- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Functional Food & Nutraceuticals Market Size Forecast 2025–2034 | 7.8% CAGR

Global Functional Food and Nutraceuticals Market Size, Share, Analysis By Product Type (Functional Foods, Functional Beverages, Dietary Supplements), By Functional Food Category (Cereals, Bakery & Confectionery, Dairy Products, Snacks & Nutrition Bars, Other Functional Foods), By Functional Beverages (Weight Management Drinks, Nutritional Drinks, Muscle Building Drinks, Other Functional Beverages), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores) Industry Region & Key Players – Market Dynamics, Innovation Trends & Forecast 2025–2034

Report Overview

The Functional Food & Nutraceuticals Market was valued at USD 334.8 Billion in 2024 and is estimated to reach approximately USD 360.9 Billion in 2025. Driven by increasing consumer focus on preventive healthcare, rising demand for fortified foods, and growing adoption of dietary supplements, the market is projected to grow from about USD 389.0 Billion in 2026 to nearly USD 709.5 Billion by 2034, registering a compound annual growth rate (CAGR) of around 7.8% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportThe sector is consolidating its position within the global health and wellness economy as consumers prioritize prevention and daily performance. Category expansion is supported by higher per-capita intake, premium formulations, and broader retail and digital availability.

Demand is driven by the rising chronic disease burden and the mainstreaming of food-as-health behaviors. Non-communicable diseases account for 74% of global deaths, and diet quality remains a leading contributing factor, which sustains policy attention and consumer spending. In the United States, nearly 40% of adults reported daily dietary supplement use in 2022, underscoring mature-market depth. Aging further strengthens consumption. The population aged 60 and above is projected to rise from 1.0 billion in 2020 to 2.1 billion by 2050, expanding the addressable base for immunity, cardiovascular, cognition, bone, and metabolic health solutions. This aligns with global healthcare spending of USD 9.8 trillion in 2022, where preventive routines increasingly complement clinical care.

On the supply side, companies compete on substantiated efficacy, ingredient purity, and scalable production. Probiotics, omega-3 fatty acids, vitamins, and plant bioactives remain core revenue pools, while fortification and sugar-reduction technologies extend functional positioning into beverages, dairy, and snacks. Digitalization is reshaping commercialization and product design. E-commerce and direct-to-consumer models are reasonably estimated at 20–25% of global sales in 2024 and continue to rise as brands build first-party data. AI and automation support faster ingredient screening, stability modeling, and quality testing, while personalization engines improve conversion and retention through targeted bundles and subscription programs.

Regulation influences both growth and execution risk. The FDA’s authorized health claims, Japan’s FOSHU framework with more than 1,000 approved products, India’s FSSAI approvals exceeding 4,000 products, and sustained EFSA submissions between 2007 and 2023 signal a clear shift toward validated science and compliant innovation. North America likely contributes about 35% of 2024 revenue, while Asia Pacific leads growth, with investment hotspots in China, India, Southeast Asia, and the Gulf. Key risks include tighter claim enforcement, variability in clinical evidence standards, supply-chain volatility for specialty ingredients, and data privacy obligations as personalization expands.

, By Functional Food Category (Cereals, Bakery & Confectionery, Dairy Products, Snacks & Nutrition Bars, Other Functional Foods), By Functional Beverages (Weight Management Drinks, Nutritional Drinks, Muscle Building Drinks, Other Functional Beverages), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores) Industry Region & Key Players – Market Dynamics, Innovation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market will expand from 334.8 billion USD, 2024 to 709.5 billion USD, 2034, reflecting a 7.8% CAGR, 2026-2034. This trajectory implies net growth of 374.7 billion USD, 2034.

- Segment Dominance: Functional Food leads the product mix with a 47.3% share, 2024. It remains the largest revenue contributor at estimated: 158.4 billion USD, 2024.

- Segment Dominance: Supermarkets/Hypermarkets lead distribution with a 44.1% share, 2024. This channel generates an estimated: 147.6 billion USD, 2024 in sales.

- Driver: Consumer health management accelerates adoption, supported by a 7.8% CAGR, 2024-2034. Preventive nutrition spending sustains demand at 334.8 billion USD, 2024.

- Restraint: Regulatory scrutiny and claim substantiation raise compliance costs to estimated: 1.5% of revenue, 2024. This pressure can delay launches by estimated: 9.0 months, 2024.

