- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Gene Therapy Manufacturing Market Size, Share | CAGR 14.6%

Global Gene Therapy Manufacturing Market Size, Share, Analysis By Vector Type (Viral Vectors – AAV, Lentivirus, Adenovirus, Retrovirus; Plasmid DNA; Non-Viral Vectors Including Lipid Nanoparticles and Transposons), By Therapy Type (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Cardiovascular & Metabolic Diseases), By Manufacturing Mode (CDMO, In-House), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 5.8 Billion | USD 19.8 Billion | 14.6% | North America, 44.5% |

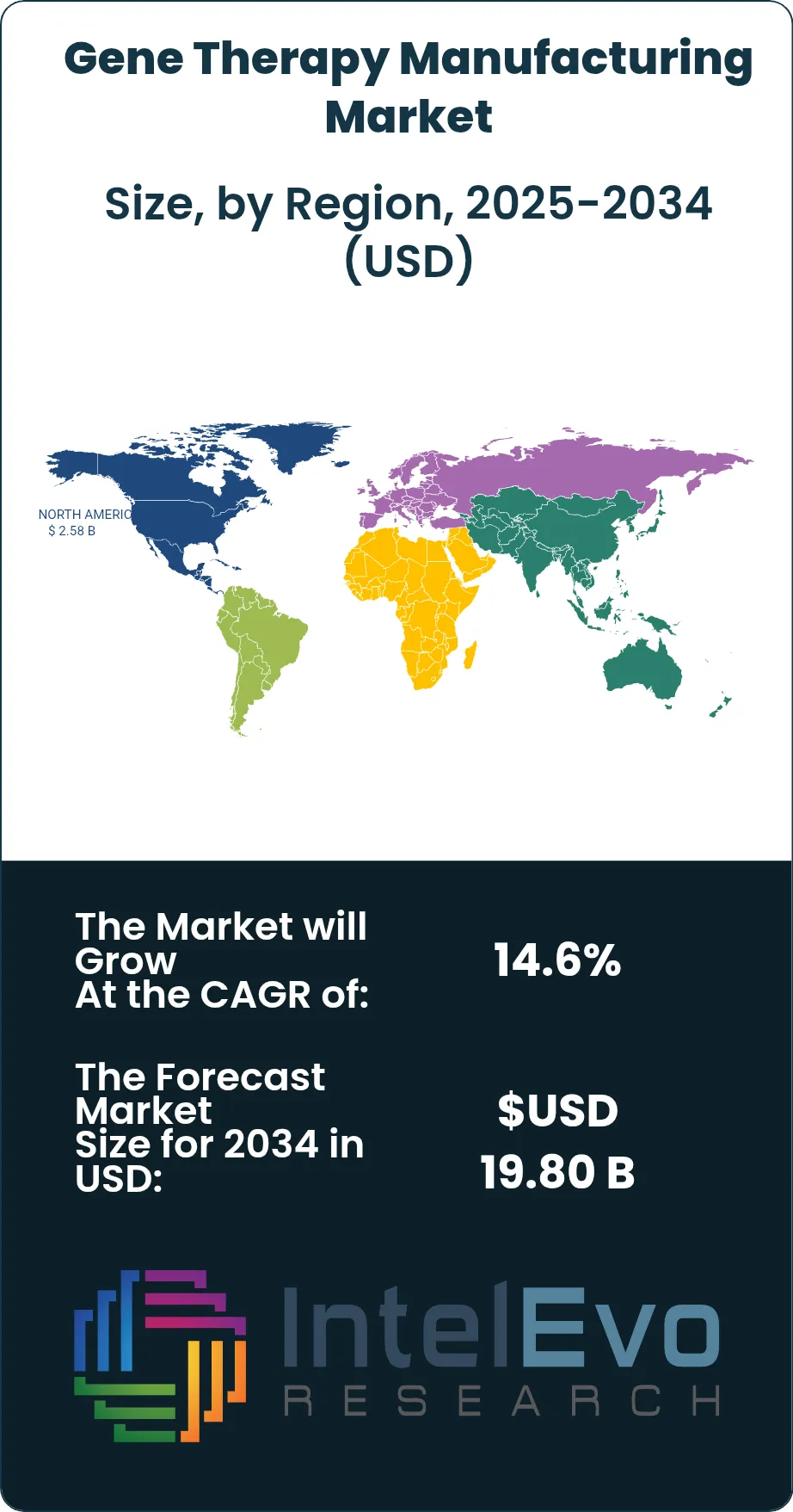

The Gene Therapy Manufacturing Market was valued at approximately USD 5.06 Billion in 2024 and reached USD 5.80 Billion in 2025. The market is projected to grow to USD 19.80 Billion by 2034, expanding at a CAGR of 14.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.0 Billion over the analysis period. The rise of the gene therapy manufacturing market reflects a structural shift in biopharmaceutical production from traditional biologics toward advanced therapy medicinal products, with viral vector capacity now ranked among the most constrained inputs in the global drug supply chain.

Get More Information about this report -

Request Free Sample ReportDemand is being pulled forward by a commercial pipeline of more than 2,000 active gene and cell therapy candidates tracked across global clinical registries, with roughly 38% in Phase II or later as of 2025. AAV and lentiviral vectors together represent the dominant modality, accounting for close to 68.5% of manufacturing output by value. Approved products in hemophilia, sickle cell disease, spinal muscular atrophy, and inherited retinal disorders have created sustained batch demand, while a deeper oncology pipeline in CAR-T and in-vivo editing is absorbing incremental capacity. FDA CBER reviewed a record volume of IND submissions for cell and gene therapies in 2024-2025, forcing developers to secure long-dated slots at specialist facilities.

