- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Functional Ink and Coating Market Size, Share & Forecast | CAGR 8.6%

Global Functional Ink and Coating Market Size, Share, Growth Analysis By Product Type (Conductive Inks & Coatings, Anti-Microbial Coatings, Anti-Corrosion Coatings, UV-Curable Functional Inks, Self-Healing Coatings), By Function (Electrical Conductivity, Barrier Protection, Optical & Photovoltaic, Thermal Management), By Application, By End-Use Industry, Market Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 42.6 Billion | USD 89.4 Billion | 8.6% | Asia Pacific, 41.8% |

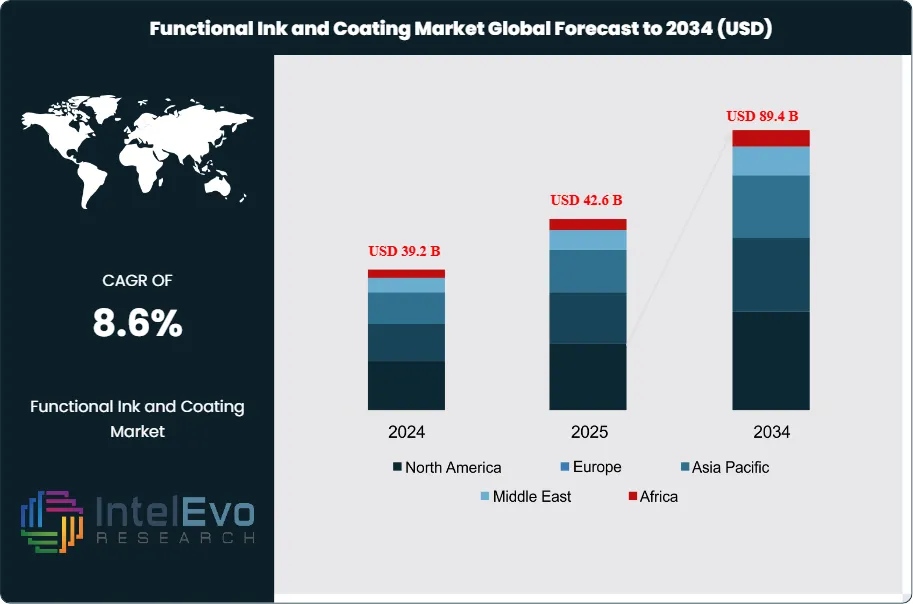

The Functional Ink and Coating Market was valued at approximately USD 39.2 Billion in 2024 and reached USD 42.6 Billion in 2025. The market is projected to grow to USD 89.4 Billion by 2034, expanding at a CAGR of 8.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 46.8 Billion over the analysis period, driven by accelerating deployment across printed electronics, high-barrier food packaging, electric vehicle battery systems, and anti-microbial healthcare surfaces where conventional inks and coatings no longer meet performance specifications.

Get More Information about this report -

Request Free Sample ReportFunctional inks and coatings are engineered formulations that deliver specific technical performance beyond decoration, including electrical conductivity, anti-microbial activity, anti-corrosion protection, thermal management, UV curability, self-healing capability, and optical functionality. Unlike conventional inks and coatings, functional variants incorporate specialty additives such as silver nanoparticles, carbon black, quaternary ammonium biocides, zinc phosphate corrosion inhibitors, and photoinitiators that activate specific performance attributes under defined service conditions. The functional ink and coating market spans seven end-use industries, with printed electronics and advanced packaging representing the fastest-growing demand centers.

The functional ink and coating market is being reshaped by regulatory-driven reformulation activity across major industrial geographies. The European Chemicals Agency (ECHA) has classified several conventional solvent systems under REACH Annex XVII restrictions, requiring reformulation to water-based or UV-curable functional alternatives by 2027. In the United States, the Environmental Protection Agency (EPA) National Emission Standards for Hazardous Air Pollutants (NESHAP) under 40 CFR Part 63 is driving accelerated conversion from solvent-based to UV-curable and powder functional coating systems, with an estimated 42% of US industrial coating lines scheduled for reformulation between 2025 and 2028. These regulatory forces are simultaneously increasing functional coating premium pricing and shifting market share toward suppliers with advanced sustainable formulation platforms.

