- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Generative AI in Legal Services Market Forecast 2034 | CAGR 22.7%

Global Generative AI in Legal Services Market Size, Share, Growth & Industry Analysis By Application (Contract Analysis & Drafting, Legal Research & Case Analysis, Litigation Analytics & E-Discovery, Compliance Monitoring, Document Summarization & Brief Generation), By End-User (Law Firms, Corporate Legal Departments, LPO Providers, Government & Judiciary, Individual Practitioners), By Deployment (Cloud, Hybrid, On-Premise), By Technology (LLM, NLP, ML, Knowledge Graphs) Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

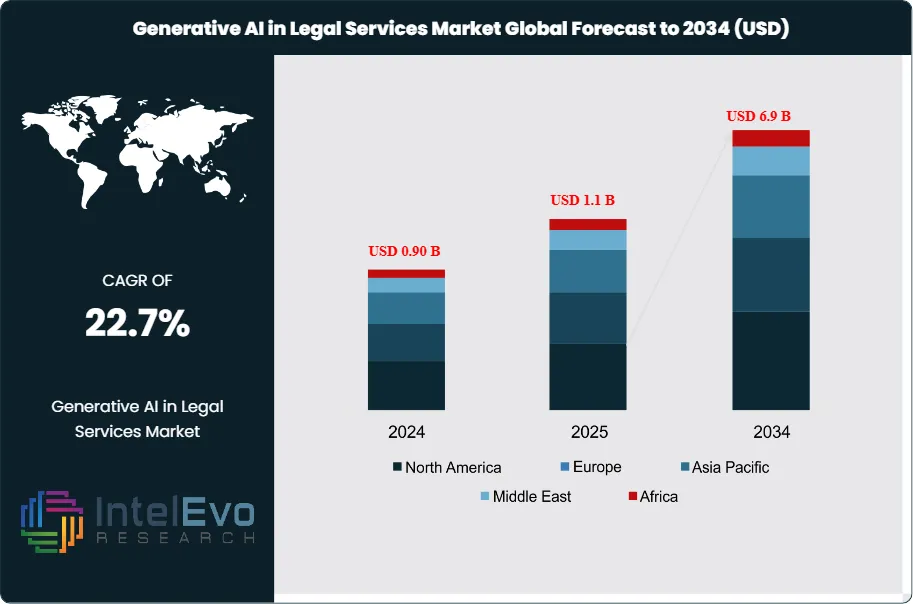

| USD 1.1 Billion | USD 6.9 Billion | 22.7% | North America, 48.0% |

The Generative AI in Legal Services Market was valued at approximately USD 0.90 Billion in 2024 and reached USD 1.1 Billion in 2025. The market is projected to grow to USD 6.9 Billion by 2034, expanding at a CAGR of 22.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.8 billion over the analysis period. Generative AI in legal services encompasses LLM-powered contract drafting and review, legal research assistants, litigation analytics, document summarization, compliance monitoring, e-discovery automation, and AI-assisted brief generation deployed across law firms, corporate legal departments, courts, and government agencies.

Get More Information about this report -

Request Free Sample ReportAdoption of generative AI in legal services is accelerating as law firms and corporate legal departments face mounting pressure to reduce costs while managing increasing regulatory complexity. The American Bar Association (ABA) reported in 2025 that 42% of Am Law 200 firms had deployed at least one generative AI tool, up from 11% in 2023. Corporate legal departments spent an average of USD 1.8 million annually on legal technology in 2025, with AI-powered tools consuming 28% of that budget. The EU AI Act classified certain legal AI applications, including automated judicial decision support, as high-risk systems requiring conformity assessments and human oversight, creating a compliance-driven product differentiation tier.

Technology effects are pronounced. Large language models fine-tuned on legal corpora now achieve 89% accuracy on contract clause extraction benchmarks, up from 71% in 2023. Retrieval-augmented generation (RAG) architectures connecting AI models to case law databases, regulatory repositories, and internal precedent libraries have reduced legal research time by 45–60% in enterprise deployments. Multi-jurisdictional AI tools that handle legal analysis across US, UK, EU, and common law frameworks grew from 8% of deployments in 2023 to 24% in 2025.

