- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Foundation Model as a Service Market Forecast 2034 | CAGR 23.4%

Global Foundation Model as a Service (FMaaS) Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, Hybrid, On-Premise), By Model Type (Large Language Models, Multimodal Models, Code Generation Models, Vision Models), By Application (Content Generation, Conversational AI, Search & Retrieval, Code Development, Data Analysis, Others), By End-User Industry (Technology, BFSI, Retail, Healthcare, Professional Services, Manufacturing, Government) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

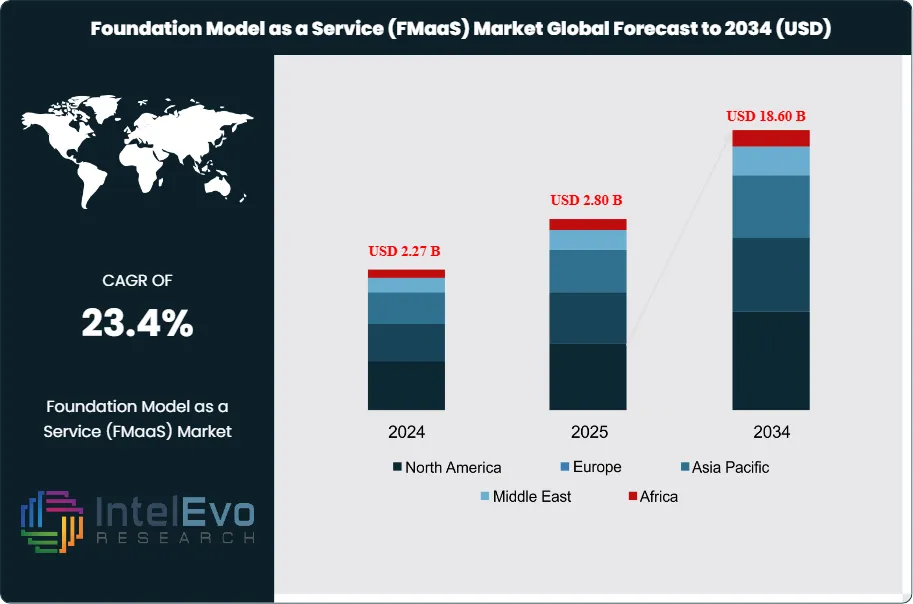

| USD 2.8 Billion | USD 18.6 Billion | 23.4% | North America, 42.5% |

The Foundation Model as a Service (FMaaS) Market was valued at approximately USD 2.27 Billion in 2024 and reached USD 2.80 Billion in 2025. The market is projected to grow to USD 18.60 Billion by 2034, expanding at a CAGR of 23.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.8 Billion over the analysis period. Foundation models are large-scale AI systems trained on extensive datasets that can be fine-tuned or adapted for diverse downstream applications. The as-a-service delivery model enables organizations to access these computationally intensive models via APIs without maintaining dedicated infrastructure.

Get More Information about this report -

Request Free Sample ReportEnterprise adoption has accelerated sharply since 2023 as organizations across industries seek to integrate generative AI into workflows. The market expansion is driven by rapid improvements in model capabilities, declining inference costs, and increasing availability of specialized industry-specific adaptations. API-based consumption eliminates the capital expenditure and technical complexity associated with training proprietary foundation models, which can exceed USD 100 million for frontier systems. Cloud hyperscalers have emerged as dominant distribution channels, with Microsoft Azure, Google Cloud, and AWS collectively facilitating access to models from both proprietary and open-source providers.

Regulatory frameworks are evolving to address foundation model deployment. The EU AI Act establishes tiered compliance requirements based on risk classification, while Executive Orders in the United States mandate transparency for dual-use foundation models exceeding certain compute thresholds. These requirements create market opportunities for compliance-focused service layers and audit tools. The NIST AI Risk Management Framework provides voluntary guidance that influences enterprise procurement decisions, particularly in regulated sectors including financial services and healthcare.

