- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

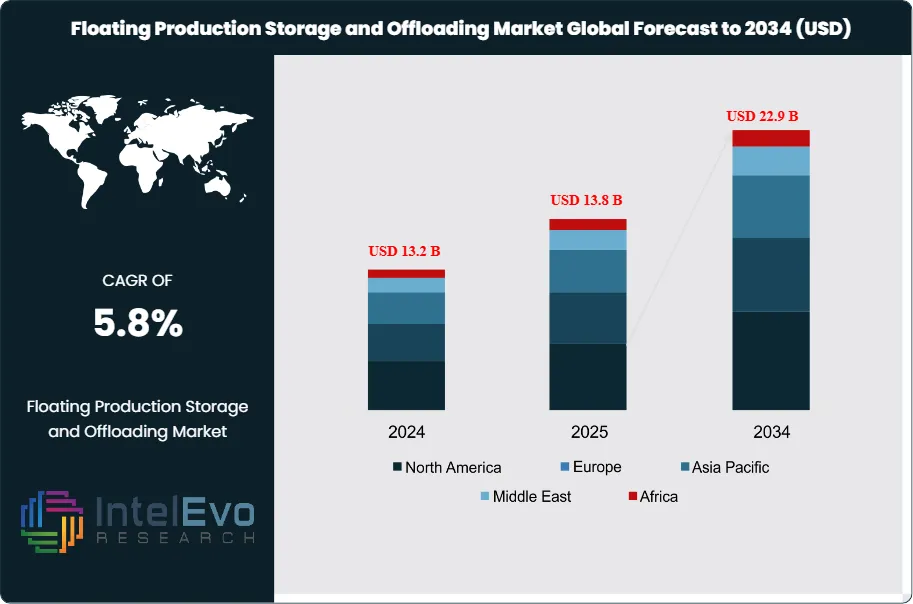

Floating Production Storage and Offloading Market

Global Floating Production Storage and Offloading Market Size, Share & Industry Analysis By Ownership Model (Lease and Operate, Sale and Transfer), By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-Deepwater, Shallow-Water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends, Strategic Developments & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

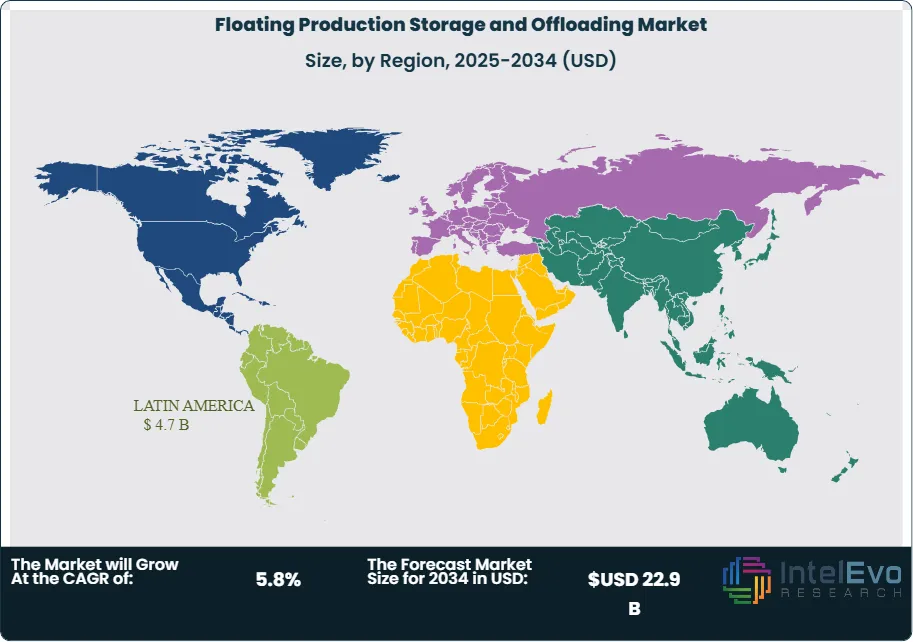

| USD 13.8 Billion | USD 22.9 Billion | 5.8% | Latin America, 34.0% |

The Floating Production Storage and Offloading Market was valued at approximately USD 13.2 Billion in 2024 and increased to USD 13.8 Billion in 2025. The market is projected to reach nearly USD 22.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2026 to 2034. The growth path is mathematically aligned with the forecast horizon and reflects the pace of new deepwater sanctions, vessel awards, and long-term offshore production contracts.

