- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Food Waste Management Technology Market Size, Share | CAGR of 7.5%

Global Food Waste Management Technology Market Size, Share, Growth By Technology (Anaerobic Digestion, Composting, Waste-to-Energy, Recycling, Smart Monitoring), By End-User (Food Processing, Retail, Hospitality, Municipalities, Households), By Application (Collection, Treatment, Energy Recovery, Fertilizer, Animal Feed) Region, Key Players – Dynamics, Circular Bioeconomy & Sustainable Waste Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 26.4 Billion | USD 50.6 Billion | 7.5% | North America, 36.8% |

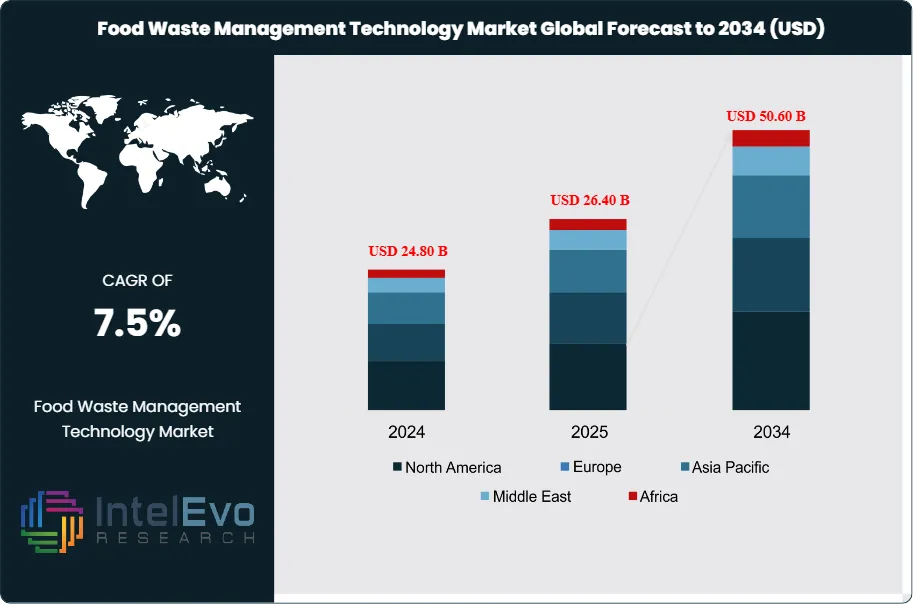

The Food Waste Management Technology Market was valued at USD 24.80 Billion in 2024 and is estimated to reach USD 26.40 Billion in 2025. The market is projected to reach USD 50.60 Billion by 2034, expanding at a CAGR of 7.5% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 24.2 Billion over the analysis period, expanding 1.92 times across nine years.

Get More Information about this report -

Request Free Sample ReportDemand for food waste management technology is anchored in three reinforcing forces: regulatory pressure forcing organics out of landfills, corporate net-zero commitments tied to Scope 3 emissions, and unit economics that now make anaerobic digestion and aerobic processing profitable on a five-year payback. The United States Environmental Protection Agency reports more than 40 million tonnes of food waste generated annually, while UNEP Food Waste Index Report 2024 data shows global food waste reached 1.05 billion tonnes in 2022.

Regulatory frameworks have moved from voluntary to binding. The revised EU Waste Framework Directive entered into force on October 16, 2025, mandating a 10% reduction in food waste from processing and manufacturing and a 30% reduction per capita at retail and consumption levels by 2030. California Senate Bill 1383 requires 75% diversion of organic waste from landfills, while United Kingdom Simpler Recycling rules came into force on March 31, 2026, requiring weekly household food waste collections across England.

Anaerobic digestion technology dominates technology spend, with American Biogas Council data from February 2026 confirming 70 new biogas projects came online in 2025, representing more than USD 2 Billion in fresh recycling infrastructure. AI-enabled food waste tracking platforms from Winnow Solutions, Leanpath, and Metafoodx are reducing kitchen waste by 25% to 70% in commercial deployments, while sensor-equipped bins from Mill Industries Inc. cut waste volumes by 80% through dehydration.

