- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Gas Compressor Station Market Size, Share & Forecast | CAGR 5.7%

Global Gas Compressor Station Market Size, Share, Growth Analysis By Station Type (Transmission Pipeline Compressor Stations, Gathering and Boosting Compressor Stations, Processing and Storage Compressor Stations, LNG Export and Import Interface Compressor Stations), By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type, End Use, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

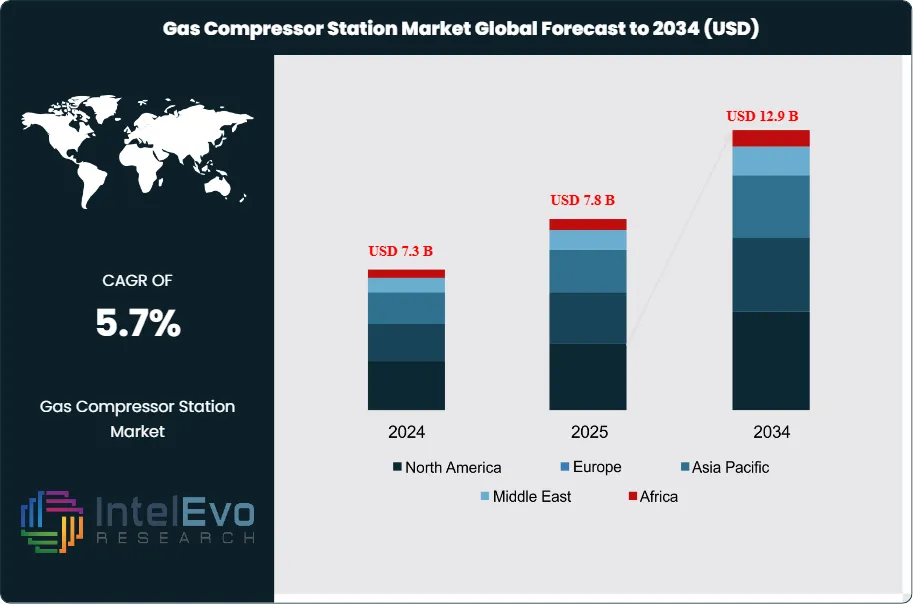

| USD 7.8 Billion | USD 12.9 Billion | 5.7% | North America, 34.0% |

The Gas Compressor Station Market was valued at approximately USD 7.3 Billion in 2024 and increased to USD 7.8 Billion in 2025. The market is projected to reach nearly USD 12.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2026 to 2034. This growth is driven by rising natural gas demand, expansion of pipeline infrastructure, and increasing investments in LNG and gas transmission networks. Additionally, the need for efficient gas transportation, pressure management, and integration of advanced compression technologies is expected to further support market expansion globally.