Technology development in the functional ink and coating market is converging around three strategic priorities: conductive inks enabling printed electronics scale-up, sustainable bio-based formulations meeting Scope 3 emission reduction commitments from consumer brands, and multifunctional coatings that combine two or more performance attributes within a single formulation. Silver nanoparticle-based conductive inks, priced at USD 3,200-4,500 per kilogram in 2025, are projected to decline to USD 1,800-2,400 per kilogram by 2028 as copper-based conductive ink alternatives achieve commercial parity in low-to-mid-conductivity applications. This cost reduction will expand the addressable market for printed electronics deployment in RFID, smart packaging, and biosensor applications by an estimated USD 3.2 Billion through 2030.

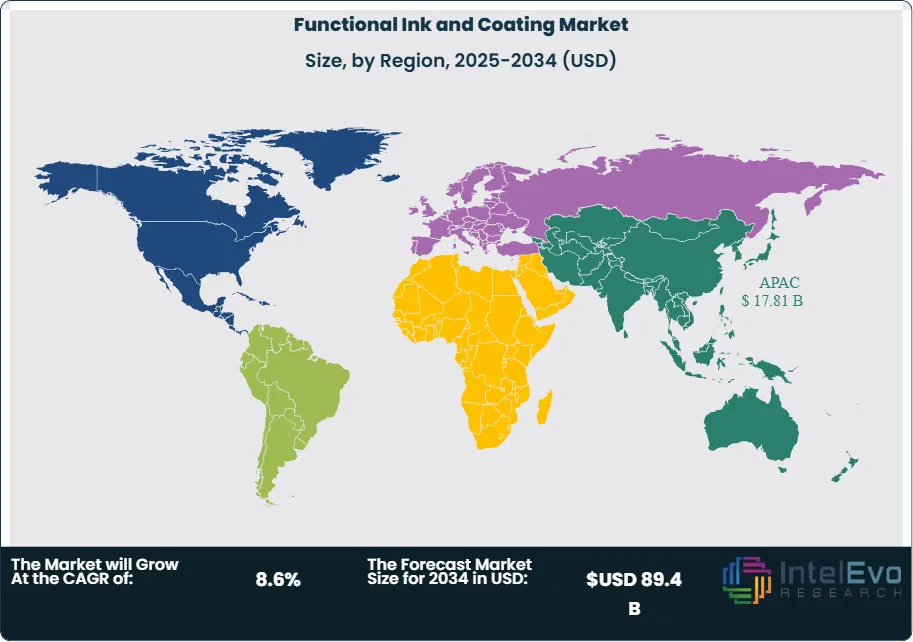

Regional dynamics in the functional ink and coating market are dominated by Asia Pacific, which commands 41.8% share in 2025 at USD 17.8 Billion. China alone accounts for 49% of regional demand, supported by the Made in China 2025 industrial policy prioritizing advanced coatings manufacturing and a domestic electronics industry producing over 1.8 Billion smartphones, PCs, and IoT devices annually that collectively consume substantial quantities of conductive and protective inks. Japan's position as global leader in specialty chemicals manufacturing, anchored by DIC, Toyo Ink, and Nippon Paint, sustains Asia Pacific's technology leadership in high-performance functional ink and coating formulations.

, By Function (Electrical Conductivity, Barrier Protection, Optical & Photovoltaic, Thermal Management), By Application, By End-Use Industry, Market Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The functional ink and coating market was valued at USD 42.6 Billion in 2025 and is projected to reach USD 89.4 Billion by 2034, expanding at a CAGR of 8.6% across the 2026-2034 forecast period.

- Segment Dominance: Anti-corrosion coatings lead the By Product Type segment with 28.5% market share in 2025, valued at USD 12.14 Billion, driven by industrial infrastructure maintenance demand and accelerating wind energy and marine sector adoption.

- Segment Dominance: Packaging applications dominate the By Application segment with 24.8% share in 2025, representing USD 10.57 Billion in revenue, supported by food brand owner demand for high-barrier functional inks meeting extended shelf-life and food contact safety standards.

- Driver: Accelerating industrial deployment of printed electronics, forecast to reach USD 78 Billion in output value by 2030 per IDTechEx sector estimates, is driving above-market growth in conductive inks with 2024-2025 year-on-year demand increase of 18.2%.

- Restraint: Volatility in silver and specialty pigment raw material prices, with silver spot prices rising 28% between 2023 and 2025, is compressing functional ink formulator margins by an estimated 4-7 percentage points and delaying price-sensitive project commitments.

- Opportunity: The emerging EV battery and motor coating segment represents a USD 6.8 Billion incremental opportunity by 2034, driven by global EV production scaling from 14 million units in 2024 to a projected 42 million units by 2030 per IEA forecasts.

