- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Food Traceability Blockchain Market Size, Share | CAGR of 32.9%

Global Food Traceability Blockchain Market Size, Share, Analysis By Offering (Platforms, Software, Services), By Type (Public, Private, Consortium, Hybrid), By Application (Product Traceability, Quality Assurance, Supply Chain, Food Safety, Inventory), By End-User (Manufacturers, Retailers, Logistics, Farmers, Government) Region, Key Players – Dynamics, Farm-to-Fork Digital Supply Chain & AgTech IoT Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

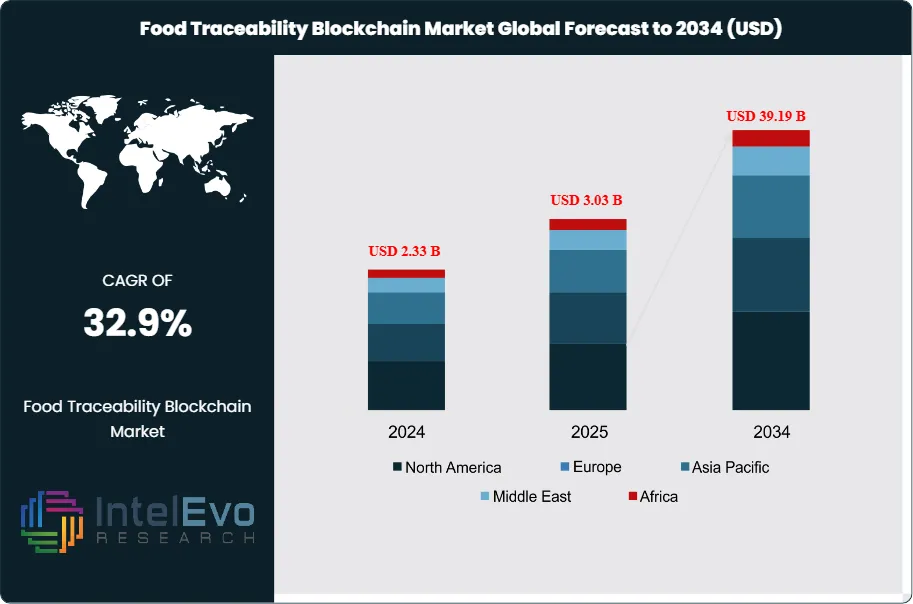

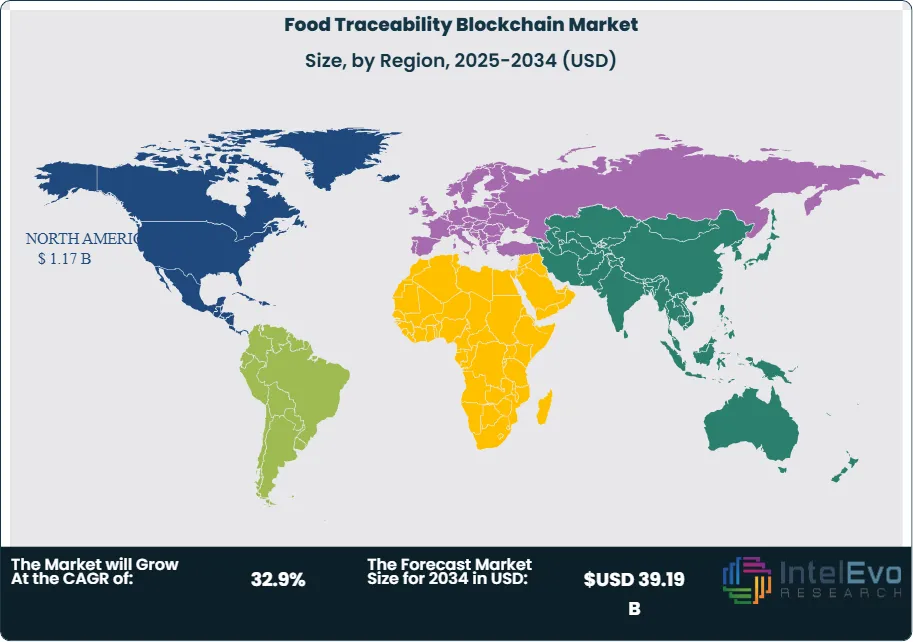

| USD 3.03 Billion | USD 39.19 Billion | 32.9% | North America, 38.5% |

The Food Traceability Blockchain Market was valued at USD 2.33 Billion in 2024 and is estimated to reach USD 3.03 Billion in 2025. The market is projected to grow to USD 39.19 Billion by 2034, expanding at a CAGR of 32.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 36.16 Billion over the analysis period. The forecast reflects a shift from retailer-led pilots toward regulated, standards-based data exchange.

Get More Information about this report -

Request Free Sample ReportDemand in the food traceability blockchain market is driven by three connected forces: FSMA Section 204 recordkeeping in the United States, EU General Food Law traceability duties under Regulation (EC) No 178/2002, and commercial sourcing requirements for seafood, meat, coffee, cocoa, palm oil, and fresh produce. The U.S. Food and Drug Administration moved the Food Traceability Rule compliance date from January 20, 2026 to July 20, 2028, giving suppliers more implementation time while preserving the recordkeeping direction. Large retailers are using the delay to standardize critical tracking events, key data elements, and supplier onboarding workflows.

Technology adoption is moving from proof-of-concept ledgers to hybrid architectures that combine GS1 identifiers, EPCIS 2.0 event data, QR codes, RFID, IoT temperature sensors, satellite verification, and permissioned blockchain records. Walmart's early Hyperledger Fabric deployment with IBM showed the operational logic of the model when mango trace-back time dropped from roughly seven days to 2.2 seconds. Newer procurement requirements focus on data quality, interoperability, audit trails, and standardized trading-partner exchange.

