- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Flange Management Services Market Forecast 2034 | CAGR 7.0%

Global Flange Management Services Market Size, Share, Growth & Industry Analysis By Service Type (Bolt Tensioning, Flange Facing & Machining, Joint Integrity Management & Software, Hydraulic Torquing, Ultrasonic Bolt Monitoring), By End-User Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Water & Wastewater, Others), By Application (Onshore, Offshore Surface & Subsea) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

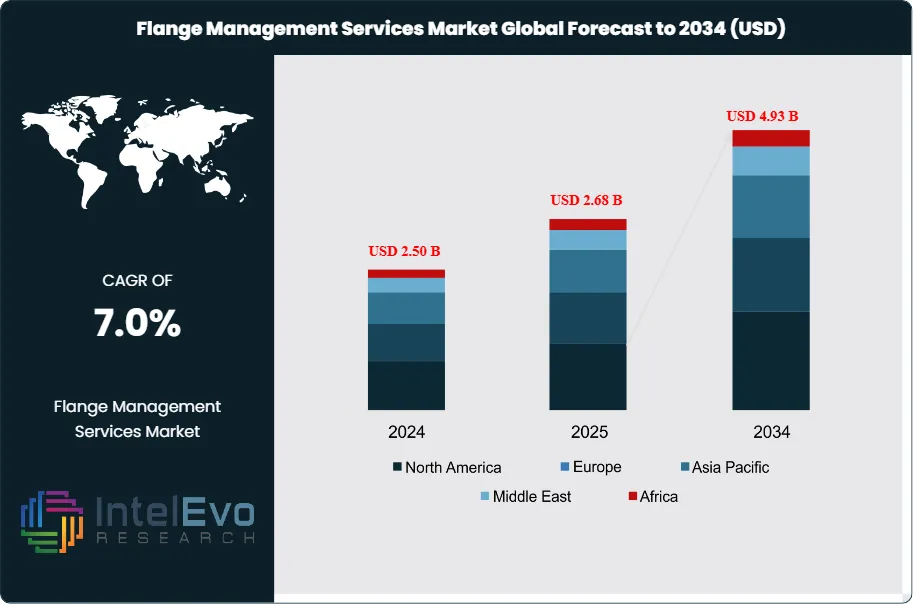

| USD 2.68 Billion | USD 4.93 Billion | 7.0% | Asia Pacific, 31.2% |

The Flange Management Services Market was valued at approximately USD 2.50 Billion in 2024 and reached USD 2.68 Billion in 2025. The market is projected to grow to USD 4.93 Billion by 2034, expanding at a CAGR of 7.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.25 Billion over the analysis period. The requirement for specialized leak detection and prevention during joint integrity procedures has transformed flange management from a basic maintenance task into a critical safety-driven technical service. Current industry analysis indicates that the expansion of midstream infrastructure and the modernization of aging refineries are the primary catalysts for service demand. As operators move toward zero-leakage policies to meet stringent ESG mandates, the reliance on third-party specialists for bolt tensioning, torquing, and flange facing has intensified.

Get More Information about this report -

Request Free Sample ReportThe supply-side of the flange management services market is undergoing a significant transition toward digital integration. Field technicians now utilize cloud-based joint integrity software to record torque values and assembly data in real-time, providing an audit trail for regulatory compliance with ASME PCC-1 standards. Demand and supply forces are currently balanced by the high volume of turnaround maintenance projects in the Middle East and North America, though the industry faces a tightening supply of ASME-certified technicians. Regulatory influences, particularly from the Bureau of Safety and Environmental Enforcement (BSEE) and the American Petroleum Institute (API), have mandated more frequent inspections of subsea and surface bolted connections, further anchoring market stability.