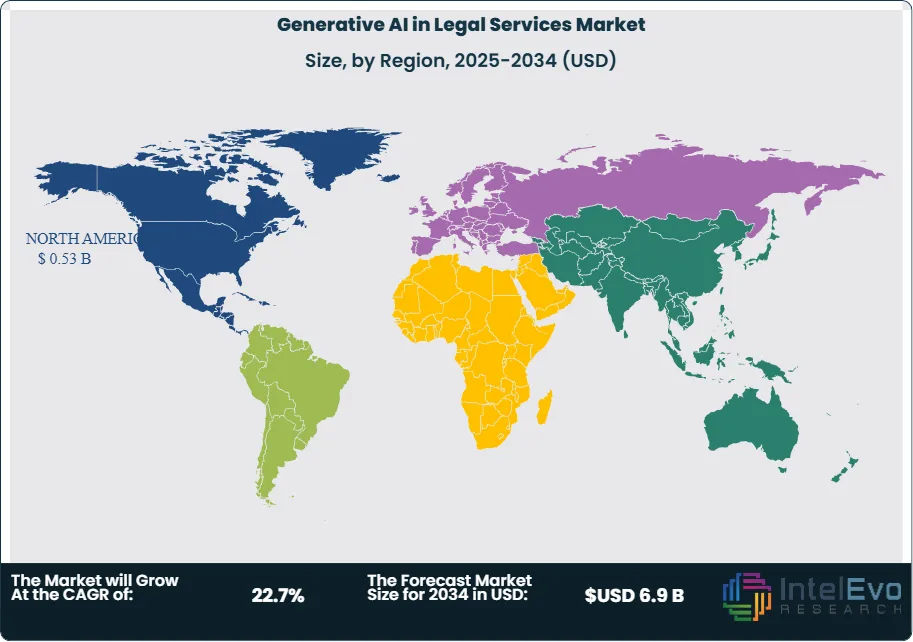

Regional patterns show North America leading with 48.0% share in 2025, driven by the concentration of Am Law 100 firms, Fortune 500 corporate legal departments, and legal AI startup funding in the US. Europe held 26.0%, shaped by GDPR compliance automation demand and AI Act documentation requirements. Asia Pacific accounted for 16.0%, with growing adoption in India's legal process outsourcing sector, Japan's corporate governance reforms, and Australia's litigation technology market. Latin America contributed 5.5%, concentrated in Brazil's complex regulatory environment. The Middle East and Africa held 4.5%, led by UAE legal modernization programs. Risk factors include judicial skepticism toward AI-generated legal work, hallucination risks in case citation, professional liability concerns, and bar association regulatory uncertainty. The generative AI in legal services market outlook remains strong as legal spending exceeds USD 1 trillion globally and AI penetration remains below 5% of total addressable spend.

, By End-User (Law Firms, Corporate Legal Departments, LPO Providers, Government & Judiciary, Individual Practitioners), By Deployment (Cloud, Hybrid, On-Premise), By Technology (LLM, NLP, ML, Knowledge Graphs) Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The generative AI in legal services market was valued at USD 1.1 billion in 2025 and is projected to reach USD 6.9 billion by 2034, registering a CAGR of 22.7% over the forecast period 2025–2034.

- Segment Dominance (By Application): Contract analysis and drafting captured 32.0% of the market in 2025, valued at USD 0.35 billion, as law firms and corporate legal departments prioritized AI tools that automate the most time-intensive transactional workflow.

- Segment Dominance (By End-User): Law firms accounted for 45.0% of market revenue in 2025, driven by Am Law 200 adoption and competitive pressure to improve realization rates and reduce associate hours on routine tasks.

- Driver: Billable hour cost pressure compelled adoption; generative AI tools reduced contract review time by 50–65% and legal research hours by 45–60%, enabling firms to reallocate associate capacity to higher-value advisory work.

- Restraint: AI hallucination in legal citations remained a barrier; 31% of law firms reported at least one instance of fabricated case references in 2025, prompting mandatory human review protocols that slowed deployment timelines.

- Opportunity: AI-powered compliance monitoring for regulated industries represents a USD 1.8 billion incremental opportunity through 2034, as financial services, healthcare, and energy firms automate regulatory change tracking across multiple jurisdictions.

- Trend: Agentic legal AI workflows capable of autonomous document assembly, filing, and deadline management grew from 4% to 19% of enterprise deployments in 2025, signaling a shift from assistive research to autonomous legal task execution.

- Regional Analysis: North America led with 48.0% market share, generating USD 0.53 billion in 2025; Am Law 100 firm adoption, concentrated VC funding, and the world's largest legal services market anchored demand.