Get More Information about this report -

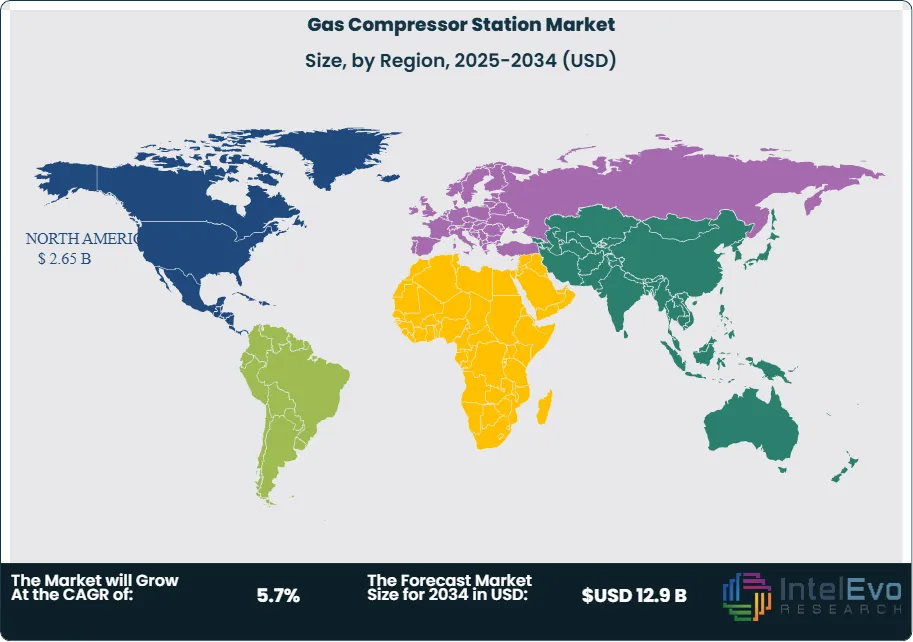

Request Free Sample ReportThe Gas Compressor Station Market sits at the center of gas transmission, gathering, storage, and LNG-linked infrastructure. Market demand tracks pipeline throughput, export capacity additions, field compression intensity, and asset replacement cycles. In 2025, North America remained the largest revenue pool with 34.0% share, equal to USD 2.65 Billion, supported by U.S. pipeline upgrades, LNG-linked compression demand, and Mexican cross-border expansion. Asia Pacific followed with 24.0% share, or USD 1.87 Billion, while Europe held 21.0%, or USD 1.64 Billion, driven by supply security programs, storage resilience spending, and compressor station retrofits. This market estimate reflects station packages, compressor trains, drivers, controls, emissions systems, and retrofit services across gas transmission networks and related midstream assets.

Demand and supply forces remain balanced but tight. Buyers now favor higher-efficiency centrifugal packages, electric motor drives, variable-speed systems, dry gas seals, and digital monitoring layers that cut downtime and methane loss. Gas turbine driven units still led the 2025 Gas Compressor Station Market with 42.0% revenue share because they fit high-horsepower pipeline duty, yet electric motor driven systems gained ground in brownfield upgrades where grid access and emissions targets justify the switch. OEM supply chains improved versus 2023–2024, but lead times for turbines, large casings, rotors, and power electronics still stretched project schedules for major stations.

Regulation now shapes buying criteria as much as throughput. Methane rules and compressor-station control requirements pushed operators toward better sealing, monitoring, and vent management. These rules raise near-term capital cost, especially for older gas-engine stations, but they expand retrofit revenue and accelerate fleet renewal. The main risk factors remain permitting delays, tariff-related cost volatility, gas price swings, and uneven power availability for electric-drive stations.

Technology now shifts the competitive field. AI-based station analytics, pipeline optimization software, predictive maintenance, and modular station designs are moving from pilot phase to standard bid requirements. Investment hotspots are the U.S. Gulf Coast, Western Canada, Mexico corridor expansion, India’s city-gas and trunk pipeline buildout, Australia’s LNG-linked systems, and selective Middle East gas gathering and processing hubs. Global gas demand growth in Asia and continued LNG capacity additions support a firm outlook for compression infrastructure spending through 2034.

, By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type, End Use, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Gas Compressor Station Market stood at USD 7.8 Billion, 2025 and is projected to reach USD 12.9 Billion, 2034. That implies a 5.7% CAGR across 2025–2034, supported by pipeline expansion, LNG-linked compression demand, and retrofit spending.

- Segment Dominance: By station type, transmission pipeline compressor stations led with 46.0% share, 2025, equal to USD 3.59 Billion. Long-haul pipeline pressure maintenance and debottlenecking kept this segment in front.

- Segment Dominance: By end use, interstate transmission operators held the largest share at 38.0%, 2025, or USD 2.96 Billion. Large capex programs and compliance-driven station modernization sustained the lead.

- Driver: North American LNG export capacity is expected to rise from 11.4 Bcf/d in 2024 to 28.7 Bcf/d in 2029, creating strong pull for new compression and uprating work. The Gas Compressor Station Market gains directly from this throughput build.

