- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

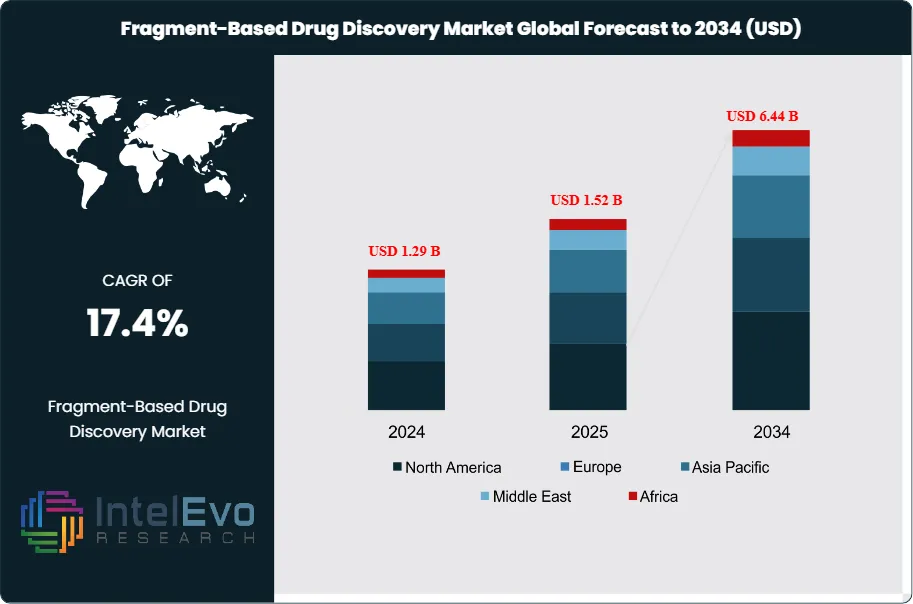

Global Fragment-Based Drug Discovery Market Size, Share | CAGR 17.4%

Global Fragment-Based Drug Discovery Market Size, Share, Growth Analysis By Technology Platform (Nuclear Magnetic Resonance, X-Ray Crystallography, Surface Plasmon Resonance, Mass Spectrometry, Cryo-EM), By Application (Oncology, Neurology, Infectious Diseases, Cardiovascular Disorders), By End-User (Pharmaceutical Companies, CROs, Biotechnology Firms, Research Institutes), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

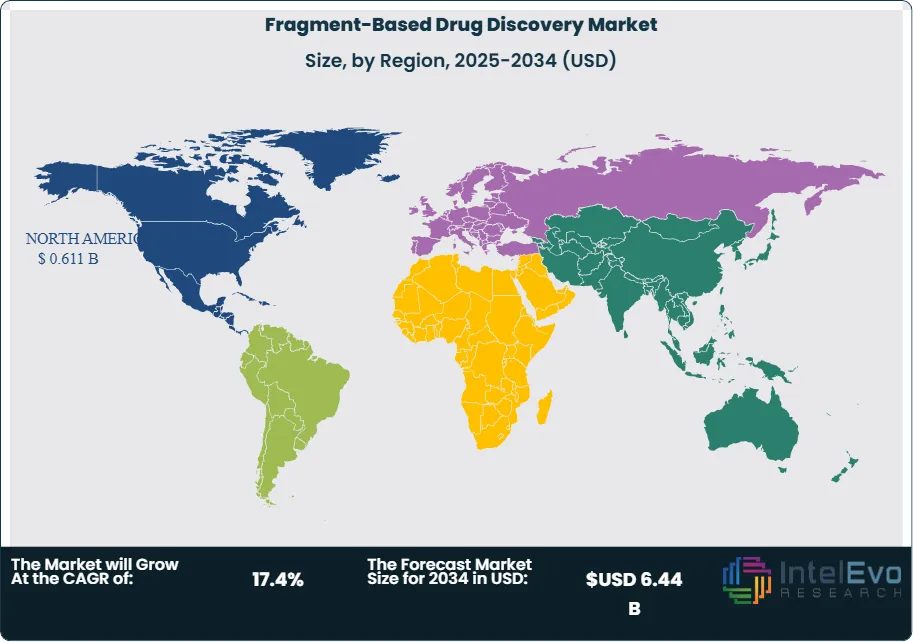

| USD 1.52 Billion | USD 6.44 Billion | 17.4% | North America, 40.2% |

The Fragment-Based Drug Discovery Market was valued at approximately USD 1.29 Billion in 2024 and reached USD 1.52 Billion in 2025. The market is projected to grow to USD 6.44 Billion by 2034, expanding at a CAGR of 17.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.92 Billion over the analysis period — growth anchored by the convergence of structural biology technology maturation enabling fragment-to-lead optimization at previously impractical speed, the pharmaceutical industry's intensifying focus on undruggable targets that conventional high-throughput screening cannot address, and the integration of computational and artificial intelligence tools that are compressing fragment-based drug discovery cycle times to competitive parity with high-throughput screening for structurally characterized target classes.

