- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Generative AI in Media & Entertainment Market Size 2025–2034 | CAGR 27.1%

Global Generative AI in Media and Entertainment Market Size, Share, Growth & Analysis By Type (Text-to-Image, Image-to-Image, Video Generation, Music Generation, 3D Modeling & Animation), By Deployment Mode (Cloud-Based, On-Premise), By Application (Gaming, Film & Television, Advertising & Marketing, Music Production, VR & AR), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

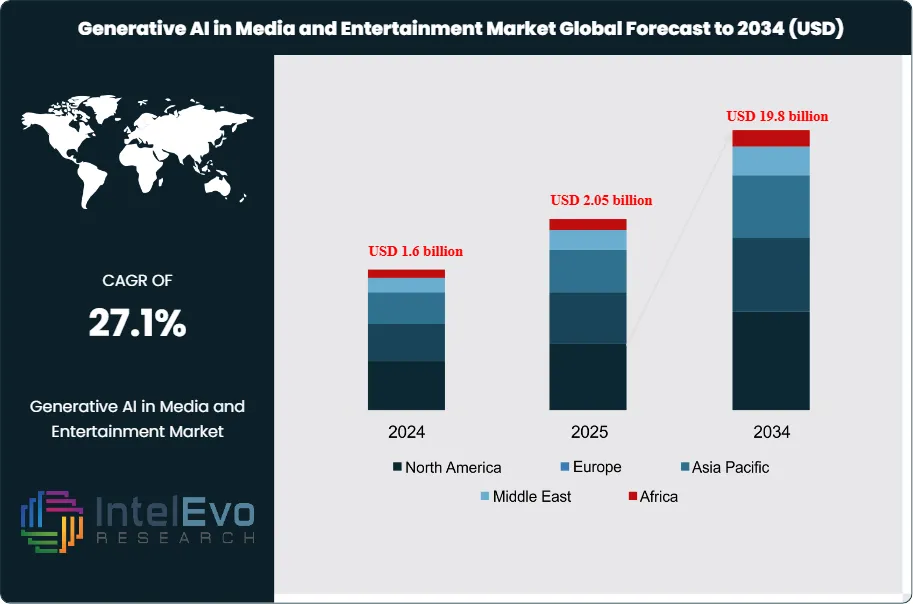

The Generative AI in Media and Entertainment Market is estimated to reach approximately USD 2.05 billion in 2025 and is projected to surge to around USD 19.8 billion by 2034, registering an accelerated compound annual growth rate (CAGR) of about 27.1% during the forecast period from 2026 to 2034. This rapid expansion is driven by increasing adoption of AI-powered content creation tools across film, television, gaming, music, and digital advertising platforms. Media companies are leveraging generative AI for scriptwriting, visual effects, animation, personalized content, and virtual production to reduce production costs and shorten development timelines. Additionally, rising demand for immersive experiences, real-time personalization, and scalable content generation is positioning generative AI as a transformative force reshaping creative workflows and monetization models across the global entertainment ecosystem.

Get More Information about this report -

Request Free Sample ReportAdvances in deep learning, transformer models, and multimodal architectures are changing how content is conceived, produced, and distributed. Studios, streaming platforms, gaming companies, and advertisers adopt generative AI to automate asset creation, compress production cycles, and deliver personalized experiences. In 2024, content creation and enhancement solutions account for an estimated 55% of global revenues, driven by script assistance, synthetic performers, and virtual production. Service providers, including consulting, integration, and managed AI operations, contribute roughly 30%, as enterprises seek guidance on model selection, workflow redesign, and risk management.

On the demand side, the shift to direct-to-consumer streaming, short-form video, and interactive formats increases pressure to release more content at lower marginal cost. Generative AI reduces post-production time by 20–40% in early deployments and allows marketing assets to be produced in minutes rather than days. On the supply side, hyperscale cloud platforms and specialized GPU infrastructure lower entry barriers for smaller studios and independent creators, while model vendors and startups compete to offer media-tuned tools. Talent gaps in AI engineering and data governance, together with rising compute costs, remain limiting factors.

