- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global GLP-1 Drug Delivery Systems Market Size, Share | CAGR 13.8%

Global GLP-1 Drug Delivery Systems Market Size, Share & Industry Analysis By Delivery Device Type (Prefilled Pens, Auto-Injectors, Wearable Injectors, Syringes, Smart Injection Devices and Oral Delivery Platforms), By Application (Type 2 Diabetes Management, Obesity and Weight Management, Cardiovascular Risk Reduction and Metabolic Disorders), By End User, Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Technological Advancements, Pipeline Innovations and Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

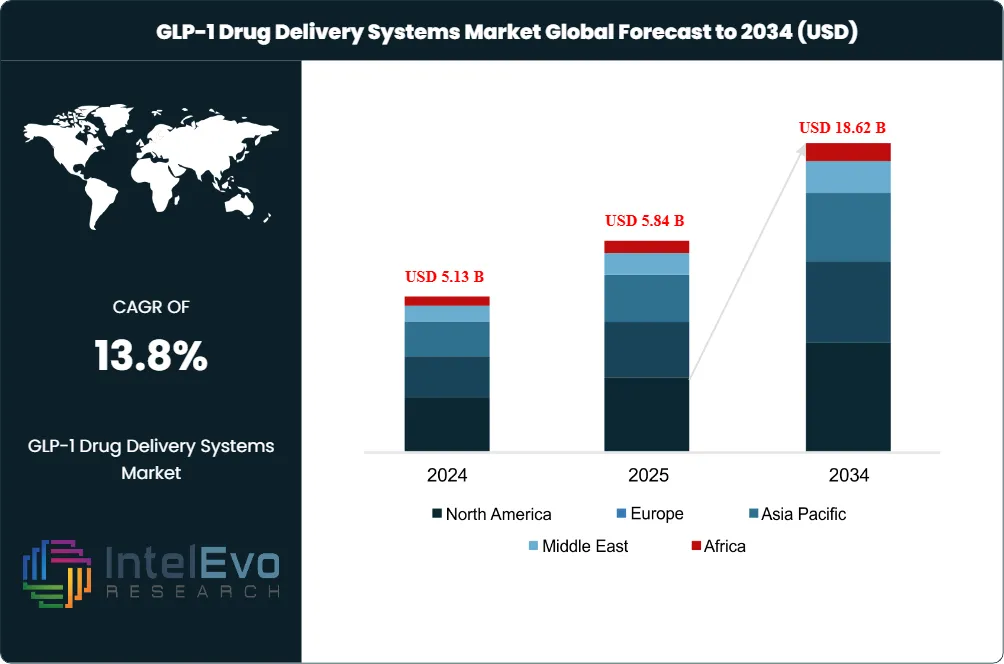

| USD 5.84 Billion | USD 18.62 Billion | 13.8% | North America, 57.2% |

The GLP-1 Drug Delivery Systems Market was valued at USD 5.13 Billion in 2024 and USD 5.84 Billion in 2025. The market is projected to reach USD 18.62 Billion by 2034, expanding at a CAGR of 13.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.78 Billion over the analysis period. The GLP-1 drug delivery systems market encompasses the devices, technologies, and primary packaging solutions that enable the administration of glucagon-like peptide-1 receptor agonist therapies, including prefilled pen injectors, disposable and reusable autoinjectors, oral absorption enhancement platforms, implantable sustained-release systems, smart connected injection devices, and cold chain packaging required for peptide stability.

Get More Information about this report -

Request Free Sample ReportThe GLP-1 receptor agonist drug market reached approximately USD 64.4 Billion in 2025, and device-level delivery systems represent approximately 9.1% of total drug product value, a ratio that is increasing because delivery platform differentiation is becoming a primary competitive battleground. GLP-1 therapies are projected to reach 30 million patients in the United States alone by 2030, translating to an estimated 1 billion injections per year in the U.S. market. Novo Nordisk's FlexTouch prefilled pen and Eli Lilly's KwikPen are the two dominant device platforms, collectively delivering over 85% of all injectable GLP-1 doses globally. In February 2026, Eli Lilly received FDA label expansion for the Zepbound KwikPen, a four-dose, single-patient-use prefilled pen that consolidates a full month of tirzepatide therapy into one device, priced at USD 299 per month through LillyDirect.