On the supply side, capital deployment into GMP viral vector suites exceeded USD 3.1 Billion across 2024-2025, with new sites coming online in Maryland, North Carolina, the UK, and the Research Triangle. Regulatory pressure is also shaping the gene therapy manufacturing market. FDA guidance on potency assurance, ICH Q5A revisions on viral safety for advanced therapy products, and EMA ATMP framework updates are raising the bar on analytical and release testing. Reimbursement signals, including the CMS Cell and Gene Therapy Access Model rolling into effect for sickle cell disease, are de-risking volume forecasts for 2026-2028 launches.

Technology is reshaping cost-of-goods. Suspension-based HEK293 AAV platforms, intensified lentiviral production using stable producer cell lines, AI-enabled process analytical technology, and closed automated fill-finish systems are cutting cost per dose by an estimated 22-30% relative to adherent legacy workflows. North America leads regional activity at 44.5% of 2025 value, driven by the US CGT clinical base and aggressive CDMO expansion. Asia Pacific is the fastest-growing regional pocket, anchored by China's NMPA licensing reforms and Japan's established regenerative medicine framework.

, By Therapy Type (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Cardiovascular & Metabolic Diseases), By Manufacturing Mode (CDMO, In-House), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The gene therapy manufacturing market was valued at USD 5.8 Billion in 2025 and is projected to reach USD 19.8 Billion by 2034, expanding at a CAGR of 14.6% across the 2026-2034 forecast period.

- Segment Dominance: Viral vectors accounted for 68.5% of total manufacturing value in 2025, with AAV and lentivirus forming the core of clinical and commercial batch demand.

- Segment Dominance: Oncology applications captured 42.8% of end-use demand in 2025, underpinned by the commercial CAR-T franchise and a deepening solid tumor cell therapy pipeline.

- Driver: A global pipeline of over 2,000 active gene and cell therapy candidates, with roughly 38% in Phase II or later, is driving multi-year GMP capacity bookings and long-dated CDMO contracts.

- Restraint: Viral vector cost per dose remains in the USD 500,000-800,000 range for commercial CAR-T batches, limiting affordability and pushing payers toward outcomes-based contracts.

