- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Flare Gas Recovery System Market Size & Forecast | CAGR 8.0%

Global Flare Gas Recovery System Market Size, Share, Growth & Industry Analysis By System Type (Enclosed Vapor Recovery Systems, Open Flare Gas Recovery Systems, Ejector-Based Recovery Systems, Mobile & Modular Recovery Units), By Application (Upstream Production Operations, Refinery & Petrochemical Operations, Midstream Gas Processing, LNG Terminals & Storage), By Capacity (Small, Medium, Large), By End-Use (Gas Sales, Power Generation, Reinjection, Feedstock Supply) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.1 Billion | USD 4.2 Billion | 8.0% | North America, 32.4% |

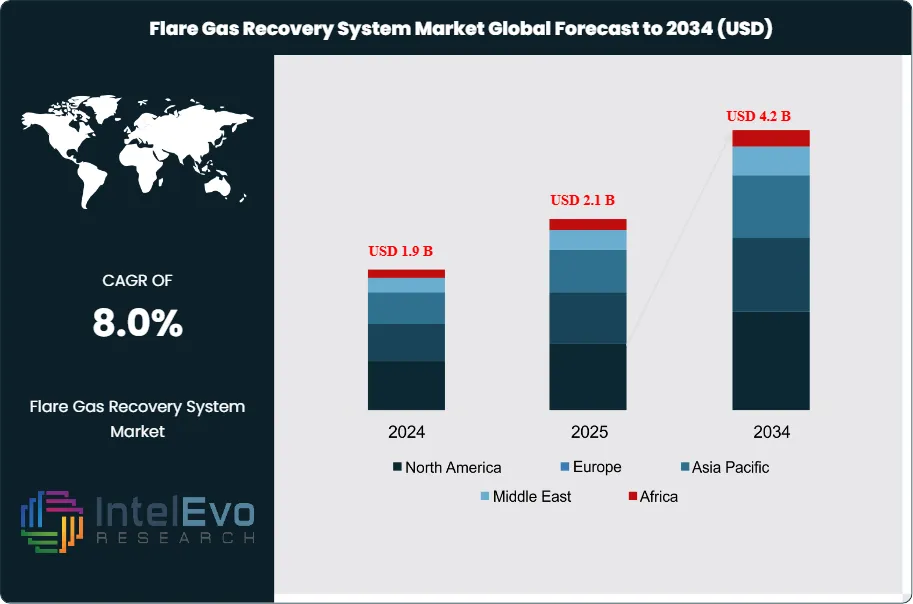

The Flare Gas Recovery System Market was valued at approximately USD 1.9 Billion in 2024 and reached USD 2.1 Billion in 2025. The market is projected to grow to USD 4.2 Billion by 2034, expanding at a CAGR of 8.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.1 Billion over the analysis period. Flare gas recovery systems capture and process hydrocarbon gases that would otherwise be combusted at flare stacks, converting waste streams into valuable fuel, feedstock, or power generation inputs across upstream, midstream, and downstream oil and gas operations.

Get More Information about this report -

Request Free Sample ReportMarket expansion is driven by tightening emissions regulations, carbon pricing mechanisms, and operator commitments to eliminate routine flaring. The World Bank Global Gas Flaring Reduction Partnership reports that global flaring volumes reached 139 billion cubic meters in 2024, representing USD 18 billion in lost gas value annually. Regulatory pressure from the EPA in North America, the EU Methane Regulation, and national flaring reduction mandates in Nigeria, Iraq, and Russia are compelling operators to invest in recovery infrastructure. The International Energy Agency targets a 90% reduction in oil and gas methane emissions by 2030, creating sustained demand for flare gas recovery system installations.