North America led the food traceability blockchain market with 38.5% share in 2025, equivalent to approximately USD 1.17 Billion. Europe held 26.0% share because Article 18 traceability obligations, retailer private-label programs, and deforestation-related sourcing rules create sustained demand for product-origin proof. Asia Pacific represented 24.5% of revenue and is forecast to advance fastest through 2034, supported by seafood export digitization in India, Japanese exporter traceability programs, Chinese retail transparency pilots, and Southeast Asian aquaculture supply-chain modernization.

The food traceability blockchain market outlook through 2034 depends on one practical test: whether vendors can make verified supply-chain data cheaper than recall reconstruction, manual supplier audits, and fragmented spreadsheet compliance. Procurement leads increasingly evaluate blockchain traceability pricing benchmarks through three-year total cost of ownership, supplier adoption rates, and integration with ERP, warehouse management, product lifecycle management, and food-safety systems. Vendors that solve data capture at the farm and vessel level, rather than only selling dashboards, are positioned to capture the highest-margin enterprise contracts.

Market Definition & Scope

The food traceability blockchain market is defined as the global commercial activity surrounding distributed-ledger software, managed services, QR/RFID data capture, standards-based data exchange, and integration tools that record verified food supply-chain events from origin to consumer-facing sale. The market encompasses permissioned blockchain networks, public-chain verification layers, GS1 Digital Link, EPCIS 2.0 event records, smart contracts, IoT-enabled cold-chain logs, supplier identity modules, and consumer provenance applications used by food producers, processors, retailers, distributors, foodservice groups, certification bodies, and regulators.

This analysis includes blockchain-enabled traceability platforms, implementation services, supplier onboarding, audit-ready compliance modules, seafood GDST workflows, carbon and deforestation traceability add-ons when tied to food-origin records, and consumer-facing provenance labels. It excludes generic ERP systems, ordinary barcode software without distributed-ledger validation, laboratory food-safety testing, broad cold-chain logistics platforms without traceability records, and cryptocurrency payment tools. The food traceability blockchain market sits inside the broader food traceability technology category, which industry analysis places above USD 20 Billion in 2025.