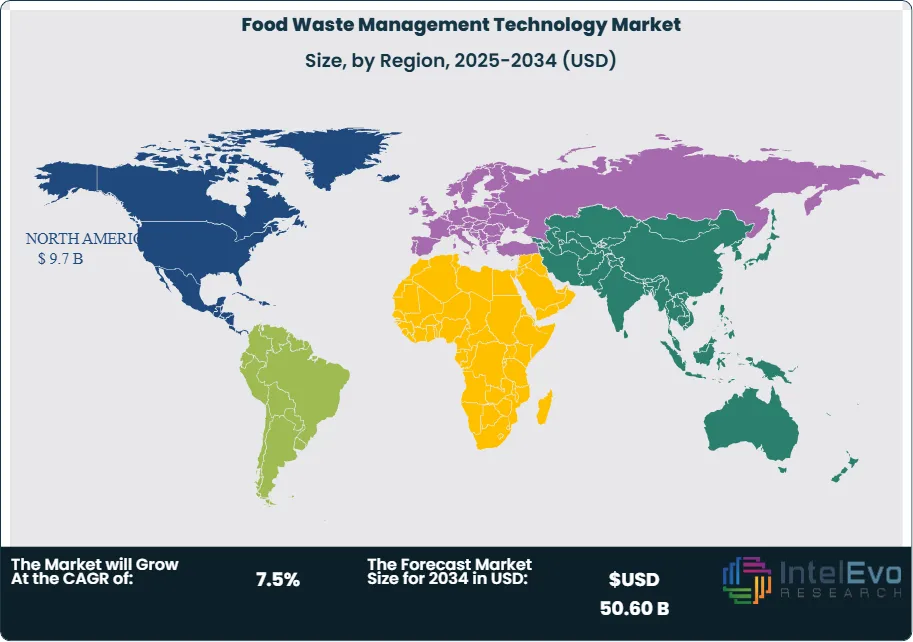

North America held the leading regional position at 36.8% market share in 2025, supported by Inflation Reduction Act methane provisions and aggressive state-level mandates. Asia Pacific is expected to record the fastest growth, propelled by India's 2026 Food Loss Reduction Roadmap and China scaling wet-market separation pilots in 36 mega-cities. Through 2034, the food waste management technology market will reward operators that integrate hardware, software, and feedstock contracts into closed-loop systems delivering renewable natural gas, soil amendments, and animal feed.

Market Definition & Scope

The food waste management technology market is defined as the technology-enabled segment of the broader food waste management industry, encompassing equipment, software, and integrated systems used to prevent, capture, process, and valorize food waste across the supply chain. The market includes anaerobic digestion systems, in-vessel and aerobic composting equipment, dehydration and pulping units, depackaging machinery, AI-enabled food waste tracking platforms, smart bins with computer vision, and surplus food marketplace platforms.

Included in this analysis are commercial and industrial digesters, modular on-site processing units, retail-aisle scanning hardware, kitchen analytics software, AD-derived renewable natural gas systems, and food rescue platforms operating at scale. Excluded are general municipal solid waste collection vehicles unrelated to organics, generic landfill operations, agricultural pest-control technology, and consumer-level kitchen appliances such as conventional garbage disposers without connected analytics. The food waste management technology market is a subset of the broader USD 81 Billion food waste management market and represents approximately 32% of the parent category by 2025 revenue.

, By End-User (Food Processing, Retail, Hospitality, Municipalities, Households), By Application (Collection, Treatment, Energy Recovery, Fertilizer, Animal Feed) Region, Key Players – Dynamics, Circular Bioeconomy & Sustainable Waste Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global food waste management technology market grew from USD 26.4 Billion in 2025 toward a forecast value of USD 50.6 Billion by 2034, advancing at a CAGR of 7.5%.

- Segment Dominance: Anaerobic digestion technology held 41.6% of technology revenue in 2025, supported by USD 2 Billion in new US biogas project investment confirmed by the American Biogas Council in February 2026.

- Segment Dominance: The commercial end-use segment captured 45.8% of market revenue in 2025, driven by hospitality, foodservice, and retail compliance with state and EU diversion mandates.

- Driver: Binding regulatory targets are accelerating adoption; the revised EU Waste Framework Directive requires 30% per capita reduction in retail and consumer food waste by 2030 against the 2021-2023 baseline.

- Restraint: Capital costs remain high; a 100-tonne-per-day anaerobic digestion plant requires upfront investment exceeding USD 10 Million, limiting deployment among small and medium operators.

- Opportunity: The American Biogas Council estimates more than 17,000 additional biogas systems could be built across the United States, representing a multi-billion-dollar buildout window through 2035.