- Trend: Bio-based and renewable-content functional inks are the dominant sustainability trend, with 23% of new functional ink product launches in 2025 incorporating biomass-derived binders or renewable carbon content above 30%, up from 7% in 2021.

- Regional Analysis: Asia Pacific leads all regions with a 41.8% share in 2025, representing USD 17.81 Billion in revenue, supported by China's dominant electronics manufacturing base, Japan's specialty chemicals leadership, and India's accelerating packaging sector demand.

Competitive Landscape Overview

The functional ink and coating market exhibits a moderately consolidated structure in 2025, with the top four companies — DIC Corporation (including Sun Chemical), PPG Industries, AkzoNobel, and Sherwin-Williams — collectively holding approximately 34% of global revenue. Competition is primarily technology-driven, centered on advanced formulation performance, sustainability credentials, supply chain reliability for specialty raw materials, and vertical integration into functional pigment and additive production. M&A intensity has intensified, with five transactions exceeding USD 500 Million closed between 2024 and mid-2026, most notably DIC's EUR 1.15 Billion acquisition of BASF's pigments business. Market share gains are increasingly won through long-term OEM supply contracts spanning 3-5 years, with Tier 1 electronics and automotive customers preferring suppliers that can guarantee formulation consistency and regulatory documentation across multiple geographies.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Platform | Geo Strength | Recent Strategic Move (2024-2026) |

| DIC Corporation | Japan | Leader | SunPROOF Conductive Inks | Asia Pacific / Global | Acquired BASF's global pigments business in 2024 for EUR 1.15B, consolidating functional pigment supply for printed electronics inks. |

| Sun Chemical (DIC) | USA | Leader | SunTronic Silver Conductive Inks | North America / Global | Launched new low-temperature cure conductive ink series for flexible printed circuits (Q2 2025), targeting wearable electronics OEMs. |

| PPG Industries | USA | Leader | DURANAR Functional Coatings | North America / Europe | Commissioned USD 380M specialty coatings facility in South Carolina (Mar 2025), expanding functional coating output by 28,000 tonnes/year. |

| AkzoNobel N.V. | Netherlands | Leader | Interpon Functional Powder Coatings | Europe / Global | Launched anti-microbial functional coating range certified under ISO 22196, targeting healthcare and food processing facility coatings (2025). |

| Henkel AG & Co. | Germany | Challenger | LOCTITE ECI Conductive Inks | Europe / Global | Partnered with Samsung Display for OLED conductive ink supply covering 12 production lines (Jan 2026), valued at EUR 420M over 4 years. |

| Nippon Paint Holdings | Japan | Challenger | Perfect UV Cure Functional Coatings | Asia Pacific | Completed acquisition of DuluxGroup integration, expanding functional architectural coatings footprint across Asia Pacific (2024). |

| Sherwin-Williams | USA | Challenger | POWDURA Functional Powder Coatings | North America / Europe | Launched anti-corrosion functional coating platform for wind turbine blades, capturing 22% of US wind OEM specifications in 2025. |

| Flint Group | Luxembourg | Challenger | EkoCure NCR Functional UV Inks | Europe / North America | Expanded UV-curable functional ink capacity by 35% across German and Belgian plants (Q4 2025) to meet food packaging demand. |

| Axalta Coating Systems | USA | Niche Player | Voltatex Functional Electrical Coatings | Global | Secured multi-year supply contract with Tesla for functional EV motor winding coatings valued at USD 240M (Jun 2025). |

| Toyo Ink SC Holdings | Japan | Niche Player | REXALPHA Functional Inks | Asia Pacific | Launched sustainable biomass-based functional packaging ink series with 40% renewable carbon content (Sep 2025). |

By Product Type:

