- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Gardening Hand Tools Market Size, Share & Forecast 2034 | CAGR 6.2%

Global Gardening Hand Tools Market Size, Share, Analysis By Product Type (Hand Tools & Wheeled Implements, Cutting & Pruning Tools, Digging Tools, Water Equipment, Garden Hoses, Sprinklers, Watering Cans), By Distribution Channel (Home Centers, Specialty Stores, Retailers, E-commerce Platforms), By End-User (Residential, Commercial Landscaping, Public Parks), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

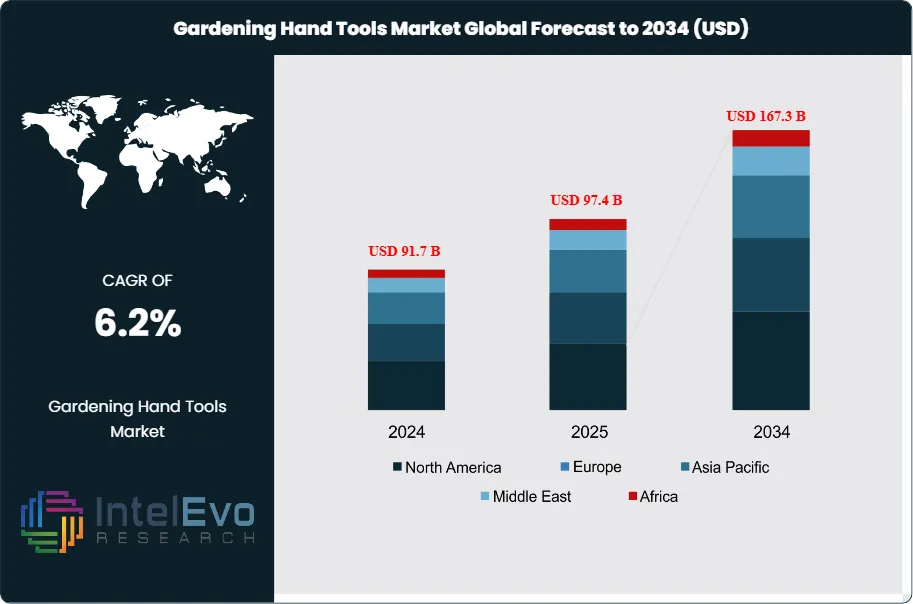

| USD 97.4 Billion | USD 167.3 Billion | 6.2% | North America, 36.7% |

The Gardening Hand Tools Market is estimated at USD 91.7 Billion in 2024 and is on track to reach roughly USD 167.3 Billion by 2034, The market is further estimated to reach approximately USD 97.4 Billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 6.2% during the forecast period from 2026 to 2034. Growth is driven by rising interest in home gardening, increasing urban landscaping activities, and expanding demand for ergonomic and sustainable gardening tools. Additionally, the rapid expansion of e-commerce distribution channels and DIY gardening trends is further supporting market growth globally.

Get More Information about this report -

Request Free Sample ReportDemand expands as households prioritize outdoor living and food gardening, while commercial landscaping and municipal green-space budgets provide steady baseline volumes. Food gardening remains a material catalyst, supported by the National Gardening Association’s indication that 35% of U.S. households grow fruits, vegetables, or herbs, and by the U.K.’s high hobby participation, where 42% of residents garden regularly. These behaviors sustain repeat purchases across pruners, trowels, weeders, and digging tools, with replacement cycles tightening as users trade up to longer-life products.

The supply side is shaped by steel and aluminum price volatility, regional forging capacity, and rising requirements for durability and ergonomics. Manufacturers are shifting toward higher-grade alloys, corrosion-resistant finishes, and composite or certified wood handles to reduce breakage and returns. Regulatory pressure reinforces these moves. Product safety and chemical regimes, including EU REACH restrictions and tighter rules around certain surface treatments, increase testing and compliance costs and encourage reformulation of coatings and lubricants. Sustainability standards also influence sourcing, as retailers push traceability and certified materials in premium lines. Key risks include inflation-driven downtrading, weather variability that disrupts seasonal demand, and trade frictions that can raise landed costs for metal components and finished tools.

Technology is now a competitive lever across both manufacturing and go-to-market. Automation improves consistency in forging, heat treatment, and sharpening, while sensor-based quality inspection reduces defect rates. AI-enabled demand forecasting and dynamic replenishment help balance inventory across spring peaks, supporting service levels in big-box and online channels. Digital commerce continues to take share, with online and marketplace-led sales plausibly reaching about 35% of category revenue by 2034 as consumers compare specifications and reviews across brands.