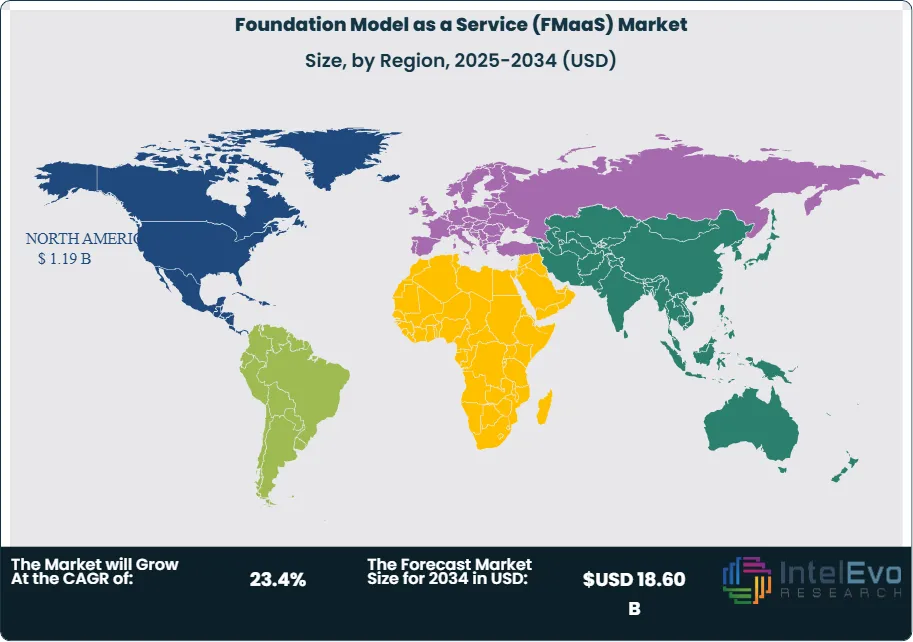

Regional concentration remains pronounced. North America captured 42.5% of market revenue in 2025, reflecting the geographic clustering of leading AI research labs and cloud providers. Asia Pacific represents the fastest-growing region, with enterprise adoption in China, Japan, South Korea, and India accelerating through 2024 and into 2025. European demand is shaped by data sovereignty requirements and the AI Act compliance timeline, creating opportunities for regional providers and localized deployments.

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, Hybrid, On-Premise), By Model Type (Large Language Models, Multimodal Models, Code Generation Models, Vision Models), By Application (Content Generation, Conversational AI, Search & Retrieval, Code Development, Data Analysis, Others), By End-User Industry (Technology, BFSI, Retail, Healthcare, Professional Services, Manufacturing, Government) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Foundation Model as a Service market reached USD 2.8 Billion in 2025 and is projected to grow to USD 18.6 Billion by 2034, registering a CAGR of 23.4% across the forecast period.

- Segment Dominance: By deployment mode, cloud-based delivery dominated with 78.2% market share in 2025 as enterprises prioritized scalability and reduced infrastructure burden.

- Segment Dominance: By application, content generation and conversational AI collectively accounted for 47.5% of market revenue in 2025, driven by enterprise productivity use cases.

- Driver: Enterprise productivity gains from AI-assisted workflows increased demand by an estimated 34% year-over-year in 2025, with organizations reporting 25-40% efficiency improvements in content-heavy processes.

- Restraint: Data privacy concerns limited adoption among 31% of surveyed enterprises in 2025, particularly in healthcare and financial services sectors where regulatory scrutiny is highest.

- Opportunity: Vertical-specific fine-tuned models represent a USD 4.2 Billion addressable segment by 2030, with legal, medical, and financial services leading demand for specialized adaptations.

- Trend: Agentic AI architectures capable of multi-step reasoning and tool use gained adoption among 18% of enterprise API consumers in 2025, up from under 5% in early 2024.

- Regional Analysis: North America led the market with 42.5% share and USD 1.19 Billion revenue in 2025, anchored by hyperscaler infrastructure and concentrated AI research investment.