, By Type (Public, Private, Consortium, Hybrid), By Application (Product Traceability, Quality Assurance, Supply Chain, Food Safety, Inventory), By End-User (Manufacturers, Retailers, Logistics, Farmers, Government) Region, Key Players – Dynamics, Farm-to-Fork Digital Supply Chain & AgTech IoT Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The food traceability blockchain market expanded from USD 3.03 Billion in 2025 toward a projected USD 39.19 Billion by 2034 at a 32.9% CAGR, creating USD 36.16 Billion in absolute dollar opportunity.

- Segment Dominance: Software and platform subscriptions held approximately 58.0% revenue share in 2025, equal to USD 1.76 Billion, because retailers and processors prioritize interoperable event records over hardware ownership.

- Segment Dominance: Meat, seafood, eggs, and high-risk fresh foods led application demand with 36.5% share in 2025, equal to USD 1.11 Billion, because recall speed and origin proof carry higher risk-adjusted returns in these categories.

- Driver: FSMA Section 204, EU Regulation (EC) No 178/2002, GDST seafood standards, and retailer supplier mandates create a compliance-driven demand base covering thousands of food operators by 2028.

- Restraint: Supplier onboarding remains the largest constraint, with small farms, vessels, and processors often lacking clean lot-level records, mobile connectivity, and GS1 identifier discipline.

- Opportunity: Asia Pacific represents the largest incremental growth opportunity, adding approximately USD 9.35 Billion in forecast revenue through 2034 because export-led seafood, cocoa, coffee, tea, spices, and produce chains face stricter buyer proof requirements.

- Trend: Interoperability is the dominant trend, with GS1 EPCIS 2.0, GDST, QR-based consumer access, and API integrations replacing isolated blockchain pilots.

- Regional: North America led with 38.5% market share and USD 1.17 Billion in 2025, supported by FDA traceability policy, Walmart supplier precedents, and enterprise software budgets.

Key Insights Summary

- FDA's Food Traceability Rule enforcement is aligned to July 20, 2028 after a 30-month extension from the initial January 20, 2026 compliance date, extending the implementation runway for covered foods on the Food Traceability List.

- GS1 EPCIS 2.0 supports event-based supply-chain visibility by structuring what happened, where it happened, when it happened, why it happened, and which objects were involved.

- Walmart's Hyperledger Fabric traceability pilot cut mango origin tracing from about seven days to 2.2 seconds, creating the benchmark used by many enterprise blockchain business cases.

- Wholechain's seafood traceability platform is verified capable against GDST V1.2 and performs automated capability testing, positioning interoperability as a daily operating control rather than a one-time certificate.

- Trustwell's FoodLogiQ platform passed the GDST Capability Test in August 2025, widening standardized seafood traceability options beyond blockchain-native vendors.

- India released a national digital fisheries and aquaculture traceability framework in November 2025 to support seafood exports targeted at INR 1 lakh crore by 2030.

- IBM reported USD 67.5 Billion in 2025 revenue, while Oracle reported USD 57.4 Billion in fiscal 2025 revenue, giving large enterprise vendors the balance-sheet scale to integrate traceability with cloud, ERP, and supply-chain suites.

Competitive Landscape Overview

The food traceability blockchain market is fragmented by vendor count but concentrated by enterprise credibility. IBM Food Trust, Wholechain, TE-FOOD, and TraceX Technologies account for an estimated 34% of commercially visible blockchain-enabled deployments in 2025, while Trustwell FoodLogiQ, SAP, Oracle, Kezzler, and VeChain compete through adjacent supply-chain, compliance, and product-identity systems. Competition is platform-based rather than price-only because buyers need standards mapping, supplier onboarding, offline data capture, and audit evidence that survives retailer or regulator review.