Regionally, North America is expected to remain a high-value market at roughly 32% share, supported by DIY culture and premiumization. Europe should sustain about 28% share, with stronger pull for eco-labeled products and ergonomic designs. Asia-Pacific is positioned as the primary growth engine at roughly 30% share, led by urban gardening and expanding middle-class participation; India, Southeast Asia, and selected Tier-1 Chinese city clusters stand out as investment hotspots for compact tool sets, micro-gardening formats, and localized manufacturing partnerships.

, By Distribution Channel (Home Centers, Specialty Stores, Retailers, E-commerce Platforms), By End-User (Residential, Commercial Landscaping, Public Parks), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market expands from 86.3 billion USD, 2023 to 157.5 billion USD, 2033 at 6.2%, 2026-2034.

- Segment Dominance: Lawnmowers lead the product segment with estimated: 28.0%, 2023 due to their central role in routine maintenance.

- Segment Dominance: Home centers lead distribution with estimated: 44.0%, 2023 as shoppers consolidate purchases in one-stop retail formats.

- Driver: Residential gardening lifts tool demand, with residential end-users holding estimated: 62.0%, 2023 as households increase home cultivation activities.

- Restraint: Raw material and freight volatility pressures margins, with estimated: 8.0%, 2024 cost inflation risk affecting metal components and logistics.

- Opportunity: Urban and indoor gardening supports premium and compact tool adoption, with estimated: 4.0 billion USD, 2024 incremental revenue potential from ergonomics and space-saving formats.

- Trend: Brands accelerate digitalization and precision manufacturing, with estimated: 35.0%, 2024 online channel penetration driven by product comparison and replenishment convenience.

- Regional Analysis: North America leads with 36.7%, 2023 share and 31.7 billion USD, 2023 value as home gardening remains highly prevalent.

Competitive Landscape

The Global Gardening Hand Tools Market is moderately fragmented, with the top five manufacturers accounting for an estimated 28.0%–35.0% of 2025 market revenue. Competition is brand-driven and distribution-led, with product durability, ergonomic design, pricing, and retail presence shaping market share more than pure technological differentiation. Competitive intensity increased in 2025–2026 as companies expanded e-commerce channels, introduced sustainable materials, and strengthened DIY and home gardening product lines, reflecting growing consumer interest in gardening and outdoor activities.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| FISKARS GROUP | Finland | Leader | Pruners, shears, axes, and ergonomic gardening tools | Europe, North America | Expanded sustainable product lines and recycled-material tools portfolio in 2025. |

| STANLEY BLACK & DECKER | US | Leader | Hand tools including garden tools under multiple brands | North America, Global retail | Strengthened retail partnerships and expanded DIY gardening tool offerings in 2025. |

| HUSQVARNA GROUP | Sweden | Leader | Premium gardening tools and outdoor equipment | Europe, North America | Expanded battery-powered and ergonomic gardening tools segment in 2025. |

| AMES COMPANIES | US | Leader | Shovels, rakes, and lawn & garden hand tools | North America | Invested in supply chain and expanded big-box retail distribution in 2025. |

| TRUPER | Mexico | Leader | Wide range of affordable gardening hand tools | Latin America, North America | Expanded manufacturing capacity and export distribution in 2025. |

| WOLF-GARTEN (MTD) | Germany | Challenger | Interchangeable multi-head gardening tools | Europe | Strengthened modular tool systems and European dealer network in 2025. |

| SPEAR & JACKSON | UK | Challenger | Traditional and premium gardening hand tools | Europe, Commonwealth markets | Focused on heritage branding and expanded online sales channels in 2025. |

| CORONA TOOLS | US | Challenger | Professional pruning and cutting tools | North America | Expanded professional-grade tool offerings and contractor channels in 2025. |

| BAHCO (SNA EUROPE) | Sweden | Niche Player | Professional-grade cutting and pruning tools | Europe | Strengthened industrial and professional landscaping segments in 2025. |

| WORTH GARDEN | China | Niche Player | Value-focused gardening hand tools | Asia-Pacific, Global exports | Expanded e-commerce presence and private-label partnerships in 2025. |

Summary Insight:

The market is shifting toward ergonomic, durable, and eco-friendly gardening tools, with increasing importance of e-commerce distribution and private-label manufacturing. Companies with strong retail networks, brand recognition, and sustainable product innovation are gaining share, while smaller players compete on price and regional distribution through 2034.