Competitive Landscape Overview

The Foundation Model as a Service market exhibits moderate consolidation, with the top four providers accounting for approximately 68% of market revenue in 2025. Competition is technology-driven rather than price-driven, as model capabilities, inference latency, context window size, and multimodal support differentiate offerings. Microsoft, Google, Amazon, and OpenAI maintain leadership positions through integrated cloud ecosystems and proprietary model development. Challengers including Anthropic and Cohere have gained enterprise traction through differentiated safety approaches and domain-specific optimization. M&A activity intensified through 2024 and 2025, with hyperscalers acquiring model providers and infrastructure startups to strengthen vertical integration.

| Company | HQ | Position | Key Solution | Strength | Recent Strategic Move (2024–2026) |

| Microsoft | USA | Leader | Azure OpenAI Service | North America | Expanded Copilot integration across enterprise suite (Jan 2025) |

| USA | Leader | Vertex AI (Gemini) | Global | Launched Gemini 2.0 with enhanced multimodal capabilities (Feb 2025) | |

| Amazon Web Services | USA | Leader | Amazon Bedrock | North America | Added Claude 3.5 and Llama 3 to Bedrock model garden (Dec 2024) |

| OpenAI | USA | Leader | OpenAI API Platform | North America | Released GPT-5 with improved reasoning and tool use (Mar 2025) |

| Anthropic | USA | Challenger | Claude API | North America | Secured USD 2B Series C funding for enterprise expansion (Jan 2025) |

| Cohere | Canada | Challenger | Cohere Command | North America | Launched Command R+ with 128K context for enterprise RAG (Dec 2024) |

| Meta Platforms | USA | Challenger | Llama API (via partners) | Global | Open-sourced Llama 3 405B for commercial deployment (Mar 2025) |

| IBM | USA | Niche Player | watsonx.ai | Enterprise | Integrated Granite models with hybrid cloud deployments (Feb 2025) |

| Hugging Face | USA | Niche Player | Inference Endpoints | Developer | Surpassed 1M hosted models on platform (Jan 2025) |

| Mistral AI | France | Niche Player | Mistral Platform | Europe | Raised EUR 600M Series B; launched Mistral Large 2 (Dec 2024) |

By Deployment Mode

The Foundation Model as a Service market segmentation by deployment mode distinguishes cloud-based, hybrid, and on-premise implementations. Cloud-based deployment commanded 78.2% market share in 2025, generating USD 2.19 Billion in revenue. This dominance reflects the computational requirements of foundation model inference, which benefits from elastic cloud infrastructure that scales with variable workloads. Enterprises prefer cloud consumption for rapid deployment, automatic updates to newer model versions, and avoidance of specialized GPU procurement. Major cloud providers bundle foundation model APIs with existing enterprise agreements, simplifying procurement and consolidating vendor relationships.

Hybrid deployment captured 15.3% market share in 2025, valued at USD 428 Million. This architecture addresses data residency requirements by processing sensitive data locally while routing non-sensitive workloads to cloud endpoints. Financial institutions and healthcare organizations favor hybrid configurations to maintain regulatory compliance while accessing frontier model capabilities. The approach requires additional orchestration infrastructure, increasing implementation complexity but providing granular control over data flows.

On-premise deployment accounted for the remaining 6.5% of market share in 2025. Government agencies, defense contractors, and organizations with air-gapped security requirements represent primary adopters. On-premise implementations utilize smaller, efficient models that run on available hardware, often sacrificing performance for security isolation. This segment is expected to grow modestly as edge-optimized models become available.

By Model Type

Segmentation by model type includes large language models, multimodal models, vision models, and code generation models. Large language models represented 52.8% of market revenue in 2025, totaling USD 1.48 Billion. Text-centric applications including document summarization, customer service automation, and content generation drove this segment. GPT-4, Claude 3, Gemini Pro, and Llama 3 constituted the most frequently accessed LLM families through commercial APIs. Enterprise adoption concentrated on models with strong instruction-following capabilities and low hallucination rates.

Multimodal models captured 24.6% market share in 2025, generating USD 689 Million. These systems process combinations of text, images, audio, and video, enabling applications including visual question answering, document understanding, and accessibility features. Google Gemini and GPT-4V led adoption in this segment. Demand accelerated as organizations sought to automate workflows involving unstructured visual content, particularly in insurance claims processing, retail product cataloging, and medical imaging triage.