Regulation and governance form a critical shaping force. Emerging rules on copyright, synthetic media disclosure, and child protection in digital content introduce new compliance requirements, particularly in North America and Europe, which represent around 60% of current market revenue. Providers implement consent management, watermarking, and content provenance controls, creating opportunities for assurance and monitoring services but increasing operational complexity. Intellectual property disputes and reputational exposure from misuse of generative tools are key constraints to faster adoption.

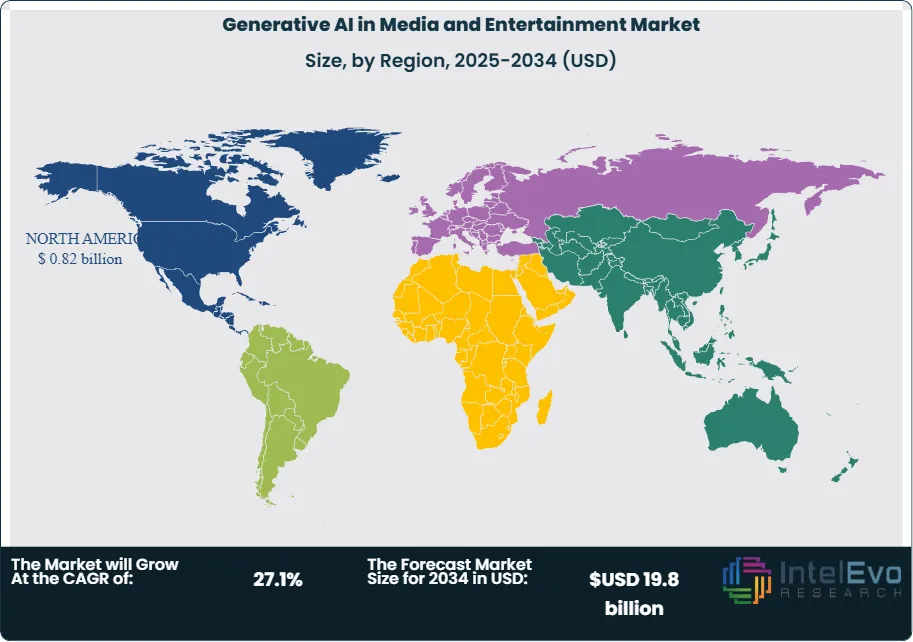

Regionally, North America holds an estimated 38% share in 2024, supported by major film studios, digital platforms, and advertising budgets. Europe follows with approximately 24%, influenced by public-service media and data-protection frameworks. Asia Pacific is the fastest-growing region, with a projected CAGR above 30%, underpinned by mobile-first consumers and local streaming platforms. Capital flows concentrate in virtual production, AI-assisted animation, real-time localization, and dynamic in-game content, positioning generative AI as a core capability in media and entertainment value creation.

, By Deployment Mode (Cloud-Based, On-Premise), By Application (Gaming, Film & Television, Advertising & Marketing, Music Production, VR & AR), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The generative AI in media and entertainment market will reach USD 19.8 billion by 2034, supported by a high CAGR of 27.1%, 2026 to 2034, from an estimated USD 2.05 billion in 2025 base.

- Segment Dominance: In deployment mode, cloud-based solutions hold a leading 52.7%, 2023 share because media enterprises prioritize scalability, flexibility, and cost efficiency for workloads valued at estimated: 1.5 billion USD, 2023.

- Segment Dominance: Within solution types, text-to-image generation grows from 299.3 million USD, 2022 to 2,644.9 million USD, 2032. Gaming use cases expand from 477.7 million USD, 2022 to 4,817.2 million USD, 2032, reinforcing their role as anchor segments.

- Driver: Demand for personalized, dynamic content and VR/AR experiences drives spending, with personalized media expected to represent estimated: 45.0% of generative AI project budgets, 2025 and overall adoption supporting a CAGR of 26.3%, 2024-2034.

- Restraint: Data privacy, security concerns, and authenticity risks limit rollout, with an estimated: 30.0% of media organizations, 2024 citing regulatory uncertainty and high initial deployment costs near estimated: 1.0 million USD per large-scale implementation, 2024.

- Opportunity: Vendors unlock upside by expanding into emerging markets expected to contribute estimated: 35.0% of global revenues, 2030 and by forming cross-industry alliances that can add estimated: 2.0 billion USD, 2034 in incremental value through education, training, and immersive formats.