By Type

Lawn mowers account for the largest share of the gardening tools market in 2025, representing an estimated 38 to 40 percent of total revenue. Their position reflects the ongoing need for regular lawn maintenance across residential properties, commercial landscapes, and public green spaces. In North America and Europe, lawn ownership rates exceed 60 percent of households, which sustains steady replacement demand and supports sales of electric and battery-powered models. Commercial landscaping firms also rely on high-capacity mowers to manage large surface areas efficiently.

Handheld power tools form the second major category, led by hedge trimmers, leaf blowers, and chainsaws. This segment benefits from rising adoption of cordless tools, with battery-powered models estimated to represent over 55 percent of handheld power tool sales in 2025. Hand tools and wheeled implements remain essential for soil preparation, planting, and weeding. These products maintain stable volumes due to their low cost and long service life. Water equipment, including hoses and sprinklers, supports recurring demand driven by climate variability and growing emphasis on efficient irrigation.

By Application

Garden maintenance remains the primary application area, accounting for more than half of total tool usage in 2025. Routine tasks such as mowing, trimming, pruning, and debris removal drive consistent purchasing cycles, particularly in suburban residential zones. Public parks and institutional landscapes also contribute stable demand due to scheduled maintenance requirements and municipal spending on green infrastructure.

Decorative and functional landscaping applications show faster growth. Pavers, retaining walls, and structured garden layouts increase the need for precision tools, compact wheeled implements, and cutting equipment. Urban households increasingly invest in balcony gardens and small yards, which supports demand for lightweight and space-efficient tools. This shift favors ergonomic designs and multipurpose products suited to limited outdoor areas.

By End-Use

Residential users represent the dominant end-use segment, contributing an estimated 62 percent of global revenue in 2025. Rising participation in home gardening supports this trend. In the United States, more than one-third of households grow food crops, while hobby gardening participation in Western Europe remains above 40 percent. Gardening also aligns with wellness and cost-saving priorities, reinforcing tool purchases across income groups.

Commercial end users include landscaping contractors, sports facilities, hospitality properties, and public authorities. Although smaller in volume, this segment generates higher average selling prices due to demand for durable and high-output equipment. Commercial buyers prioritize reliability and service support, which drives demand for professional-grade tools and long-term supplier relationships.

By Region

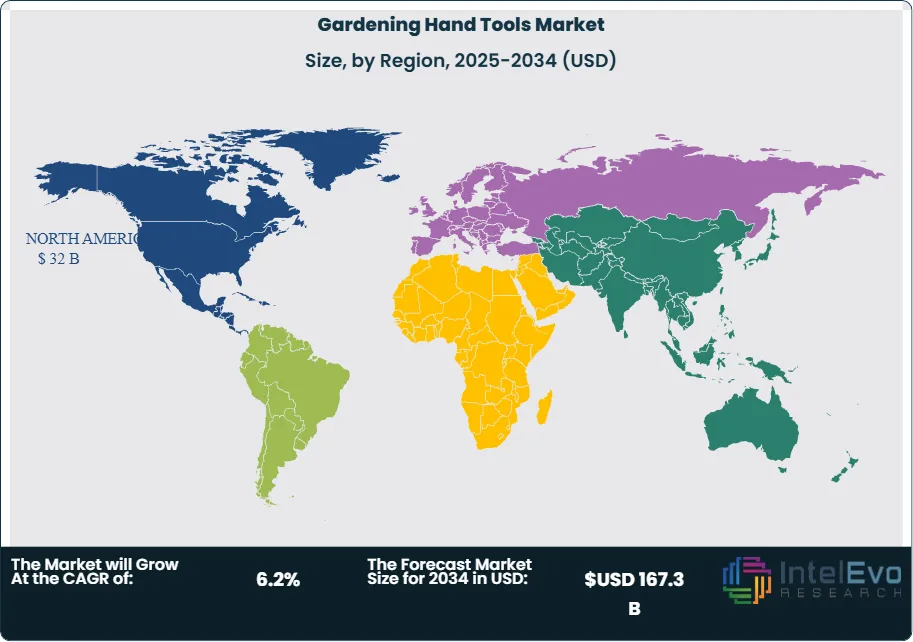

North America leads the global market with a 36.7 percent share in 2025, equivalent to approximately USD 32 billion in annual revenue. Strong retail penetration, high disposable income, and a mature DIY culture support continued dominance. Europe follows with a sizable share driven by urban gardening and established horticultural practices in Germany, the United Kingdom, and France.