- Opportunity: Suspension AAV platforms and stable producer cell lines can reduce cost of goods by 22-30%, opening a USD 3.5-4.2 Billion incremental opportunity for CDMOs adopting these workflows by 2030.

- Trend: Outsourced CDMO manufacturing held 61.8% share of spend in 2025 as sponsor biotechs prioritize speed to IND over in-house vector facility construction.

- Regional Analysis: North America led the gene therapy manufacturing market in 2025 with 44.5% share and USD 2.58 Billion in revenue, driven by FDA-aligned CDMO capacity in the US Mid-Atlantic and North Carolina corridors.

Competitive Landscape Overview

The gene therapy manufacturing market is moderately consolidated at the top, with the four largest CDMO platforms accounting for an estimated 46.8% of commercial vector output in 2025. Competition is technology-driven rather than price-driven, with differentiation built on viral vector titer, suspension platform maturity, analytical release testing depth, and ability to support regulatory filings in both FDA and EMA jurisdictions. Mergers and capacity additions have intensified since 2024, including Novo Holdings' take-private of Catalent and a wave of US Mid-Atlantic and North Carolina greenfield builds. Specialist entrants focused on plasmid DNA and stable lentiviral producer cells are taking niche share in the 10-15% band.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Platform / Service | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Lonza Group | Switzerland | Leader | Cell & Gene Technologies (viral vector, cell therapy) | North America, Europe | Expanded Portsmouth viral vector suite in 2025 with added AAV capacity |

| Catalent (Novo Holdings) | United States | Leader | Maryland gene therapy network (AAV, lentiviral) | North America | Integrated into Novo Holdings portfolio in 2024, triggering CGT capacity expansion |

| Thermo Fisher Scientific | United States | Leader | Patheon Viral Vector Services | North America, Europe | Commissioned new Plainville viral vector facility in 2025 |

| WuXi Advanced Therapies | China / United States | Leader | CAR-T and viral vector CTDMO platform | Asia Pacific, North America | Expanded Philadelphia commercial lentiviral suite in 2025 |

| Charles River Laboratories | United States | Challenger | Cobra Biologics plasmid DNA and viral vector services | North America, Europe | Added pDNA capacity at Keele site in early 2025 |

| Oxford Biomedica | United Kingdom | Challenger | LentiVector enabled platform | Europe | Secured multi-year CDMO deal with a Tier 1 CAR-T developer in 2025 |

| Fujifilm Diosynth Biotechnologies | Japan / United States | Challenger | Advanced therapies manufacturing network | North America, Asia Pacific | Opened Holly Springs North Carolina CGT wing in 2025 |

| Merck KGaA (MilliporeSigma) | Germany | Challenger | Integrated viral vector and pDNA offerings | Europe, North America | Expanded Carlsbad viral vector site in 2025 to support pipeline demand |

| Samsung Biologics | South Korea | Niche Player | ADC and mRNA/CGT capabilities (Plant 5) | Asia Pacific | Announced Plant 5 CGT-enabled buildout moving to commissioning in 2026 |

| AGC Biologics | Japan / Denmark | Niche Player | Plasmid DNA and cell therapy services | Europe, North America, Asia Pacific | Doubled Longmont cell therapy footprint mid-2025 |

By Vector Type

Viral vectors dominated the gene therapy manufacturing market with 68.5% revenue share in 2025, translating to approximately USD 3.97 Billion. Within viral systems, AAV serotypes AAV2, AAV5, AAV8, and AAV9 carry the bulk of in-vivo commercial demand, while lentiviral vectors anchor ex-vivo CAR-T and stem cell programs. Yield improvement in suspension HEK293 processes has taken typical AAV titers from 1e14 vg/L range in adherent systems to 1e15 vg/L and above in intensified suspension, materially lowering cost per dose. Adenoviral platforms maintain a smaller but persistent role in oncolytic and vaccine-adjacent programs. Competition is dominated by specialist CDMOs with bioreactor scale above 2,000 liters and validated purification trains.