Technological effects are reshaping the competitive environment, with automation and robotics beginning to handle flange facing and machining in hazardous environments. The introduction of ultrasonic bolt monitoring systems allows for precise measurement of bolt elongation, reducing the margin of human error during critical path activities. Digitalization has enabled "Digital Twin" modeling for entire piping systems, where flange integrity is monitored through a centralized dashboard. Regional highlights show that emerging investment hotspots are concentrated in the Asia Pacific LNG sector and the Brazilian pre-salt offshore developments, where extreme pressures necessitate high-tier flange management services.

Risk factors for the flange management services market include the volatility of crude oil prices, which can lead to the deferral of non-essential maintenance. However, the mission-critical nature of joint integrity for safety and environmental protection often shields this sector from drastic CAPEX cuts. The integration of artificial intelligence in predictive maintenance schedules is a rising trend, allowing operators to identify potential flange failures before leaks occur. Based on trade data and supply-chain evaluation, the market is moving toward a service-as-a-product model, where long-term integrity contracts are replacing transactional service calls.

, By End-User Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Water & Wastewater, Others), By Application (Onshore, Offshore Surface & Subsea) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The industry was valued at USD 2.68 Billion in 2025 and is projected to reach USD 4.93 Billion by 2034, maintaining a steady CAGR of 7.0%.

- Segment Dominance: The Bolt Tensioning segment holds the leading share of 42.4% in 2025 due to its precision in high-pressure oil and gas applications.

- Segment Dominance: The Oil & Gas industry remains the primary end-user, accounting for 58.6% of the total market revenue in 2025.

- Driver: Stringent environmental regulations regarding methane slip and pipeline leaks are driving a USD 850 Million increase in service demand through 2034.

- Restraint: A shortage of specialized technical labor and certified joint integrity inspectors is limiting regional service expansion by approximately 4.5% annually.

- Opportunity: The adoption of digital joint integrity software presents a USD 1.1 Billion untapped addressable market for service providers offering integrated data solutions.

- Trend: The shift toward ultrasonic bolt load measurement is growing at an annual rate of 12.5%, replacing traditional hydraulic torquing in subsea applications.

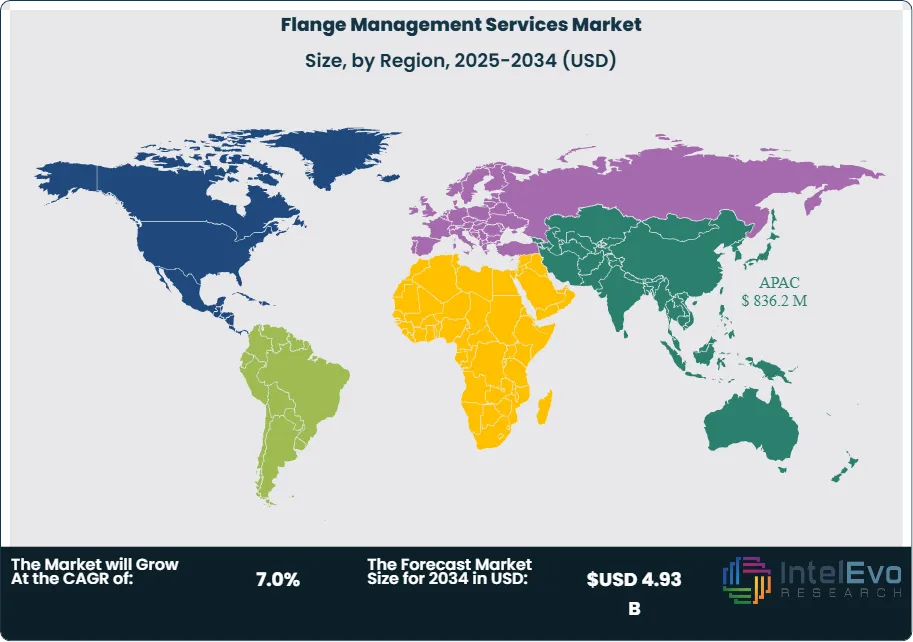

- Regional Analysis: Asia Pacific is the leading region with a 31.2% market share, valued at USD 836.2 Million in 2025, fueled by massive petrochemical expansions.