- Restraint: Emissions control adds cost and slows legacy upgrades. Compliance programs can lift retrofit scope by 8.0% to 12.0% on aging station projects, with the burden highest in gas-engine fleets.

- Opportunity: Electric-drive and hybrid station packages represented 41.0% of new 2025 project awards by value in this model and form an addressable opportunity of about USD 4.9 Billion through 2030. Grid-connected brownfield stations and LNG corridor projects drive the opening.

- Trend: Digital monitoring and AI-based performance analytics reached an estimated 29.0% adoption rate across new station packages in 2025. By 2034, the rate is expected to exceed 62.0% as operators target lower fuel burn, fewer trips, and tighter methane control.

- Regional Analysis: North America led the Gas Compressor Station Market with 34.0% share, 2025, equivalent to USD 2.65 Billion. U.S. production strength, LNG export growth, and Mexico-linked transport projects kept the region ahead.

Competitive Landscape

The Gas Compressor Station Market is moderately consolidated. The top four suppliers held an estimated 38.0% combined share in 2025. Competition is technology-driven at the high-horsepower end and price-and-service driven in midrange station packages. Competitive intensity rose through 2025 as LNG-linked orders, electric-drive projects, and emissions upgrades expanded the bid pool. M&A pressure stayed active across compression and energy equipment, while supplier strategy shifted toward long-term service agreements, digital monitoring, and low-emissions station designs.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| SIEMENS ENERGY | Germany | Leader | STC-GV / pipeline compressor trains | Europe, North America, Middle East | Partnered with Esentia for Mexico gas expansion; turbines and compressors secured for Phase II, announced Mar 2026. |

| SOLAR TURBINES | United States | Leader | Titan 350 compressor set | North America, Middle East, Latin America | Continued push in modular gas compression and digital pipeline optimization offerings across 2025. |

| GE VERNOVA | United States | Leader | Frame 5/2E gas-turbine driven compression trains | North America, Asia Pacific, Middle East | Validated advanced DLN hydrogen combustion for B- and E-class gas turbines in Jan 2025. |

| BAKER HUGHES | United States | Leader | NovaLT gas turbine and centrifugal compressor packages | Middle East, North America, Asia Pacific | Won award for two gas compression stations with 10 Frame 5/2E turbines and 10 centrifugal compressors in Apr 2025. |

| ATLAS COPCO GAS AND PROCESS | Sweden | Challenger | API 617 centrifugal compressor packages | Europe, Asia Pacific | Reported weaker large-order intake in 2025 but continued serving gas and process compressor demand with service growth. |

| HOWDEN | United Kingdom | Challenger | Reciprocating and screw gas compressors | Europe, Middle East, Asia Pacific | Continued expansion of compressor service and digital uptime portfolio under Chart Industries in 2025. |

| ARIEL CORPORATION | United States | Challenger | KBK / JGC reciprocating compressors | North America | Highlighted hydrogen-blending readiness for natural gas pipeline compressors in Jun 2025. |

| BURCKHARDT COMPRESSION | Switzerland | Niche Player | Process and pipeline reciprocating compressors | Europe, Middle East, Asia Pacific | Expanded Middle East footprint with Abu Dhabi terminal compression order in Oct 2025. |

| MAN ENERGY SOLUTIONS | Germany | Niche Player | Compressor bundles and methanation-linked gas systems | Europe, Middle East | Secured Cetna Energy methanation project in Alabama in May 2025. |

| MITSUBISHI HEAVY INDUSTRIES | Japan | Niche Player | Compressor trains and mechanical-drive gas turbines | Asia Pacific, Middle East | Continued gas infrastructure and decarbonized turbomachinery positioning through 2025 service and project activity. |