- Opportunity: Premiumization and personalized nutrition expand wallet share, targeting estimated: 12.0% of category revenue, 2034. This creates incremental upside of estimated: 85.1 billion USD, 2034.

- Trend: Brands scale data-driven formulation and digital commerce, lifting online share to estimated: 24.0% of sales, 2024. AI-enabled product development reduces cycle times by estimated: 20.0%, 2024.

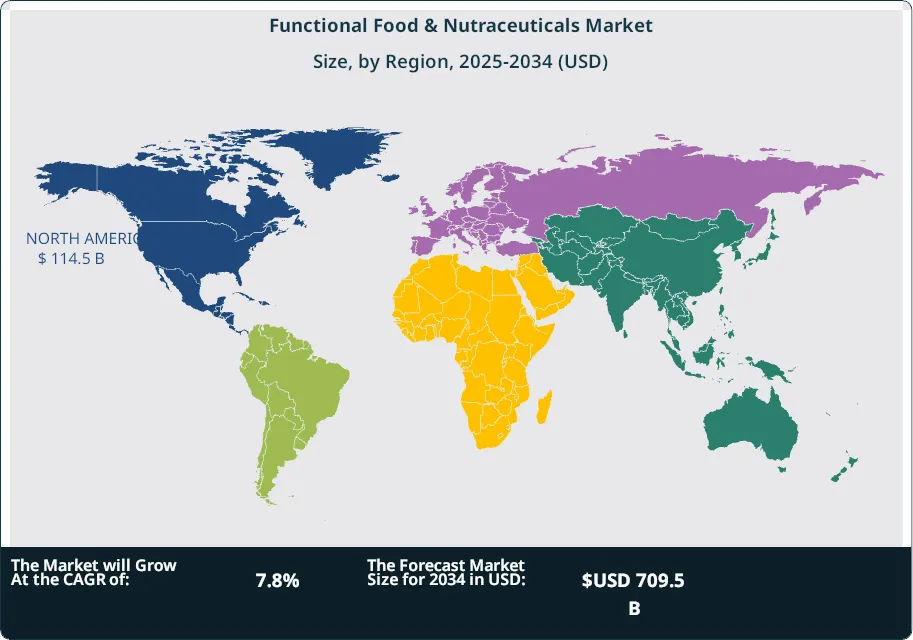

- Regional Analysis: North America holds a 34.2% share, 2024, representing 114.5 billion USD, 2024 in market value. The region remains a primary profit pool through 709.5 billion USD, 2034 global scale, 2024-2034.

By Product Type

Functional food remained the largest product category in the global functional food and nutraceuticals market, accounting for 47.3 percent of total revenue in 2024. The segment benefits from sustained consumer focus on diet-based risk reduction and daily nutrition routines. Fortified staples, probiotic dairy products, fiber-enriched snacks, and omega-3-enhanced bakery items continue to gain traction as consumers prefer food formats over capsules and tablets. High penetration among working-age adults and seniors supports repeat consumption, particularly for digestive health, immunity support, and heart health.

From 2025 onward, functional food demand is expected to grow in line with overall market expansion at a mid-to-high single-digit CAGR through 2034. Product development activity centers on protein fortification, sugar reduction, and plant-based formulations. Asia Pacific and North America remain key launch markets due to scale and purchasing power. Manufacturers are also increasing investment in clinical validation to support on-pack claims and maintain regulatory compliance, which strengthens long-term category credibility.

By Distribution Channel

Supermarkets and hypermarkets led distribution in 2024 with a 44.1 percent market share, reflecting their role as the primary purchasing point for daily nutrition products. Consumers favor these outlets for product variety, price visibility, and the ability to compare labels and ingredients in person. Large-format retailers continue to expand shelf space for fortified foods, functional beverages, and dietary supplements, integrating them into mainstream grocery aisles rather than niche sections.

Looking ahead to 2025 and beyond, this channel is expected to maintain leadership as modern retail networks expand across emerging economies. Growth is supported by private-label functional foods, in-store nutrition education programs, and targeted promotions linked to lifestyle conditions such as diabetes and cholesterol management. While online retail is growing faster, supermarkets and hypermarkets retain scale advantages and account for the majority of volume sales in developing and mature markets.