Code generation models accounted for 14.2% of market share, with USD 398 Million in 2025 revenue. Developer productivity tools including GitHub Copilot, Amazon CodeWhisperer, and Anthropic Claude for coding drove enterprise subscriptions. Software development organizations reported 30-55% productivity gains for code completion and debugging tasks. Vision-only models held the remaining 8.4% share, serving specialized applications in manufacturing quality inspection and autonomous systems.

By Application

Application-based segmentation spans content generation, conversational AI, search and retrieval, code development, data analysis, and other specialized functions. Content generation led with 26.3% market share in 2025, valued at USD 736 Million. Marketing teams, media organizations, and professional services firms deployed foundation models for drafting, editing, and repurposing content across formats. Productivity gains of 40-60% in initial content drafting were reported across enterprise surveys.

Conversational AI applications captured 21.2% market share, generating USD 594 Million in 2025. Customer service chatbots, virtual assistants, and internal knowledge management systems represented primary deployment scenarios. Foundation models replaced rule-based chatbot systems that required extensive intent mapping, reducing implementation time from months to weeks. Retrieval-augmented generation architectures connected conversational interfaces to enterprise knowledge bases, improving response accuracy.

Search and retrieval applications held 18.5% share at USD 518 Million. Semantic search over enterprise documents, legal discovery, and research acceleration constituted leading use cases. Code development applications accounted for 17.8% share. Data analysis and insight generation captured 10.7%, while remaining specialized applications including translation, summarization, and accessibility tools held 5.5%.

By End-User Industry

End-user industry segmentation reveals technology and media leading adoption with 28.4% market share in 2025. Software companies embedded foundation model capabilities into products, while media organizations automated content production workflows. Financial services followed with 19.7% share, applying models to document processing, compliance monitoring, and customer communication. Retail and e-commerce captured 15.2%, leveraging models for product description generation, customer service, and personalization.

Healthcare and life sciences represented 12.8% of market revenue despite regulatory caution, with applications in clinical documentation, medical literature analysis, and patient communication. Professional services including legal, consulting, and accounting held 11.3% share. Manufacturing and industrial segments accounted for 7.1%, while government and public sector captured 5.5% as procurement cycles lengthened adoption timelines.

Regional Analysis

North America

North America commanded the Foundation Model as a Service market with 42.5% share and USD 1.19 Billion revenue in 2025. The United States represented 89% of regional revenue, benefiting from the concentration of leading AI research labs, venture capital investment, and cloud hyperscaler headquarters. Silicon Valley and Seattle corridors host OpenAI, Anthropic, Google DeepMind, and Microsoft AI Research, creating infrastructure and talent density unmatched globally. Enterprise adoption reached approximately 35% penetration among Fortune 500 companies by end of 2025.

The regulatory environment supported innovation while establishing guardrails. Executive Orders mandated safety testing and reporting for dual-use foundation models, influencing procurement requirements among government contractors and defense adjacent industries. California introduced state-level AI transparency requirements that may establish precedent for broader adoption. Canada contributed 8% of regional revenue, with Cohere headquartered in Toronto and federal AI investment programs supporting research commercialization. Mexico represented an emerging opportunity as nearshoring trends increased technology investment.

Enterprise spending concentrated among financial services, technology, and healthcare verticals. JPMorgan Chase, Bank of America, and Goldman Sachs deployed foundation model APIs for document processing and customer interaction. Technology companies including Salesforce, ServiceNow, and Adobe embedded foundation model capabilities into SaaS platforms. The U.S. Department of Defense initiated pilot programs exploring foundation model applications for logistics and administrative functions.

Europe

Europe captured 23.8% of the Foundation Model as a Service market in 2025, generating USD 666 Million in revenue. The regulatory framework shaped competitive dynamics distinctly from other regions. The EU AI Act, entering phased implementation, established compliance requirements for foundation model providers and deployers. Organizations began allocating budgets for AI governance, creating adjacent market opportunities for compliance tooling and audit services.