Plasmid DNA held 18.2% share at roughly USD 1.06 Billion in 2025. Plasmid DNA is the single most constrained raw material for viral vector production and for non-viral delivery in mRNA and DNA vaccines, which creates a structurally tight demand profile. GMP-grade pDNA capacity additions in the UK, Germany, and the US Midwest are coming online through 2026, but lead times still run 9-14 months. Non-viral vectors including lipid nanoparticles, electroporation workflows, and transposon systems contributed 13.3% at approximately USD 0.77 Billion, with rapid uptake expected as in-vivo editing programs mature and move out of viral-only delivery.

By Therapy Type

Ex-vivo gene therapy manufacturing accounted for 53.7% of market value in 2025, equivalent to USD 3.11 Billion. This category covers CAR-T, hematopoietic stem cell engineering for sickle cell disease and beta-thalassemia, and emerging allogeneic cell therapy programs. Complex vein-to-vein logistics, cryopreservation integrity, and release testing turnaround are the defining cost and quality variables. Autologous processing remains capacity-heavy, while allogeneic platforms are expanding rapidly with a view to improving slot utilization and reducing per-dose cost.

In-vivo gene therapy manufacturing contributed 46.3% of value at USD 2.69 Billion. The segment is concentrated in AAV-based systemic and targeted delivery for rare monogenic disorders, inherited retinal conditions, and neuromuscular indications. In-vivo workflows are batch-efficient compared with ex-vivo but face tighter potency, empty-to-full capsid ratio, and host cell protein specifications. Growth through 2034 will be driven by in-vivo gene editing candidates progressing from Phase II into Phase III, with multiple CRISPR, base editing, and prime editing programs expected to reach BLA-enabling stages.

By Application

Oncology applications led end-use demand with 42.8% share in 2025 at approximately USD 2.48 Billion, anchored by commercial CAR-T therapies in large B-cell lymphoma, multiple myeloma, and ALL, plus an expanding solid tumor cell therapy pipeline. Rare genetic disorders followed at 28.4% or USD 1.65 Billion, covering hemophilia A and B, spinal muscular atrophy, Duchenne muscular dystrophy, and inherited metabolic conditions. Neurological disorders captured 12.6% at USD 0.73 Billion, with AAV9-enabled CNS delivery platforms expanding into ALS, Huntington's, and select tauopathies.

Ophthalmology held 8.9% share at USD 0.52 Billion in 2025, led by AAV subretinal delivery programs for inherited retinal dystrophies and growing interest in suprachoroidal delivery for more prevalent eye conditions. Other applications, including cardiovascular, infectious disease, and metabolic indications, contributed 7.3% at USD 0.42 Billion. Oncology is expected to retain leadership through 2034, though rare disease manufacturing will grow fastest in absolute terms as approved AAV products scale and new pediatric indications reach approval.

By Mode of Manufacturing

Outsourced CDMO manufacturing accounted for 61.8% of market spend in 2025, equivalent to USD 3.58 Billion. Sponsor biotechs and mid-cap pharma continue to favor contract manufacturing to preserve capital, shorten timelines to IND, and secure regulatory precedent. Specialist CDMOs with integrated plasmid, vector, fill-finish, and analytical capabilities command premium pricing and long-dated slot commitments. In-house manufacturing held 38.2% at USD 2.22 Billion, concentrated among large pharma with commercial CGT franchises and a small group of vertically integrated biotechs that have invested in proprietary suites to control cost of goods, IP, and release testing tempo.

Regional Analysis

North America

North America led the gene therapy manufacturing market in 2025 with 44.5% share and USD 2.58 Billion in revenue. The United States accounts for the majority of regional value, supported by a clinical base of more than 1,200 active cell and gene therapy trials, FDA CBER regulatory throughput, and concentrated CDMO capacity in Maryland, North Carolina, and the Philadelphia corridor. NIH funding programs, the Bespoke Gene Therapy Consortium, and ARPA-H initiatives are reinforcing early-stage translation. Canada contributes a smaller but growing share via public-private investments in Ontario and Quebec, including the Centre for Commercialization of Regenerative Medicine. Mexico remains a minor contributor primarily serving clinical trial logistics and fill-finish functions. The CMS Cell and Gene Therapy Access Model, launched for sickle cell disease coverage, is stabilizing commercial volume forecasts through 2028 and supporting further US capacity commitments.