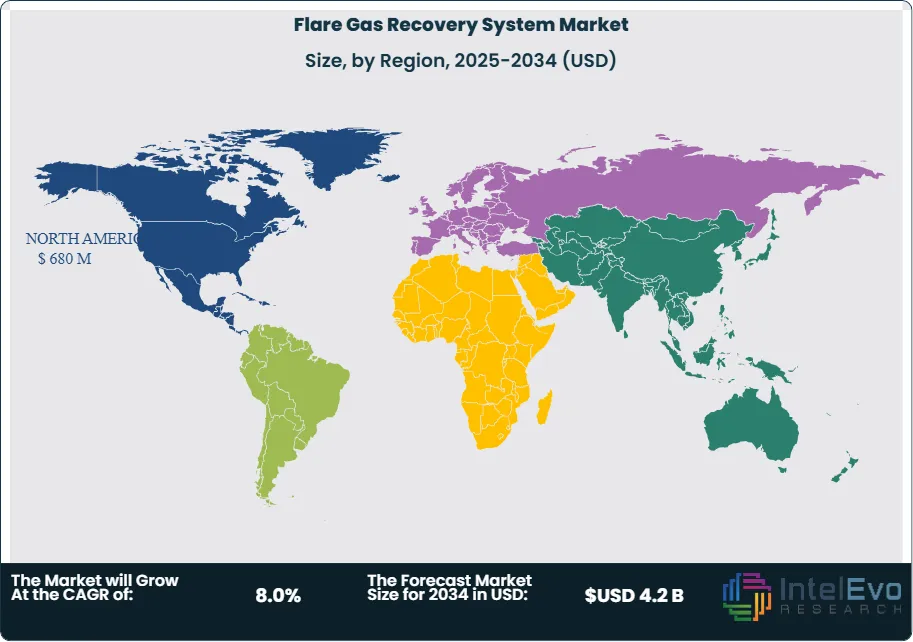

North America leads the flare gas recovery system market with 32.4% revenue share in 2025, valued at USD 680 million. The Permian Basin and Bakken Formation represent primary deployment zones. The Middle East follows with 27.6% share as national oil companies accelerate flaring reduction programs. Russia and the Caspian region account for 15.2% driven by government mandates targeting zero routine flaring by 2030.

Technology advancement is accelerating across the industry. Modular and skid-mounted recovery units now enable rapid deployment at remote wellheads, reducing installation timelines from 18 months to under 6 months. Digital monitoring systems integrate with SCADA platforms for real-time gas composition analysis and compression optimization. Small-scale liquefaction technology is emerging for stranded gas monetization. AI-enabled predictive maintenance reduces system downtime by 25-35%. The shift toward associated gas utilization for onsite power generation and distributed grid supply is creating new value chains beyond simple gas sales or reinjection.

, By Application (Upstream Production Operations, Refinery & Petrochemical Operations, Midstream Gas Processing, LNG Terminals & Storage), By Capacity (Small, Medium, Large), By End-Use (Gas Sales, Power Generation, Reinjection, Feedstock Supply) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The flare gas recovery system market is projected to expand from USD 2.1 Billion in 2025 to USD 4.2 Billion by 2034, registering a CAGR of 8.0% during 2025-2034.

- Segment Dominance (By Type): Enclosed vapor recovery systems command 44.8% market share in 2025, valued at USD 941 million, due to superior emissions control and regulatory compliance capabilities.

- Segment Dominance (By Application): Upstream production operations represent 52.3% of market demand in 2025 at USD 1.10 Billion, driven by wellhead and gathering system flare reduction initiatives.

- Driver: Regulatory pressure and carbon pricing mechanisms are accelerating adoption. Over 45 countries have implemented flaring reduction mandates, with penalty rates reaching USD 150 per tonne of CO2 equivalent in the EU.

- Restraint: High capital costs and infrastructure gaps limit deployment in remote locations. Average system costs range from USD 5 million to USD 25 million, with payback periods of 3-7 years depending on gas prices.

- Opportunity: Modular and portable recovery systems present a USD 780 million addressable market by 2034, enabling cost-effective deployment at marginal wells and temporary production sites.

- Trend: Onsite power generation using recovered flare gas is being adopted by 38% of new installations in 2025, enabling grid-independent operations and reduced diesel consumption at remote facilities.

- Regional Analysis: North America leads the global market with 32.4% share and USD 680 million revenue in 2025, supported by Permian Basin production growth and state-level flaring restrictions.