- Trend: AI-enabled waste tracking platforms now deliver 25% to 70% waste reduction in hotel kitchens, with paybacks under 24 months for high-volume operators per peer-reviewed ScienceDirect research published in March 2025.

- Regional: North America led the global market with 36.8% share in 2025, equating to USD 9.7 Billion in technology revenue, on the back of Inflation Reduction Act incentives and California SB 1383 enforcement.

Key Insights Summary

- Per the UNEP Food Waste Index Report 2024, the world wasted 1.05 billion tonnes of food in 2022, equating to 19% of food available to consumers; households accounted for 631 million tonnes, foodservice for 290 million tonnes, and retail for 131 million tonnes.

- Industry data published by the American Biogas Council on February 24, 2026 confirmed 70 new biogas projects came online in 2025, representing capital expenditure above USD 2 Billion and bringing the US system count to nearly 2,600 facilities producing 780.7 billion cubic feet of biogas capacity per year.

- United States Environmental Protection Agency data shows the country generates more than 40 million tonnes of food waste annually, with anaerobic digestion facilities reporting median tipping fees of USD 24.26 per tonne in 2021.

- California's Senate Bill 1383 targets 75% diversion of organic waste from landfills against 2014 levels, equivalent to redirecting roughly 20 million tonnes from disposal by the 2025 milestone, per CalRecycle implementation guidance.

- Per the European Commission, the revised Waste Framework Directive that entered into force in October 2025 mandates a 10% reduction in processing and manufacturing food waste plus a 30% per capita reduction at retail and consumption levels by 2030.

- Food and Agriculture Organization figures put the value of post-harvest food losses globally at approximately USD 400 Billion per year, with food loss and waste contributing 8% to 10% of global greenhouse gas emissions.

- Surplus-food marketplace operator Too Good To Go disclosed in August 2025 that its US user base reached 15 million, with 17,000 partner businesses contributing to over 8.1 million meals saved during the first seven months of 2025, a 67% year-over-year jump.

Competitive Landscape Overview

The food waste management technology market is moderately consolidated. The combined revenue share of the top four players, comprising Veolia Environnement SA, Waste Management Inc., Republic Services Inc., and Divert Inc., reached an estimated 27.4% in 2025, with the next ten companies adding a further 22%. Competition is technology-led at the upstream end, with AD process licensors and AI vendors competing on yield, uptime, and integration depth, while downstream collection and processing competition remains regional and contract-driven.

Competitive positioning is shifting in three measurable ways. Integrated infrastructure players are buying organics specialists; Circular Services completed back-to-back acquisitions of Quantum Organics in February 2025 and Atlas Organics in November 2025. Technology specialists are partnering with retailers to lock in feedstock; the December 2025 Mill Industries and Amazon arrangement secures Whole Foods Market produce scraps from 2027. Private equity is funding AD operators at USD 1 Billion-plus valuations, exemplified by Divert's January 2026 capital round led by Wittington Investments Limited.

Competitive Landscape Matrix:

| Company | HQ | Position | Key Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Veolia Environnement SA | France | Leader | Anaerobic digestion systems, BioSV depackaging, biogas upgrading | Europe, North America, Asia Pacific | Closed Clean Earth purchase for USD 3.04 Billion in November 2025 |

| Waste Management, Inc. | United States | Leader | Organics collection, AD plants, in-vessel composting | North America (US, Canada) | Brought Stericycle into the fold in late 2024 for USD 7.2 Billion |

| Republic Services, Inc. | United States | Leader | Organics processing, RNG production, source-separated collection | North America | Joined forces with Opal Fuels on landfill RNG plant in North Carolina |

| Divert, Inc. | United States | Leader | Integrated Diversion and Energy Facilities, AD-derived RNG | United States, Canada | Opened Longview, Washington 100,000-tonne AD facility on April 29, 2026 |

| Anaergia Inc. | Canada | Challenger | Proprietary AD process, biogas upgrading (BUG) systems | North America, EMEA | Inked C$8 Million equipment supply deal with Vanguard Renewables in April 2026 |

| Vanguard Renewables | United States | Challenger | Farm Powered AD network, RNG offtake | United States Midwest, Northeast, Southeast | Backed by BlackRock-affiliated Global Infrastructure Partners; pipeline above 30 markets |