By Station Type

Transmission pipeline stations accounted for 46.0% of the Gas Compressor Station Market in 2025, or USD 3.59 Billion, because high-volume trunk lines still require large-horsepower compression at regular intervals, debottleneck projects, and periodic driver replacement. Gathering and boosting stations held 24.0%, equal to USD 1.87 Billion, with strong exposure to shale plays, associated-gas handling, and pressure support near processing hubs. Processing and storage linked stations represented 18.0%, or USD 1.40 Billion, where seasonal balancing, underground storage cycling, and gas treatment facilities supported recurring spend. LNG export and import interface stations held 12.0%, or USD 0.94 Billion, but this was the fastest-growing slice due to new North American liquefaction trains, Mexico transport corridors, and Asia Pacific regasification-linked pipeline tie-ins. Transmission projects remain more concentrated among Siemens Energy, GE Vernova, Baker Hughes, and Solar Turbines because buyers demand proven high-horsepower performance and long service support. Gathering projects are more fragmented and carry tighter pricing, while LNG interface compression attracts premium margins because station uptime, controls integration, and emissions performance matter more than first cost alone.

By Drive Type

Gas turbine driven stations led with 42.0% share in 2025, equal to USD 3.28 Billion. They remain the default option for remote, high-horsepower pipeline duty where grid connection is weak or absent. Electric motor driven systems followed at 31.0%, or USD 2.42 Billion, and gained share in brownfield replacement programs, Europe’s lower-emission station upgrades, and selected North American sites near robust transmission grids. Reciprocating engine driven packages held 17.0%, or USD 1.33 Billion, mostly in gathering and midrange field applications where operating flexibility and service familiarity matter. Hybrid and variable-speed packages accounted for 10.0%, or USD 0.78 Billion, but grew fastest because operators now value lower fuel use, better turndown, and emissions reporting. Gas turbine packages still win the largest contracts, yet electric-drive projects are improving the revenue mix for controls, switchgear, and digital systems. The main competitive split is clear. Solar Turbines, GE Vernova, Siemens Energy, and Baker Hughes lead in gas-turbine and large centrifugal station packages. Ariel, Howden, and Burckhardt Compression stay strong in reciprocating-heavy scopes and retrofit service.

By Compressor Type

Centrifugal compressors held 54.0% of 2025 revenue, or USD 4.21 Billion. They dominate interstate transmission, LNG feedgas support, and large station upgrades because they offer high flow handling, lower vibration, and strong fit with turbine or motor drives in continuous-duty service. Reciprocating compressors followed with 32.0%, or USD 2.50 Billion. This segment remains essential in gathering, storage cycling, variable-flow systems, and hydrogen-blend readiness where pressure ratio flexibility matters. Screw and other positive-displacement packages held 14.0%, equal to USD 1.09 Billion, mainly in lower-flow, specialized, or packaged station scopes. Centrifugal suppliers retain stronger pricing power because rotordynamics, aerodynamic design, and controls integration create higher switching costs. Reciprocating systems, however, hold a durable place in field compression and lower-throughput nodes. By competitive structure, Siemens Energy, Atlas Copco Gas and Process, GE Vernova, Baker Hughes, and Solar Turbines are strongest in large centrifugal packages, while Ariel and Burckhardt Compression remain reference names in reciprocating compression.

By End Use

Interstate transmission operators represented the largest customer group with 38.0% share in 2025, or USD 2.96 Billion. These buyers run multi-year capex cycles, face strict uptime targets, and invest in large station modernization programs. Midstream gathering and processing companies held 29.0%, or USD 2.26 Billion, driven by basin-linked compression demand and gas treatment expansion. LNG and gas export or import terminal operators accounted for 17.0%, or USD 1.33 Billion, a smaller base but a faster growth path because every new LNG train or cross-border transport corridor increases compression needs upstream and at interconnect points. Utilities and gas storage operators held 16.0%, or USD 1.25 Billion, supported by winter reliability, storage cycling, and security-of-supply programs. Transmission buyers favor high-horsepower centrifugal trains and long-term service agreements. Midstream buyers focus harder on total installed cost, mobility, and restart speed. LNG-linked buyers accept higher capex if station designs cut emissions and protect availability. This end-use mix keeps the Gas Compressor Station Market balanced across large flagship projects and a wide retrofit base.