Get More Information about this report -

Request Free Sample ReportThe fragment-based drug discovery market's commercial logic rests on a fundamental pharmacological argument that distinguishes it from all other small-molecule lead generation strategies. Conventional high-throughput screening evaluates libraries of 100,000–10 million drug-like compounds (molecular weight 300–600 Da) against a target, relying on statistically finding pre-optimized molecules with sufficient binding affinity for detection. Fragment-based screening evaluates libraries of 500–10,000 low-molecular-weight fragments (typically 100–250 Da, obeying the Rule of Three: molecular weight below 300 Da, ClogP below 3, hydrogen bond donors and acceptors below 3) that bind with weak affinity (typically Kd of 100 μM–10 mM) but high ligand efficiency — the binding energy per heavy atom. This ligand efficiency prioritization identifies chemically tractable starting points for optimization that, by construction, occupy chemical space more efficiently than larger drug-like molecules and therefore afford greater medicinal chemistry design freedom during lead optimization. The commercial implication is clinical: fragment-derived leads have demonstrated superior ADMET profiles in optimization compared with HTS-derived leads in systematic comparisons, contributing to the observation that seven FDA-approved drugs — including venetoclax (ABT-199), erdafitinib, and vemurafenib — trace their discovery origins to fragment-based approaches.

Three specific triggers explain the market's current 17.4% CAGR acceleration. The first is the cryo-electron microscopy resolution revolution: cryo-EM achieved routine sub-2-Ångström resolution for soluble protein targets by 2024, enabling direct fragment binding mode visualization for protein classes including GPCRs, ion channels, and large protein complexes that resist X-ray crystallography due to difficulty achieving diffraction-quality crystals. The Medical Research Council's Laboratory of Molecular Biology in Cambridge and Diamond Light Source's national synchrotron facility at Harwell both reported 2024 fragment screening campaigns against GPCR targets using cryo-EM structural confirmation — a technical milestone that extends fragment-based drug discovery to the estimated 800+ GPCR family members representing 34% of current FDA-approved drug targets but historically underserved by fragment methods. Each GPCR added to the fragment-accessible target universe represents potentially hundreds of millions of dollars in drug discovery investment redirected toward FBDD-compatible approaches.

The second trigger is the commercial validation of fragment-derived drugs in oncology's most competitive therapeutic area. AstraZeneca's osimertinib (Tagrisso) generated USD 5.7 billion in 2024 revenue, making the EGFR inhibitor with partial fragment-based design heritage the highest-revenue oncology drug with FBDD input globally — a commercial reference point that pharmaceutical R&D investment committees cite when justifying FBDD platform allocation over conventional HTS approaches. More directly, Relay Therapeutics' RLY-2608, a PI3Kα allosteric inhibitor discovered through cryo-EM-guided fragment screening of allosteric sites, advanced into a pivotal Phase II breast cancer study in January 2026 — the first FBDD-discovered allosteric kinase inhibitor to reach pivotal clinical assessment and validating fragment methods for the most challenging kinase selectivity design problem in oncology.

The third trigger is Roche's USD 2.7 billion acquisition of Carmot Therapeutics in January 2025, which brought Carmot's Chemotype Evolution fragment-based platform into one of the world's largest pharmaceutical R&D organizations and specifically deployed it for GLP-1 receptor and GIPR fragment programs in metabolic disease. This acquisition signal — the largest deal in the FBDD space since AbbVie's USD 21 billion acquisition of Pharmacyclics brought venetoclax's FBDD-derived linker technology into AbbVie's portfolio — communicated to the pharmaceutical industry that fragment-based discovery infrastructure carries acquisition value comparable to clinical-stage asset portfolios. A contrarian observation qualifies the market's growth trajectory: fragment-based drug discovery remains structurally limited by the requirement for high-quality three-dimensional protein structural data. Approximately 42% of human drug targets with validated biological rationale lack sufficient structural characterization for structure-guided fragment optimization as of 2025, according to the Protein Data Bank coverage analysis — a ceiling on the fragment-addressable universe that AlphaFold3 structural predictions are partially but not fully resolving, since predicted structures carry binding site geometry uncertainties that experimental fragment electron density maps do not.

