- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Genome Editing Market Size, Share & Growth Forecast | 17.7% CAGR

Global Genome Editing Market Size, Share & Analysis By Delivery Method (Ex-vivo, In-vivo), By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) Industry Developments, Regulatory Trends & Forecast 2025–2034

Report Overview

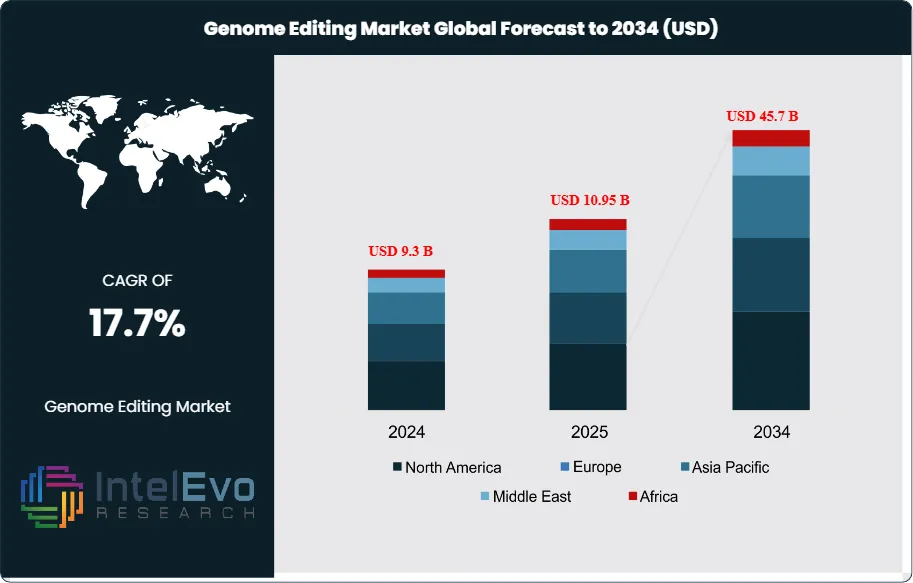

The genome editing market size is expected to be worth around USD 45.7 billion by 2034, from USD 9.3 billion in 2024, growing at a CAGR of 17.7% during the forecast period from 2025 to 2034. Genome editing is moving beyond its origins as a research tool to become a cornerstone of biotechnology, with applications spanning healthcare, agriculture, and industrial sciences. Breakthroughs in CRISPR-Cas9, TALENs, base editing, and prime editing are enabling researchers to precisely manipulate genes with higher efficiency and fewer errors. These advances are fueling adoption in therapeutic pipelines, crop engineering, and disease modeling as organizations seek targeted, cost-efficient solutions.

Get More Information about this report -

Request Free Sample ReportHealthcare remains the leading driver, as gene and cell therapies using genome editing enter late-stage clinical trials for rare genetic diseases, oncology, and chronic conditions. The ability to directly repair or replace faulty genes is improving treatment outcomes and lowering long-term care costs. Meanwhile, biotech and pharmaceutical companies are significantly scaling investments into genome editing R&D, signaling robust commercial potential.

Agriculture is emerging as a complementary growth engine, with editing tools being deployed to engineer climate-resilient, pest-resistant, and nutrient-rich crops. This is especially critical for Asia Pacific and Africa, where climate challenges and food security concerns are pressing. Collaborations between biotech firms and agricultural institutes are further accelerating adoption in this sector.

Challenges persist, including regulatory complexities, ethical concerns, and high costs of therapy development. Yet, improvements in precision editing, AI-enabled analytics, and favorable regulatory progress are helping to lower barriers and expand adoption.