| Mill Industries Inc. | United States | Niche Player | Sensor-laden food recycling bins, dehydration platform | United States, Canada | Picked up Amazon Climate Pledge Fund equity in December 2025; Whole Foods deployment from 2027 |

| Too Good To Go | Denmark | Niche Player | Surplus food marketplace mobile platform | Europe, North America, Australia, Japan | Crossed 17,000 US partners and 15 million users by August 2025 |

| Winnow Solutions Ltd | United Kingdom | Niche Player | AI computer-vision food waste tracking | Europe, Middle East, Asia Pacific | Mandarin Oriental rolled out Throw and Go across all hotels by end of 2025 |

| Apeel Sciences | United States | Niche Player | Plant-based shelf-life extension coatings | Europe, North America | Operates with 40 retail partners across eight countries |

Segmentation Analysis

The food waste management technology market segments across three primary axes: by technology type, by end-use, and by application.

By Technology Type

Anaerobic digestion held 41.6% revenue share in 2025, equivalent to USD 11.0 Billion, supported by data from Global Market Insights confirming AD systems accounted for 51.5% of food waste recycling capacity in 2024. Anaerobic digestion converts food waste into biogas and digestate, with US tipping fee economics averaging USD 30.74 per tonne per EPA 2021 data and capital expenditure ranging from USD 10 Million for a 100-tonne-per-day facility to USD 100 Million for a 75,000-tonne-per-year integrated plant such as Dem-Con's Louisville Township project. Major operators in this sub-segment include Anaergia Inc., Vanguard Renewables, and Divert Inc.

Aerobic composting technology held 28.4% share in 2025, supported by lower capital intensity and 70% to 80% mass reduction yields documented by the Institute for Sustainable Futures at the University of Technology Sydney in a 2024 study. In-vessel composting and modular containerized units have proliferated in dense urban deployments; Tokyo alone has installed more than 1,200 on-site aerobic digesters in commercial kitchens since 2020. Compared with anaerobic digestion, aerobic systems achieve breakeven in 24 to 72 hours of processing time and avoid the gas-capture infrastructure cost burden.

In-vessel and mechanical biological treatment captured 14.2% of 2025 revenue, with depackaging equipment from Smicon, Anaergia, and Atlas Copco enabling output purity above 99.5% to comply with the May 2025 amendments to Germany's Bioabfallverordnung. Digital tracking and software took 8.7% share, led by Winnow Solutions, Leanpath, Metafoodx, and Phood, with Metafoodx securing USD 9.4 Million in May 2025 for AI-driven scanner deployments. Other technology categories, including thermal conversion and dehydration platforms such as Mill Industries' commercial unit, accounted for the remaining 7.1%.

By End-User

Commercial end-users took 45.8% revenue share in 2025, encompassing restaurants, hotels, supermarkets, foodservice contractors, and quick-service chains. The hospitality vertical has been the most rapid technology adopter; Winnow's Throw and Go AI platform reaches all Mandarin Oriental hotels by end-2025, while Sodexo's WasteWatch program, anchored on Leanpath hardware, runs across global foodservice contracts. Compass Group North America disclosed an 11% year-on-year reduction in food waste during 2025 across its kitchen network, validating commercial ROI.

Industrial end-users represented 28.4% of 2025 revenue, dominated by food and beverage processors using on-site AD or wastewater anaerobic treatment systems. Veolia Water Technologies' Biothane Biobed EGSB and AnoxKaldnes MBBR installations operate at confectionery and dairy plants across Europe and North America. Municipal and household end-users accounted for 22.7% of revenue, growing fastest in regions with new collection mandates. Institutional accounts including hospitals, universities, and military canteens contributed the remaining 3.1%; Arizona State University reported a 39% waste reduction using Leanpath hardware in 2024.

By Application

Energy recovery applications, principally biogas and renewable natural gas, captured 39.2% of 2025 revenue, equivalent to USD 10.4 Billion. RNG production rose 24% year-on-year in 2025 to 225.6 million MMBtu per American Biogas Council data, with 68 of the 70 new biogas projects in 2025 designed for RNG upgrade. Soil amendment and compost applications followed with 28.7% share, supported by California's mandatory procurement of 0.08 tonnes of organic recovery products per resident per year under SB 1383.