Get More Information about this report -

Request Free Sample ReportThe Floating Production Storage and Offloading Market remains tied to deepwater and ultra-deepwater capital spending. Brazil anchors the installed base and the forward orderbook. At the start of the 2025 planning cycle, Brazil accounted for 45 operating FPSOs and 15 of 36 FPSOs on order worldwide, which placed more than 40% of visible near-term demand in one country. Guyana added another layer of demand through ExxonMobil-led developments, while Angola and the wider West African margin supported fresh charter starts and redevelopment programs. This geographic concentration gives the market a strong pipeline, but it also raises exposure to operator procurement delays, local-content rules, and yard capacity constraints.

Demand in the Floating Production Storage and Offloading Market comes from three clear forces. First, deepwater oil remains cost-competitive on a full-cycle basis in several basins. Second, FPSOs shorten export infrastructure needs because they process, store, and offload offshore. Third, leasing models reduce upfront operator capital pressure on selected projects. Supply remains concentrated among a small group of specialist contractors with long execution records, turret and mooring know-how, and established yard networks. SBM Offshore reported a 2025 directional backlog of USD 31.1 Billion and a fleet of 16 FPSOs. MODEC reported an order backlog of USD 18.6 Billion at 2025 year-end and a record USD 12.2 Billion O&M backlog. These figures show how backlog strength supports current construction visibility.

Regulation shapes project economics. Petrobras continues to press local-content requirements in Brazil. During 2025, cost tension around at least one Petrobras FPSO tender showed that a quoted day rate of USD 1.5 million could trigger procurement reviews and contract pressure. At the same time, technology is changing vessel design. Agogo FPSO entered service with a carbon-capture pilot, and leading contractors moved carbon-capture and digital integrity systems closer to commercial deployment. Digital twins, predictive maintenance, remote inspection, and automation are moving from pilot use to commercial use because operators want higher uptime and lower emissions intensity.

Regional momentum stays strongest in Latin America, which represented 34.0% of global market revenue in 2025, equal to USD 4.7 Billion. Asia Pacific followed with 23.0%, Europe with 18.0%, Middle East & Africa with 16.0%, and North America with 9.0%. Investment hotspots include Brazil’s pre-salt, Guyana’s Stabroek block, Angola’s redevelopment programs, and selected frontier projects in Norway and the Eastern Mediterranean. The result is a market with visible medium-term demand, high contract values, and persistent execution risk.

, By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-Deepwater, Shallow-Water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends, Strategic Developments & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Floating Production Storage and Offloading Market stood at USD 13.8 Billion in 2025 and is projected to reach USD 22.9 Billion by 2034 at a 5.8% CAGR across 2026–2034. The growth path reflects sustained deepwater awards, large Brazilian pre-salt demand, and fresh Guyana capacity additions.

- Segment Dominance: By ownership model, Lease and Operate led the market with 62.0% share in 2025, equal to USD 8.6 Billion. Contractors with large O&M backlogs and existing fleet platforms held the strongest position in this format.

- Segment Dominance: By application, Crude Oil Production held the largest market share at 71.0% in 2025, or USD 9.8 Billion. Most large projects in Brazil, Guyana, and Angola remain oil-led developments with associated gas handling rather than pure gas monetization.

- Driver: The main growth driver is the deepwater project pipeline. Brazil alone accounted for 45 operating FPSOs and 15 of 36 units on order in late 2024, which materially lifted 2025 award visibility.