Competitive Landscape Overview

The flare gas recovery system market exhibits moderate consolidation, with the top four players capturing approximately 58% combined market share in 2025. John Zink Hamworthy leads through its extensive combustion and emissions control portfolio, followed by Zeeco Inc., Honeywell UOP, and Wärtsilä Corporation. Competition centers on technology differentiation, with suppliers emphasizing system efficiency, modular design, and digital integration. Recent strategic activity has intensified, including three acquisitions exceeding USD 100 million and multiple capacity expansions across the Middle East and North America.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| JOHN ZINK HAMWORTHY | US | Leader | ZINK FGRU Platform | North America | Launched modular recovery unit (Feb 2025) |

| ZEECO INC. | US | Leader | Zeeco Recovery Systems | Global | Expanded Middle East operations (Jan 2025) |

| HONEYWELL UOP | US | Leader | Callidus FGRS | North America | Integrated AI monitoring suite (Mar 2025) |

| WÄRTSILÄ CORPORATION | Finland | Challenger | Wärtsilä Gas Recovery | Europe | Partnership with Equinor (Dec 2024) |

| SCHLUMBERGER (SLB) | US | Challenger | REDA Gas Recovery | Middle East | Acquired gas processing firm USD 320M (Jun 2025) |

| MPR INDUSTRIES | US | Niche Player | MPR Vapor Recovery | North America | New compact system launch (Sep 2025) |

| AEREON | US | Niche Player | AEREON VRU Systems | Americas | Expanded Latin America presence (Nov 2025) |

| CIMARRON ENERGY | US | Niche Player | Cimarron Gas Recovery | North America | Digital monitoring upgrade (Jan 2026) |

By System Type

The flare gas recovery system market segmentation by type reveals enclosed vapor recovery systems as the dominant category with 44.8% share valued at USD 941 million in 2025. These systems capture vent gases within sealed containment, compress the recovered hydrocarbons, and route them to processing or utilization equipment. Enclosed systems meet stringent emissions standards including EPA New Source Performance Standards and EU Industrial Emissions Directive requirements. Open flare gas recovery systems hold 31.5% market share at USD 662 million, primarily deployed at existing production facilities where retrofit economics favor simpler configurations. These systems capture a portion of flare header gases but allow residual combustion at the flare tip. Ejector-based recovery systems account for 15.2% share at USD 319 million, utilizing high-pressure motive gas to entrain and compress low-pressure flare streams without mechanical compressors. Mobile and modular recovery units comprise the remaining 8.5% at USD 178 million, serving temporary production operations and marginal well applications where permanent infrastructure is uneconomic.

By Application

Application-based segmentation of the flare gas recovery system market positions upstream production operations as the largest segment with 52.3% share worth USD 1.10 Billion in 2025. Wellhead separators, gathering systems, and tank batteries generate associated gas streams requiring recovery infrastructure. The Permian Basin alone operates over 15,000 active flares, representing significant recovery potential. Refinery and petrochemical operations represent 28.4% share at USD 596 million, addressing process upset venting, tank breathing losses, and routine flaring from crude distillation and cracking units. Midstream gas processing facilities account for 12.8% at USD 269 million, targeting inlet separator vents, amine unit flashes, and dehydration system emissions. LNG terminals and storage operations comprise 6.5% at USD 136 million, focusing on boil-off gas recovery and ship loading vapor return systems.

By Capacity

Capacity-based analysis shows medium-capacity systems between 1 and 10 MMSCFD commanding 48.6% of the flare gas recovery system market in 2025, valued at USD 1.02 Billion. This range addresses typical wellpad and gathering system applications where gas volumes support economic recovery but do not justify large-scale infrastructure. Small-capacity systems below 1 MMSCFD account for 26.3% share at USD 552 million, serving marginal wells, tank batteries, and stranded gas sites where modular equipment enables cost-effective deployment. Large-capacity systems exceeding 10 MMSCFD represent 25.1% at USD 527 million, installed at major production facilities, refineries, and gas processing plants where high-volume recovery justifies substantial capital investment.

By End-Use

End-use segmentation of the flare gas recovery system market reveals gas sales and pipeline injection as the primary utilization pathway with 42.1% share at USD 884 million in 2025. Recovered gas meeting pipeline specifications generates direct revenue through gas marketing. Onsite power generation represents 28.7% at USD 603 million, with operators using recovered gas to fuel reciprocating engines or gas turbines for facility power, reducing diesel imports at remote locations. Reinjection for enhanced oil recovery accounts for 18.4% at USD 386 million, where operators inject recovered gas into reservoirs to maintain pressure and improve crude recovery rates. Feedstock supply to petrochemical and processing facilities comprises 10.8% at USD 227 million, providing NGLs and lean gas for downstream manufacturing.

