- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Generative AI in Chemical Market Size, Growth & Forecast | CAGR 29.1%

Global Generative AI in Chemical Market Size, Share & Industry Analysis By Technology (Machine Learning, Deep Learning, Generative Models, Quantum Computing, Reinforcement Learning, NLP), By Application (Molecular Design & Drug Discovery, Process Optimization, Chemical Engineering, Market Trend & Pricing Analysis), Industry Region & Key Players – Industry Segment Overview, Market Drivers, Challenges, Competitive Strategies, Innovation Trends & Forecast 2025–2034

Report Overview

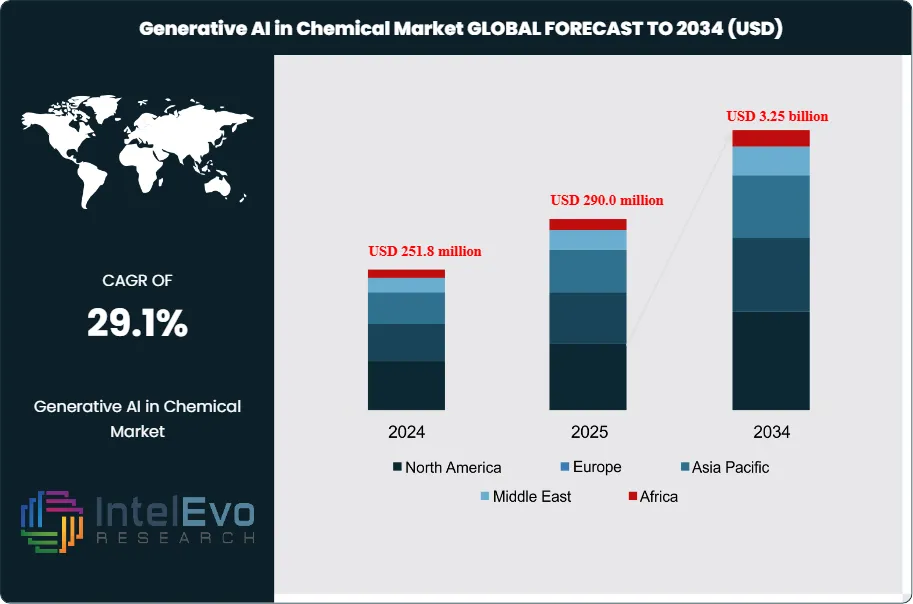

The Generative AI in Chemical Market is valued at approximately USD 290.0 million in 2025 and is projected to reach around USD 3.25 billion by 2034, expanding at a robust compound annual growth rate (CAGR) of about 29.1% during the forecast period from 2026 to 2034. Market growth is fueled by accelerating adoption of AI-driven molecular design, reaction optimization, and predictive analytics across specialty chemicals, pharmaceuticals, and materials science. In addition, rising R&D automation, increasing demand for faster product development cycles, and growing integration of generative models in sustainable chemistry and green manufacturing workflows are positioning the market for exponential long-term expansion.

Growth reflects a move from pilot projects to integrated AI engines embedded in research, development, and manufacturing. Generative models propose novel molecules, estimate properties, and optimize formulations, which shortens discovery cycles and can lower early-stage R&D spending by 20–30% for advanced users.

Get More Information about this report -

Request Free Sample ReportDemand for sustainable chemistries, higher asset utilization, and rapid product refresh drives adoption. Generative AI supports low-carbon process design, better catalysts, and bio-based materials that help producers respond to stricter emissions rules and circular economy goals. On the supply side, cloud providers, AI platforms, and leading chemical companies form alliances that link molecular design software with automated laboratories and plant control systems, enabling more continuous, data-driven development.

Scientific uptake underpins commercial progress. The Royal Society of Chemistry expects institutions using generative AI to predict chemical behaviors and characteristics to increase by about 40% from 2022 to 2024. The Materials Research Society notes that around 50% of materials science experts plan to use generative AI for new materials design and performance tuning by the end of 2024. The National Science Foundation points to a 35% rise in generative AI use to simulate and visualize complex chemical processes over the same period, reinforcing trust in the technology.