Animal feed applications represented 13.5% of revenue, including Mill Industries' chicken-feed conversion model and rendering technologies operated by Darling Ingredients. Food rescue and redistribution platforms held 11.4% share, encompassing Too Good To Go's surplus marketplace, Olio's neighbor-sharing app, and Phenix's retailer-to-charity logistics network. Bio-products including bioplastics, lactic acid, and specialty chemicals took 7.2%, supported by upcyclers such as TripleW, Bio-bean Ltd., and SCO2.

Regional Analysis

North America led the global food waste management technology market with 36.8% revenue share in 2025, equivalent to USD 9.7 Billion. The United States dominates regional spend, with California, Vermont, Massachusetts, Washington, Oregon, and New York operating active organic waste diversion mandates. Canada contributes through Ontario's organics regulations and Vanguard Renewables' Midwest network expansion. The Inflation Reduction Act's methane fee provisions and renewable identification number values for AD-derived RNG underpin the regional investment thesis. As of February 2026, the US biogas industry totaled nearly 2,600 facilities, with 124 dedicated food-waste-only systems.

Europe held 31.4% revenue share in 2025, equivalent to USD 8.3 Billion, anchored by Germany, France, the Netherlands, Italy, and the United Kingdom. The revised Waste Framework Directive entered into force on October 16, 2025, while the EU Packaging and Packaging Waste Regulation 2025/40 takes direct effect from August 12, 2026. UK Simpler Recycling rules became operational on March 31, 2026, with Veolia rolling out collection services to over 16 million residents. Lincolnshire began weekly household food waste collections in early 2026. Germany's BioAbfV amendments took effect in May 2025, tightening plastic contamination thresholds to 0.5% post-depackaging.

Asia Pacific captured 23.7% revenue share in 2025, valued at USD 6.3 Billion, and is forecast to grow fastest at a 9.1% CAGR through 2034. China is scaling wet-market separation pilots in 36 mega-cities, while India is preparing its 2026 Food Loss Reduction Roadmap. Japan's Ministry of the Environment data shows over 1,200 on-site aerobic digesters installed in Tokyo commercial kitchens, and Mitsubishi Heavy Industries upgraded urban food-waste-to-energy systems for higher biogas yields in February 2026. Australia's organic waste mandates are driving Veolia's 50,000-tonne Melbourne AD facility commissioned in April 2025.

Latin America held 4.6% revenue share in 2025, valued at USD 1.2 Billion, with Brazil and Mexico leading deployment. SUEZ's January 2024 Chengdu partnership model is being adapted for Sao Paulo and Mexico City. Middle East and Africa accounted for 3.5% revenue share, equivalent to USD 924 Million, with the United Arab Emirates and Saudi Arabia driving regional demand under their respective national circular-economy visions. Remondis opened a 40,000-tonne composting plant in Jakarta, Indonesia in June 2025 under a 10-year government supply contract, marking expanded private-sector activity in emerging markets. African deployments remain pilot-scale, often supported by NGOs and development agencies.

Country Analysis

United States: The US food waste management technology market reached USD 9.4 Billion in 2025 and is forecast to expand at a 7.8% CAGR through 2034. EPA data confirms more than 40 million tonnes of food waste are generated annually, with the Resource Conservation and Recovery Act providing the federal regulatory backbone. State mandates including California SB 1383, Vermont Universal Recycling Law, and Washington's Organics Management Law are forcing food-service compliance. The US Department of Agriculture and EPA jointly target a 50% reduction in food waste by 2030 against 2010 baselines.

Germany: The German market reached USD 1.8 Billion in 2025 and is projected to grow at 6.4% CAGR through 2034. The May 2025 amendments to Bioabfallverordnung and Gewerbeabfallverordnung mandate depackaging before treatment and impose plastic contamination thresholds of 0.5%. Domestic operators including Remondis, Bauer Group, and Smicon dominate equipment supply. Germany's Green Dot system, combined with biogas plant density above 9,000 facilities, makes the country Europe's deepest end-market for digestion equipment.

United Kingdom: The UK market reached USD 2.1 Billion in 2025, growing at 7.2% CAGR through 2034 per industry analysis. The Simpler Recycling rules effective March 31, 2026 require weekly household food waste collections across England, with Defra committing GBP 340 Million to support local authorities. Biffa, Veolia UK, and FCC Environment Ltd lead collection and AD operations. Winnow Solutions, headquartered in London, leads the global AI food waste tracking category by deployment count.