- Restraint: The main restraint is capital and procurement inflation. Petrobras reviewed at least one FPSO tender in 2025 after a quoted USD 1.5 million daily rate and local-content issues raised cost concerns.

- Opportunity: The largest opportunity sits in redeployment, brownfield growth, and frontier deepwater sanctioning. Hammerhead and Maromba activity points to a multi-billion-dollar opening for newbuild and refurbished FPSO supply through the forecast period.

- Trend: The strongest trend is lower-emission FPSO design. Agogo launched a 15-year charter with carbon-capture capability, while other contractors advanced offshore carbon-capture and digital monitoring suited to FPSO operations.

- Regional Analysis: Latin America led the market with 34.0% share in 2025, or USD 4.7 Billion. Brazil remained the largest national market and Guyana delivered the fastest expansion rate.

Competitive Landscape

The Floating Production Storage and Offloading Market is moderately consolidated. The top four players held an estimated 46.0% market share in 2025. Competition is driven by execution record, hull conversion economics, financing strength, local-content compliance, and long-term O&M capability. Competitive intensity rose in 2025 as Guyana awards moved forward, Brazil kept large tenders active, and contractors pushed lower-emission FPSO designs to defend margins and win complex charters.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SBM OFFSHORE | Netherlands | Leader | FPSO Jaguar | Latin America | Completed USD 1.5 Billion financing for FPSO Jaguar in Nov 2024 |

| MODEC | Japan | Leader | Hammerhead FPSO | Latin America | Won Hammerhead FPSO scope for Guyana and advanced to EPCI after FID in 2025 |

| YINSON PRODUCTION | Malaysia | Challenger | Agogo FPSO | Middle East & Africa | Achieved first oil at Agogo and started a 15-year firm charter in 2025 |

| BW OFFSHORE | Norway | Challenger | FPSO Maromba | Latin America | Backed Maromba redevelopment through Brazil FID and vessel refurbishment in 2025 |

| SEATRIUM | Singapore | Challenger | P-84 / P-85 FPSO newbuilds | Latin America | Continued Petrobras P-84 and P-85 construction program through 2025 |

| ALTERA INFRASTRUCTURE | UK | Niche Player | Petrojarl I | Latin America | Stayed active in redeployment and mature-field FPSO operations in Brazil in 2025 |

| BLUEWATER ENERGY SERVICES | Netherlands | Niche Player | Aoka Mizu FPSO | Europe | Maintained North Sea FPSO base and life-extension focus in 2025 |

| BUMI ARMADA | Malaysia | Niche Player | Armada Olombendo FPSO | Asia Pacific | Maintained Asia-linked fleet exposure and charter portfolio discipline in 2025 |

| MITSUI O.S.K. GROUP | Japan | Niche Player | FPSO conversion and marine support capability | Asia Pacific | Expanded participation in offshore marine support tied to floating production in 2025 |

| SHAPOORJI PALLONJI ENERGY | India | Niche Player | Brazil-bound FPSO tender participation | Latin America | Remained active in Petrobras-related FPSO procurement discussions in 2025 |

By Ownership Model

The Lease and Operate segment led the Floating Production Storage and Offloading Market with an estimated 62.0% share in 2025, equivalent to USD 8.6 Billion. This segment remains dominant because operators use leased FPSOs to reduce early capital strain, shorten field development cycles, and shift part of execution risk to specialist contractors. Lease structures are strongest in Brazil, West Africa, and selected redeployments where contractors can combine financing, engineering, and O&M in one package. The Sale and Transfer segment accounted for 38.0%, or USD 5.2 Billion, and expanded in Guyana and selected Petrobras-linked projects where operators wanted more direct long-term control over strategic production assets. Lease and Operate still holds the edge because the installed contractor base is large, proven, and backed by strong long-term service cash flows. Sale and Transfer gains share where supermajors and national oil companies want asset control, lower lifetime charter cost, or stronger domestic-content alignment.