Competitive pressure is shifting toward interoperability. IBM's withdrawal of select Blockchain Transparent Supply cloud services in 2025 reduced confidence in single-vendor ledgers, while Wholechain's GDST activity, Trustwell's TPG-backed expansion, and Kezzler's acquisition of Scanbuy show investment moving toward data exchange, QR engagement, and compliance workflows. The most defensible vendors combine blockchain integrity with GS1 identifiers, ERP connectors, mobile field tools, and multi-tier supplier management.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| International Business Machines Corporation | United States | Leader | IBM Food Trust, IBM Blockchain Platform | North America, Europe, global retailers | 2025 service withdrawal notice shifted buyer focus toward continuity planning for IBM-linked blockchain supply-chain deployments |

| Wholechain, Inc. | United States | Leader | Wholechain traceability platform, GDST workflows | Seafood, agriculture, North America, global export chains | Thai Union selected Wholechain in April 2026 for standardized seafood traceability across global operations |

| TE-FOOD International GmbH | Hungary | Leader | TE-FOOD blockchain traceability system | Europe, Asia, export-oriented food chains | Continued to serve QR-enabled consumer provenance and import-compliance workflows in 2025 |

| TraceX Technologies Private Limited | India | Challenger | TraceX blockchain-enabled supply-chain platform | India, Africa, agricultural export chains | Expanded Ghana-focused food and agriculture traceability use cases in late 2025 and early 2026 |

| VeChain Foundation | Singapore / San Marino | Challenger | VeChainThor supply-chain verification | China, Asia Pacific, consumer goods | Historic Walmart China deployments remain a reference case for fresh-food provenance programs |

| Trustwell LLC | United States | Challenger | FoodLogiQ Traceability | United States, seafood, restaurant and retail channels | Received TPG Rise Funds strategic investment in January 2026 |

| Kezzler AS | Norway | Challenger | Kezzler traceability and product identity platform | Europe, North America, global brands | Partnered with CTG in May 2025 to support enterprise traceability deployments |

| Oracle Corporation | United States | Challenger | Oracle Intelligent Track and Trace, supply-chain cloud | Global enterprise installed base | Reported fiscal 2025 revenue of USD 57.4 Billion, supporting continued supply-chain cloud investment |

| SAP SE | Germany | Challenger | SAP supply-chain, product compliance, traceability integrations | Europe, global manufacturers | Published 2025 integrated reporting showing continued cloud and software momentum |

| Trace Register LLC | United States | Niche Player | Seafood traceability and compliance systems | Seafood supply chains | Demonstrated interoperability with Wholechain based on GDST compatibility standards |

Segmentation Analysis

The food traceability blockchain market segments by offering, blockchain type, application, and end-user, with each segment shaped by compliance deadlines, commodity risk, and the cost of supplier data capture.

By Offering

The food traceability blockchain market by offering is led by software and platform subscriptions, which held 58.0% share and USD 1.76 Billion in 2025. IBM Food Trust, Wholechain, TE-FOOD, TraceX Technologies, Trustwell FoodLogiQ, and Kezzler sell dashboards, event-record systems, compliance modules, supplier portals, and API access that can sit above ERP and warehouse platforms. Subscription economics are strongest where retailers require supplier participation, because one enterprise buyer can force hundreds of upstream nodes into a shared data model. Software also benefits from FSMA 204 and GDST because the buyer's core problem is not scanning alone; it is the creation, storage, and exchange of critical tracking events.

Implementation services, data migration, training, and supplier onboarding represented 24.0% of revenue in 2025, equal to USD 0.73 Billion. This services share is high because farms, vessels, packhouses, brokers, and processors often hold incomplete lot records. Hardware and data-capture devices accounted for 18.0% share, or USD 0.55 Billion, spanning QR labels, RFID tags, scanners, temperature sensors, and mobile devices. Hardware grows slower than software because GS1 Digital Link and smartphone-based scanning reduce proprietary device dependence.

By Blockchain Type

Permissioned blockchain networks dominated the food traceability blockchain market with 64.0% revenue share and USD 1.94 Billion in 2025. IBM Food Trust, Wholechain, and enterprise deployments based on Hyperledger Fabric use permissioned models because retailers, processors, and logistics providers need access controls for prices, supplier identities, volumes, and audit records. Permissioned ledgers also fit food-safety investigations because regulators can receive a controlled data package without exposing all commercial relationships. The procurement checklist for enterprise buyers now tests identity governance, role-based access, API security, and data-retention rules before ledger performance.