Risk factors remain significant. Data are fragmented, proprietary, and uneven in quality, which constrains model accuracy in specialized domains. Concerns around intellectual property, model explainability, and reproducibility slow deployment in safety-critical and regulated segments. Regulators in North America and Europe now expect explainable models, auditable data pipelines, and alignment with chemical safety regimes, pushing governance and validation costs up by an estimated 10–15% for large implementations.

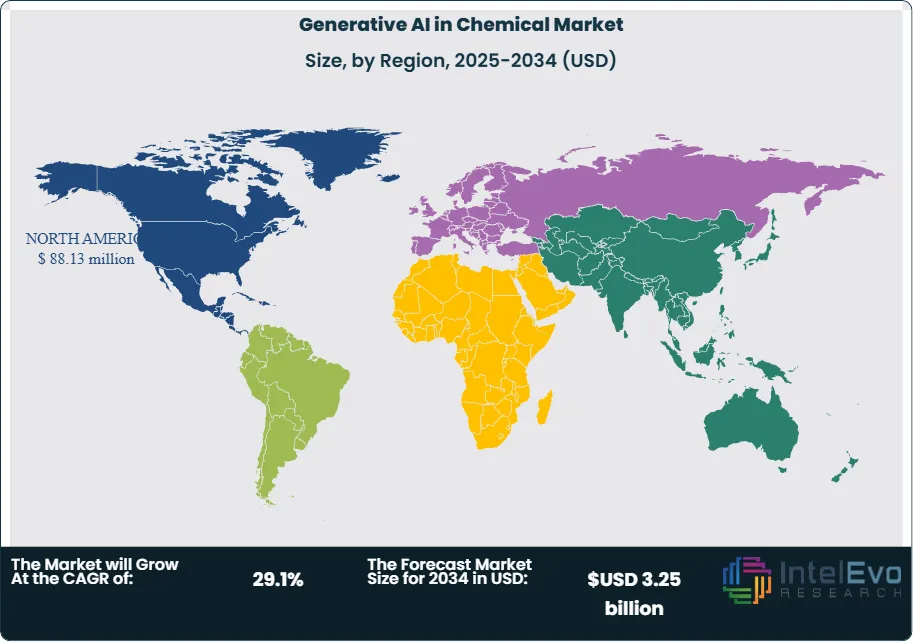

North America is expected to represent about 35% of revenue in 2024, with Europe near 30%, supported by strong pharmaceutical and specialty chemical clusters. Asia Pacific is the fastest-growing region, with a projected CAGR above 30% through 2034, led by China, Japan, South Korea, and India in batteries, electronic materials, and advanced polymers. New initiatives in the Middle East and Latin America around petrochemicals and sustainable feedstocks signal additional investment opportunities across the forecast horizon.

, By Application (Molecular Design & Drug Discovery, Process Optimization, Chemical Engineering, Market Trend & Pricing Analysis), Industry Region & Key Players – Industry Segment Overview, Market Drivers, Challenges, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global generative AI in chemicals space accelerates from early pilots to scaled adoption, with market value reaching estimated: USD 251.8 million in 2024; USD 290.0 million in 2025 and projected to approach estimated: USD 3.25 billion by 2034, implying a CAGR of estimated: 29.1%, 2026-2034.

- Segment Dominance: R&D and molecular design workflows hold the largest revenue share as firms prioritize AI-driven compound and formulation discovery, with these use cases accounting for estimated: 55.0%, 2024 of total spending and maintaining leadership through estimated: 2034.

- Segment Dominance: Pharmaceuticals and specialty chemicals remain the primary adopters of generative AI platforms, together contributing estimated: 60.0%, 2024 of end-user demand and expected to retain more than estimated: 50.0%, 2034 as downstream industries scale AI-enabled innovation.

- Driver: Pressure to cut development timelines and achieve sustainable chemistry outcomes acts as the main growth engine, with leading adopters targeting R&D cycle-time reductions of estimated: 20.0%, 2024 and cost savings of estimated: 15.0%, 2024 versus traditional methods.