By Hull Construction

Converted hull FPSOs held the largest share of the Floating Production Storage and Offloading Market at 58.0% in 2025, or USD 8.0 Billion. The segment remains strong because conversions usually offer shorter build schedules and lower upfront cost than full newbuilds, especially for brownfield programs and medium-sized developments. Newbuild FPSOs represented 42.0%, equal to USD 5.8 Billion, and they are gaining ground in very large deepwater projects that need higher processing capacity, stronger gas handling systems, and longer design life. Converted units hold the bigger installed revenue share in 2025 because the global fleet base is older and broad. Newbuilds, however, post the faster forecast growth because fresh awards increasingly require low-emission design, digital monitoring systems, and integrated subsea tieback capability.

By Water Depth

The Deepwater segment accounted for 47.0% of the Floating Production Storage and Offloading Market in 2025, or USD 6.5 Billion. It remains the broadest segment because many producing basins still fall in the deepwater range and support both new projects and brownfield tiebacks. Ultra-deepwater followed closely at 39.0%, or USD 5.4 Billion, and is the faster-growth band through 2034. Brazil’s pre-salt, Guyana’s Stabroek block, and several frontier Atlantic Margin opportunities continue to push capital toward larger, more complex FPSOs in harsher environments and deeper reservoirs. Shallow-water and shelf redeployment represented 14.0%, equal to USD 1.9 Billion, and remains relevant for early production systems, lower-capex redevelopment, and selective regional fields in Asia and Africa.

By Application

Crude Oil Production dominated the Floating Production Storage and Offloading Market with 71.0% share in 2025, or USD 9.8 Billion. Large oil-led projects in Brazil, Guyana, and Angola keep this segment ahead because FPSOs remain the preferred offshore production solution where export pipelines are limited and storage flexibility matters. Gas and Condensate Production represented 18.0%, or USD 2.5 Billion, driven by projects that need stronger gas processing, reinjection, or associated condensate handling offshore. Early Production and Redeployment held 11.0%, or USD 1.5 Billion, and serves mature fields, appraisal programs, and lower-risk phased developments. Crude oil production remains the core revenue engine in 2025 because the largest sanctioned projects still target long-life offshore oil reserves.

Regional Analysis

Market in North America

North America accounted for 9.0% of the Floating Production Storage and Offloading Market in 2025, equal to USD 1.2 Billion. The region remains smaller than Latin America because the Gulf of Mexico uses a wider mix of floating production systems, fixed platforms, and subsea tiebacks rather than heavy FPSO concentration. The US is the core market. It supports engineering, subsea integration, and contractor services even when local installed FPSO numbers stay limited. Canada contributes through offshore project engineering and Atlantic basin know-how, though direct FPSO demand remains selective. Mexico offers medium-term potential through deepwater reform momentum, but execution remains slower than earlier expectations. Regional demand depends on high-value deepwater developments with clear export logic and stable oil-price assumptions.

Market in Europe

Europe held 18.0% of the Floating Production Storage and Offloading Market in 2025, equivalent to USD 2.5 Billion. The market is led by Germany, France, the UK, Norway, and the rest of Europe, with Norway carrying the strongest strategic weight through North Sea and Barents Sea offshore development planning. Europe is not the largest fleet market, but it remains central for FPSO technology, financing, marine engineering, and environmental standards. The Netherlands matters through contractor leadership, while the UK and Norway remain important for design, operations, and life-extension work. Cost discipline and concept redesign in projects such as Wisting show how future European FPSO demand can reopen when project economics improve.

Market in Asia Pacific

Asia Pacific represented 23.0% of the Floating Production Storage and Offloading Market in 2025, or USD 3.2 Billion. The region is anchored by China, Japan, India, Australia, and the wider Southeast Asian offshore corridor. Japan matters through MODEC’s global leadership and engineering base. China matters through yard capacity, fabrication activity, and refurbishment support for large floating systems. Australia remains one of the region’s most strategically relevant deployment markets because offshore developments require long-distance export solutions and complex floating production architecture. Asia Pacific is also central to the supply side of the market because many hull conversions, topside modules, and integration scopes depend on Asian yards.