Regional Analysis

North America

North America commands 32.4% of the global flare gas recovery system market with USD 680 million revenue in 2025. The United States dominates regional consumption at 84% share, driven by Permian Basin production growth and state-level flaring restrictions in Texas and New Mexico. The Texas Railroad Commission has implemented gas capture requirements mandating 98% capture rates by 2030. The Bakken Formation in North Dakota operates under similar constraints following EPA consent decrees. Canada contributes 12% of regional demand, with Alberta Energy Regulator directives targeting routine flaring elimination. Montney and Duvernay shale developments are incorporating recovery systems in initial field design. Mexico accounts for 4% as Pemex implements flaring reduction programs at legacy onshore and offshore facilities. Digital monitoring adoption leads globally, with 52% of new installations in North America incorporating real-time gas composition analysis and automated compression control.

Middle East and Africa

The Middle East and Africa region holds 27.6% of the flare gas recovery system market with USD 580 million in 2025. Saudi Arabia leads at 32% regional share, with Saudi Aramco operating under a zero routine flaring commitment since 2019. The Kingdom has invested over USD 1.5 billion in flare reduction infrastructure across Ghawar, Shaybah, and offshore fields. Iraq follows at 24%, where flaring volumes exceed 17 billion cubic meters annually, representing the largest untapped recovery opportunity globally. The Iraq National Oil Company has initiated recovery projects at Rumaila and West Qurna with international partners. The UAE contributes 18% through ADNOC programs at onshore and offshore facilities. Nigeria accounts for 14% as the federal government enforces flare-out legislation with penalty rates of USD 3.50 per 1,000 standard cubic feet. The region benefits from associated gas utilization for power generation in countries with constrained electricity infrastructure.

Europe

Europe represents 14.3% of the flare gas recovery system market with USD 300 million in 2025. Norway leads regional demand at 38% share, with the Norwegian Petroleum Directorate enforcing strict flaring limits since the 1970s. Equinor and other North Sea operators have achieved near-zero routine flaring. The United Kingdom follows at 28%, driven by North Sea Transition Authority requirements and carbon pricing through the UK Emissions Trading Scheme. The Netherlands contributes 14% through Groningen field operations and Rotterdam refining complex upgrades. Russia accounts for 12% of European market share, where government Resolution 7 mandates 95% associated petroleum gas utilization. The EU Methane Regulation adopted in 2024 requires operators to submit flaring reduction plans and prohibits routine flaring at new developments, creating sustained demand through 2034.

Asia Pacific

Asia Pacific captures 15.2% of the flare gas recovery system market with USD 319 million in 2025 and represents the fastest-growing region at 9.4% CAGR through 2034. China leads at 42% regional share, driven by CNOOC, PetroChina, and Sinopec programs addressing associated gas from the Bohai Bay and Sichuan Basin. India follows at 22%, with ONGC and Reliance Industries implementing recovery at Mumbai High and Krishna-Godavari Basin installations. Indonesia contributes 18% as Pertamina addresses legacy flaring at aging Sumatra and Kalimantan fields. Malaysia accounts for 12% via Petronas offshore recovery programs in the Sarawak and Sabah basins. Southeast Asian operators are increasingly deploying modular systems for marginal field developments where pipeline infrastructure is absent. Regional growth is supported by rising domestic gas demand and LNG export ambitions requiring feedstock supply.