- Restraint: Data scarcity, IP concerns, and explainability requirements restrict deployment in regulated domains, with governance and compliance efforts adding an extra overhead of estimated: 10.0%, 2024 to large-scale implementations and slowing full-stack integration.

- Opportunity: Generative AI unlocks new revenue pools in green chemistry, battery materials, and advanced polymers, where solution providers can capture incremental opportunities worth estimated: 1.0 billion USD, 2034 as clients pursue decarbonization and performance gains.

- Trend: Partnerships between AI vendors, cloud platforms, and chemical producers expand, with collaborative ecosystems expected to power more than estimated: 65.0%, 2030 of new deployments and drive strong growth in integrated design-to-manufacturing workflows by estimated: 2034.

- Regional Analysis: North America leads early adoption with an estimated: 35.0%, 2024 revenue share, while Europe holds estimated: 30.0%, 2024 and Asia Pacific, at estimated: 25.0%, 2024, records the fastest trajectory toward an expected regional CAGR above estimated: 30.0%, 2024-2034.

By Technology

Machine learning continues to anchor the technology landscape in 2025 as the most widely adopted toolset across chemical research, modeling, and production workflows. It accounted for more than 26 percent of global revenue in 2024 and maintains its lead in 2025 due to its capacity to process large datasets and generate accurate predictions for molecular behavior, process variables, and material performance. You see this reflected in R&D teams that rely on trained models to shorten discovery cycles and improve hit rates in early-stage screening. Adoption remains high because machine learning supports the full chain of activities from formulation work to plant-level quality assurance.

Its position strengthens as downstream technologies draw from machine learning foundations. Deep learning and generative models, including GANs and VAEs, require structured datasets and pre-trained feature extraction systems that machine learning provides. These models now assist chemical developers in exploring new compound families and simulating structural variations at speeds unattainable through conventional laboratory workflows. Quantum computing and reinforcement learning add further scale. Early pilots in 2025 show improvements in reaction optimization and property prediction for catalysts and energy materials, signaling broader use of hybrid approaches over the next five years.

As the technology stack matures, natural language processing and other analytical tools help researchers consolidate scientific literature, patents, and experimental reports into actionable intelligence. Combined, these technologies create an integrated environment where chemical insights update continuously and guide high-value decisions in R&D and advanced manufacturing.

By Application

Molecular design and drug discovery continue to dominate application demand. This segment held more than 39 percent of the market in 2024 and remains the fastest-growing area in 2025. Generative models evaluate molecular structures, simulate behavior, and rank candidates with higher precision than traditional computational tools. Pharmaceutical companies now shorten target identification phases by up to 30 percent, and your teams can screen thousands of potential drug candidates in a fraction of the time required in the past. Chemical producers apply similar methods to design polymers, coatings, additives, and specialty materials with tailored property profiles.

Process optimization and chemical engineering follow as major application clusters. AI systems help operators reduce energy use, stabilize product specifications, and extend asset uptime. Plants implementing AI-supported process control have reported energy reductions of 8 to 12 percent, with measurable improvements in overall throughput. These systems also identify failure risks early, which supports maintenance planning and safety compliance.

Market trend analysis and pricing optimization increase in importance as global volatility raises pressure on margins. AI models track feedstock movements, supply shifts, and customer demand patterns to support commercial decisions. The remaining application areas include recycling optimization, carbon monitoring, and predictive environmental assessment. These segments expand gradually as chemical companies prepare for regulatory targets tied to emissions and waste recovery.

By End-Use

Residential builders show growing interest in generative chemical design as material standards move toward durability, safety, and environmental compliance. AI-assisted formulations for construction chemicals, such as admixtures and sealants, support improved performance with lower resource use. These solutions gain relevance in 2025 as governments push for higher energy-efficiency ratings and longer product life cycles.