By Region

North America led the global market in 2024 with a 34.2 percent share, equivalent to approximately USD 114.5 billion in revenue. The region benefits from high consumer awareness, strong supplement usage rates, and a mature regulatory environment that supports clearly defined health claims. The United States represents the largest national market, driven by aging demographics and high prevalence of lifestyle-related conditions that influence preventive nutrition spending.

Europe followed closely, supported by demand for fortified foods, functional dairy, and plant-based nutrition. Regulatory oversight from regional authorities continues to shape product formulation and claim approval. Asia Pacific represents the fastest-growing region entering 2025, led by China, India, and Japan. Rising disposable incomes, urbanization, and government-backed nutrition programs are accelerating adoption. Latin America and the Middle East and Africa show gradual uptake, supported by expanding retail access and growing interest in immunity and chronic disease management. This regional growth is further bolstered by a rising middle class that prioritizes value-added nutrition, such as fortified cereals and energy-boosting beverages, as part of a post-pandemic shift toward proactive health maintenance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Functional Food

- Cereals

- Bakery and Confectionery

- Dairy Products

- Snacks & Bars

- Other Functional Foods

- Functional Beverages

- Weight Management Drinks

- Nutritional Drinks

- Muscle Building Drinks

- Other Functional Beverages

- Dietary Supplements

- Vitamins & Mineral

- Herbal Supplements

- Protein Supplements

- Other Dietary Supplements

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Drug Stores/Pharmacies

- Online Retail Stores

- Other Distribution Channels

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 360.9 B |

| Forecast Revenue (2034) | USD 709.5 B |

| CAGR (2025-2034) | 7.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Functional Food, Functional Beverages, Dietary Supplements), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores, Other Distribution Channels) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Bayer AG, Nu Skin Enterprises, Inc., Kellogg Company, Nature’s Sunshine Products, Inc., PepsiCo, Inc., Alticor Inc. (Amway Corporation), Abbott Laboratories, NOW Health Group, Inc. (NOW Foods), Red Bull GmbH, Danone S.A., The Hain Celestial Group, Inc., Herbalife International of America, Inc., Nestlé S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Functional Food Category (Cereals, Bakery & Confectionery, Dairy Products, Snacks & Nutrition Bars, Other Functional Foods), By Functional Beverages (Weight Management Drinks, Nutritional Drinks, Muscle Building Drinks, Other Functional Beverages), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores) Industry Region & Key Players – Market Dynamics, Innovation Trends & Forecast 2025–2034")

, By Functional Food Category (Cereals, Bakery & Confectionery, Dairy Products, Snacks & Nutrition Bars, Other Functional Foods), By Functional Beverages (Weight Management Drinks, Nutritional Drinks, Muscle Building Drinks, Other Functional Beverages), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores) Industry Region & Key Players – Market Dynamics, Innovation Trends & Forecast 2025–2034")

, By Functional Food Category (Cereals, Bakery & Confectionery, Dairy Products, Snacks & Nutrition Bars, Other Functional Foods), By Functional Beverages (Weight Management Drinks, Nutritional Drinks, Muscle Building Drinks, Other Functional Beverages), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores) Industry Region & Key Players – Market Dynamics, Innovation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Functional Food & Nutraceuticals Market?

The Global Functional Food & Nutraceuticals Market was valued at USD 334.8 Billion in 2024 and is projected to reach USD 709.5 Billion by 2034, expanding at a CAGR of 7.8% from 2026–2034. Explore key market trends, growth drivers, consumer demand for fortified foods, dietary supplements, and future industry opportunities.

Who are the major players in the Functional Food & Nutraceuticals Market?

Bayer AG, Nu Skin Enterprises, Inc., Kellogg Company, Nature’s Sunshine Products, Inc., PepsiCo, Inc., Alticor Inc. (Amway Corporation), Abbott Laboratories, NOW Health Group, Inc. (NOW Foods), Red Bull GmbH, Danone S.A., The Hain Celestial Group, Inc., Herbalife International of America, Inc., Nestlé S.A.

Which segments covered the Functional Food & Nutraceuticals Market?

By Product Type (Functional Food, Functional Beverages, Dietary Supplements), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Drug Stores/Pharmacies, Online Retail Stores, Other Distribution Channels)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Functional Food and Nutraceuticals Market

Published Date : 05 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date