- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Gas Cylinder Market Size 2034 Global Growth & Trends| 6.0% CAGR

Global Gas Cylinder Market Size, Share & Analysis By Material (Steel, Aluminium, Composites, Others), By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial), Safety Regulations, Distribution Network, Competitive Analysis & Forecast 2025–2034

Report Overview

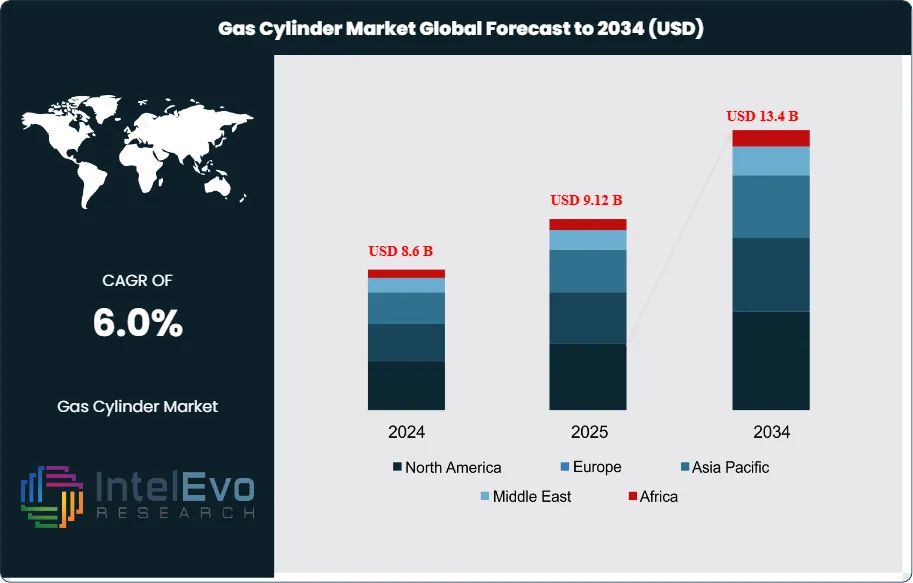

The Gas Cylinder Market is estimated at USD 8.6 billion in 2024 and is on track to reach roughly USD 13.4 billion by 2034, implying a compound annual growth rate of 6.0% over 2024–2034. Demand has historically been anchored in household LPG, medical oxygen, and industrial gases, with unit volumes steadily expanding as governments replace biomass and kerosene with cleaner fuels and as healthcare systems strengthen oxygen security. The market’s size evolution reflects this policy momentum: Asia–Pacific already accounts for 46.4% of global revenues, underpinned by rapid consumer adoption and industrialization, while multi-year programs have widened affordability and last-mile access. India’s LPG consumption alone rose more than 84%—from 15.3 million tonnes in 2011–12 to 28.3 million tonnes in 2021–22—illustrating how sustained subsidies translate into cylinder penetration and refill frequency. Targeted cash transfers in Latin America (e.g., monthly vouchers of S/25 per household, totaling S/.1.36 billion by October 2022) and the distribution of 60,000 six-kilogram cylinders alongside VAT exemptions for cooking LPG further underscore the policy tailwinds. India’s Pradhan Mantri Ujjwala Yojana, covering over 90 million beneficiaries, increased its per-cylinder subsidy to ₹300 in 2024 for up to 12 refills, reinforcing demand elasticity at the base of the pyramid.

Get More Information about this report -

Request Free Sample ReportGrowth drivers over the forecast horizon include accelerated clean-cooking transitions in South and Southeast Asia and parts of Africa; post-pandemic resilience in medical oxygen infrastructure; and industrial demand from metals, fabrication, and specialty gases. On the supply side, manufacturers benefit from scale in cylinder fabrication, automated testing, and globalized valve and regulator supply chains. Key challenges persist: input-material volatility (steel and aluminum), safety and recertification compliance costs, counterfeiting risks in informal resale markets, and distribution inefficiencies in remote geographies. Regulatory tightening—covering design codes, periodic inspection, and traceability—raises barriers to entry but supports long-term quality and brand consolidation.

Technology is reshaping adoption. Lightweight composite cylinders (often 30–50% lower tare weight than steel) improve safety and ergonomics for rural users; RFID/IoT tagging and smart valves enhance asset tracking, anti-pilferage, and predictive maintenance; AI-enabled routing optimizes last-mile delivery and refill logistics; and automated filling lines raise throughput and consistency. Regionally, Asia–Pacific will remain the anchor of absolute growth, with South Asia as the largest volume opportunity and Southeast Asia as a fast-follower. Investment hotspots to watch include Africa’s emerging clean-cooking initiatives, Latin America’s targeted subsidy frameworks, and Europe’s specialty and hydrogen-ready cylinder niches, collectively shaping a stable, policy-backed growth trajectory through 2034.