Oral drug delivery technology is the fastest-growing subsegment, driven by the clinical success of Eli Lilly's orforglipron, which completed three Phase 3 trials in 2025 and triggered global regulatory submissions. Orforglipron is a small-molecule GLP-1 agonist taken without food or water restrictions, a formulation breakthrough that eliminates the absorption enhancement technology (SNAC, sodium N-[8-(2-hydroxybenzoyl) amino] caprylate) required by Novo Nordisk's oral semaglutide (Rybelsus). The shift toward oral delivery is projected to capture 25 to 30% of all GLP-1 administrations by 2034, up from approximately 12.7% in 2025. Monthly injectable platforms, led by Pfizer/Metsera's MET-097i entering Phase 3, represent a parallel innovation track that could reduce annual device consumption per patient from 52 autoinjectors to 12 pen doses.

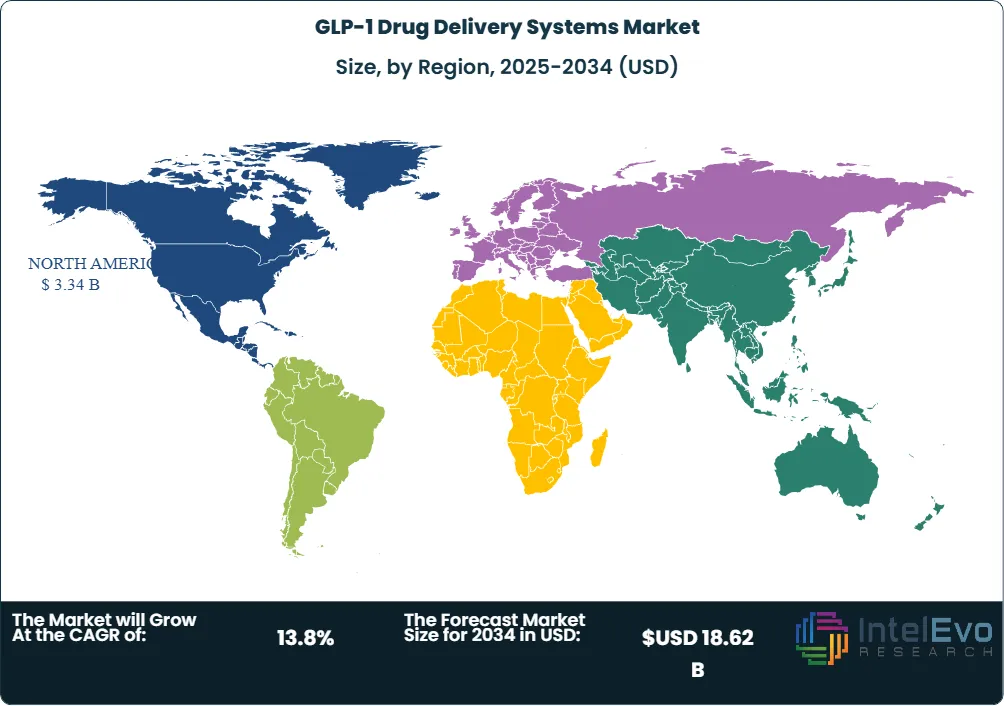

North America held 57.2% of the GLP-1 drug delivery systems market in 2025 at approximately USD 3.34 Billion, reflecting the concentration of Novo Nordisk and Eli Lilly manufacturing in the United States. Eli Lilly committed USD 27 Billion to U.S. manufacturing expansion in 2025, including a USD 3.5 Billion injectable medicine facility in Pennsylvania. Europe accounted for 23.8% at USD 1.39 Billion, where device manufacturers Ypsomed (Switzerland), Gerresheimer (Germany), SHL Medical (Sweden/Taiwan), and Stevanato Group (Italy) supply critical prefilled syringe, autoinjector, and pen injector platforms. Asia Pacific represented 13.4% at USD 783 million, with device contract manufacturing in China and India expanding to serve global pharmaceutical supply chains.

Market Definition & Scope

The GLP-1 drug delivery systems market is defined as the global commercial segment for devices, technologies, and primary packaging solutions that enable administration of GLP-1 receptor agonist therapies to patients. The market encompasses five categories: injectable delivery devices (prefilled multi-dose pen injectors, single-use disposable autoinjectors, reusable autoinjectors with replaceable cartridges); oral drug delivery platforms (absorption enhancers such as SNAC for oral semaglutide, small-molecule oral formulations requiring no permeation enhancers); implantable and sustained-release systems (osmotic pump implants, biodegradable polymer depots); connected and smart injection devices (Bluetooth-enabled dose tracking, companion mobile applications); and specialized packaging and cold chain systems (temperature-controlled shipping, prefilled syringe glass and polymer barrels, plunger systems).