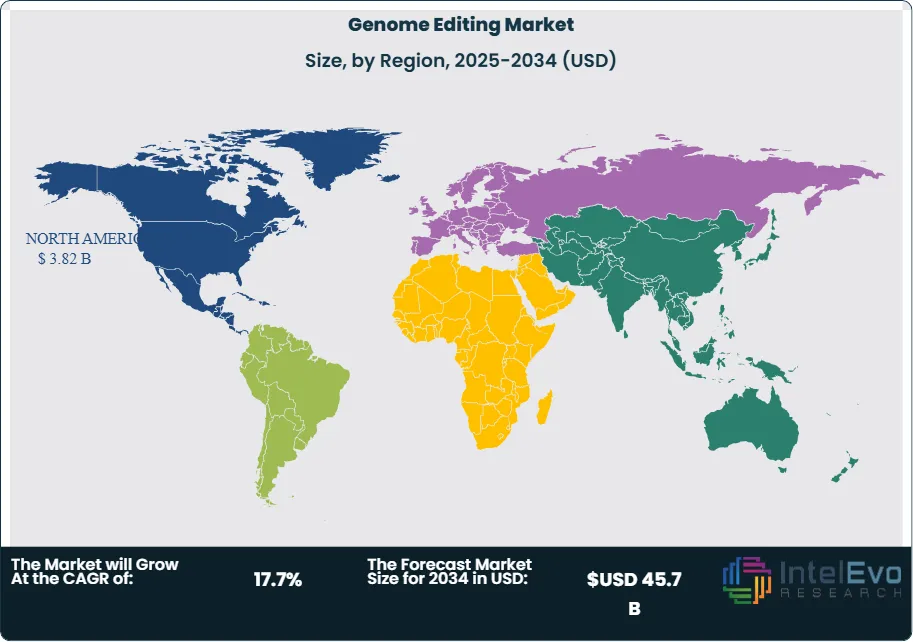

Regionally, North America continues to lead with just over 41% of revenues, supported by robust research infrastructure and early clinical approvals. Europe maintains steady momentum with policy-driven innovation clusters, while Asia Pacific is expected to record the fastest growth, underpinned by government-led genomics programs and agricultural biotechnology expansion.

, By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) Industry Developments, Regulatory Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The genome editing market generated USD 9.3 billion in 2024 and is projected to reach USD 45.7 billion by 2034, expanding at a CAGR of 17.7%. Growth is driven by rising demand for precision medicine, expanding agricultural biotechnology, and continuous improvements in editing platforms.

- Delivery Method: Ex-vivo editing approaches dominated with 63.5% share in 2024, reflecting their established use in controlled laboratory and clinical environments, particularly in cell-based therapies where accuracy and safety are paramount.

- Technology: CRISPR/Cas9 accounted for 55.3% of revenues in 2024, benefiting from its cost-effectiveness, versatility, and strong adoption across therapeutic development, agriculture, and academic research.

- Application: Genetic engineering represented 72.6% of the market in 2024, supported by applications in crop enhancement, livestock genetics, and industrial biotechnology, alongside its growing role in basic research.

- End Use: Biotechnology and pharmaceutical companies held the largest share at 60.1%, reflecting increasing reliance on genome editing for drug discovery, clinical trial pipelines, and advanced therapies.

- Driver: Rising investments in personalized medicine and successful preclinical demonstrations of genome editing in rare disease therapies are reinforcing its role as a transformative pillar of modern healthcare.

- Restraint: Ethical concerns, high R&D costs, and evolving regulatory hurdles—particularly surrounding germline modification—continue to delay widespread clinical adoption.

- Opportunity: Expanding applications in agricultural biotechnology, including pest-resistant crops and climate-resilient varieties, offer significant growth potential amid global food security concerns.

- Trend: Next-generation platforms such as base and prime editing are gaining momentum, with collaborations between biotech firms and AI-driven analytics providers accelerating innovation and reducing risk.

- Regional Analysis: North America led with just over 41% market share in 2024, supported by strong research infrastructure and funding, while Asia Pacific is set to be the fastest-growing region through 2034 due to government-backed initiatives and agricultural adoption.

Delivery Method Analysis

Ex-vivo genome editing continues to dominate the market, accounting for 63.7% of revenues in 2024, and is expected to expand further through 2025 and beyond. This method enables the precise modification of patient-derived cells outside the body before reinfusion, ensuring greater control over editing accuracy and reducing the likelihood of adverse outcomes. Its proven effectiveness in areas such as oncology and rare genetic disorders is fueling demand, particularly in cell-based therapies like CAR-T and stem cell applications.

The rising emphasis on personalized medicine is a major driver of ex-vivo adoption. With more clinical trials targeting diseases such as sickle cell anemia and certain forms of cancer, pharmaceutical and biotech companies are prioritizing ex-vivo strategies due to their higher safety profile and ability to generate reproducible therapeutic results. Continuous improvements in delivery systems, including electroporation and viral vectors, are expected to further enhance the clinical viability of this approach.

Technology Analysis

CRISPR/Cas9 remains the leading genome editing technology, commanding 55.5% of the global market in 2024 and projected to strengthen its position through 2030. Its dominance is attributed to its unmatched efficiency, versatility, and relatively low cost compared with older methods such as zinc finger nucleases (ZFNs), TALENs/MegaTALs, and meganucleases. The ability to design CRISPR systems rapidly and target specific DNA sequences has made it the preferred tool for both research and therapeutic development.

As of 2025, advances in CRISPR delivery and specificity—such as base editing and prime editing—are addressing early limitations like off-target effects. This technological evolution is expected to accelerate clinical adoption in areas such as genetic disorder therapies, cancer treatment, and agricultural biotechnology. While CRISPR leads, niche demand persists for TALENs and ZFNs, particularly in applications requiring high precision or proprietary platforms, ensuring a competitive but CRISPR-driven landscape.

