose technology choices influence procurement decisions across 40+ Latin American neobanks and fintech lenders. Colombia's open-banking regulation, under development by the Superintendencia Financiera de Colombia since 2022, reached its API standardization phase in Q1 2025, with Bogota-based fintech lenders Addi and Rappi Financial anticipating commercial API deployments by mid-2026. The regional constraint on faster adoption is infrastructure fragility: a 2025 GSMA study found that 34% of Latin American mobile financial transactions experience connectivity interruption before completion, creating data completeness gaps that aggregation platforms must address through fallback data-estimation models unavailable to platforms optimized for high-connectivity North American environments.

Middle East & Africa:

Saudi Arabia's SAMA Open Banking Framework — published February 2022, Phase 2 fully operational in 2024 — and the UAE Central Bank's open-banking regulation under CBUAE guidelines effective Q1 2025 created the MEA financial data aggregation platform market's regulatory foundation, lifting the region to USD 284 million (4.5% global share) in 2025. Riyadh's fintech ecosystem, concentrated in the King Abdullah Financial District and the Saudi Fintech hub adjacent to SAMA's headquarters, generated 14 licensed open-banking participant registrations in 2024 — the highest single-year count in the GCC — with Lean Technologies and Tarabut Gateway emerging as the primary aggregation infrastructure providers for the Arabian Peninsula. Dubai's DIFC fintech cluster, specifically the DIFC Innovation Hub's 300+ resident technology firms, generated the UAE's largest concentration of financial data aggregation API consumption in 2025, driven by wealth management platforms servicing South Asian and GCC high-net-worth clients who maintain financial assets across six-to-twelve institutions simultaneously. South Africa's PASA (Payments Association of South Africa) open-banking working group published its data-sharing framework in March 2025, committing to API standardization by 2027 — a timeline that is generating anticipatory platform investment from Johannesburg's Standard Bank Group and FirstRand, both of which announced partnerships with international aggregation platform vendors during 2025.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software Platform (Aggregation Engine & API Gateway)

- Data Enhancement & Analytics Modules

- Compliance & Consent Management

- Professional Services (Implementation & Integration)

- Managed Services & Support

By Connectivity Method

- Screen Scraping / Credential-Based

- API-Based / OAuth 2.0 Open Banking

- FDX-Standard Direct Data Access

- Hybrid (API + Fallback Scraping)

By Application

- Personal Finance Management (PFM)

- Credit Underwriting & Alternative Scoring

- Wealth Management & Investment Advisory

- Payment Initiation & Account Verification

- Regulatory Reporting & Compliance Analytics

By End-User

- Banks & Credit Unions

- Fintech Applications & Neobanks

- Wealth Management & Robo-Advisory Firms

- Insurance & Lending Platforms

- Enterprise Corporate Treasury

By Deployment

- Cloud-Native SaaS

- Hybrid Cloud / On-Premise

- Private Cloud / Bank-Operated

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.32 B |

| Forecast Revenue (2034) | USD 27.44 B |

| CAGR (2025-2034) | 17.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software Platform (Aggregation Engine & API Gateway), Data Enhancement & Analytics Modules, Compliance & Consent Management, Professional Services (Implementation & Integration), Managed Services & Support), By Connectivity Method, (Screen Scraping / Credential-Based, API-Based / OAuth 2.0 Open Banking, FDX-Standard Direct Data Access, Hybrid (API + Fallback Scraping)), By Application, (Personal Finance Management (PFM), Credit Underwriting & Alternative Scoring, Wealth Management & Investment Advisory, Payment Initiation & Account Verification, Regulatory Reporting & Compliance Analytics), By End-User, (Banks & Credit Unions, Fintech Applications & Neobanks, Wealth Management & Robo-Advisory Firms, Insurance & Lending Platforms, Enterprise Corporate Treasury), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Private Cloud / Bank-Operated) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PLAID INC., MX TECHNOLOGIES, INC., TINK AB (VISA INC.), TRUELAYER LIMITED, YODLEE, INC. (ENVESTNET, INC.), FINICITY CORPORATION (MASTERCARD INCORPORATED), AKOYA LLC, BASIQ PTY LTD, LEAN TECHNOLOGIES, TARABUT GATEWAY, NOVA CREDIT, INC., STRIPE, INC. (FINANCIAL CONNECTIONS), INTUIT INC. (MINT / CREDIT KARMA DATA PLATFORM), PERFIOS ACCOUNT AGGREGATION SERVICES PVT. LTD., SALT EDGE INC., NORDIGEN (GOBANKING RATES GROUP), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Connectivity Method (API-Based Open Banking, Screen Scraping, FDX Direct Access, Hybrid Connectivity), By Application (PFM, Credit Scoring, Wealth Management, Payment Verification), Industry Trends & Forecast 2026-2034")

, By Connectivity Method (API-Based Open Banking, Screen Scraping, FDX Direct Access, Hybrid Connectivity), By Application (PFM, Credit Scoring, Wealth Management, Payment Verification), Industry Trends & Forecast 2026-2034")

, By Connectivity Method (API-Based Open Banking, Screen Scraping, FDX Direct Access, Hybrid Connectivity), By Application (PFM, Credit Scoring, Wealth Management, Payment Verification), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Financial Data Aggregation Platform Market?

The Global Financial Data Aggregation Platform Market was valued at USD 5.37 Billion in 2024 and is projected to reach USD 27.44 Billion by 2034, growing at a CAGR of 17.7% from 2026 to 2034, driven by rising adoption of open banking frameworks, increasing demand for real-time financial data connectivity, expanding fintech ecosystems, and growing integration of AI-powered financial analytics, embedded finance, and API-based account aggregation platforms worldwide.es worldwide.

Who are the major players in the Financial Data Aggregation Platform Market?

PLAID INC., MX TECHNOLOGIES, INC., TINK AB (VISA INC.), TRUELAYER LIMITED, YODLEE, INC. (ENVESTNET, INC.), FINICITY CORPORATION (MASTERCARD INCORPORATED), AKOYA LLC, BASIQ PTY LTD, LEAN TECHNOLOGIES, TARABUT GATEWAY, NOVA CREDIT, INC., STRIPE, INC. (FINANCIAL CONNECTIONS), INTUIT INC. (MINT / CREDIT KARMA DATA PLATFORM), PERFIOS ACCOUNT AGGREGATION SERVICES PVT. LTD., SALT EDGE INC., NORDIGEN (GOBANKING RATES GROUP), OTHERS

Which segments covered the Financial Data Aggregation Platform Market?

By Component, (Software Platform (Aggregation Engine & API Gateway), Data Enhancement & Analytics Modules, Compliance & Consent Management, Professional Services (Implementation & Integration), Managed Services & Support), By Connectivity Method, (Screen Scraping / Credential-Based, API-Based / OAuth 2.0 Open Banking, FDX-Standard Direct Data Access, Hybrid (API + Fallback Scraping)), By Application, (Personal Finance Management (PFM), Credit Underwriting & Alternative Scoring, Wealth Management & Investment Advisory, Payment Initiation & Account Verification, Regulatory Reporting & Compliance Analytics), By End-User, (Banks & Credit Unions, Fintech Applications & Neobanks, Wealth Management & Robo-Advisory Firms, Insurance & Lending Platforms, Enterprise Corporate Treasury), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Private Cloud / Bank-Operated)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Financial Data Aggregation Platform Market

Published Date : 26 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date