Competitive Landscape Overview

The flange management services market is moderately consolidated, with the top four players commanding a combined market share of 46.2% in 2025. Competition is primarily technology-driven, as companies differentiate themselves through proprietary joint integrity software and specialized hydraulic tools. Strategic pivots toward "Integrated Integrity Management" have become common, where service providers bundle flange management with piping inspections and valve maintenance. Recent competitive intensity has shifted toward M&A activity focused on local service boutiques to gain access to regional national oil company (NOC) contracts.

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| ENERPAC TOOL GROUP | United States | Leader | Hydratight Joint Integrity | Global | Launched digital torque logging system in May 2025 |

| ENERMECH | United Kingdom | Leader | Integrated Flange Management | Europe / MEA | Expanded Australian service hub for LNG projects, 2025 |

| BAKER HUGHES | United States | Leader | Pipeline & Process Services | North America | Integrated AI-driven leak detection in service kits, 2025 |

| STORK (FLUOR) | Netherlands | Challenger | Asset Integrity Services | Europe | Secured 5-year maintenance contract in North Sea, 2025 |

| TEAM INC. | United States | Challenger | Field Machining & Bolting | North America | Restructured technical service division for downstream, 2025 |

| SPARROWS GROUP | United Kingdom | Niche Player | Offshore Bolting Services | MEA / Asia | Partnered with local Saudi firms for Vision 2030, 2025 |

| DELTA CORPORATION | Qatar | Niche Player | High-Pressure Flange Services | Middle East | Commissioned new facility for flange facing tools, 2024 |

| INTERTEK | United Kingdom | Challenger | Technical Inspection Services | Global | Acquired regional bolting specialist in SE Asia, 2025 |

| SPERRY MARINE | United States | Niche Player | Subsea Flange Integrity | North America | Released new subsea ultrasonic bolt monitor, 2025 |

| STATS GROUP | United Kingdom | Challenger | Piping Integrity Solutions | Global | Signed strategic alliance with Middle Eastern NOC, 2026 |

Segmentation Analysis

The Global Flange Management Services Market is analyzed through several critical lenses, including service type, end-user industry, and application environment, reflecting the technical complexity of modern piping systems.

By Service Type

Bolt Tensioning stands as the dominant service type, representing a market share of 42.4% and a value of USD 1.14 Billion in 2025. This dominance is attributed to the superior accuracy and evenness of load distribution provided by hydraulic tensioning compared to traditional torquing. In high-pressure environments, such as offshore subsea manifolds and high-temperature refinery units, bolt tensioning is the preferred method to prevent gasket crushing and ensure a leak-free seal. The segment is characterized by high technical requirements and a transition toward automated tensioning systems that can handle multiple bolts simultaneously, reducing critical path time during plant turnarounds.

Flange Facing and Machining services account for 26.5% of the market share, valued at USD 0.71 Billion in 2025. This segment is driven by the physical degradation of flange surfaces over time due to corrosion, erosion, and thermal cycling. Field machining allows for the restoration of flange surfaces without removing the piping, providing significant cost savings for operators. The integration of portable, high-precision CNC machines has revolutionized this segment, allowing for tighter tolerances and surface finishes that meet modern metal-to-metal seal requirements.

Joint Integrity Management and Software services, while smaller at 18.2% share (USD 0.49 Billion in 2025), is the fastest-growing sub-segment. This area focuses on the "cradle-to-grave" tracking of every bolted connection in a facility. Operators are increasingly demanding digital records of torque values, technician IDs, and calibration certificates. This trend is driven by liability management and the need for a "golden thread" of information in asset integrity. Other services, including ultrasonic bolt monitoring and specialized torquing, make up the remaining 12.9% of the market.