Germany led regional adoption with 24% of European revenue, followed by the United Kingdom at 21%, France at 18%, and the Netherlands at 9%. German automotive and manufacturing enterprises deployed foundation models for technical documentation and engineering support. The UK financial services sector in London adopted conversational AI and document processing applications. France emerged as a foundation model development hub with Mistral AI raising EUR 600 Million and attracting enterprise customers seeking European alternatives to U.S. providers.

Data sovereignty requirements influenced architectural decisions, with European enterprises preferring providers offering EU-based inference endpoints. Microsoft expanded Azure OpenAI availability across European data centers. Google Cloud established Vertex AI access in multiple European regions. Sovereign cloud initiatives in France and Germany created protected infrastructure environments for sensitive government applications.

Asia Pacific

Asia Pacific represented 24.2% of the Foundation Model as a Service market with USD 678 Million revenue in 2025. The region exhibited the fastest growth trajectory, projected to achieve 26.8% CAGR through 2034. China accounted for 38% of regional revenue through domestic foundation model providers including Baidu, Alibaba, and Tencent, as geopolitical restrictions limited access to U.S.-developed models. The Chinese government supported domestic AI development through policy initiatives and computing infrastructure investment.

Japan contributed 22% of regional revenue, with enterprises in automotive, electronics, and financial services deploying foundation models for customer service and technical applications. Language-specific model adaptations addressed Japanese linguistic complexity. South Korea represented 16% of Asia Pacific revenue, with Samsung, LG, and Hyundai integrating foundation model capabilities into product development and customer support workflows. India captured 12% share, led by IT services companies deploying models for software development acceleration and customer service automation.

Australia contributed 7% of regional revenue with adoption concentrated in financial services and professional services. Singapore established itself as a Southeast Asian hub for AI deployment, benefiting from regulatory clarity and infrastructure availability. Cloud hyperscaler expansion across the region improved latency and data residency options, supporting enterprise adoption acceleration.

Latin America

Latin America accounted for 5.2% of the Foundation Model as a Service market in 2025, generating USD 146 Million in revenue. Brazil dominated regional adoption with 52% of Latin American revenue, driven by financial services modernization and e-commerce growth. Nubank, Mercado Libre, and Itau Unibanco deployed conversational AI and customer service automation. Portuguese and Spanish language model capabilities improved through 2024-2025, reducing barriers to regional deployment.

Mexico contributed 28% of regional revenue, benefiting from nearshoring investment that increased technology spending. U.S.-adjacent time zones and bilingual workforce availability supported customer service deployments serving North American markets. Chile and Colombia represented emerging opportunities with startup ecosystems and government digitalization initiatives driving early adoption. Argentina faced economic headwinds limiting enterprise technology investment despite technical talent availability.

Infrastructure constraints including data center availability and network latency impacted deployment options. Cloud hyperscalers expanded regional presence, with AWS and Microsoft Azure establishing additional availability zones in Brazil and Mexico. Cost sensitivity influenced adoption patterns, with enterprises favoring API consumption models that avoided capital expenditure commitments.

Middle East & Africa

The Middle East & Africa region captured 4.3% of the Foundation Model as a Service market with USD 120 Million revenue in 2025. The United Arab Emirates led regional adoption at 38% share, driven by government AI initiatives and financial services modernization. The UAE national AI strategy established ambitious deployment targets, with government entities piloting foundation model applications in citizen services and administrative automation.

Saudi Arabia represented 31% of regional revenue, with Vision 2030 diversification initiatives spurring technology investment. NEOM and other giga-projects integrated AI capabilities into planning and operations. South Africa accounted for 15% of MEA revenue, with adoption concentrated in financial services including Standard Bank, FirstRand, and Nedbank. Arabic language model capabilities remained limited compared to English, constraining adoption in some applications while creating opportunities for specialized providers.

