- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Generative AI in Video Creation Market Size, Growth | CAGR 23.6%

Global Generative AI in Video Creation Market Size, Share & Analysis By Deployment Type (On-premise, Cloud), By Application (Marketing, Education, Entertainment, Social Media), By End-Users (Large Enterprises, SMEs, Individual Content Creators), Innovation Roadmap & Forecast 2025–2034

Report Overview

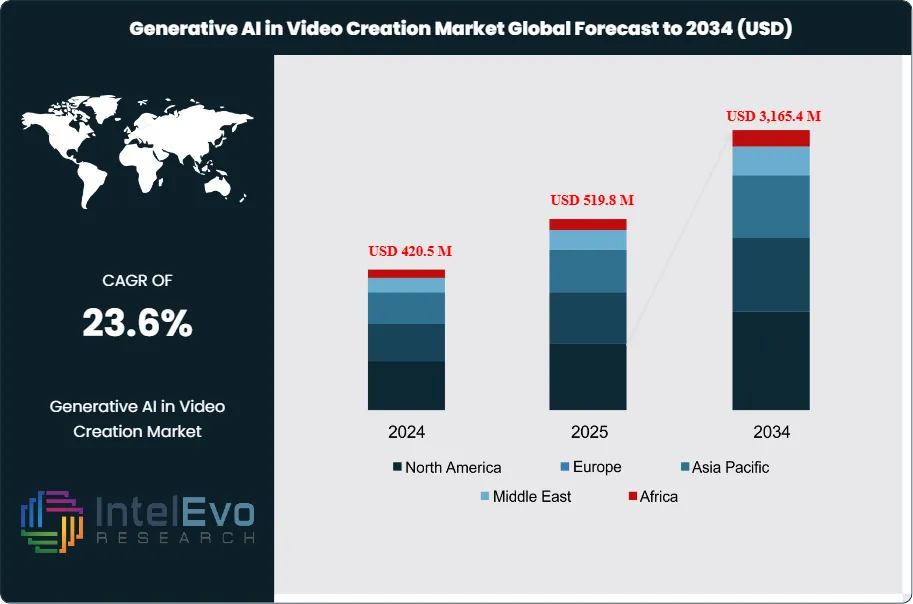

The Generative AI in Video Creation market is valued at approximately USD 420.5 million in 2024 and is projected to reach nearly USD 3,165.4 million by 2034, registering a strong CAGR of around 23.6% during 2025–2034. This accelerated growth reflects the rising adoption of AI-powered automated video tools across marketing, entertainment, education, and digital content ecosystems.

Get More Information about this report -

Request Free Sample ReportThis market is undergoing rapid expansion, driven by the escalating demand for dynamic, personalized video content across media, advertising, education, and corporate sectors. As digital content consumption reaches new heights globally, businesses are under increasing pressure to produce high-quality, engaging videos at scale and speed. Generative AI, powered by advanced deep learning algorithms and neural networks, has emerged as a transformative solution—enabling automatic creation of contextually relevant, emotionally resonant video content while significantly reducing production time and cost.

In 2023, North America led the global market with a dominant 42% revenue share, equivalent to USD 141 million, owing to the early adoption of AI technologies and strong presence of tech innovators. However, Asia Pacific is expected to witness accelerated growth through the forecast period, driven by expanding digital economies, increased investments in AI R&D, and a growing base of content creators and e-learning platforms across emerging markets.

Key growth drivers include the surge in AI-generated marketing content, rising demand for automated training and educational materials, and the proliferation of personalized video experiences. AI platforms such as Synthesia have demonstrated measurable efficiency gains—reducing video production time by 34% for corporate users—thus supporting widespread enterprise adoption. Additionally, the ongoing refinement of generative models is enabling higher-quality outputs, further bridging the gap between human-created and AI-generated content.

However, challenges such as ethical concerns, misuse of synthetic media, and lack of standard regulations remain critical barriers. The parallel rise of the DeepFake AI market, projected to reach USD 18.99 billion by 2033, underscores the urgent need for frameworks to balance innovation with responsible use.

Consumer sentiment is also shifting—52% of users now feel comfortable interacting with AI-generated content, and 43% believe it matches traditional production standards. As confidence in AI capabilities grows, adoption will deepen, opening new opportunities across journalism, product marketing, e-commerce, and immersive digital storytelling. With the broader generative AI market projected to exceed USD 255 billion by 2033, video creation stands out as one of its most impactful and fast-evolving applications.