By End-User Industry

The Oil & Gas sector remains the primary consumer of flange management services, capturing 58.6% of the market with a valuation of USD 1.57 Billion in 2025. Within this sector, the demand is split between upstream offshore platforms, midstream pipeline stations, and downstream refineries. The extreme pressures found in deepwater drilling and the corrosive nature of sour gas processing necessitate rigorous flange management protocols. Furthermore, the global push to reduce methane emissions from flared gas and leaking valves has directly increased the frequency of flange inspections and maintenance interventions.

The Power Generation industry accounts for 22.4% of the market share, valued at USD 0.60 Billion in 2025. This includes nuclear, thermal, and combined-cycle gas turbine (CCGT) plants. In nuclear facilities, flange management is a high-stakes activity where zero-leakage is a regulatory mandate. The specialized nature of steam-carrying flanges in thermal plants, which undergo extreme thermal expansion and contraction, requires unique torquing sequences and high-temperature gasket materials. The expansion of renewable energy infrastructure, particularly concentrated solar power (CSP) and geothermal plants, is providing new growth avenues for this segment.

Chemical and Petrochemical plants contribute 14.5% to the market revenue, totaling USD 0.39 Billion in 2025. These facilities often handle hazardous and volatile substances where a single flange failure can lead to catastrophic fires or environmental contamination. The complexity of petrochemical piping, with its numerous heat exchangers and pressure vessels, creates a high volume of flange joints per square meter, driving recurring maintenance demand. Other end-users, such as water treatment, pharmaceutical manufacturing, and marine industries, account for the remaining 4.5%.

By Application

Onshore applications represent the majority share of 64.8%, valued at USD 1.74 Billion in 2025. The vast networks of cross-country pipelines, sprawling refinery complexes, and power plants located on land provide a consistent volume of work. Onshore services are generally more price-competitive but require high mobility and the ability to deploy large teams for seasonal turnarounds. The growth in this segment is currently driven by the revitalization of shale gas infrastructure in North America and the construction of new chemical hubs in China and India.

Offshore applications, while smaller in volume at 35.2% (USD 0.94 Billion in 2025), command much higher margins due to the extreme environments and logistical challenges. Working on FPSOs, jack-up rigs, and subsea assets requires specialized subsea bolting tools and technicians trained for offshore survival. The segment is experiencing a surge in demand due to the focus on deepwater exploration in the Atlantic Margin and the expansion of offshore wind farms, which require high-integrity structural bolting in addition to traditional piping flanges.

Regional Analysis

The regional distribution of the flange management services market highlights the shifting centers of global industrial production and energy extraction.

Asia Pacific

Asia Pacific is the largest and fastest-growing region, holding a 31.2% market share with a value of USD 836.2 Million in 2025. This dominance is powered by China’s massive investment in downstream petrochemical capacity and India’s expansion of its domestic refining sector. Furthermore, Australia’s established LNG export infrastructure requires continuous flange integrity services to maintain operational safety. Regulatory frameworks in these countries are becoming increasingly aligned with international standards, forcing local operators to move away from in-house general maintenance toward specialized third-party flange management providers.

North America

North America follows with a 27.8% market share, valued at USD 745.0 Million in 2025. The market here is characterized by a high degree of technical sophistication and a strict regulatory environment governed by the EPA and OSHA. The Permian Basin and the Gulf of Mexico remain centers of high activity, while the aging infrastructure in the Northeast and Midwest drives a significant volume of repair and replacement work. The adoption of digital joint integrity software is highest in this region, as companies seek to minimize liability and improve operational efficiency through data-driven maintenance.

Europe

Europe maintains a 22.5% share, worth USD 603.0 Million in 2025. The regional market is driven by North Sea offshore activities and the stringent safety standards of the European Union. Germany and the UK are the primary hubs for technical innovation in bolting tools and integrity software. The European market is also at the forefront of the energy transition, with flange management services being adapted for hydrogen transport pipelines and carbon capture and storage (CCS) facilities, both of which require specialized sealing technologies due to the unique properties of hydrogen and CO2.