- Trend: Key trends include adoption of generative AI in advertising and AI-driven animation, with NLP-enhanced campaigns projected to lift engagement rates by estimated: 15.0%, 2026 and AI-based graphics tools potentially supporting 40.0% of new interactive media projects, 2028.

- Regional Analysis: North America maintains leadership with a 40.6%, 2023 share of market revenue, while Europe holds an estimated: 25.0% share, 2023 and Asia Pacific accelerates toward an estimated: 30.0% share, 2034 as infrastructure investment and content innovation scale.

Deployment Mode

Cloud deployment continues to set the pace in 2025. Media and entertainment companies use cloud platforms to run generative AI workloads that rely on large datasets and high computational demand. Cloud environments captured more than 52 percent of global deployment in 2023 and are expected to hold a larger share through 2028 as studios, streaming platforms, and gaming firms shift more production tasks to remote pipelines. You gain access to pretrained models, scalable processing, and continuous updates without carrying the cost of in-house infrastructure. This matters for firms managing unpredictable workloads or operating on tight production cycles.

Cloud systems also support distributed teams. Production units in different countries can work on the same AI-generated assets in real time, which has become essential as remote collaboration remains part of the industry’s operating model. Cloud platforms now integrate AI-native rendering tools, real-time animation engines, and workflow orchestration systems that shorten delivery timelines across film, gaming, advertising, and post-production.

On-premise deployment maintains relevance for organizations that require strict control of sensitive assets. In 2025, large film studios, broadcasters, and security-focused enterprises continue to run proprietary models on local servers. These setups allow tighter control of high-value creative material and meet compliance requirements governing confidential or unreleased content. However, they also carry higher fixed costs and limited flexibility. As more organizations blend workloads across environments, hybrid models are gaining traction as a preferred configuration for companies that require both security and rapid scaling.

Type

Text-to-image tools continue to gain acceptance across production workflows. The segment grew from USD 299 million in 2022 and is expected to exceed USD 2.5 billion by 2032, supported by demand from advertising, digital publishing, and pre-visualization in film. Studios use these tools to create storyboards, concept art, and early-stage design assets in minutes rather than weeks. This improves creative throughput and reduces dependence on manual rendering during early phases of production.

Image-to-image generation remains essential in visual effects, animation, and digital art. Teams use these systems to refine textures, alter visual styles, and produce alternate scenes. Adoption rates continue to rise as creators shift repetitive editing and asset variations to automated tools. Music generation also advances quickly. Platforms use AI to produce background scores, thematic tracks, and adaptive soundscapes for games and streaming libraries. You see broader use among independent creators and production studios that require large volumes of audio assets.

Video generation and 3D modeling represent some of the fastest-growing categories. AI-based video tools support rapid creation of trailers, explainer clips, and short-form content, reducing production time and widening accessibility for marketing teams. In 3D modeling, AI enhances motion capture, scene building, and asset optimization used in gaming, animation, and mixed-reality applications. These tools reduce manual workload and speed up asset delivery for large-scale productions.

Application

Gaming remains the largest application area. The category grew from USD 477 million in 2022 to an expected multi-billion-dollar value by 2032 as developers use AI to build responsive environments, adaptive gameplay, and procedural assets. Generative AI supports character design, narrative branching, and content variations that enhance player engagement. You also see AI engines integrated into mobile, PC, and console titles as publishers aim to increase retention and accelerate content production.

Film and television continue to integrate AI across scripting, scene generation, localization, and visual effects. Production teams apply AI to automate rotoscoping, lighting adjustments, texture creation, and dialogue enhancement. The rise of global streaming heightens demand for faster post-production cycles and multilingual content, making AI-supported pipelines increasingly common. Advertising and marketing teams use generative AI to build large volumes of personalized assets. Brands rely on AI-driven images, videos, and audio creatives to adjust campaigns in real time.

Music and sound production benefit from AI tools that support composition, mixing, and automated mastering. These systems supply rapid variations of mood-based tracks for games, podcasts, and advertisements. VR and AR applications also grow as companies use AI to create immersive settings, responsive avatars, and training simulations. Additional uses in education, digital art, and interactive media highlight the expanding footprint of generative tools across creative sectors.