This analysis includes device platforms sold as combination products (drug-device combinations regulated under FDA 21 CFR Part 4 and EU MDR) as well as standalone device components supplied by contract device manufacturers to pharmaceutical companies. The report explicitly excludes the GLP-1 drug substance and active pharmaceutical ingredient value, insulin delivery devices not used for GLP-1 therapies, infusion pumps, and manual vial-and-syringe administration. The GLP-1 drug delivery systems market operates at the intersection of the broader pen and injector drug delivery devices market (USD 114.67 Billion in 2025) and the GLP-1 receptor agonist therapeutics market (USD 64.4 Billion in 2025).

, By Application (Type 2 Diabetes Management, Obesity and Weight Management, Cardiovascular Risk Reduction and Metabolic Disorders), By End User, Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Technological Advancements, Pipeline Innovations and Forecast 2026-2034")

Key Takeaways

- Market Growth: The GLP-1 drug delivery systems market grew from USD 5.84 Billion in 2025 to a projected USD 18.62 Billion by 2034, at a 13.8% CAGR, representing USD 12.78 Billion in absolute dollar opportunity.

- Segment Dominance (By Device Type): Prefilled pen injectors held the largest share at 48.3% in 2025 at approximately USD 2.82 Billion, because multi-dose pens (delivering 4 weekly doses per device) remain the most cost-efficient injectable format, requiring only 13 pens per patient per year compared to 52 single-use autoinjectors.

- Segment Dominance (By End-User): Home-based self-administration accounted for 72.4% of end-user demand in 2025 at approximately USD 4.23 Billion, reflecting the structural shift from clinic-based injection to patient self-care for chronic metabolic disease management.

- Driver: The projected expansion to 30 million GLP-1 patients in the U.S. by 2030 will generate demand for approximately 1 billion injections per year, creating device manufacturing capacity requirements that exceed current installed production lines by 3 to 4 times.

- Restraint: Cold chain logistics requirements for peptide-based GLP-1 injectables add USD 2 to USD 5 per dose in distribution costs, limiting penetration in regions with unreliable temperature-controlled supply chains across sub-Saharan Africa, South Asia, and Latin America.

- Opportunity: Oral GLP-1 delivery platforms represent the largest growth opportunity, projected to shift from 12.7% to 25–30% of all GLP-1 administrations by 2034. Eli Lilly's orforglipron eliminates the need for permeation enhancers, simplifying oral manufacturing compared to Novo Nordisk's SNAC-dependent Rybelsus formulation.

- Trend: Multi-dose pen configurations are replacing single-use autoinjectors for cost and sustainability reasons. Eli Lilly's Zepbound KwikPen (FDA expanded February 2026) consolidates four weekly doses into one device, reducing per-patient device consumption by 75% and easing assembly capacity constraints.

- Regional: North America led the GLP-1 drug delivery systems market with 57.2% share valued at USD 3.34 Billion in 2025, anchored by the U.S. manufacturing concentration of Novo Nordisk and Eli Lilly, plus Eli Lilly's USD 3.5 Billion Pennsylvania injectable facility investment.

Key Insights Summary

- The projected 30 million GLP-1 patients in the U.S. by 2030 would generate demand for approximately 1.5 billion injection devices annually if served exclusively by single-use autoinjectors, or approximately 390 million pen injectors in multi-dose configurations (industry estimates, 2025).

- Eli Lilly received FDA label expansion for the Zepbound KwikPen in February 2026, a four-dose prefilled pen consolidating one month of tirzepatide therapy at a self-pay price of USD 299 per month through LillyDirect, reducing device component requirements by 75% compared to weekly autoinjectors.

- Novo Nordisk's FlexTouch pen platform delivers over 85% of all semaglutide injectable doses globally. The FlexTouch uses a spring-assisted plunger mechanism with 10mm-accuracy dose dialing, compatible with NovoFine Plus and NovoTwist needles.

- Gerresheimer invested USD 180 million in expanding its Peachtree City, Georgia facility in May 2024 to increase production of medical systems including autoinjectors. In April 2025, Gerresheimer partnered with Injecto to launch silicone oil-free and PFAS-free syringe systems.