Anti-corrosion coatings command the largest share at 28.5% of the functional ink and coating market in 2025, valued at USD 12.14 Billion, reflecting sustained demand from industrial infrastructure, marine, oil and gas, and renewable energy sectors where asset protection economics justify premium functional coating pricing. Zinc-rich epoxy and polyurethane anti-corrosion systems meeting ISO 12944 category C5-M (offshore) specifications generate the highest per-kilogram revenue within this segment. Conductive inks and coatings hold 18.5% share at USD 7.88 Billion, growing at an above-market rate of 14.8% CAGR through 2034 as printed electronics production scales across RFID tags, flexible PCBs, automotive sensors, and solar photovoltaic busbar applications. UV-curable functional inks account for 16.0% at USD 6.82 Billion, preferred in high-speed packaging printing lines where rapid curing eliminates solvent drying ovens and reduces energy consumption by 35-50%. Anti-microbial inks and coatings represent 12.5% at USD 5.33 Billion, a segment that experienced 2.8x growth between 2019 and 2024 following heightened post-pandemic demand across healthcare, food processing, and public infrastructure coating specifications. Self-healing coatings, an emerging category, hold 3.5% share at USD 1.49 Billion and are growing fastest at an estimated 22% CAGR as automotive OEM specifications incorporate self-healing clear coats for premium vehicle models. The remaining 21.0% spans multiple specialty product classes.

By Function:

Electrical and conductivity functions represent 22.5% of the functional ink and coating market at USD 9.59 Billion in 2025, driven by printed electronics and electronic component protection requirements. Barrier and protective functions hold the largest share at 32.0% (USD 13.63 Billion), encompassing anti-corrosion, moisture barrier, and chemical resistance coatings used across infrastructure, automotive, and packaging applications. Anti-microbial and biocidal functions account for 12.5% (USD 5.33 Billion). Optical and photovoltaic functions, including anti-reflective coatings for solar panels and optical waveguide inks for display applications, represent 15.0% at USD 6.39 Billion. Thermal management coatings, covering heat-dissipating and insulating formulations for electronics and EV batteries, contribute 10.5% at USD 4.47 Billion. The remaining 7.5% covers miscellaneous functional classes.

By Formulation:

Water-based functional inks and coatings lead at 38.0% share, valued at USD 16.19 Billion in 2025, reflecting regulatory-driven migration away from solvent-based systems under REACH and NESHAP rules. Water-based formulations achieve VOC emission levels below 50 g/L, significantly below the 350-450 g/L typical of conventional solvent systems. UV-curable formulations hold 22.5% at USD 9.59 Billion, growing at 11.2% CAGR as fast-curing performance supports high-throughput printing and coating lines. Solvent-based formulations retain 24.0% share at USD 10.22 Billion, maintained primarily in applications where performance specifications cannot yet be matched by aqueous or UV alternatives, particularly in high-humidity industrial and marine environments. Powder-based functional coatings account for 12.0% at USD 5.11 Billion, widely used in automotive, appliance, and architectural aluminum applications. Bio-based formulations, a small but fast-growing category, hold 3.5% at USD 1.49 Billion.

By Application:

Packaging is the leading application at 24.8% share, valued at USD 10.57 Billion in 2025, with food packaging functional inks complying with EU Regulation 10/2011 and FDA 21 CFR Parts 174-178 food contact material rules commanding the highest premium. Printed electronics and PCB applications represent 18.5% at USD 7.88 Billion. Automotive and EV applications hold 17.2% at USD 7.33 Billion, with EV-specific functional coatings growing at 15% CAGR to reach USD 6.8 Billion by 2034. Construction and architectural applications account for 16.0% at USD 6.82 Billion. Healthcare and medical device applications represent 9.5% at USD 4.05 Billion, driven by ISO 22196 antimicrobial efficacy requirements. Textiles and apparel contribute 7.0% at USD 2.98 Billion, with functional coatings enabling moisture management, UV protection, and anti-odor properties in performance apparel. Other applications represent 7.0%.

By End-Use Industry: Electronics and semiconductors account for 22.5% (USD 9.59 Billion); packaging 21.0% (USD 8.95 Billion); automotive 17.5% (USD 7.46 Billion); building and construction 14.5% (USD 6.18 Billion); healthcare 9.0% (USD 3.83 Billion); energy sector (solar and wind) 8.5% (USD 3.62 Billion); textiles 5.0% (USD 2.13 Billion); other industries 2.0%.

Regional Analysis

Asia Pacific

Asia Pacific dominates the global functional ink and coating market with a 41.8% share in 2025, valued at USD 17.81 Billion. China is the largest country market within the region, contributing 49% of Asia Pacific revenue at USD 8.73 Billion, driven by its position as the world's largest electronics manufacturing base and rapidly expanding domestic EV production reaching 12 million units in 2024. The Ministry of Industry and Information Technology (MIIT) has prioritized high-performance coatings and specialty chemicals within the Made in China 2025 advanced manufacturing framework, with provincial subsidies supporting domestic formulation capacity expansion. Japan accounts for 22% of Asia Pacific revenue at USD 3.92 Billion, anchored by DIC, Toyo Ink, Nippon Paint, and Kansai Paint, which collectively supply premium functional formulations to global OEM customers. India represents 16% of regional demand at USD 2.85 Billion, with the Production Linked Incentive (PLI) scheme for electronics manufacturing driving 24% year-on-year growth in conductive ink consumption. South Korea contributes 11% at USD 1.96 Billion, supported by Samsung, LG, and SK Hynix semiconductor and display manufacturing demand. Asia Pacific is forecast to grow at a CAGR of 9.6% to reach USD 40.7 Billion by 2034.