, By Application (Oncology, Neurology, Infectious Diseases, Cardiovascular Disorders), By End-User (Pharmaceutical Companies, CROs, Biotechnology Firms, Research Institutes), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global fragment-based drug discovery market reached USD 1.52 Billion in 2025 and is forecast to reach USD 6.44 Billion by 2034 at a CAGR of 17.4% during the 2026–2034 period, driven by cryo-EM's extension of fragment screening to GPCR and ion channel target classes, commercial validation of fragment-derived clinical candidates in oncology, and AI-accelerated fragment-to-lead optimization reducing cycle times by 40–50%.

- Segment Dominance (By Technology): Nuclear magnetic resonance held 34.6% of technology-platform revenue at USD 0.526 Billion in 2025 because NMR's ability to detect fragment binding in solution without crystallization prerequisites — and to simultaneously characterize binding mode, stoichiometry, and competitive displacement — provides mechanistic information depth that SPR and thermal shift assays cannot replicate for mechanistically complex targets where binding mode understanding drives lead optimization strategy.

- Segment Dominance (By Application): Oncology commanded 38.7% of application revenue at USD 0.589 Billion in 2025, anchored by the concentration of structurally characterized oncology targets in the Protein Data Bank, the commercial validation of fragment-derived oncology drugs including venetoclax (USD 2.1 billion 2024 revenue) and vemurafenib, and the pharmaceutical industry's allocation of FBDD resources toward undruggable oncology target classes including transcription factor-DNA interfaces and allosteric kinase sites.

- Driver: Cryo-EM resolution reaching sub-2-Ångström for soluble proteins by 2024 — enabling direct fragment binding visualization for GPCRs, ion channels, and protein complexes that resist X-ray crystallography — extended the fragment-accessible target universe to 800+ GPCR family members representing 34% of FDA-approved drug targets, creating the largest single expansion of FBDD's addressable market since the technique's commercialization in the late 1990s.

- Restraint: Approximately 42% of human drug targets with validated biological rationale lack sufficient three-dimensional structural characterization for structure-guided fragment optimization, and AlphaFold3 predicted structures carry binding site geometry uncertainties of 0.8–2.4 Ångströms at catalytic and allosteric residues that generate false lead optimization vectors — a structural data gap that constrains the fragment-addressable universe and limits FBDD adoption for target classes where structural biology investment has historically been lowest.

- Opportunity: Protein-protein interaction fragment targeting represents an addressable market expansion of USD 1.4–2.2 Billion by 2030, as foldamer and macrocyclic fragment technologies specifically designed for PPI binding interfaces overcome the affinity detection barrier that prevents conventional fragment screening from identifying hits at the large, shallow surfaces characteristic of the 650,000+ biologically validated protein-protein interactions that currently lack small-molecule tool compounds.

- Trend: AI-integrated fragment optimization platforms reached 44% adoption among North American FBDD practitioners in 2025 versus 18% in Asia Pacific, with generative AI fragment design reducing median fragment-to-lead cycle time from 18 months to 9 months in documented Evotec EAF and Schrödinger FEP+ platform benchmarks — a productivity differential that is driving outsourcing of AI-enabled FBDD services from pharma organizations that lack internal computational chemistry infrastructure.

- Regional Analysis: North America held 40.2% of global fragment-based drug discovery revenue at USD 0.611 Billion in 2025, anchored by NIH-funded structural genomics consortia providing open-access fragment screening data for academic FBDD programs, the concentration of FBDD-capable CROs and technology vendors in Boston and San Diego, and the highest density of clinical-stage FBDD-derived programs globally at 23 active Phase I/II candidates.