, By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial), Safety Regulations, Distribution Network, Competitive Analysis & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global gas cylinder market is projected to expand from USD 7.6 billion in 2024 to USD 13.4 billion by 2034, reflecting a 6.0% CAGR (2025–2034), underpinned by clean-cooking programs, industrial gas demand, and resilient medical oxygen infrastructure.

- Material: Steel cylinders lead with a 64.5% revenue share due to lower cost, established codes, and high-pressure ratings; however, composite cylinders, which are typically 30–50% lighter, are gaining share in consumer and healthcare segments on safety and ergonomics.

- Application: Liquefied gases (primarily LPG) account for 52.4% of demand, sustained by household and small-business refills as governments subsidize clean cooking and expand last-mile distribution.

- Capacity: 10–50 kg formats hold 37.1% share, balancing portability with refill economics for household clusters, micro-enterprises, and field industrial uses.

- Driver: Policy support is a decisive catalyst—industrial end-use already contributes 42.2% of market revenues, while clean-cooking subsidies (e.g., India’s PMUY at ₹300 per 14.2-kg refill and Latin American voucher programs) have lifted LPG adoption and refill frequency.

- Restraint: Input-material volatility and compliance costs weigh on margins; steel price swings can materially affect cylinder ASPs, while mandatory inspection/recertification cycles (often every 5 years) add recurring OPEX and downtime, especially for small distributors.

- Opportunity: A USD 4.8 billion incremental pool opens through 2034; if composites capture even +5 percentage points of share from steel by 2034, that shift alone would reallocate roughly USD 620 million of annual revenue toward higher-value lightweight designs.

- Trend: Digitization is scaling fast—RFID/IoT-tagged cylinders enable asset traceability and anti-pilferage, and route optimization/automated filling lines are reducing delivery and turnaround costs, supporting higher refill throughput and improved safety performance.

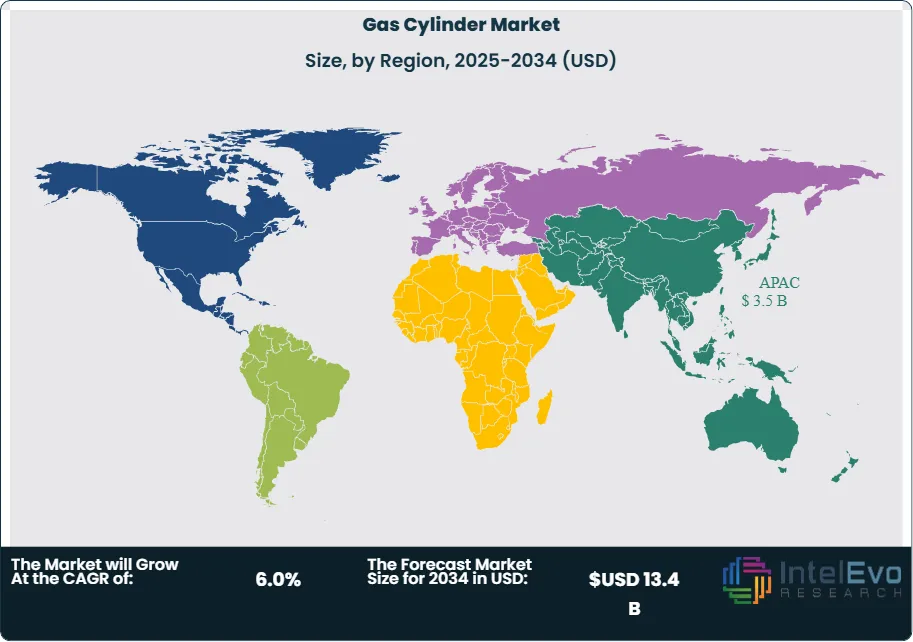

- Regional Analysis: Asia–Pacific is the demand anchor at approximately USD 3.5 billion in 2024 (≈46% share), led by South and Southeast Asia’s clean-cooking transitions and industrialization; Latin America remains subsidy-driven and Africa is emerging as the next clean-cooking hotspot, while Europe skews toward specialty and hydrogen-ready cylinders.

Material Analysis

Steel remains the reference material in 2025, accounting for roughly 64.5% of installed cylinder revenues. Its dominance reflects a superior cost-to-pressure ratio, broad code acceptance (ISO/EN/DOT), and proven performance in high-pressure service for LPG, oxygen, nitrogen, and industrial mixes. High recyclability also aligns steel with tightening stewardship and end-of-life mandates, supporting procurement in industrial, healthcare, and municipal contracts.

Aluminium and advanced composites are, however, capturing incremental share in weight-sensitive use cases. Aluminium’s corrosion resistance and clean internal finish suit medical and beverage gases, while Type III/IV composites deliver 30–50% lower tare weight, reducing handling risk and last-mile costs in residential LPG and home-care oxygen. As AI-enabled route planning and IoT tracking scale, the economics of lighter, traceable assets improve; the resulting shift is expected to move several share points from steel to composites through 2030–2034, particularly in retail LPG and mobility pilots.