Competitive Landscape Overview

The generative AI in legal services market is moderately fragmented, with the top four vendors collectively holding approximately 42% of global revenue in 2025. Competition is technology-driven, centering on legal domain model accuracy, jurisdictional coverage, integration with existing practice management systems, and data privacy guarantees. Legal AI startups attracted over USD 2.1 billion in venture funding during 2024–2025, intensifying competition with established legal technology incumbents. Recent acquisition activity surged as Thomson Reuters, LexisNexis, and enterprise software firms bought AI-native legal startups to embed generative capabilities into their established platforms.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Thomson Reuters | US/Canada | Leader | CoCounsel (Westlaw AI) | North America | Launched CoCounsel 2.0 with GPT-4o integration (Mar 2025) |

| LexisNexis (RELX) | US/UK | Leader | Lexis+ AI | North America | Released multi-jurisdictional research across 50 countries (Feb 2025) |

| Harvey AI | US | Leader | Harvey Legal AI Platform | North America | Raised USD 300M Series D at USD 3B valuation (Jan 2026) |

| Microsoft (Copilot) | US | Leader | Microsoft 365 Copilot for Legal | Global | Partnered with Allen & Overy for firm-wide legal Copilot (Apr 2025) |

| Ironclad | US | Challenger | Ironclad AI Contract Intelligence | North America | Launched AI contract generation from natural language (Jun 2025) |

| Casetext (Thomson Reuters) | US | Challenger | CoCounsel Legal Research | North America | Integrated into Westlaw ecosystem post-acquisition (Dec 2024) |

| Robin AI | UK | Challenger | Robin AI Contract Platform | Europe | Expanded to 15 European jurisdictions (Sep 2025) |

| Luminance | UK | Challenger | Luminance Autopilot | Europe | Released autonomous contract negotiation agent (Aug 2025) |

| EvenUp | US | Niche Player | EvenUp Claims AI | North America | Processed 500,000+ personal injury demand letters (May 2025) |

| Spellbook | Canada | Niche Player | Spellbook Contract Drafting | North America | Reached 10,000 law firm users across US and Canada (Jul 2025) |

By Application:

Contract analysis and drafting led with 32.0% market share, generating USD 0.35 billion in 2025. This application uses LLMs to extract key clauses, identify risk provisions, compare terms against playbooks, and generate first drafts of standard agreements. Law firms handling M&A transactions report that AI-assisted contract review reduced due diligence timelines by 50–65%. Ironclad, Luminance, and Robin AI dominate the contract-focused segment. Legal research and case analysis held 28.0%, valued at USD 0.31 billion. CoCounsel by Thomson Reuters and Lexis+ AI by LexisNexis lead this segment, providing AI-powered case law search, statutory interpretation, and argument generation. Retrieval-augmented generation architectures connected to proprietary legal databases achieve 89% accuracy on case citation benchmarks. Litigation analytics and e-discovery captured 18.0%, worth USD 0.20 billion, driven by the exponential growth of electronically stored information in disputes. Compliance monitoring and regulatory tracking held 13.0%, generating USD 0.14 billion, serving corporate legal departments that track regulatory changes across multiple jurisdictions. Legal document summarization and brief generation accounted for the remaining 9.0%, valued at USD 0.10 billion, targeting associates and paralegals who summarize depositions, filings, and court opinions.

By End-User:

Law firms commanded 45.0% of market revenue in 2025, generating USD 0.50 billion. Am Law 200 firms drove adoption, with 42% having deployed at least one generative AI tool by 2025. Large firms use AI for contract review, legal research, brief drafting, and knowledge management. Competitive pressure to improve realization rates and reduce costs per matter accelerated procurement timelines from 12 months to under 6 months. Corporate legal departments held 30.0%, valued at USD 0.33 billion. In-house counsel at Fortune 500 companies deploy AI for contract management, compliance monitoring, and routine legal question answering, reducing reliance on outside counsel for standard matters. Average corporate legal department AI spending reached USD 510,000 per year in 2025. Legal process outsourcing (LPO) providers captured 12.0%, generating USD 0.13 billion, with Indian LPO firms integrating AI to improve throughput on document review and contract abstraction projects. Government and judicial institutions held 8.0%, worth USD 0.09 billion, focused on court administration, sentencing guideline analysis, and public records processing. Individual legal practitioners and small firms accounted for 5.0%, valued at USD 0.06 billion, adopting affordable SaaS legal AI tools from Spellbook and similar providers.

By Deployment:

Cloud-based deployment dominated with 68.0% share, valued at USD 0.75 billion in 2025. Cloud delivery enables continuous model updates, lower upfront costs, and integration with web-based legal research platforms. Most legal AI startups, including Harvey AI, CoCounsel, and Spellbook, operate exclusively as cloud SaaS products. Hybrid deployment held 22.0%, generating USD 0.24 billion. Large law firms and corporate legal departments with strict client confidentiality requirements deploy hybrid architectures that process sensitive matter data on-premise while routing general research queries through cloud endpoints. Am Law 50 firms showed the strongest preference for hybrid, with 58% selecting this model. On-premise deployment captured 10.0%, valued at USD 0.11 billion, serving government agencies, defense contractors, and law firms handling classified or highly sensitive litigation that cannot leave controlled environments.