The Middle East & Africa (MEA)

The Middle East & Africa (MEA) region accounts for 14.5% of the market, valued at USD 388.6 Million in 2025. Saudi Arabia, the UAE, and Qatar are the key drivers, where massive oil and gas projects like the North Field Expansion and the Aramco expansion projects create consistent demand. The market in MEA is dominated by long-term maintenance contracts with national oil companies. In Africa, Nigeria and Angola provide significant offshore opportunities, though geopolitical risks and logistical hurdles can impact service delivery timelines.

Latin America

Latin America represents the remaining 4.0% of the market, valued at USD 107.2 Million in 2025. Brazil is the undisputed leader in this region, with Petrobras’ investments in pre-salt oil fields driving the need for high-pressure flange management services. Mexico also presents opportunities in its refining sector as it seeks to modernize its downstream assets. While smaller in share, Latin America offers high growth potential as offshore exploration expands into new frontiers like Guyana and Suriname.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Bolt Tensioning

- Flange Facing and Machining

- Joint Integrity Management & Software

- Hydraulic Torquing

- Ultrasonic Bolt Monitoring

By End-User Industry

- Oil & Gas (Upstream, Midstream, Downstream)

- Power Generation (Nuclear, Thermal, Renewables)

- Chemical and Petrochemical

- Water & Wastewater

- Others

By Application

- Onshore

- Offshore (Surface & Subsea)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.68 B |

| Forecast Revenue (2034) | USD 4.93 B |

| CAGR (2025-2034) | 7.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Tensioning, Flange Facing and Machining, Joint Integrity Management & Software, Hydraulic Torquing, Ultrasonic Bolt Monitoring), By End-User (Industry, Oil & Gas (Upstream, Midstream, Downstream), Power Generation (Nuclear, Thermal, Renewables), Chemical and Petrochemical, Water & Wastewater, Others), By Application, (Onshore, Offshore (Surface & Subsea)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ENERPAC TOOL GROUP, ENERMECH, BAKER HUGHES, STORK (FLUOR), TEAM INC., SPARROWS GROUP, DELTA CORPORATION, INTERTEK, SPERRY MARINE, STATS GROUP, IKM GRUPPEN, TENSION CONTROL BOLTS LTD, PARK OHIO HOLDINGS, INTEGRATED SUBSEA SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Water & Wastewater, Others), By Application (Onshore, Offshore Surface & Subsea) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By End-User Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Water & Wastewater, Others), By Application (Onshore, Offshore Surface & Subsea) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By End-User Industry (Oil & Gas, Power Generation, Chemical & Petrochemical, Water & Wastewater, Others), By Application (Onshore, Offshore Surface & Subsea) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Flange Management Services Market?

Global Flange management services market valued at USD 2.50B in 2024, reaching USD 4.93B by 2034, growing at a CAGR of 7.0% from 2026–2034.

Who are the major players in the Flange Management Services Market?

ENERPAC TOOL GROUP, ENERMECH, BAKER HUGHES, STORK (FLUOR), TEAM INC., SPARROWS GROUP, DELTA CORPORATION, INTERTEK, SPERRY MARINE, STATS GROUP, IKM GRUPPEN, TENSION CONTROL BOLTS LTD, PARK OHIO HOLDINGS, INTEGRATED SUBSEA SERVICES, Others

Which segments covered the Flange Management Services Market?

By Service Type, (Tensioning, Flange Facing and Machining, Joint Integrity Management & Software, Hydraulic Torquing, Ultrasonic Bolt Monitoring), By End-User (Industry, Oil & Gas (Upstream, Midstream, Downstream), Power Generation (Nuclear, Thermal, Renewables), Chemical and Petrochemical, Water & Wastewater, Others), By Application, (Onshore, Offshore (Surface & Subsea))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Flange Management Services Market

Published Date : 07 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date