Capacity Analysis

The 10–50 kg band remains the workhorse of the market with about 37.1% share, balancing refill economics and portability. This format underpins household and micro-enterprise LPG use and supports field operations in hospitality, light fabrication, and construction where manual handling and rapid swap-outs are critical. Distributors favor this range for higher asset turns and better truck utilization.

Sub-10 kg packs are expanding with clean-cooking programs and last-mile delivery platforms, offering safer alternatives to biomass in peri-urban and rural settings. At the other end, 50–100 kg and >100 kg formats anchor industrial consumption—cutting/welding shops, chemical dosing, and water treatment—where stationary storage and manifolded banks dominate and price sensitivity to steel and valve components is highest. Across tiers, compliance (hydrostatic tests, periodic inspection) and improved valve/OPD designs are raising safety while preserving uptime.

Application Analysis

Liquefied gases lead with an estimated 52.4% share in 2025, propelled by LPG for cooking and commercial energy, and CO₂/N₂O in food, beverage, and medical applications. Growth is reinforced by subsidy frameworks, VAT relief in select markets, and expanding cold-chain and carbonation demand, which prefer standardized cylinders and well-developed exchange networks.

Non-liquefied (compressed) gases—oxygen, nitrogen, argon—remain essential to hospitals and fabrication shops, benefiting from post-pandemic oxygen infrastructure and ongoing manufacturing recovery. Dissolved gases, led by acetylene for welding, constitute a smaller but resilient niche; innovations in porous mass and safety valves continue to reduce incident rates and insurance costs, protecting share despite slower volume growth.

End-use Analysis

Industrial users account for roughly 42.2% of 2025 consumption, underwritten by metals fabrication (O₂/Ar/CO₂ blends), chemicals and petrochemicals (N₂ blanketing, specialty gases), and water treatment (chlorination/ozonation). Capital projects and infrastructure upgrades in emerging markets sustain multi-year demand visibility, while strict plant safety audits favor certified suppliers and drive replacement of legacy assets.

Residential and commercial segments grow on the back of LPG penetration and small-format refills for restaurants and small industries. Healthcare maintains elevated baseline demand for medical oxygen and specialty gases, with hospitals specifying lighter cylinders and integrated regulators to reduce manual-handling risk. In transportation, early hydrogen mobility and composite cylinder adoption in fleets and aerospace ground support remain pilot-scale but represent the fastest structural optionality for the supply base.

Regional Analysis

Asia Pacific remains the demand anchor with a mid-40s revenue share (~46%) and an estimated value near USD 3.5 billion in 2024, extending momentum into 2025. India, Southeast Asia, and China drive volumes via clean-cooking expansion and industrialization, while localization of cylinder manufacturing and valve assembly shortens lead times and buffers FX risk.

North America and Europe are mature, compliance-intensive markets where growth is tied to asset renewal, healthcare resilience, and specialty gases. Uptake of composite cylinders and hydrogen-ready designs is most pronounced here, aided by stringent safety frameworks and decarbonization funding. Latin America and the Middle East & Africa show accelerating, subsidy-supported LPG adoption and industrial project pipelines; although smaller in absolute value, these regions offer above-market CAGRs through 2034 as distribution networks formalize and medical gas infrastructure scales.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material

- Steel

- Aluminium

- Composites

- Glass Fiber

- Carbon Fiber

- Aramid Fiber

- Others

- Others

By Capacity

- Less than 10 Kg

- 10 to 50 Kg

- 50 to 100 Kg

- Above 100 Kg

By Application

- Liquefied Gases

- Non-liquefied Gases

- Dissolved Gases

By End-use

- Industrial

- Food and Beverages

- Chemical and Petrochemicals

- Healthcare

- Oil and Gas

- Metal and Mining

- Water Treatment

- Others

- Transportation

- Automotive

- Aerospace

- Marine

- Others

- Residential

- Commercial

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 8.6 B |

| Forecast Revenue (2034) | USD 13.4 B |

| CAGR (2024-2034) | 6.0% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material (Steel, Aluminium, Composites, Others), By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Worthington Industries, Faber Industrie, 3M Company, Luxfer Gas Cylinders, Jiangsu Minsheng Heavy Industries Co., Ltd., Quantum Fuel Systems LLC., Al Aman Gas Cylinders Manufacturing, Manchester Tank, Beijing Tianhai Industrial Co., Ltd., Supreme Industries Limited, Aygaz A.Ş, Hexagon Composites, Everest Kanto Cylinder Ltd., BINA (SHANGHAI) GAS CYLINDER CO., LTD., Confidence Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial), Safety Regulations, Distribution Network, Competitive Analysis & Forecast 2025–2034")

, By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial), Safety Regulations, Distribution Network, Competitive Analysis & Forecast 2025–2034")

, By Capacity (Less than 10 Kg, 10 to 50 Kg, 50 to 100 Kg, Above 100 Kg), By Application (Liquefied Gases, Non-liquefied Gases, Dissolved Gases), By End-use (Industrial, Transportation, Residential, Commercial), Safety Regulations, Distribution Network, Competitive Analysis & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date