, By Application (Marketing, Education, Entertainment, Social Media), By End-Users (Large Enterprises, SMEs, Individual Content Creators), Innovation Roadmap & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Generative AI in Video Creation market is projected to grow from USD 420.5 million in 2024 to USD 3,165.4 million by 2034, registering a CAGR of 23.6%. Growth is fuelled by rising demand for automated content production, increasing personalization in digital marketing, and ongoing advancements in AI-powered video generation tools.

- Deployment Type: The cloud-based segment led the market in 2023 with over 55% share, driven by its scalability, cost-efficiency, and ease of integration with existing video production workflows, particularly for remote teams and content platforms.

- Application: The marketing and advertising segment accounted for more than 34% of total revenue in 2023, as enterprises increasingly adopted AI-generated videos for campaign personalization, customer engagement, and performance optimization across digital channels.

- Enterprise Size: Large enterprises dominated the market with a 60%+ share in 2023, owing to their early adoption of AI tools, higher content production volumes, and greater investment capacity in emerging technologies such as generative video models.

- Driver: A key growth driver is the operational efficiency offered by AI platforms like Synthesia, which have reduced training video production time by 34%, enabling enterprises to streamline workflows and scale content delivery without proportional increases in cost or manpower.

- Restraint: Concerns surrounding deepfake misuse and content authenticity pose a significant restraint. With the DeepFake AI market projected to reach USD 18.99 billion by 2033, regulatory uncertainty and ethical risks could hinder broader adoption in sensitive sectors such as journalism and public communications.

- Opportunity: The Asia Pacific region presents a major growth opportunity, supported by rising digital content consumption, increased AI investments, and growing demand for video-based learning and marketing across emerging economies. The region is expected to witness above-average CAGR through 2033.

- Trend: A notable trend is the rise of AI-driven video personalization and localization, with companies deploying generative tools to create region-specific, language-adaptive content at scale—reshaping global content strategies and enhancing audience engagement.

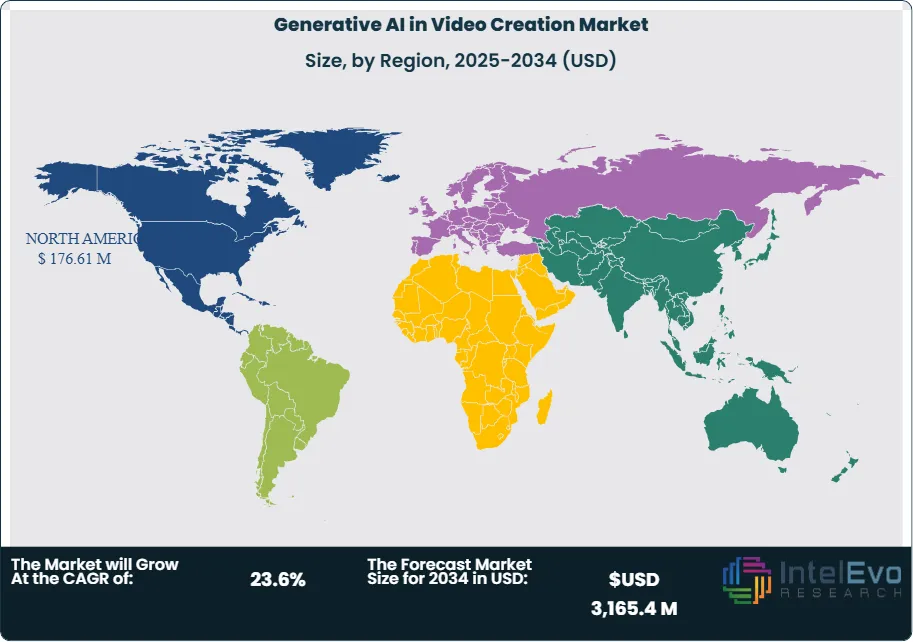

- Regional Analysis: North America led the market in 2023 with over 42% revenue share (USD 141 million), supported by early technology adoption and a mature digital media ecosystem. However, Asia Pacific is expected to be the fastest-growing region, driven by expanding internet penetration and AI-backed content creation platforms.

Deployment Type Analysis

As of 2025, cloud-based deployment continues to dominate the Generative AI in Video Creation market, accounting for over 55% of total market share. This growth is attributed to the scalability, accessibility, and cost-efficiency that cloud infrastructure offers. Cloud platforms eliminate the need for heavy upfront investments in hardware, making high-performance AI tools accessible to a broader user base, including startups, SMEs, and individual creators. With flexible subscription-based pricing models and reduced maintenance costs, cloud deployment is rapidly becoming the preferred model for both enterprise and independent users.