Public or hybrid blockchain architectures captured 21.5% share in 2025, equal to USD 0.65 Billion, with VeChain, TE-FOOD, and QR-based consumer provenance projects representing the most visible deployments. Hybrid models are useful when consumer-facing trust, anti-counterfeit verification, and sustainability claims require a public proof layer while private supply-chain details remain restricted. Off-chain data layers and interoperability middleware held 14.5% share, or USD 0.44 Billion. This third category is growing because GS1 EPCIS 2.0, GDST, ERP connectors, and certification data exchanges matter more than raw block creation speed.

By Application

Meat, seafood, eggs, and high-risk fresh foods led the food traceability blockchain market with 36.5% share and USD 1.11 Billion in 2025. These categories carry high recall exposure, animal-origin fraud risk, and strict buyer demands for vessel, farm, harvest, processing, and cold-chain records. Wholechain's seafood work with GDST, Mars's June 2025 seafood traceability initiative, and Thai Union's April 2026 partnership with Wholechain illustrate why seafood has become a reference category for standardized data exchange. Meat and poultry programs rely on lot, slaughter, processing, and distribution records that need stronger interoperability than paper certificates can provide.

Fresh produce represented 24.0% of market revenue in 2025, or USD 0.73 Billion, because leafy greens, tomatoes, melons, cucumbers, peppers, and herbs are central to FSMA 204 planning. Coffee, cocoa, tea, spices, and specialty ingredients accounted for 19.5% share, equal to USD 0.59 Billion, driven by origin claims, export audits, and sustainability rules. Packaged foods, dairy, beverages, and pet food represented the remaining 20.0% share. Pet food demand is rising after Mars committed to GDST-aligned seafood traceability for its pet nutrition supply chains in 2025.

By End-User

Food retailers and foodservice groups accounted for 31.0% of food traceability blockchain market revenue in 2025, equal to USD 0.94 Billion. Walmart, Carrefour, Costco-style club retailers, restaurant chains, and grocery distributors use supplier mandates to create network effects that standalone producers cannot generate. Food manufacturers and processors held 29.0% share, or USD 0.88 Billion, because FSMA 204, private-label requirements, allergen control, and recall-readiness need traceability records across ingredients and finished goods. The return on investment improves when traceability data also supports shelf-life, waste, and supplier-scorecard workflows.

Primary producers, cooperatives, fisheries, and aquaculture operators captured 18.0% of 2025 revenue, equal to USD 0.55 Billion, with growth tied to export access and certification. Logistics providers and cold-chain operators represented 12.5% share because temperature excursions, handoffs, and warehouse events are critical in blockchain audit trails. Regulators, certification bodies, and NGOs accounted for 9.5% share, using traceability data to validate claims related to food safety, deforestation, labor, and sustainability.

Regional Analysis

North America led the food traceability blockchain market with 38.5% share and USD 1.17 Billion in 2025. The United States represented approximately USD 0.98 Billion of regional demand, with Canada at USD 0.13 Billion and Mexico at USD 0.06 Billion. FDA FSMA Section 204 remains the core regulatory catalyst even after the compliance date moved to July 20, 2028, because large retailers and foodservice buyers are not waiting for enforcement to standardize supplier data. IBM, Trustwell, Wholechain, Oracle, SAP North America, and retailer-led programs define the regional vendor mix. The non-obvious buyer signal is that the deadline delay may increase software revenue by allowing phased enterprise rollouts instead of narrow emergency compliance purchases.