By Technology:

Large language model (LLM) platforms led with 55.0% share, valued at USD 0.61 billion in 2025. LLM-based solutions from Harvey AI, Thomson Reuters CoCounsel, and Lexis+ AI use models fine-tuned on legal corpora to generate, analyze, and summarize legal text. GPT-4o, Claude, and Gemini serve as the primary foundation models. Natural language processing (NLP) and entity extraction held 25.0%, generating USD 0.28 billion, covering traditional AI techniques for clause identification, named entity recognition in contracts, and structured data extraction from legal documents. Machine learning analytics captured 13.0%, worth USD 0.14 billion, applied to litigation outcome prediction, judge behavior modeling, and case timeline estimation. Knowledge graph and semantic search technology held 7.0%, valued at USD 0.08 billion, powering legal research tools that map relationships between cases, statutes, and regulatory provisions.

Regional Analysis

North America:

North America led the generative AI in legal services market with 48.0% share, generating USD 0.53 billion in 2025. The United States accounted for over 92% of regional revenue, anchored by the world's largest legal services market valued at USD 440 billion. Am Law 100 firms collectively invested an estimated USD 680 million in legal technology during 2025, with generative AI tools consuming a growing share. Thomson Reuters and LexisNexis, both headquartered in North America, dominate the legal research AI segment. Harvey AI, the highest-valued legal AI startup at USD 3 billion, serves over 50 Am Law 100 firms. The US federal judiciary's 2024 guidance on AI use in court filings established disclosure requirements that encouraged adoption of citation-verified AI research tools. Canada contributed through its legal AI startup community, with Spellbook and Blue J Legal serving both Canadian and US markets. Mexico's corporate legal sector began piloting contract review AI for cross-border transactions.

Europe:

Europe held 26.0% of the global market, valued at USD 0.29 billion in 2025. The United Kingdom led European demand through London's Magic Circle law firms and Chancery Lane legal technology community. Allen & Overy's firm-wide deployment of Harvey AI in 2023 set a precedent that other UK firms followed. Luminance and Robin AI, both headquartered in the UK, provide contract AI platforms serving European corporate clients. Germany contributed through its corporate legal sector, where compliance with the EU AI Act's documentation requirements for high-risk legal AI systems created a distinct market segment. France invested in sovereign legal AI initiatives, with the Ministry of Justice piloting AI-assisted case management in administrative courts. The Netherlands emerged as a hub for cross-border legal AI, serving pan-European firms managing GDPR, competition law, and trade regulation compliance. The EU AI Act's classification of certain legal AI tools as high-risk systems required conformity assessments, favoring established vendors with audit-ready platforms.

Asia Pacific:

Asia Pacific captured 16.0% market share, generating USD 0.18 billion in 2025. India represented the fastest-growing country-level market, driven by its USD 2.5 billion legal process outsourcing industry that integrates AI to improve document review and contract abstraction throughput. Indian LPO firms serving US and UK law firms adopted generative AI at rates exceeding 35% in 2025. Japan contributed through corporate governance reforms that increased demand for compliance monitoring and board reporting AI tools. Australia's litigation technology market, one of the most advanced in the region, adopted e-discovery AI and legal research tools across its top-tier firms. South Korea's legal sector invested in Korean-language legal AI models for contract analysis and regulatory tracking. China's legal AI market grew rapidly but remained largely separate from Western providers due to data localization requirements and domestic platform dominance by Baidu and iFlytek legal products.

Latin America:

Latin America accounted for 5.5% of the global market, generating USD 0.06 billion in 2025. Brazil dominated regional demand, driven by its notoriously complex regulatory and tax system that generates massive volumes of legal documentation. Brazilian law firms handling tax litigation and labor disputes adopted contract review and regulatory tracking AI at rates of 18% in 2025. Mexico contributed through cross-border legal work supporting US-Mexico trade, where bilingual contract AI tools gained traction. Argentina's Buenos Aires legal technology community produced several startups focused on Spanish-language legal document automation. Colombia invested in judicial modernization programs that included AI-assisted case management pilots. Limited Portuguese and Spanish legal training data for LLMs remains a constraint, though providers like Thomson Reuters began releasing multi-language legal models in 2025.