Competitive Landscape Overview

The fragment-based drug discovery market exhibits moderate fragmentation, with the top four organizations — Astex Pharmaceuticals, Evotec SE, Schrödinger, and Relay Therapeutics — collectively accounting for an estimated 42.6% of total market revenue in 2025. The competitive landscape operates across two structurally distinct commercial tiers: integrated FBDD platform companies that generate revenue through discovery partnerships, milestone payments, and royalties on fragment-derived drug candidates (Astex, Evotec, Relay); and technology and instrumentation vendors that generate recurring revenue through FBDD-enabling equipment, software, and CRO services (Bruker, Schrödinger, Charles River). These tiers are increasingly converging as technology vendors develop proprietary drug discovery programs and discovery organizations develop technology licensing revenue streams. The competitive dynamic in 2025 shifted materially following Roche's integration of Carmot Therapeutics' Chemotype Evolution platform, which removed one of the field's most distinctive fragment discovery methodologies from the commercial market and placed it within Roche's internal R&D infrastructure — a consolidation pattern that mirrors the 2019 integration of Vernalis' fragment discovery unit into Dompe Farmaceutici. Four Big Pharma organizations — Novartis in Basel, AstraZeneca in Cambridge, GSK in Stevenage, and Pfizer in Groton — now operate fully internal FBDD infrastructure at scale sufficient to reduce external CRO dependency for standard target classes, creating a competitive dynamic where remaining external FBDD market share concentrates in technically differentiated programs requiring novel fragment detection methodologies.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Astex Pharmaceuticals (Otsuka) | UK | Leader | Astex Pyramid FBDD Platform | Europe / North America | Advanced AT-527 (bemnifosbuvir) and AT-752 through Phase II in collaboration with Roche in 2025; Astex's FBDD pipeline now spans 12 active programs across oncology and virology, the largest proprietary fragment-derived clinical portfolio globally. |

| Evotec SE | Germany | Leader | Evotec BRIDGE Fragment Discovery Suite | Europe / North America | Launched Evotec AI Fragment (EAF) platform in Feb 2025, integrating generative AI with SPR and NMR fragment screening to reduce fragment-to-lead optimization timelines from 18 months to 9 months; secured three new pharma co-discovery agreements worth EUR 280 million total. |

| Schrödinger Inc. | USA | Leader | FEP+ Fragment Evolution Platform | North America / Europe | Released Schrödinger Fragment Network v3.0 in Q1 2025, incorporating quantum mechanical free energy perturbation calculations for fragment linking and merging across 220,000+ fragment library compounds with predicted binding affinity accuracy of ±0.5 kcal/mol. |

| Relay Therapeutics | USA | Leader | Dynamo Computational FBDD Platform | North America | Progressed RLY-2608 (PI3Kα inhibitor discovered via FBDD) to Phase II in allosteric oncology in 2025; Dynamo platform now integrates cryo-EM protein dynamics with fragment docking for previously undruggable allosteric site identification. |

| Bruker Corporation | USA | Challenger | Bruker AVANCE NMR FBDD Systems | North America / Europe | Launched Bruker BioSolve NMR Fragment Screening System in Sep 2025, reducing NMR-based fragment screening throughput time by 40% through cryo-probe optimization and automated ligand-observe STD experiment batching for 96-compound fragment libraries. |

| Vividion Therapeutics (Bayer) | USA | Challenger | Chemoproteomic Fragment Platform | North America | Expanded Vividion's chemoproteomic fragment map to 3,400+ druggable protein sites in Dec 2024, identifying 180 previously uncharacterized binding pockets across oncology and immunology target classes under Bayer's USD 1.5 billion collaboration framework. |

| Charles River Laboratories | USA | Challenger | Charles River FBDD CRO Services | North America / Europe | Integrated AI-assisted fragment hit triage into its FBDD service offering in Mar 2025, using ML-ranked binding mode predictions from AlphaFold3 structural outputs to prioritize fragment hits for SPR confirmation, reducing false-positive follow-up rates by 34%. |

| Carmot Therapeutics (Roche) | USA | Challenger | Chemotype Evolution FBDD Platform | North America | Roche fully integrated Carmot's Chemotype Evolution platform following acquisition completion in Jan 2025, deploying the technology across GLP-1 receptor and GIPR fragment-based lead generation programs in metabolic disease — Roche's largest FBDD infrastructure investment. |

| Fog Pharmaceuticals | USA | Niche Player | Foldamer Fragment Mimetics Platform | North America | Raised USD 62 million Series B in Jul 2025 to expand its hydrogen-bond surrogate foldamer technology into protein-protein interaction fragment targets across oncology, adding 14 novel scaffolds covering alpha-helix mimicry for previously intractable PPI binding sites. |

| Nuclera | UK | Niche Player | eProtein Desktop Protein Production | Europe / North America | Launched Nuclera eProtein v2 in Oct 2025 — a desktop cell-free protein expression system enabling rapid target protein production for NMR and SPR fragment screening without dedicated biochemistry infrastructure, reducing target preparation lead times from 8 weeks to 5 days. |