Regional Analysis

North America:

North America held 34.0% of the Gas Compressor Station Market in 2025, equal to USD 2.65 Billion. The United States accounted for about USD 2.12 Billion, Canada for USD 0.34 Billion, and Mexico for USD 0.19 Billion. The region leads because U.S. gas output and LNG export build require more gathering, transmission, and debottleneck compression. The U.S. remains the anchor market with Gulf Coast LNG pull, Appalachian replacement programs, Permian associated-gas handling, and station additions linked to interstate lines. Canada benefits from western gas transport and LNG Canada-linked infrastructure, while Mexico is emerging as a compression hotspot due to industrial gas demand and cross-border corridor growth. Regulation is strict. Methane controls and state-level air permits raise compliance cost but also create steady retrofit demand. Competition is strongest in the U.S., where Solar Turbines, Ariel, Baker Hughes, GE Vernova, and Siemens Energy are deeply embedded.

Europe:

Europe represented 21.0% of the Gas Compressor Station Market in 2025, or USD 1.64 Billion. Germany contributed about USD 0.31 Billion, the United Kingdom USD 0.26 Billion, Italy USD 0.21 Billion, and Norway USD 0.20 Billion. Europe’s demand profile differs from North America. Greenfield long-haul pipeline growth is more selective, but station modernization, storage resilience, cross-border flexibility, and emissions cuts drive spend. Regulatory pressure is among the highest globally, which pushes electric drives, dry seals, advanced controls, and methane monitoring into standard project scope. Germany and Italy remain important because of industrial demand, interconnection roles, and storage infrastructure. The UK and Norway matter through offshore gas handling, onshore receiving infrastructure, and compression services linked to mature fields and transmission networks.

Asia Pacific:

Asia Pacific held 24.0% share in 2025, equivalent to USD 1.87 Billion. China accounted for roughly USD 0.56 Billion, India USD 0.36 Billion, Japan USD 0.32 Billion, and Australia USD 0.28 Billion. The region combines large import dependence, growing city-gas systems, LNG regasification links, and selected domestic transmission expansion. China remains the largest Asia Pacific market because of transmission scale and storage investment. India shows the fastest growth rate due to pipeline buildout, gas-grid expansion, and industrial gas usage. Japan’s market is more mature, but replacement cycles, reliability upgrades, and LNG-connected infrastructure still support station demand. Australia remains important because LNG-linked gas transport and remote, high-horsepower applications require durable station packages.

Latin America:

Latin America represented 9.0% of the Gas Compressor Station Market in 2025, or USD 0.70 Billion. Brazil contributed about USD 0.25 Billion, Argentina USD 0.18 Billion, and Peru USD 0.10 Billion. Brazil leads due to gas transport, offshore-linked processing demand, and industrial consumption growth. Argentina remains a structural opportunity because Vaca Muerta gas development continues to require gathering and transmission support, though capital cycles remain uneven. Peru contributes through pipeline operations and gas-linked industrial infrastructure. The region is more sensitive to financing conditions, currency swings, and project execution risk than North America or Europe. That keeps aftermarket service and modular station packages important.