End-Use

Residential, commercial, and industrial environments across the entertainment ecosystem increasingly adopt generative AI as production processes shift to digital formats. Residential creators, including independent designers, streamers, and small studios, use text-to-image and AI video tools to scale content output at lower cost. Adoption rises among online creators as platforms prioritize short-form and personalized media.

Commercial end-users show the strongest growth. Studios, broadcasters, streaming services, and marketing agencies use generative models to reduce production times and expand multi-format content libraries. These organizations invest heavily in AI-supported editing, animation, dubbing, and automated advertising content. Industrial users, including large gaming publishers and high-budget film studios, rely on generative systems for advanced 3D modeling, environment design, and high-volume rendering tasks that require consistent output quality and strict workflow control.

Region

North America remains the leading market in 2025 with more than 40 percent share. The region benefits from strong investment in AI research, major cloud providers, and large entertainment ecosystems. US-based studios and streaming platforms adopt generative tools to accelerate production and personalization. Canada contributes growth through gaming and VFX clusters.

Europe follows with consistent expansion supported by active R&D programs in the UK, Germany, France, and the Nordics. Strict data-governance frameworks shape corporate adoption, while regional studios use AI to support localization, animation, and digital content distribution. Asia Pacific shows the fastest rise. Markets such as China, India, Japan, and South Korea increase usage across mobile entertainment, gaming, and e-commerce content. Wider internet access, growing creator economies, and investment in digital production hubs lift regional demand.

Latin America gains momentum as smartphone adoption and local content platforms increase the need for AI-supported creative tools. The Middle East and Africa continue to expand through investments in digital media, public-sector innovation programs, and emerging creator communities. The region sees rising interest in AI-generated content for marketing, entertainment, and virtual experiences.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud-Based

- On-Premise

By Type

- Text-to-Image Generation

- Image-to-Image Generation

- Music Generation

- Video Generation

- 3D Modeling and Animation

By Application

- Gaming

- Film & Television

- Advertising & Marketing

- Music & Sound Production

- Virtual Reality (VR) and Augmented Reality (AR)

- Other Applications

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.05 billion |

| Forecast Revenue (2034) | USD 19.8 billion |

| CAGR (2025-2034) | 27.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode (Cloud-Based, On-Premise), By Type (Text-to-Image Generation, Image-to-Image Generation, Music Generation, Video Generation, 3D Modeling and Animation), By Application (Gaming, Film & Television, Advertising & Marketing, Music & Sound Production, Virtual Reality (VR) and Augmented Reality (AR), Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Unity Software Inc., Adobe Inc., Synthesis AI, Nvidia Corporation, Autodesk, Inc., Alphabet Inc., IBM Corporation, OpenAI, Inc., Epic Games, Inc., Microsoft Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise), By Application (Gaming, Film & Television, Advertising & Marketing, Music Production, VR & AR), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Deployment Mode (Cloud-Based, On-Premise), By Application (Gaming, Film & Television, Advertising & Marketing, Music Production, VR & AR), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Deployment Mode (Cloud-Based, On-Premise), By Application (Gaming, Film & Television, Advertising & Marketing, Music Production, VR & AR), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Generative AI in Media and Entertainment Market?

The Generative AI in Media and Entertainment Market is projected to grow from USD 2.05 billion in 2025 to USD 19.8 billion by 2034, expanding at a CAGR of 27.1% during 2026–2034, driven by AI-powered content creation, virtual production, gaming, and personalized digital experiences.

Who are the major players in the Generative AI in Media and Entertainment Market?

Unity Software Inc., Adobe Inc., Synthesis AI, Nvidia Corporation, Autodesk, Inc., Alphabet Inc., IBM Corporation, OpenAI, Inc., Epic Games, Inc., Microsoft Corporation

Which segments covered the Generative AI in Media and Entertainment Market?

By Deployment Mode (Cloud-Based, On-Premise), By Type (Text-to-Image Generation, Image-to-Image Generation, Music Generation, Video Generation, 3D Modeling and Animation), By Application (Gaming, Film & Television, Advertising & Marketing, Music & Sound Production, Virtual Reality (VR) and Augmented Reality (AR), Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Generative AI in Media and Entertainment Market

Published Date : 31 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date