Europe

Europe held 26.8% share at USD 1.55 Billion in 2025. Germany leads regional activity with clinical, industrial, and academic strength centered in the Rhine-Main corridor and Bavaria, supported by Paul-Ehrlich-Institut oversight on ATMPs. The United Kingdom is the second-largest country market, anchored by the Cell and Gene Therapy Catapult, Oxford and Stevenage life science clusters, and MHRA's ILAP pathway that is accelerating ATMP approvals. France contributes via public-private CGT infrastructure including Yposkesi and Genopole. Italy rounds out the top four with strong academic-industrial programs in Milan and Rome. EMA's ATMP framework, PRIME scheme, and updated GMP Annex 1 sterile manufacturing guidance are shaping production standards across the region. Horizon Europe funding is channelling more than EUR 1 Billion into advanced therapy research over the current cycle.

Asia Pacific

Asia Pacific captured 20.4% share at USD 1.18 Billion in 2025 and is the fastest-growing regional market. China leads the region with a deep CAR-T clinical pipeline under NMPA oversight, supported by reforms under Chapter 8 of the Drug Administration Law and accelerated review pathways for urgent clinical needs. Japan ranks second, leveraging the Sakigake conditional approval pathway and a mature regenerative medicine framework under the PMDA that has enabled early cell therapy commercial precedents. South Korea is advancing rapidly with MFDS-enabled ATMP-style regulation, strong CDMO participation from Samsung Biologics and SK pharmteco, and sovereign support through K-BIO initiatives. India completes the top four through a combination of domestic CAR-T launches under CDSCO review and growing CDMO export ambitions in Hyderabad and Bengaluru.

Latin America

Latin America accounted for 4.2% share at USD 0.24 Billion in 2025. Brazil represents the dominant country market, with ANVISA advancing ATMP-specific guidance and public sector investment in CAR-T programs through institutions such as the Hemocentro network and USP. Mexico follows via clinical trial execution and early-stage investment in biologics infrastructure, though regulatory timelines for ATMPs remain longer than in North America. Argentina rounds out the top three, supported by ANMAT engagement with international regulators on cell therapy guidelines. Reimbursement remains the principal barrier across the region, with out-of-pocket and private insurance routes currently dominating patient access. Manufacturing capacity is limited, so most approved products are imported under named-patient and early access programs, with local fill-finish and logistics partnerships emerging as the near-term expansion mode.

Middle East & Africa

The Middle East & Africa region held 4.1% share at USD 0.24 Billion in 2025. The United Arab Emirates leads the region, with Abu Dhabi and Dubai actively building biopharma infrastructure under the Operation 300bn industrial strategy and Department of Health frameworks for advanced therapies. Saudi Arabia is investing through Vision 2030 bio-industrial programs, including sovereign commitments under PIF-backed Lifera to establish local biomanufacturing capability. South Africa anchors sub-Saharan activity with clinical research capacity in Johannesburg and Cape Town and SAHPRA engagement on cell therapy pathways. Israel is a notable innovation contributor with active CAR-T and AAV clinical programs, though commercial manufacturing scale remains limited. The broader region is a net importer of approved products and is prioritizing training, fill-finish, and clinical manufacturing partnerships rather than early greenfield vector builds.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Vector Type

- Viral Vectors (AAV, Lentivirus, Adenovirus, Retrovirus)

- Plasmid DNA

- Non-Viral Vectors (Lipid Nanoparticles, Electroporation, Transposons)

By Therapy Type

- Ex-vivo Gene Therapy

- In-vivo Gene Therapy

By Application

- Oncology

- Rare Genetic Disorders

- Neurological Disorders

- Ophthalmology

- Others (Cardiovascular, Infectious Disease, Metabolic)