Europe accounted for 26.0% of the food traceability blockchain market in 2025, equivalent to USD 0.79 Billion. Germany, France, the United Kingdom, the Netherlands, Italy, and Spain lead demand because EU Regulation (EC) No 178/2002 requires traceability across production, processing, and distribution. Retailer private-label rules, seafood import requirements, and deforestation-related sourcing programs raise demand for origin records across cocoa, coffee, beef, palm oil, and specialty ingredients. TE-FOOD in Hungary, Kezzler in Norway, SAP in Germany, and food retailers across France and Spain strengthen Europe's vendor and buyer base.

Asia Pacific held 24.5% share and USD 0.74 Billion in 2025, and it is forecast to outpace other regions through 2034. China, India, Japan, Australia, Thailand, Indonesia, and Vietnam are the main national markets because seafood, tea, rice, spices, aquaculture, and processed food exports need trusted origin and movement data. India released a national digital traceability framework for fisheries and aquaculture in November 2025, targeting stronger seafood export access by 2030. Japanese exporters and retailers are also adopting blockchain-backed traceability to support food safety and trade credibility.

Latin America represented 6.8% of the food traceability blockchain market in 2025, equal to USD 0.21 Billion. Brazil, Mexico, Chile, Colombia, Peru, and Argentina anchor regional demand because beef, coffee, cocoa, fruit, seafood, and soy buyers need stronger proof of origin. Wholechain's cattle data-framework work in Brazil and TraceX's sustainability-oriented agricultural traceability use cases show how blockchain can combine food provenance with deforestation and carbon data. The largest constraint is field-level data quality across fragmented farms.

Middle East and Africa accounted for 4.2% share and USD 0.13 Billion in 2025. The Gulf markets use traceability to support food import security, while Ghana, Kenya, South Africa, Morocco, and Egypt apply digital records to cocoa, sesame, coffee, horticulture, and seafood exports. TraceX's Ghana-focused supply-chain content and Univision partnership signal rising African demand for export-grade proof systems. Adoption remains services-heavy because mobile onboarding, multilingual records, and cooperative-level training are needed before blockchain records become reliable.

Country Analysis

The United States food traceability blockchain market reached approximately USD 0.98 Billion in 2025 and is projected to grow at a country-specific CAGR of 31.8% through 2034. FSMA Section 204, FDA Food Traceability List coverage, retailer supplier mandates, and recall-cost control anchor demand. Walmart's early blockchain benchmark remains influential because it showed that farm-to-store visibility can move from days to seconds when suppliers use shared event records. Trustwell, Wholechain, IBM, Oracle, SAP, and Kezzler compete for enterprise budgets tied to ERP, food safety, supplier management, and audit evidence.

China's food traceability blockchain market reached approximately USD 0.31 Billion in 2025, with a projected CAGR of 35.5% through 2034. Retail food-safety programs, fresh meat provenance, e-commerce grocery channels, and cross-border trade support adoption. VeChain's Walmart China program remains a reference case for fresh-food provenance. Domestic demand is shaped by consumer confidence after prior food-safety incidents, while exporters need traceability records accepted by overseas retailers and regulators.

Germany's food traceability blockchain market reached approximately USD 0.20 Billion in 2025, with a projected CAGR of 30.4% through 2034. EU General Food Law traceability rules, SAP's enterprise software footprint, retailer private-label systems, and meat processing compliance support demand. German food manufacturers typically prefer interoperable systems that map to ERP, GS1 identifiers, and audit documentation rather than standalone public-chain proofs. Procurement teams compare vendors by EPCIS support, onboarding cost, and EU-facing data retention rules.