Israel contributed to regional technical development despite geographic classification complexity, with AI startups and enterprise adoption rates comparable to European markets. Infrastructure investment across Gulf Cooperation Council states improved cloud availability, with hyperscalers establishing regional data centers in the UAE and Saudi Arabia. Economic diversification objectives aligned with AI adoption, supporting above-average growth projections for the region.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud-Based

- Hybrid

- On-Premise

By Model Type

- Large Language Models (LLMs)

- Multimodal Models

- Code Generation Models

- Vision Models

By Application

- Content Generation

- Conversational AI

- Search and Retrieval

- Code Development

- Data Analysis

- Others

By End-User Industry

- Technology and Media

- Financial Services

- Retail and E-commerce

- Healthcare and Life Sciences

- Professional Services

- Manufacturing

- Government and Public Sector

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.80 B |

| Forecast Revenue (2034) | USD 18.60 B |

| CAGR (2025-2034) | 23.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, (Cloud-Based, Hybrid, On-Premise), By Model Type, (Large Language Models (LLMs), Multimodal Models, Code Generation Models, Vision Models), By Application, (Content Generation, Conversational AI, Search and Retrieval, Code Development, Data Analysis, Others), By End-User Industry, (Technology and Media, Financial Services, Retail and E-commerce, Healthcare and Life Sciences, Professional Services, Manufacturing, Government and Public Sector) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT CORPORATION, GOOGLE LLC, AMAZON WEB SERVICES (AWS), OPENAI, ANTHROPIC, META PLATFORMS INC., COHERE INC., IBM CORPORATION, HUGGING FACE INC., MISTRAL AI, AI21 LABS, NVIDIA CORPORATION, ALIBABA CLOUD, BAIDU INC., TENCENT CLOUD, ORACLE CORPORATION, SALESFORCE INC., SAP SE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, Hybrid, On-Premise), By Model Type (Large Language Models, Multimodal Models, Code Generation Models, Vision Models), By Application (Content Generation, Conversational AI, Search & Retrieval, Code Development, Data Analysis, Others), By End-User Industry (Technology, BFSI, Retail, Healthcare, Professional Services, Manufacturing, Government) Industry Trends & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, Hybrid, On-Premise), By Model Type (Large Language Models, Multimodal Models, Code Generation Models, Vision Models), By Application (Content Generation, Conversational AI, Search & Retrieval, Code Development, Data Analysis, Others), By End-User Industry (Technology, BFSI, Retail, Healthcare, Professional Services, Manufacturing, Government) Industry Trends & Forecast 2026–2034")

Market Size, Share, Growth & Industry Analysis By Deployment Mode (Cloud-Based, Hybrid, On-Premise), By Model Type (Large Language Models, Multimodal Models, Code Generation Models, Vision Models), By Application (Content Generation, Conversational AI, Search & Retrieval, Code Development, Data Analysis, Others), By End-User Industry (Technology, BFSI, Retail, Healthcare, Professional Services, Manufacturing, Government) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Foundation Model as a Service (FMaaS) Market?

Global Foundation Model as a Service market valued at USD 2.27B in 2024, reaching USD 18.6B by 2034, growing at a CAGR of 23.4% from 2026–2034.

Who are the major players in the Foundation Model as a Service (FMaaS) Market?

MICROSOFT CORPORATION, GOOGLE LLC, AMAZON WEB SERVICES (AWS), OPENAI, ANTHROPIC, META PLATFORMS INC., COHERE INC., IBM CORPORATION, HUGGING FACE INC., MISTRAL AI, AI21 LABS, NVIDIA CORPORATION, ALIBABA CLOUD, BAIDU INC., TENCENT CLOUD, ORACLE CORPORATION, SALESFORCE INC., SAP SE, Others

Which segments covered the Foundation Model as a Service (FMaaS) Market?

By Deployment Mode, (Cloud-Based, Hybrid, On-Premise), By Model Type, (Large Language Models (LLMs), Multimodal Models, Code Generation Models, Vision Models), By Application, (Content Generation, Conversational AI, Search and Retrieval, Code Development, Data Analysis, Others), By End-User Industry, (Technology and Media, Financial Services, Retail and E-commerce, Healthcare and Life Sciences, Professional Services, Manufacturing, Government and Public Sector)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Foundation Model as a Service (FMaaS) Market

Published Date : 11 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date