The increasing complexity of generative AI models, especially those requiring high computational power for rendering videos and real-time personalization, further drives demand for cloud services. Additionally, cloud-based platforms support seamless integration with other digital tools and enable real-time collaboration among distributed teams—an essential capability in today’s remote-first work culture. While on-premise deployment remains relevant for organizations with strict data control or compliance needs, its growth is relatively constrained due to high infrastructure costs and limited scalability. Consequently, cloud deployment is expected to maintain its lead, supported by growing demand for agility, remote access, and AI-driven innovation.

Application Analysis

Marketing applications continue to lead in the adoption of generative AI video tools, capturing more than 34% of the market in 2025. The marketing sector is leveraging AI to create personalized, data-driven video content that enhances audience engagement and campaign performance. From automated ad generation to product explainers and influencer-style videos, AI-generated video content enables brands to communicate more efficiently and at scale. Companies are increasingly using behavioral data and CRM insights to tailor video messaging, resulting in higher conversion rates and improved ROI.

In addition to marketing, applications in education and training are expanding significantly. AI is being used to develop localized training materials, onboarding content, and explainer videos—cutting production time and costs by up to 40% compared to traditional methods. Entertainment and social media also represent high-growth segments, with generative tools enabling the rapid creation of interactive content, virtual avatars, and real-time video responses. As video consumption continues to surge across digital platforms, the role of generative AI in powering hyper-personalized and on-demand video creation is expected to intensify, particularly in short-form and vertical content strategies.

End-User Analysis

Large enterprises remain the primary users of generative AI video solutions, accounting for more than 60% of the market share in 2025. These organizations have the capital and infrastructure to adopt sophisticated AI systems and integrate them into their expansive marketing, communication, and training ecosystems. Multinational corporations are using AI to produce region-specific, multilingual video content—enhancing their localization efforts and improving global engagement.

Moreover, large enterprises typically work with complex data sets, allowing generative AI to deliver highly tailored video content based on behavioral insights, purchase patterns, and demographic profiles. This level of personalization supports deeper brand-audience connections and increased campaign efficiency. Meanwhile, adoption among SMEs and individual creators is on the rise, driven by the democratization of AI tools through cloud platforms and freemium models. As generative video tools become more user-friendly and accessible, this segment is expected to contribute significantly to market growth in the coming years.

Regional Analysis

North America continues to lead the global Generative AI in Video Creation market, representing over 42% of the market share in 2025, with revenues surpassing USD 141 million. This dominance is underpinned by strong investment in AI infrastructure, early adoption of generative technologies, and the presence of leading tech players such as Microsoft, Google, Meta, and a vibrant startup ecosystem. Favorable government policies, combined with a digitally mature user base, contribute to widespread implementation across industries.

Looking ahead, the Asia Pacific region is poised for the highest growth, driven by rapid digitalization, expanding internet penetration, and increasing adoption of video-first platforms. Countries like China, India, and South Korea are witnessing a surge in demand for AI-powered video tools, particularly in e-learning, e-commerce, and social media. Meanwhile, Europe is focusing on regulatory frameworks and ethical AI, which may moderate growth but foster long-term stability. Latin America and the Middle East & Africa are emerging markets with untapped potential, where rising smartphone usage and social media engagement are likely to drive adoption in the years ahead.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Type

- On-premise

- Cloud

By Application

- Marketing

- Education

- Entertainment

- Social Media

- Others

By End-Users

- Large Enterprises

- SMEs

- Individual Content Creators

By Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 420.5 M |

| Forecast Revenue (2034) | USD 3,165.4 M |

| CAGR (2024-2034) | 23.6% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Type (On-premise, Cloud), By Application (Marketing, Education, Entertainment, Social Media, Others), By End-Users (Large Enterprises, SMEs, Individual Content Creators) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Elai.io, Wibbitz, DeepBrain, Runway ML, Animoto, Pictory, Rephrase AI, Synthesia, Magisto (a Vimeo company), Lumen5, Other key players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Marketing, Education, Entertainment, Social Media), By End-Users (Large Enterprises, SMEs, Individual Content Creators), Innovation Roadmap & Forecast 2025–2034")

, By Application (Marketing, Education, Entertainment, Social Media), By End-Users (Large Enterprises, SMEs, Individual Content Creators), Innovation Roadmap & Forecast 2025–2034")

, By Application (Marketing, Education, Entertainment, Social Media), By End-Users (Large Enterprises, SMEs, Individual Content Creators), Innovation Roadmap & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Generative AI in Video Creation Market

Published Date : 02 Dec 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date