By Technology Platform

Nuclear magnetic resonance captured 34.6% of technology-platform segmented fragment-based drug discovery revenue at USD 0.526 Billion in 2025 — a leadership position grounded in NMR's unique combination of solution-phase sensitivity, binding mode characterization capability, and absence of crystallization prerequisites that collectively make it the only fragment screening technique providing mechanistic binding information rather than purely affinity measurements. The specific advantage of NMR-based fragment screening over competing detection platforms is its ability to distinguish between fragments binding at the target site versus non-specific aggregation binding — a critical disambiguation that avoids the false-positive hits that represent 40–60% of SPR fragment hits in screening campaigns against proteins with exposed hydrophobic patches. Astex Pharmaceuticals' proprietary Pyramid platform, which combines 19F NMR fragment library screening with 1H STD experiments for primary hit identification, achieves false-positive rates below 8% on campaign benchmarks — a precision level that justifies the higher per-compound screening cost of NMR (USD 85–120 per fragment) compared with SPR (USD 35–65 per fragment) for high-value target programs where false-positive follow-up costs exceed the primary screening differential. The Bruker BioSolve NMR Fragment Screening System's September 2025 launch, achieving 40% throughput improvement through cryo-probe optimization, is reducing NMR's throughput disadvantage relative to SPR-based competitive platforms.

X-ray crystallography held 28.4% of technology revenue at USD 0.432 Billion in 2025, its position sustained by the irreplaceable structural detail that fragment electron density maps provide for structure-guided lead optimization — the stage where X-ray data translates fragment binding mode into medicinal chemistry hypotheses for potency improvement. Diamond Light Source's I04-1 beamline at Harwell, operating the world's highest-throughput fragment crystallography pipeline and screening approximately 500 fragments per day against crystallizable targets under the XChem national access program, has processed over 28,000 fragment screening experiments since inception — generating a public dataset that academic FBDD groups globally access through PDB deposition. Surface plasmon resonance at 18.2% is growing fastest within the technology segmentation at an estimated 21.4% annually, driven by its amenability to automation and relatively low per-compound screening cost that makes SPR the preferred primary screening platform for industrial-scale campaigns at pharmaceutical company FBDD groups with 1,000+ compound fragment libraries requiring rapid throughput. Mass spectrometry at 12.4% is growing through the specific application of native mass spectrometry for fragment screening against membrane proteins and protein-protein interaction targets that resist crystallographic and NMR approaches, while thermal shift assay, isothermal titration calorimetry, and cryo-EM-based methods collectively account for the remaining 6.4% of technology revenue.

By Application

Oncology commanded 38.7% of application-segmented fragment-based drug discovery revenue at USD 0.589 Billion in 2025. This dominance reflects a specific structural reason rather than general therapeutic area priority: oncology possesses the largest repository of high-resolution protein structural data in the Protein Data Bank, particularly for kinases, E3 ubiquitin ligases, and epigenetic reader domains, which collectively represent 44% of oncology drug targets and for which fragment screening is most structurally tractable. The commercial validation argument for oncology FBDD is quantifiable: venetoclax generated USD 2.1 billion in 2024 revenue and was discovered through a fragment-based approach at Abbvie/Genentech targeting the BH3-binding groove of BCL-2 — a protein-protein interaction groove that conventional HTS failed to address over a decade of attempts. The fastest-growing oncology sub-application is covalent fragment screening targeting KRAS, KRASG12D, and other historically undruggable oncoproteins, where fragment-sized electrophilic warheads identify covalent binding sites at allosteric and switch regions inaccessible to conventional competitive inhibitors. AstraZeneca's Cambridge Oncology Discovery group and Mirati Therapeutics' — prior to its Roche acquisition — deployed covalent fragment screening as the primary hit identification strategy for the KRASG12D programs that produced adagrasib and follow-on candidates.

Neurology held 21.4% of application revenue at USD 0.325 Billion in 2025, growing at 19.8% annually — above the overall market rate — driven by the structural characterization of neurodegenerative disease targets including LRRK2, PINK1, parkin, and tau that previously lacked adequate structural data for FBDD. The specific event accelerating neurology FBDD is the Aligning Science Across Parkinson's consortium's structural atlas initiative, which funded cryo-EM structures of 34 Parkinson's disease-relevant proteins between 2022 and 2025, directly enabling fragment screening campaigns at academic and industry FBDD groups that lacked resources for independent structural biology programs. Infectious diseases at 16.8% benefits from the post-COVID-19 investment in antiviral fragment screening — Astex Pharmaceuticals' bemnifosbuvir entered Phase II against RSV and influenza in 2025 as a fragment-derived nucleoside analog — while cardiovascular at 13.6% and other therapeutic areas at 9.5% complete the application distribution.