North America

North America accounts for 26.4% of the functional ink and coating market in 2025, valued at USD 11.25 Billion. The United States dominates regional demand with 83% share at USD 9.34 Billion, supported by reshoring of semiconductor manufacturing under the USD 52 Billion CHIPS and Science Act, which is stimulating domestic conductive ink and functional coating demand for wafer handling and packaging applications. EPA NESHAP reformulation mandates are simultaneously creating near-term product substitution opportunities for functional coating suppliers offering compliant alternatives. Canada contributes 11% of regional revenue at USD 1.24 Billion, driven by automotive OEM supply chains and specialty packaging manufacturers. Mexico accounts for 6% at USD 675 Million, with electronics and automotive tier supplier manufacturing hubs in Monterrey, Tijuana, and Guadalajara driving functional ink consumption. The presence of PPG, Sherwin-Williams, RPM International, and Axalta provides regional supply scale and R&D concentration that supports innovation speed. North America is projected to grow at 8.2% CAGR to reach USD 22.9 Billion by 2034.

Europe

Europe represents 22.6% of the functional ink and coating market in 2025, valued at USD 9.63 Billion. Germany leads European demand with 26% of regional revenue at USD 2.50 Billion, supported by the strength of its automotive, electronics, and chemical industries. German functional coatings consumption is heavily weighted toward automotive OEMs, with BMW, Mercedes-Benz, and Volkswagen specifying premium multifunctional coating systems on 94% of production lines. France holds 17% at USD 1.64 Billion, the UK 15% at USD 1.44 Billion, and Italy 13% at USD 1.25 Billion. The European REACH regulation has accelerated reformulation activity, with an estimated EUR 2.8 Billion in reformulation investment flowing through the European coating supply base between 2023 and 2026 to meet substance-of-very-high-concern substitution deadlines. The Circular Economy Action Plan is further driving bio-based functional ink adoption in packaging applications. European market growth is forecast at 8.1% CAGR to reach USD 19.4 Billion by 2034.

Latin America

Latin America holds 5.5% of the functional ink and coating market in 2025, valued at USD 2.34 Billion. Brazil represents 52% of regional revenue at USD 1.22 Billion, driven by packaging sector demand for functional food-grade inks and automotive OEM coatings consumption, primarily from Volkswagen, Fiat, and General Motors manufacturing operations. Mexico accounts for 34% at USD 796 Million, benefitting from USMCA-driven automotive and electronics manufacturing growth and proximity to the US market. Argentina represents 9% at USD 211 Million. The region is characterized by modest penetration of advanced functional coating technologies outside tier-one manufacturing segments, creating substantial upgrade opportunity over the forecast period. Mercosur trade policy harmonization with EU chemical standards under negotiation since 2024 could accelerate functional coating technology adoption if finalized. Regional growth is projected at 7.8% CAGR to reach USD 4.6 Billion by 2034.

Middle East and Africa

Middle East and Africa accounts for 3.7% of the functional ink and coating market in 2025, valued at USD 1.58 Billion. The UAE represents 36% of MEA revenue at USD 569 Million, supported by construction and infrastructure sector demand for anti-corrosion and weather-resistant functional coatings under Dubai 2040 urban master plan projects. Saudi Arabia accounts for 32% at USD 506 Million, with Vision 2030 Giga-Projects including NEOM and the Red Sea Project driving demand for advanced architectural and industrial functional coatings. South Africa contributes 17% at USD 269 Million, primarily in industrial and marine coating applications. Egypt, Nigeria, and Morocco collectively represent emerging functional packaging ink demand as consumer goods manufacturers expand regional operations. MEA is forecast to grow at 9.2% CAGR to reach USD 3.5 Billion by 2034, the highest regional growth rate after Asia Pacific.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Conductive Inks & Coatings