Commercial building projects adopt AI-enabled chemical solutions at a faster pace. Large developers and infrastructure firms prioritize materials with predictable behavior, reduced curing times, and enhanced resistance to thermal and mechanical stress. AI-generated material insights help you select products that meet project-specific constraints, which benefits large-scale flooring, façade, and structural applications.

Industrial facilities remain the most advanced users. Operators integrate AI-driven chemical models to support coatings, protective materials, process fluids, and filtration systems tailored to heavy-duty environments. Adoption rises in sectors such as oil and gas, mining, and electronics manufacturing, where even small performance improvements produce significant operational gains.

By Region

North America continues to lead global adoption in 2025 with more than 42 percent of market revenue. Strong demand from pharmaceuticals, specialty chemicals, and advanced materials accelerates uptake. Investment in AI research, high digital maturity, and an active startup base strengthens the regional position. You see partnerships forming between software providers and chemical producers to co-develop models tuned for specific chemistries and process conditions.

Europe follows with steady growth driven by regulatory pressure related to emissions, safety, and circular design. Companies adopt AI tools to meet compliance targets and support low-carbon material development. Activity is especially strong in Germany, France, and the Nordic countries, where chemical firms expand AI budgets and build long-term digitalization strategies.

Asia Pacific shows the highest growth rate through 2030. China, Japan, South Korea, and India increase investment in material science and battery technology. Regional manufacturers implement AI to accelerate product development and strengthen export competitiveness. Latin America and the Middle East and Africa expand at a slower pace but gain attention as petrochemical operators explore AI-supported process enhancement and energy optimization programs.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Machine Learning

- Deep Learning

- Generative Models (GAN & VAE)

- Quantum Computing

- Reinforcement Learning

- Natural Language Processing (NLP)

- Others

By Application

- Molecular Design and Drug Discovery

- Process Optimization and Chemical Engineering

- Market Trend Analysis & Pricing Optimization

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 290.0 million |

| Forecast Revenue (2034) | USD 3.25 billion |

| CAGR (2025-2034) | 29.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Machine Learning, Deep Learning, Generative Models (GAN & VAE), Quantum Computing, Reinforcement Learning, Natural Language Processing (NLP), Others), By Application, (Molecular Design and Drug Discovery, Process Optimization and Chemical Engineering, Market Trend Analysis & Pricing Optimization, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Sinochem Corporation, Accenture, Biesterfeld AG, IBM Corporation, Tricon Energy Inc., Omya AG, Mitsui Chemicals, Azelis Group NV, HELM AG, Google, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Molecular Design & Drug Discovery, Process Optimization, Chemical Engineering, Market Trend & Pricing Analysis), Industry Region & Key Players – Industry Segment Overview, Market Drivers, Challenges, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Application (Molecular Design & Drug Discovery, Process Optimization, Chemical Engineering, Market Trend & Pricing Analysis), Industry Region & Key Players – Industry Segment Overview, Market Drivers, Challenges, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Application (Molecular Design & Drug Discovery, Process Optimization, Chemical Engineering, Market Trend & Pricing Analysis), Industry Region & Key Players – Industry Segment Overview, Market Drivers, Challenges, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Generative AI in Chemical Market?

The global generative AI in chemical market was valued at USD 290.0 million in 2025 and is projected to reach USD 3.25 billion by 2034, growing at a CAGR of 29.1% from 2026 to 2034, driven by AI-powered molecular design, reaction optimization, R&D automation, and sustainable chemistry innovation.

Who are the major players in the Generative AI in Chemical Market?

Sinochem Corporation, Accenture, Biesterfeld AG, IBM Corporation, Tricon Energy Inc., Omya AG, Mitsui Chemicals, Azelis Group NV, HELM AG, Google, Other Key Players

Which segments covered the Generative AI in Chemical Market?

By Technology, (Machine Learning, Deep Learning, Generative Models (GAN & VAE), Quantum Computing, Reinforcement Learning, Natural Language Processing (NLP), Others), By Application, (Molecular Design and Drug Discovery, Process Optimization and Chemical Engineering, Market Trend Analysis & Pricing Optimization, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Generative AI in Chemical Market

Published Date : 04 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date