India's food traceability blockchain market reached approximately USD 0.17 Billion in 2025 and is projected to grow at a 38.0% CAGR through 2034. Seafood, spices, tea, coffee, basmati rice, fruits, and dairy exports create strong demand for low-cost mobile traceability. The November 2025 national digital traceability framework for fisheries and aquaculture supports India's goal of scaling seafood exports to INR 1 lakh crore by 2030. TraceX Technologies, GS1 India DataKart Trace, government-backed agriculture programs, and exporter consortia define the local adoption path.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Offering

- Platform

- Software

- Services

By Blockchain Type

- Public Blockchain

- Private Blockchain

- Consortium Blockchain

- Hybrid Blockchain

By Application

- Product Traceability

- Quality Assurance

- Supply Chain Management

- Food Safety & Compliance

- Inventory Management

- Others

By End-User

- Food Manufacturers

- Food Retailers

- Distributors & Logistics Providers

- Farmers & Producers

- Government & Regulatory Authorities

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.03 B |

| Forecast Revenue (2034) | USD 39.19 B |

| CAGR (2025-2034) | 32.9% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platform, Software, Services), By Blockchain Type, (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Blockchain), By Application, (Product Traceability, Quality Assurance, Supply Chain Management, Food Safety & Compliance, Inventory Management, Others), By End-User, (Food Manufacturers, Food Retailers, Distributors & Logistics Providers, Farmers & Producers, Government & Regulatory Authorities, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | INTERNATIONAL BUSINESS MACHINES CORPORATION, WHOLECHAIN, INC., TE-FOOD INTERNATIONAL GMBH, TRACEX TECHNOLOGIES PRIVATE LIMITED, VECHAIN FOUNDATION, TRUSTWELL LLC, KEZZLER AS, ORACLE CORPORATION, SAP SE, TRACE REGISTER LLC, KOLTIVA AG, FOODCHAIN ID GROUP, INC., ANTCHAIN, RIPE.IO, PROVENANCE LTD., SEAFOOD SOUQ, GS1 INDIA DATACART TRACE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Public, Private, Consortium, Hybrid), By Application (Product Traceability, Quality Assurance, Supply Chain, Food Safety, Inventory), By End-User (Manufacturers, Retailers, Logistics, Farmers, Government) Region, Key Players – Dynamics, Farm-to-Fork Digital Supply Chain & AgTech IoT Trends & Forecast 2026-2034")

, By Type (Public, Private, Consortium, Hybrid), By Application (Product Traceability, Quality Assurance, Supply Chain, Food Safety, Inventory), By End-User (Manufacturers, Retailers, Logistics, Farmers, Government) Region, Key Players – Dynamics, Farm-to-Fork Digital Supply Chain & AgTech IoT Trends & Forecast 2026-2034")

, By Type (Public, Private, Consortium, Hybrid), By Application (Product Traceability, Quality Assurance, Supply Chain, Food Safety, Inventory), By End-User (Manufacturers, Retailers, Logistics, Farmers, Government) Region, Key Players – Dynamics, Farm-to-Fork Digital Supply Chain & AgTech IoT Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Food Traceability Blockchain Market?

Global Food Traceability Blockchain Market was valued at USD 3.03 Billion in 2025 and is projected to reach USD 39.19 Billion by 2034, growing at a CAGR of 32.9% during 2026–2034. Explore market trends, drivers, opportunities, segmentation, blockchain adoption, and industry insights.

Who are the major players in the Food Traceability Blockchain Market?

INTERNATIONAL BUSINESS MACHINES CORPORATION, WHOLECHAIN, INC., TE-FOOD INTERNATIONAL GMBH, TRACEX TECHNOLOGIES PRIVATE LIMITED, VECHAIN FOUNDATION, TRUSTWELL LLC, KEZZLER AS, ORACLE CORPORATION, SAP SE, TRACE REGISTER LLC, KOLTIVA AG, FOODCHAIN ID GROUP, INC., ANTCHAIN, RIPE.IO, PROVENANCE LTD., SEAFOOD SOUQ, GS1 INDIA DATACART TRACE, OTHERS

Which segments covered the Food Traceability Blockchain Market?

By Offering, (Platform, Software, Services), By Blockchain Type, (Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Blockchain), By Application, (Product Traceability, Quality Assurance, Supply Chain Management, Food Safety & Compliance, Inventory Management, Others), By End-User, (Food Manufacturers, Food Retailers, Distributors & Logistics Providers, Farmers & Producers, Government & Regulatory Authorities, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Food Traceability Blockchain Market

Published Date : 15 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date