- Anti-Microbial Inks & Coatings

- Anti-Corrosion Coatings

- UV-Curable Functional Inks

- Self-Healing Coatings

By Function

- Electrical / Conductivity

- Barrier & Protective

- Anti-Microbial / Biocidal

- Optical & Photovoltaic

- Thermal Management

By Formulation

- Water-Based

- Solvent-Based

- UV-Curable

- Powder-Based

- Bio-Based / Renewable

By Application

- Printed Electronics & PCB

- Packaging (Food / Pharma)

- Automotive & EV

- Construction & Architectural

- Healthcare & Medical Devices

- Textiles & Apparel

By End-Use Industry

- Electronics & Semiconductors

- Packaging

- Automotive

- Building & Construction

- Healthcare

- Energy (Solar / Wind)

- Textiles

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 42.6 B |

| Forecast Revenue (2034) | USD 89.4 B |

| CAGR (2025-2034) | 8.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Conductive Inks & Coatings, Anti-Microbial Inks & Coatings, Anti-Corrosion Coatings, UV-Curable Functional Inks, Self-Healing Coatings), By Function, (Electrical / Conductivity, Barrier & Protective, Anti-Microbial / Biocidal, Optical & Photovoltaic, Thermal Management), By Formulation, (Water-Based, Solvent-Based, UV-Curable, Powder-Based, Bio-Based / Renewable), By Application, (Printed Electronics & PCB, Packaging (Food / Pharma), Automotive & EV, Construction & Architectural, Healthcare & Medical Devices, Textiles & Apparel), By End-Use Industry, (Electronics & Semiconductors, Packaging, Automotive, Building & Construction, Healthcare, Energy (Solar / Wind), Textiles) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | DIC CORPORATION, AKZONOBEL N.V., SHERWIN-WILLIAMS, TOYO INK SC HOLDINGS, KANSAI PAINT, SUN CHEMICAL, HENKEL AG & CO., FLINT GROUP, BASF SE, SIEGWERK DRUCKFARBEN, PPG INDUSTRIES, NIPPON PAINT HOLDINGS, AXALTA COATING SYSTEMS, RPM INTERNATIONAL, HEUBACH GROUP, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Function (Electrical Conductivity, Barrier Protection, Optical & Photovoltaic, Thermal Management), By Application, By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Function (Electrical Conductivity, Barrier Protection, Optical & Photovoltaic, Thermal Management), By Application, By End-Use Industry, Market Trends & Forecast 2026-2034")

, By Function (Electrical Conductivity, Barrier Protection, Optical & Photovoltaic, Thermal Management), By Application, By End-Use Industry, Market Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Functional Ink and Coating Market?

The Global Functional Ink and Coating Market was valued at USD 39.2 Billion in 2024 and is projected to reach USD 89.4 Billion by 2034, growing at a CAGR of 8.6% from 2026 to 2034, driven by rising demand for printed electronics, smart packaging, conductive inks, flexible displays, advanced industrial coatings, and increasing adoption across automotive, healthcare, electronics, and renewable energy applications.

Who are the major players in the Functional Ink and Coating Market?

DIC CORPORATION, AKZONOBEL N.V., SHERWIN-WILLIAMS, TOYO INK SC HOLDINGS, KANSAI PAINT, SUN CHEMICAL, HENKEL AG & CO., FLINT GROUP, BASF SE, SIEGWERK DRUCKFARBEN, PPG INDUSTRIES, NIPPON PAINT HOLDINGS, AXALTA COATING SYSTEMS, RPM INTERNATIONAL, HEUBACH GROUP, OTHERS

Which segments covered the Functional Ink and Coating Market?

By Product Type, (Conductive Inks & Coatings, Anti-Microbial Inks & Coatings, Anti-Corrosion Coatings, UV-Curable Functional Inks, Self-Healing Coatings), By Function, (Electrical / Conductivity, Barrier & Protective, Anti-Microbial / Biocidal, Optical & Photovoltaic, Thermal Management), By Formulation, (Water-Based, Solvent-Based, UV-Curable, Powder-Based, Bio-Based / Renewable), By Application, (Printed Electronics & PCB, Packaging (Food / Pharma), Automotive & EV, Construction & Architectural, Healthcare & Medical Devices, Textiles & Apparel), By End-Use Industry, (Electronics & Semiconductors, Packaging, Automotive, Building & Construction, Healthcare, Energy (Solar / Wind), Textiles)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Functional Ink and Coating Market

Published Date : 19 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date