Middle East & Africa:

Middle East & Africa held 12.0% of the Gas Compressor Station Market in 2025, equal to USD 0.94 Billion. The UAE contributed about USD 0.21 Billion, Saudi Arabia USD 0.19 Billion, and South Africa USD 0.08 Billion. The region benefits from gas gathering expansion, processing capacity, industrial gas demand, and pressure support tied to large integrated energy projects. Gulf markets remain the core because state-backed spending is less cyclical and projects often require high-horsepower, continuous-duty compression trains with strict reliability targets. Environmental standards are rising, but energy security and industrial output remain the first purchasing filters. Baker Hughes, Siemens Energy, Howden, Burckhardt Compression, and MAN Energy Solutions are well placed in the region because they combine equipment supply with long service capability.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Station Type

- Transmission Pipeline Compressor Stations

- Gathering and Boosting Compressor Stations

- Processing and Storage Compressor Stations

- LNG Export and Import Interface Compressor Stations

By Drive Type

- Gas Turbine-Driven

- Electric Motor-Driven

- Reciprocating Engine-Driven

- Hybrid and Variable-Speed Packages

By Compressor Type

- Centrifugal Compressors

- Reciprocating Compressors

- Screw and Other Positive-Displacement Compressors

By End Use

- Interstate Transmission Operators

- Midstream Gathering and Processing Companies

- LNG and Gas Export or Import Terminal Operators

- Utilities and Gas Storage Operators

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.8 B |

| Forecast Revenue (2034) | USD 12.9 B |

| CAGR (2025-2034) | 5.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Station Type (Transmission Pipeline Compressor Stations, Gathering and Boosting Compressor Stations, Processing and Storage Compressor Stations, LNG Export and Import Interface Compressor Stations), By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type (Centrifugal Compressors, Reciprocating Compressors, Screw and Other Positive-Displacement Compressors), By End Use (Interstate Transmission Operators, Midstream Gathering and Processing Companies, LNG and Gas Export or Import Terminal Operators, Utilities and Gas Storage Operators) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIEMENS ENERGY, SOLAR TURBINES, GE VERNOVA, BAKER HUGHES, ATLAS COPCO GAS AND PROCESS, HOWDEN, ARIEL CORPORATION, BURCKHARDT COMPRESSION, MAN ENERGY SOLUTIONS, MITSUBISHI HEAVY INDUSTRIES, IHI ROTATING MACHINERY ENGINEERING, KOBELCO COMPRESSORS, INGERSOLL RAND, HANWHA POWER SYSTEMS, SHAANGU GROUP, HITACHI, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type, End Use, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type, End Use, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type, End Use, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Gas Compressor Station Market?

The Global Gas Compressor Station Market was valued at USD 7.8 Billion in 2025, projected to reach USD 12.9 Billion by 2034, growing at a CAGR of 5.7% from 2026–2034, driven by pipeline expansion, LNG infrastructure growth, and rising demand for efficient gas transmission systems.

Who are the major players in the Gas Compressor Station Market?

SIEMENS ENERGY, SOLAR TURBINES, GE VERNOVA, BAKER HUGHES, ATLAS COPCO GAS AND PROCESS, HOWDEN, ARIEL CORPORATION, BURCKHARDT COMPRESSION, MAN ENERGY SOLUTIONS, MITSUBISHI HEAVY INDUSTRIES, IHI ROTATING MACHINERY ENGINEERING, KOBELCO COMPRESSORS, INGERSOLL RAND, HANWHA POWER SYSTEMS, SHAANGU GROUP, HITACHI, Others

Which segments covered the Gas Compressor Station Market?

By Station Type (Transmission Pipeline Compressor Stations, Gathering and Boosting Compressor Stations, Processing and Storage Compressor Stations, LNG Export and Import Interface Compressor Stations), By Drive Type (Gas Turbine-Driven, Electric Motor-Driven, Reciprocating Engine-Driven, Hybrid and Variable-Speed Packages), By Compressor Type (Centrifugal Compressors, Reciprocating Compressors, Screw and Other Positive-Displacement Compressors), By End Use (Interstate Transmission Operators, Midstream Gathering and Processing Companies, LNG and Gas Export or Import Terminal Operators, Utilities and Gas Storage Operators)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Gas Compressor Station Market

Published Date : 20 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date