Latin America

Latin America accounts for 10.5% of the flare gas recovery system market with USD 221 million in 2025. Brazil dominates at 48% regional share, with Petrobras pre-salt operations incorporating recovery systems in initial field design. The Lula, Buzios, and Tupi fields utilize recovered gas for platform power generation and pipeline export. Mexico represents 28% as Pemex rehabilitation programs address aging infrastructure at Cantarell and Ku-Maloob-Zaap complexes. Argentina contributes 14% through Vaca Muerta shale development, where YPF and private operators are installing recovery equipment to capture associated gas from oil-directed wells. Colombia accounts for 10% via Ecopetrol programs at heavy oil operations in the Llanos Basin. Regional growth is constrained by economic volatility and currency fluctuations affecting capital project economics, though ESG pressure from international investors is compelling adoption.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By System Type

- Enclosed Vapor Recovery Systems

- Open Flare Gas Recovery Systems

- Ejector-Based Recovery Systems

- Mobile and Modular Recovery Units

By Application

- Upstream Production Operations

- Refinery and Petrochemical Operations

- Midstream Gas Processing

- LNG Terminals and Storage

By Capacity

- Small (Below 1 MMSCFD)

- Medium (1-10 MMSCFD)

- Large (Above 10 MMSCFD)

By End-Use

- Gas Sales and Pipeline Injection

- Onsite Power Generation

- Reinjection for Enhanced Oil Recovery

- Feedstock Supply

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.1 B |

| Forecast Revenue (2034) | USD 4.2 B |

| CAGR (2025-2034) | 8.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By System Type, (Enclosed Vapor Recovery Systems, Open Flare Gas Recovery Systems, Ejector-Based Recovery Systems, Mobile and Modular Recovery Units), By Application, (Upstream Production Operations, Refinery and Petrochemical Operations, Midstream Gas Processing, LNG Terminals and Storage), By Capacity, (Small (Below 1 MMSCFD), Medium (1-10 MMSCFD), Large (Above 10 MMSCFD)), By End-Use, (Gas Sales and Pipeline Injection, Onsite Power Generation, Reinjection for Enhanced Oil Recovery, Feedstock Supply) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JOHN ZINK HAMWORTHY COMBUSTION, ZEECO INC., HONEYWELL UOP, WÄRTSILÄ CORPORATION, SCHLUMBERGER (SLB), MPR INDUSTRIES, AEREON, CIMARRON ENERGY, FLARETEC, ENERAQUE, COSASCO, PROCESS COMBUSTION CORPORATION, MAN ENERGY SOLUTIONS, EXTERRAN CORPORATION, PIONEER ENERGY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Upstream Production Operations, Refinery & Petrochemical Operations, Midstream Gas Processing, LNG Terminals & Storage), By Capacity (Small, Medium, Large), By End-Use (Gas Sales, Power Generation, Reinjection, Feedstock Supply) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Upstream Production Operations, Refinery & Petrochemical Operations, Midstream Gas Processing, LNG Terminals & Storage), By Capacity (Small, Medium, Large), By End-Use (Gas Sales, Power Generation, Reinjection, Feedstock Supply) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Upstream Production Operations, Refinery & Petrochemical Operations, Midstream Gas Processing, LNG Terminals & Storage), By Capacity (Small, Medium, Large), By End-Use (Gas Sales, Power Generation, Reinjection, Feedstock Supply) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Flare Gas Recovery System Market?

Global Flare Gas Recovery System Market valued at USD 1.9B in 2024, reaching USD 4.2B by 2034, growing at a CAGR of 8.0% from 2026–2034.

Who are the major players in the Flare Gas Recovery System Market?

JOHN ZINK HAMWORTHY COMBUSTION, ZEECO INC., HONEYWELL UOP, WÄRTSILÄ CORPORATION, SCHLUMBERGER (SLB), MPR INDUSTRIES, AEREON, CIMARRON ENERGY, FLARETEC, ENERAQUE, COSASCO, PROCESS COMBUSTION CORPORATION, MAN ENERGY SOLUTIONS, EXTERRAN CORPORATION, PIONEER ENERGY, Others

Which segments covered the Flare Gas Recovery System Market?

By System Type, (Enclosed Vapor Recovery Systems, Open Flare Gas Recovery Systems, Ejector-Based Recovery Systems, Mobile and Modular Recovery Units), By Application, (Upstream Production Operations, Refinery and Petrochemical Operations, Midstream Gas Processing, LNG Terminals and Storage), By Capacity, (Small (Below 1 MMSCFD), Medium (1-10 MMSCFD), Large (Above 10 MMSCFD)), By End-Use, (Gas Sales and Pipeline Injection, Onsite Power Generation, Reinjection for Enhanced Oil Recovery, Feedstock Supply)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Flare Gas Recovery System Market

Published Date : 27 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date