By Mode of Manufacturing

- Outsourced (CDMO)

- In-House Manufacturing

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.80 B |

| Forecast Revenue (2034) | USD 19.80 B |

| CAGR (2025-2034) | 14.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Vector Type, (Viral Vectors (AAV, Lentivirus, Adenovirus, Retrovirus), Plasmid DNA, Non-Viral Vectors (Lipid Nanoparticles, Electroporation, Transposons)), By Therapy Type, (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application, (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Others (Cardiovascular, Infectious Disease, Metabolic)), By Mode of Manufacturing, (Outsourced (CDMO), In-House Manufacturing) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LONZA GROUP, CATALENT, INC., THERMO FISHER SCIENTIFIC (PATHEON VIRAL VECTOR SERVICES), WUXI ADVANCED THERAPIES, CHARLES RIVER LABORATORIES, OXFORD BIOMEDICA PLC, FUJIFILM DIOSYNTH BIOTECHNOLOGIES, MERCK KGAA (MILLIPORESIGMA), SAMSUNG BIOLOGICS, AGC BIOLOGICS, CYTIVA, SARTORIUS AG, TAKARA BIO INC., NOVARTIS AG, SK PHARMTECO (YPOSKESI), MINARIS REGENERATIVE MEDICINE, CELL AND GENE THERAPY CATAPULT, PFIZER CENTREONE, BIOSPRING GMBH, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Therapy Type (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Cardiovascular & Metabolic Diseases), By Manufacturing Mode (CDMO, In-House), Industry Trends & Forecast 2026-2034")

, By Therapy Type (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Cardiovascular & Metabolic Diseases), By Manufacturing Mode (CDMO, In-House), Industry Trends & Forecast 2026-2034")

, By Therapy Type (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Cardiovascular & Metabolic Diseases), By Manufacturing Mode (CDMO, In-House), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Gene Therapy Manufacturing Market?

The Global Gene Therapy Manufacturing Market was valued at USD 5.06 Billion in 2024 and is projected to reach USD 19.80 Billion by 2034, growing at a CAGR of 14.6% from 2026 to 2034. Growth is driven by increasing gene therapy approvals, rising demand for viral vector manufacturing, expanding investments in cell and gene therapy research, advancements in AAV and lentiviral production technologies, and growing adoption of GMP-compliant bioprocessing solutions across pharmaceutical, biotechnology, and CDMO sectors worldwide.

Who are the major players in the Gene Therapy Manufacturing Market?

LONZA GROUP, CATALENT, INC., THERMO FISHER SCIENTIFIC (PATHEON VIRAL VECTOR SERVICES), WUXI ADVANCED THERAPIES, CHARLES RIVER LABORATORIES, OXFORD BIOMEDICA PLC, FUJIFILM DIOSYNTH BIOTECHNOLOGIES, MERCK KGAA (MILLIPORESIGMA), SAMSUNG BIOLOGICS, AGC BIOLOGICS, CYTIVA, SARTORIUS AG, TAKARA BIO INC., NOVARTIS AG, SK PHARMTECO (YPOSKESI), MINARIS REGENERATIVE MEDICINE, CELL AND GENE THERAPY CATAPULT, PFIZER CENTREONE, BIOSPRING GMBH, OTHERS

Which segments covered the Gene Therapy Manufacturing Market?

By Vector Type, (Viral Vectors (AAV, Lentivirus, Adenovirus, Retrovirus), Plasmid DNA, Non-Viral Vectors (Lipid Nanoparticles, Electroporation, Transposons)), By Therapy Type, (Ex-vivo Gene Therapy, In-vivo Gene Therapy), By Application, (Oncology, Rare Genetic Disorders, Neurological Disorders, Ophthalmology, Others (Cardiovascular, Infectious Disease, Metabolic)), By Mode of Manufacturing, (Outsourced (CDMO), In-House Manufacturing)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Gene Therapy Manufacturing Market

Published Date : 29 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date