Middle East and Africa:

The Middle East and Africa region held 4.5% market share, valued at USD 0.05 billion in 2025. The UAE led regional investment through its DIFC Courts Technology initiative, which piloted AI-assisted case management and legal research tools. Saudi Arabia's Vision 2030 legal reform program created demand for contract AI to support the kingdom's rapid commercial law modernization. Israel contributed through its legal AI startup sector, with companies developing tools for intellectual property analysis and patent prosecution. South Africa represented the largest sub-Saharan African market, with top-tier law firms in Johannesburg adopting legal research AI. The region faces unique challenges including Arabic-language legal corpus limitations, diverse civil and common law frameworks across jurisdictions, and limited local cloud infrastructure for data-sensitive legal workloads.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Application

- Contract Analysis and Drafting

- Legal Research and Case Analysis

- Litigation Analytics and E-Discovery

- Compliance Monitoring and Regulatory Tracking

- Legal Document Summarization and Brief Generation

By End-User

- Law Firms

- Corporate Legal Departments

- Legal Process Outsourcing (LPO) Providers

- Government and Judicial Institutions

- Individual Practitioners and Small Firms

By Deployment

- Cloud-Based

- Hybrid

- On-Premise

By Technology

- Large Language Model (LLM) Platforms

- Natural Language Processing and Entity Extraction

- Machine Learning Analytics

- Knowledge Graph and Semantic Search

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.1 B |

| Forecast Revenue (2034) | USD 6.9 B |

| CAGR (2025-2034) | 22.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application, (Contract Analysis and Drafting, Legal Research and Case Analysis, Litigation Analytics and E-Discovery, Compliance Monitoring and Regulatory Tracking, Legal Document Summarization and Brief Generation), By End-User, (Law Firms, Corporate Legal Departments, Legal Process Outsourcing (LPO) Providers, Government and Judicial Institutions, Individual Practitioners and Small Firms), By Deployment, (Cloud-Based, Hybrid, On-Premise), By Technology, (Large Language Model (LLM) Platforms, Natural Language Processing and Entity Extraction, Machine Learning Analytics, Knowledge Graph and Semantic Search) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THOMSON REUTERS, LEXISNEXIS (RELX GROUP), HARVEY AI, MICROSOFT, IRONCLAD, LUMINANCE, ROBIN AI, EVENUP, SPELLBOOK, CASETEXT (THOMSON REUTERS), KIRA SYSTEMS (LITERA), RELATIVITY (E-DISCOVERY), BLUE J LEGAL, DILIGEN, ONIT, CLIO, EVERLAW, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Law Firms, Corporate Legal Departments, LPO Providers, Government & Judiciary, Individual Practitioners), By Deployment (Cloud, Hybrid, On-Premise), By Technology (LLM, NLP, ML, Knowledge Graphs) Trends & Forecast 2026–2034")

, By End-User (Law Firms, Corporate Legal Departments, LPO Providers, Government & Judiciary, Individual Practitioners), By Deployment (Cloud, Hybrid, On-Premise), By Technology (LLM, NLP, ML, Knowledge Graphs) Trends & Forecast 2026–2034")

, By End-User (Law Firms, Corporate Legal Departments, LPO Providers, Government & Judiciary, Individual Practitioners), By Deployment (Cloud, Hybrid, On-Premise), By Technology (LLM, NLP, ML, Knowledge Graphs) Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Generative AI in Legal Services Market?

Global Generative AI in legal services market valued at USD 0.90B in 2024, reaching USD 6.9B by 2034, growing at a CAGR of 22.7% from 2026–2034.

Who are the major players in the Generative AI in Legal Services Market?

THOMSON REUTERS, LEXISNEXIS (RELX GROUP), HARVEY AI, MICROSOFT, IRONCLAD, LUMINANCE, ROBIN AI, EVENUP, SPELLBOOK, CASETEXT (THOMSON REUTERS), KIRA SYSTEMS (LITERA), RELATIVITY (E-DISCOVERY), BLUE J LEGAL, DILIGEN, ONIT, CLIO, EVERLAW, Others

Which segments covered the Generative AI in Legal Services Market?

By Application, (Contract Analysis and Drafting, Legal Research and Case Analysis, Litigation Analytics and E-Discovery, Compliance Monitoring and Regulatory Tracking, Legal Document Summarization and Brief Generation), By End-User, (Law Firms, Corporate Legal Departments, Legal Process Outsourcing (LPO) Providers, Government and Judicial Institutions, Individual Practitioners and Small Firms), By Deployment, (Cloud-Based, Hybrid, On-Premise), By Technology, (Large Language Model (LLM) Platforms, Natural Language Processing and Entity Extraction, Machine Learning Analytics, Knowledge Graph and Semantic Search)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Generative AI in Legal Services Market

Published Date : 06 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date