By End-User

Pharmaceutical and biopharmaceutical companies represented 52.3% of end-user demand at USD 0.795 Billion in 2025, their dominant position reflecting the direct integration of FBDD into industrial drug discovery pipelines at all five of the top-ten global pharmaceutical companies by R&D expenditure. The specific procurement behavior of pharma FBDD groups divides between technology acquisition (NMR instruments, X-ray crystallography beamtime, SPR instrument platforms) representing approximately 61% of pharma FBDD spend, and external service contracts with FBDD-specialized CROs for novel target classes where internal structural biology infrastructure lacks necessary expertise. Novartis' Global Discovery Chemistry group in Basel operates the largest internal pharmaceutical FBDD capability globally, with a 20,000-compound fragment library screened across 40+ targets annually using integrated NMR, X-ray, and SPR platforms — a scale that defines the internal FBDD benchmark against which external CRO service offerings must compete. Academic and research institutes at 24.6% generate significant FBDD market revenue through national facility access programs (Diamond Light Source, APS in Argonne, NSLS-II at Brookhaven) and EU Horizon Europe structural biology consortium grants that collectively fund 340+ active academic FBDD programs globally as of 2025. CROs at 16.8% are growing fastest at an estimated 22.1% annually, driven by the outsourcing trend from mid-size pharmaceutical companies lacking the capital to maintain full-spectrum internal FBDD infrastructure across NMR, crystallography, and computational platforms simultaneously.

Regional Analysis

North America

NIH-funded structural genomics consortia — including the Center for Structural Genomics of Infectious Diseases at the University of Chicago and the National Center for Advancing Translational Sciences' fragment screening program — providing open-access fragment screening data for 2,400+ protein targets, combined with the highest concentration of FBDD-capable CROs in the Boston-Cambridge and San Diego-La Jolla biotech corridors, anchored North America's fragment-based drug discovery market at 40.2% of global revenue and USD 0.611 Billion in 2025. The United States accounts for approximately 91% of North American market revenue, with the National Institutes of Health's fiscal year 2025 structural biology funding allocation of USD 1.8 billion sustaining academic FBDD programs at approximately 140 U.S. research universities with protein X-ray crystallography or cryo-EM infrastructure. The Boston-Cambridge cluster — home to Relay Therapeutics, Fog Pharmaceuticals, Vividion Therapeutics' East Coast operations, and the Broad Institute's fragment screening center — generated an estimated 38% of total U.S. FBDD-related venture capital investment in 2025, concentrated in AI-integrated platform companies developing proprietary fragment discovery pipelines rather than standalone biotech therapeutics programs. The National Synchrotron Light Source II at Brookhaven National Laboratory in Upton, New York, expanded its AMX and FMX beamlines for high-throughput fragment crystallography access in 2025, processing 18,000+ fragment soaking experiments for academic and industry users under the life sciences proposal review system.

Europe

Structural biology infrastructure across Diamond Light Source's XChem program in Harwell, the European Synchrotron Radiation Facility's ID29 serial crystallography beamline in Grenoble, and DESY's P14 beamline in Hamburg collectively processed approximately 85,000 fragment screening experiments for European pharmaceutical and academic FBDD programs in 2025, sustaining Europe's position at 28.4% global share worth USD 0.432 Billion. The United Kingdom dominated European FBDD market revenue through the geographic concentration of FBDD-specialized organizations in the Cambridge-Oxford biotech corridor: Astex Pharmaceuticals' primary research site in Cambridge, Nuclera's desktop protein production technology developed at the Wellcome Sanger Institute, and the Diamond-supported XChem national fragment screening pipeline that collectively make the UK the highest fragment screening throughput geography outside the United States. Germany contributed the second-largest European sub-market through Evotec's Hamburg and Munich research campuses and the German Cancer Research Center's (DKFZ) fragment-based chemical biology programs targeting oncology protein-protein interactions in Heidelberg — the DKFZ's collaboration with BioNTech on protein degrader target fragment mapping generated significant instrument and reagent procurement in 2025. Switzerland, home to Novartis' Basel FBDD group and Roche's Carmot-integrated fragment platform in Basel and Penzberg, represents the fourth-largest European demand center by pharmaceutical FBDD platform investment despite its relatively small population and academic FBDD sector.