Market in Latin America

Latin America led the Floating Production Storage and Offloading Market with 34.0% share in 2025, equal to USD 4.7 Billion. Brazil dominates the region by a wide margin and remains the single largest country market worldwide. Brazil had 45 operating FPSOs and 15 of 36 units on order globally. Guyana is the fastest-growing market in the region because ExxonMobil-led developments continue to add large-capacity FPSOs. Mexico contributes selective offshore demand but remains structurally smaller. Latin America combines strong reserve quality, deepwater development experience, and visible operator capital programs. It also carries the highest tender concentration and the heaviest exposure to local-content policy, cost inflation, and yard bottlenecks.

Market in Middle East & Africa

Middle East & Africa accounted for 16.0% of the Floating Production Storage and Offloading Market in 2025, or USD 2.2 Billion. The region is driven by UAE, Saudi Arabia, South Africa, and West African offshore markets inside the broader Rest of MEA bucket, especially Angola and Nigeria. Angola remains the most commercially important FPSO deployment zone in the region today. Agogo achieved first oil on 29 July 2025, started a 15-year firm charter, and carried a contract value above USD 5 Billion. The Gulf states matter more on capital access, offshore engineering, and energy financing than on installed FPSO count, while South Africa holds longer-term offshore opportunity if exploration success and field commercialization improve.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Ownership Model

- Lease and Operate

- Sale and Transfer

By Hull Construction

- Converted Hull

- Newbuild Hull

By Water Depth

- Deepwater

- Ultra-deepwater

- Shallow-water and Shelf Redeployment

By Application

- Crude Oil Production

- Gas and Condensate Production

- Early Production and Redeployment

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 13.8 B |

| Forecast Revenue (2034) | USD 22.9 B |

| CAGR (2025-2034) | 5.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Ownership Model (Lease and Operate, Sale and Transfer), By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-deepwater, Shallow-water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SBM OFFSHORE, MODEC, YINSON PRODUCTION, BW OFFSHORE, SEATRIUM, ALTERA INFRASTRUCTURE, BLUEWATER ENERGY SERVICES, BUMI ARMADA, SHAPOORJI PALLONJI ENERGY, MITSUI O.S.K. LINES, MITSUI E&S SHIPBUILDING, SAIPEM, TECHNIP ENERGIES, MITSUBISHI HEAVY INDUSTRIES, SAMSUNG HEAVY INDUSTRIES, COSCO SHIPPING HEAVY INDUSTRY, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-Deepwater, Shallow-Water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends, Strategic Developments & Forecast 2026–2034")

, By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-Deepwater, Shallow-Water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends, Strategic Developments & Forecast 2026–2034")

, By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-Deepwater, Shallow-Water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Technology Trends, Strategic Developments & Forecast 2026–2034")

Frequently Asked Questions

How big is the Floating Production Storage and Offloading Market?

Floating Production Storage and Offloading Market

Who are the major players in the Floating Production Storage and Offloading Market?

SBM OFFSHORE, MODEC, YINSON PRODUCTION, BW OFFSHORE, SEATRIUM, ALTERA INFRASTRUCTURE, BLUEWATER ENERGY SERVICES, BUMI ARMADA, SHAPOORJI PALLONJI ENERGY, MITSUI O.S.K. LINES, MITSUI E&S SHIPBUILDING, SAIPEM, TECHNIP ENERGIES, MITSUBISHI HEAVY INDUSTRIES, SAMSUNG HEAVY INDUSTRIES, COSCO SHIPPING HEAVY INDUSTRY, OTHERS

Which segments covered the Floating Production Storage and Offloading Market?

By Ownership Model (Lease and Operate, Sale and Transfer), By Hull Construction (Converted Hull, Newbuild Hull), By Water Depth (Deepwater, Ultra-deepwater, Shallow-water and Shelf Redeployment), By Application (Crude Oil Production, Gas and Condensate Production, Early Production and Redeployment)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Floating Production Storage and Offloading Market

Published Date : 12 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date