China: The Chinese market reached USD 2.4 Billion in 2025 and is forecast to grow at 9.6% CAGR through 2034, the fastest among major economies. Wet-market separation pilots are operational across 36 mega-cities. Domestic AD specialists such as Shanghai-based Enwise are deploying AI-monitored dry digestion systems with PepsiCo, Oatly, and Intel as feedstock partners. Veolia's Laogang landfill biogas operation in Shanghai recovers 60 million cubic metres of biogas annually, generating 100,000 MWh of green energy.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Technology Type

- Anaerobic Digestion

- Composting

- Waste-to-Energy (Incineration)

- Food Waste Recycling

- Smart Waste Monitoring & Analytics

By End-User

- Food Processing Companies

- Retail & Supermarkets

- Hospitality & Foodservice

- Municipalities

- Households

- Others

By Application

- Food Waste Collection

- Waste Treatment & Disposal

- Energy Recovery

- Organic Fertilizer Production

- Animal Feed Production

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 26.40 B |

| Forecast Revenue (2034) | USD 50.60 B |

| CAGR (2025-2034) | 7.5% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology Type, (Anaerobic Digestion, Composting, Waste-to-Energy (Incineration), Food Waste Recycling, Smart Waste Monitoring & Analytics), By End-User, (Food Processing Companies, Retail & Supermarkets, Hospitality & Foodservice, Municipalities, Households, Others), By Application, (Food Waste Collection, Waste Treatment & Disposal, Energy Recovery, Organic Fertilizer Production, Animal Feed Production, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEOLIA ENVIRONNEMENT SA, WASTE MANAGEMENT, INC., REPUBLIC SERVICES, INC., DIVERT, INC., ANAERGIA INC., VANGUARD RENEWABLES, MILL INDUSTRIES INC., TOO GOOD TO GO, WINNOW SOLUTIONS LTD, LEANPATH, APEEL SCIENCES, GFL ENVIRONMENTAL INC., BIFFA PLC, FCC ENVIRONMENT LTD, REWORLD (FORMERLY COVANTA), REMONDIS SE & CO. KG, STERICYCLE, INC., DARLING INGREDIENTS INC., RECOLOGY INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Food Processing, Retail, Hospitality, Municipalities, Households), By Application (Collection, Treatment, Energy Recovery, Fertilizer, Animal Feed) Region, Key Players – Dynamics, Circular Bioeconomy & Sustainable Waste Tech Trends & Forecast 2026-2034")

, By End-User (Food Processing, Retail, Hospitality, Municipalities, Households), By Application (Collection, Treatment, Energy Recovery, Fertilizer, Animal Feed) Region, Key Players – Dynamics, Circular Bioeconomy & Sustainable Waste Tech Trends & Forecast 2026-2034")

, By End-User (Food Processing, Retail, Hospitality, Municipalities, Households), By Application (Collection, Treatment, Energy Recovery, Fertilizer, Animal Feed) Region, Key Players – Dynamics, Circular Bioeconomy & Sustainable Waste Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Food Waste Management Technology Market?

Global Food Waste Management Technology Market was valued at USD 24.80 billion in 2024 and is projected to reach USD 50.60 billion by 2034, at a CAGR of 7.5% (2026–2034).

Who are the major players in the Food Waste Management Technology Market?

VEOLIA ENVIRONNEMENT SA, WASTE MANAGEMENT, INC., REPUBLIC SERVICES, INC., DIVERT, INC., ANAERGIA INC., VANGUARD RENEWABLES, MILL INDUSTRIES INC., TOO GOOD TO GO, WINNOW SOLUTIONS LTD, LEANPATH, APEEL SCIENCES, GFL ENVIRONMENTAL INC., BIFFA PLC, FCC ENVIRONMENT LTD, REWORLD (FORMERLY COVANTA), REMONDIS SE & CO. KG, STERICYCLE, INC., DARLING INGREDIENTS INC., RECOLOGY INC., OTHERS

Which segments covered the Food Waste Management Technology Market?

By Technology Type, (Anaerobic Digestion, Composting, Waste-to-Energy (Incineration), Food Waste Recycling, Smart Waste Monitoring & Analytics), By End-User, (Food Processing Companies, Retail & Supermarkets, Hospitality & Foodservice, Municipalities, Households, Others), By Application, (Food Waste Collection, Waste Treatment & Disposal, Energy Recovery, Organic Fertilizer Production, Animal Feed Production, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Food Waste Management Technology Market

Published Date : 16 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date