Asia Pacific

Sustained investment in synchrotron structural biology infrastructure across SPring-8 and Photon Factory in Japan, the Shanghai Synchrotron Radiation Facility's BL19U1 pharmaceutical crystallography beamline in Zhangjiang High-Tech Park, and the Australian Synchrotron's MX2 macromolecular crystallography beamline in Clayton, Victoria, combined with South Korea's Institute for Basic Science structural biology center in Daejeon, propelled Asia Pacific's fragment-based drug discovery market to 19.6% global share at USD 0.298 Billion in 2025. Japan led Asia Pacific FBDD revenue through Takeda Pharmaceutical's Shonan Health Innovation Park campus in Fujisawa — which operates one of Asia's largest internal pharmaceutical NMR fragment screening facilities — and through the Japan Agency for Medical Research and Development's structural biology grant program funding 48 active FBDD projects at Japanese national universities. China represented the fastest-growing APAC sub-market at an estimated 28.4% annually, driven by WuXi AppTec's Shanghai-based structural biology and FBDD service expansion, which added 14 high-field NMR instruments and two X-ray crystallography automated platforms in 2024–2025 to support pharmaceutical client fragment screening campaigns outsourced from U.S. and European drug discovery organizations. Australia's Walter and Eliza Hall Institute of Medical Research in Melbourne — the institution where venetoclax's BCL-2 fragment program clinical collaboration was co-developed — remains a globally prominent FBDD academic center with three active industry partnership agreements as of 2025.

Latin America

Structural biology capacity limitations — Latin America has four national synchrotron sources (LNLS Sirius in Campinas, Brazil; ALBA's remote user programs in Chile and Argentina; and planned facilities in Colombia) but fewer than 120 researchers with primary FBDD expertise across the region — constrain Latin America's fragment-based drug discovery market to USD 0.088 Billion (5.8% global share) in 2025, with growth concentrated in CRO service procurement rather than indigenous fragment platform development. Brazil dominates regional demand through the Laboratory of National Light Synchrotron's Sirius facility in Campinas, which opened its MX2 macromolecular crystallography beamline to pharmaceutical users in 2024 and processed the first Brazilian pharmaceutical company FBDD screening campaign for a dengue virus protease target — a program of regional health relevance given Brazil's dengue burden of 6.9 million confirmed cases in 2024. Brazilian pharmaceutical company Eurofarma's biosimilar research expansion into novel small-molecule discovery programs in 2025 created the first domestic pharma FBDD procurement event in Latin America's history, ordering Bruker NMR fragment screening infrastructure for its São Paulo research center. Argentina's FuDCI national research institute has maintained collaboration with Diamond Light Source since 2022 for Chagas disease target fragment screening — a partnership producing two published fragment hit series against Trypanosoma cruzi cruzain that represent the most advanced Latin American indigenous FBDD programs.

Middle East & Africa

Saudi Arabia's Vision 2030 life sciences investment strategy — specifically the King Abdullah University of Science and Technology's structural biology infrastructure in Thuwal and the Saudi Biobank's disease proteomics initiative — created the MEA fragment-based drug discovery market's primary indigenous demand center, contributing approximately 48% of the region's USD 0.055 Billion (3.6% share) in 2025 revenue. KAUST's beamline access program, which provides Saudi pharmaceutical researchers with remote data collection time at European synchrotron facilities pending construction of a domestic X-ray source, generated reagent and software procurement for fragment screening campaigns against tuberculosis and MERS-CoV targets of regional epidemiological significance. The UAE's Mohammed Bin Rashid University of Medicine and Health Sciences in Dubai launched a structural biology master's program in 2025 incorporating FBDD computational training using Schrödinger's Fragment Network software under an academic license agreement — the first formal FBDD academic training program in the Arabian Peninsula. South Africa's Institute of Infectious Disease and Molecular Medicine at the University of Cape Town, a WHO-designated research center, operates the most advanced FBDD program on the African continent targeting Mycobacterium tuberculosis drug-resistant strains through fragment screening campaigns conducted at Diamond Light Source under collaborative beamtime allocation agreements established through the African Light Source feasibility study consortium.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology Platform

- Nuclear Magnetic Resonance (NMR)