Application Analysis

Genetic engineering applications accounted for 72.8% of revenues in 2024, underscoring the widespread use of genome editing in agriculture, industrial biotechnology, and animal research. Plant genetic engineering is particularly prominent, as genome editing tools are being applied to develop drought-resistant, pest-tolerant, and nutritionally enhanced crops. Animal genetic engineering is also gaining traction, with applications in disease resistance and livestock improvement, reinforcing the segment’s strong position.

On the clinical side, genome editing is rapidly advancing toward therapeutic use. Improved precision and safety in CRISPR/Cas9 systems are enabling experimental treatments for inherited genetic disorders, oncology, and infectious diseases. With multiple therapies in late-stage clinical trials, the clinical application segment is projected to grow steadily, supported by increasing investments from pharmaceutical companies and growing regulatory clarity around gene-editing therapeutics.

End Use Analysis

Biotechnology and pharmaceutical companies dominate the market, representing 60.2% of revenues in 2024, and are expected to maintain leadership as gene-editing technologies move deeper into drug discovery and therapeutic pipelines. These companies are driving innovation in personalized medicine by developing curative therapies for conditions previously deemed untreatable. Notable investments in oncology, regenerative medicine, and rare disease treatment underscore the sector’s reliance on genome editing to accelerate drug development and clinical success rates.

Academic and government research institutes remain essential contributors to fundamental research, expanding the knowledge base and enabling early innovation in editing tools. Contract research organizations (CROs) are also playing a growing role by supporting biotech firms in clinical trial execution and specialized genome editing projects, helping to scale new therapies more efficiently.

Regional Analysis

North America continues to lead the global market, holding 41.1% of revenues in 2024 and maintaining its dominance in 2025. The region’s leadership stems from strong R&D infrastructure, significant public and private investment, and supportive regulatory pathways. Milestones such as Vertex Pharmaceuticals and CRISPR Therapeutics’ Biologics License Application submission to the U.S. FDA for a CRISPR-based therapy highlight the region’s pivotal role in advancing clinical applications.

Asia Pacific is emerging as the fastest-growing region, driven by increasing investments in life sciences, growing healthcare demand, and government-backed genomic initiatives. Countries such as China, Japan, and India are actively expanding their gene-editing capabilities, both in medical research and agricultural biotechnology. Local innovation, supported by strong policy backing and expanding biotech ecosystems, positions the region as a major growth engine for the global market.

Europe maintains steady growth, supported by strong ethical oversight, public funding programs, and active clinical research hubs in Germany, France, and the UK. Meanwhile, Latin America and the Middle East & Africa remain in earlier stages of adoption but show long-term potential as healthcare modernization and agricultural biotechnology gain momentum.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Delivery Method

- Ex-vivo

- In-vivo

By Technology

- CRISPR/Cas9

- Meganuclease

- TALENs/MegaTALs

- ZFN

- Others

By Application

- Genetic Engineering

- Animal Genetic Engineering

- Cell Line Engineering

- Plant Genetic Engineering

- Others

- Clinical Applications

- Diagnostics

- Therapy Development

By End-use

- Biotechnology & Pharmaceutical Companies

- Academic & Government Research Institutes

- Contract Research Organizations

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 9.3 B |

| Forecast Revenue (2034) | USD 45.7 B |

| CAGR (2024-2034) | 17.7% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Delivery Method (Ex-vivo, In-vivo), By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN, Others), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Sangamo Therapeutics, Recombinetics, Precision BioSciences, LGC, Editas Medicine, CRISPR Therapeutics, Cellectis, AstraZeneca, Intellia Therapeutics, Beam Therapeutics, Caribou Biosciences, Thermo Fisher Scientific, Lonza Group, Merck KGaA, Horizon Discovery |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) Industry Developments, Regulatory Trends & Forecast 2025–2034")

, By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) Industry Developments, Regulatory Trends & Forecast 2025–2034")

, By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations) Industry Developments, Regulatory Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Genome Editing Market?

The Genome Editing Market is projected to grow from USD 9.3 Billion in 2024 to USD 45.7 Billion by 2034, expanding at a CAGR of 17.7%. Advances in CRISPR, TALENs, base editing, and prime editing are revolutionizing biotechnology, driving innovation across healthcare, agriculture, and life sciences.

Who are the major players in the Genome Editing Market?

Sangamo Therapeutics, Recombinetics, Precision BioSciences, LGC, Editas Medicine, CRISPR Therapeutics, Cellectis, AstraZeneca, Intellia Therapeutics, Beam Therapeutics, Caribou Biosciences, Thermo Fisher Scientific, Lonza Group, Merck KGaA, Horizon Discovery

Which segments covered the Genome Editing Market?

By Delivery Method (Ex-vivo, In-vivo), By Technology (CRISPR/Cas9, Meganuclease, TALENs/MegaTALs, ZFN, Others), By Application (Genetic Engineering, Clinical Applications), By End-use (Biotechnology & Pharmaceutical Companies, Academic & Government Research Institutes, Contract Research Organizations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date