Asia Pacific records the fastest growth rate, supported by urbanization, rising middle-class income, and increasing home ownership in China and India. Market expansion in this region exceeds 7 percent annually. Latin America shows steady progress, led by Brazil and Argentina, while the Middle East and Africa benefit from urban landscaping projects and public investment in green spaces.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Lawn Mowers

- Handheld Power Tools

- Lawn Mowers

- Chainsaws

- Hedge Trimmers

- Leaf Blowers

- Hand Tools & Wheeled Implements

- Long Handled Tools

- Short-Hand Tools

- Cutting & Pruning Tools

- Striking Tools

- Wheeled Implements

- Digging Tools

- Water Equipment

- Garden Hoses

- Sprinklers

- Watering Cans

By Distribution Channel

- Home Centers

- Lawn & Garden Specialty Stores

- National Retailers & Discount Stores

- Home Improvement Stores

- Hardware Stores

- E-commerce Platforms

By End User

- Residential

- Home Gardeners

- Hobby Gardeners

- Commercial

- Landscaping Contractors

- Commercial Gardens and Parks

- Sports Grounds

- Public Parks and Botanical Gardens

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 97.4 B |

| Forecast Revenue (2034) | USD 167.3 B |

| CAGR (2025-2034) | 6.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Lawn Mowers, Handheld Power Tools, Lawn Mowers, Chainsaws, Hedge Trimmers, Leaf Blowers, Hand Tools & Wheeled Implements, Long Handled Tools, Short-Hand Tools, Cutting & Pruning Tools, Striking Tools, Wheeled Implements, Digging Tools, Water Equipment, Garden Hoses, Sprinklers, Watering Cans), By Distribution Channel (Home Centers, Lawn & Garden Specialty Stores, National Retailers & Discount Stores, Home Improvement Stores, Hardware Stores, E-commerce Platforms), By End User (Residential, (Home Gardeners, Hobby Gardeners), Commercial, (Landscaping Contractors, Commercial Gardens and Parks, Sports Grounds, Public Parks and Botanical Gardens)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Stanley Black & Decker, Spear & Jackson, Bosch, Husqvarna Group, Falcon Garden Tools, Fiskars Group, STIHL, Wolf-Garten, The Ames Companies, Inc., Bulldog Tools Ltd., DeWalt, True Temper, Gardena, FELCO |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Home Centers, Specialty Stores, Retailers, E-commerce Platforms), By End-User (Residential, Commercial Landscaping, Public Parks), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Distribution Channel (Home Centers, Specialty Stores, Retailers, E-commerce Platforms), By End-User (Residential, Commercial Landscaping, Public Parks), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Distribution Channel (Home Centers, Specialty Stores, Retailers, E-commerce Platforms), By End-User (Residential, Commercial Landscaping, Public Parks), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Gardening Hand Tools Market?

The Global Gardening Hand Tools Market was valued at USD 97.4 Billion in 2025, projected to hit USD 167.3 Billion by 2034, growing at a CAGR of 6.2% from 2026–2034, driven by rising home gardening trends, urban landscaping, and demand for ergonomic, sustainable tools.

Who are the major players in the Gardening Hand Tools Market?

Stanley Black & Decker, Spear & Jackson, Bosch, Husqvarna Group, Falcon Garden Tools, Fiskars Group, STIHL, Wolf-Garten, The Ames Companies, Inc., Bulldog Tools Ltd., DeWalt, True Temper, Gardena, FELCO

Which segments covered the Gardening Hand Tools Market?

By Product Type (Lawn Mowers, Handheld Power Tools, Lawn Mowers, Chainsaws, Hedge Trimmers, Leaf Blowers, Hand Tools & Wheeled Implements, Long Handled Tools, Short-Hand Tools, Cutting & Pruning Tools, Striking Tools, Wheeled Implements, Digging Tools, Water Equipment, Garden Hoses, Sprinklers, Watering Cans), By Distribution Channel (Home Centers, Lawn & Garden Specialty Stores, National Retailers & Discount Stores, Home Improvement Stores, Hardware Stores, E-commerce Platforms), By End User (Residential, (Home Gardeners, Hobby Gardeners), Commercial, (Landscaping Contractors, Commercial Gardens and Parks, Sports Grounds, Public Parks and Botanical Gardens))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date