- X-Ray Crystallography

- Surface Plasmon Resonance (SPR)

- Mass Spectrometry

- Others (Thermal Shift Assay, ITC, Cryo-EM)

By Application

- Oncology

- Neurology

- Infectious Diseases

- Cardiovascular

- Other Therapeutic Areas

By End-User

- Pharmaceutical & Biopharmaceutical Companies

- Academic & Research Institutes

- Contract Research Organizations (CROs)

- Biotechnology Companies

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.52 B |

| Forecast Revenue (2034) | USD 6.44 B |

| CAGR (2025-2034) | 17.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology Platform, (Nuclear Magnetic Resonance (NMR), X-Ray Crystallography, Surface Plasmon Resonance (SPR), Mass Spectrometry, Others (Thermal Shift Assay, ITC, Cryo-EM)), By Application, (Oncology, Neurology, Infectious Diseases, Cardiovascular, Other Therapeutic Areas), By End-User, (Pharmaceutical & Biopharmaceutical Companies, Academic & Research Institutes, Contract Research Organizations (CROs), Biotechnology Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ASTEX PHARMACEUTICALS (OTSUKA), EVOTEC SE, SCHRÖDINGER INC., RELAY THERAPEUTICS, BRUKER CORPORATION, VIVIDION THERAPEUTICS (BAYER), CHARLES RIVER LABORATORIES, CARMOT THERAPEUTICS (ROCHE), FOG PHARMACEUTICALS, NUCLERA, AGILENT TECHNOLOGIES, FORMA THERAPEUTICS (NOVO HOLDINGS), CYCLICA (RECURSION), PEPTILOGICS, ENSEMBLE THERAPEUTICS, ALCHEMAB THERAPEUTICS, VERNALIS (DOMPÉ FARMACEUTICI), HEPTARES THERAPEUTICS (SOSEI), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Oncology, Neurology, Infectious Diseases, Cardiovascular Disorders), By End-User (Pharmaceutical Companies, CROs, Biotechnology Firms, Research Institutes), Industry Trends & Forecast 2026-2034")

, By Application (Oncology, Neurology, Infectious Diseases, Cardiovascular Disorders), By End-User (Pharmaceutical Companies, CROs, Biotechnology Firms, Research Institutes), Industry Trends & Forecast 2026-2034")

, By Application (Oncology, Neurology, Infectious Diseases, Cardiovascular Disorders), By End-User (Pharmaceutical Companies, CROs, Biotechnology Firms, Research Institutes), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Fragment-Based Drug Discovery Market?

The Global Fragment-Based Drug Discovery Market was valued at USD 1.29 Billion in 2024 and is projected to reach USD 6.44 Billion by 2034, growing at a CAGR of 17.4% from 2026 to 2034, driven by rising demand for targeted therapeutics, increasing investments in precision medicine, AI-powered drug discovery platforms, structure-based drug design technologies, and growing adoption of advanced fragment screening methods across pharmaceutical and biotechnology industries worldwide.

Who are the major players in the Fragment-Based Drug Discovery Market?

ASTEX PHARMACEUTICALS (OTSUKA), EVOTEC SE, SCHRÖDINGER INC., RELAY THERAPEUTICS, BRUKER CORPORATION, VIVIDION THERAPEUTICS (BAYER), CHARLES RIVER LABORATORIES, CARMOT THERAPEUTICS (ROCHE), FOG PHARMACEUTICALS, NUCLERA, AGILENT TECHNOLOGIES, FORMA THERAPEUTICS (NOVO HOLDINGS), CYCLICA (RECURSION), PEPTILOGICS, ENSEMBLE THERAPEUTICS, ALCHEMAB THERAPEUTICS, VERNALIS (DOMPÉ FARMACEUTICI), HEPTARES THERAPEUTICS (SOSEI), Others

Which segments covered the Fragment-Based Drug Discovery Market?

By Technology Platform, (Nuclear Magnetic Resonance (NMR), X-Ray Crystallography, Surface Plasmon Resonance (SPR), Mass Spectrometry, Others (Thermal Shift Assay, ITC, Cryo-EM)), By Application, (Oncology, Neurology, Infectious Diseases, Cardiovascular, Other Therapeutic Areas), By End-User, (Pharmaceutical & Biopharmaceutical Companies, Academic & Research Institutes, Contract Research Organizations (CROs), Biotechnology Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Fragment-Based Drug Discovery Market

Published Date : 28 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date