- BD (Becton Dickinson) collaborated with Ypsomed in October 2024 to integrate BD's Neopak XtraFlow Glass Prefillable Syringe with Ypsomed's YpsoMate 2.25 autoinjector, enabling delivery of high-viscosity biologic drugs exceeding 15 centipoise.

- SCHOTT Pharma launched a 5.5 mL large-volume prefillable staked-needle glass syringe as part of its syriQ BioPure platform in October 2025, targeting the growing demand for large-volume subcutaneous biologic injections.

Competitive Landscape Overview

The GLP-1 drug delivery systems market operates across two competitive tiers: integrated pharmaceutical companies that design proprietary device-drug combinations (Novo Nordisk, Eli Lilly) and contract device manufacturers that supply platforms to multiple pharma clients (Ypsomed, SHL Medical, Stevanato Group, Gerresheimer, BD, Owen Mumford, Nemera). Novo Nordisk and Eli Lilly control the end-market through their proprietary FlexTouch and KwikPen platforms, but they depend on specialized component suppliers for glass barrels, elastomeric closures, spring mechanisms, and needle systems. Ypsomed supplies the YpsoMate autoinjector platform and UnoPen pen injector to over 25 pharmaceutical partners globally. SHL Medical manufactures the Molly disposable autoinjector platform used across multiple GLP-1 and biologic drug programs. Stevanato Group produces glass prefilled syringes, cartridges, and its Aidaptus hybrid autoinjector, positioning itself as a full-stack supplier from primary containment through final device assembly. The competitive dynamic is shifting because oral GLP-1 formulations threaten to reduce injectable device volumes, while monthly dosing formats (Pfizer/Metsera MET-097i) could reduce annual device consumption per patient from 52 units to 12.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform/Product | Geo Strength | Founded | Recent Strategic Move |

| Novo Nordisk | Denmark | Leader | FlexTouch pen, PDS290 implant | Global | 1923 | Oral semaglutide daily pill FDA filing (2025) |

| Eli Lilly | US | Leader | KwikPen, Tempo Pen autoinjector | Global | 1876 | Zepbound KwikPen 4-dose FDA approval (Feb 2026) |

| Ypsomed | Switzerland | Challenger | YpsoMate AI, UnoPen, ServoPen | Global | 2003 | BD NeopakXtraFlow collaboration (Oct 2024) |

| SHL Medical | Sweden/TW | Challenger | Molly disposable autoinjector | Global | 1989 | GLP-1 platform capacity expansion (2025) |

| Stevanato Group | Italy | Challenger | Aidaptus AI, Alina pen, syriQ | Global | 1949 | GLP-1 integrated solutions launch (2025) |

| Gerresheimer | Germany | Challenger | Gx RTF syringe, autoinjector | Global | 1864 | USD 180M Georgia expansion (May 2024) |

| BD | US | Challenger | Neopak PFS, Physioject AI | Global | 1897 | Ypsomed high-viscosity collaboration (Oct 2024) |

| SCHOTT Pharma | Germany | Niche | syriQ BioPure PFS platform | Global | 1884 | 5.5mL large-volume PFS launch (Oct 2025) |

By Device Type

Prefilled pen injectors dominated the GLP-1 drug delivery systems market with 48.3% share in 2025 at approximately USD 2.82 Billion. Multi-dose prefilled pens, including Novo Nordisk's FlexTouch (delivering Ozempic and Wegovy) and Eli Lilly's KwikPen (delivering Mounjaro and Zepbound), are the workhorse devices for weekly GLP-1 injection. A single pen typically contains four weekly doses, requiring only 13 pens per patient per year. The Zepbound KwikPen received FDA expanded labeling in February 2026 for four-dose monthly configuration at USD 299 self-pay price. Pen injectors offer dose titration flexibility that is critical during GLP-1 therapy initiation, when patients escalate from low starting doses over 8 to 16 weeks. Ypsomed's UnoPen and Stevanato Group's Alina pen injector platform compete for contract supply to pharmaceutical companies outside the Novo-Lilly duopoly.

Single-use disposable autoinjectors held 24.7% share at approximately USD 1.44 Billion. These spring-loaded devices deliver a fixed single dose from a prefilled syringe, used for Eli Lilly's Trulicity (dulaglutide) and emerging GLP-1 biosimilar products. SHL Medical's Molly platform and Ypsomed's YpsoMate are the leading contract-manufactured autoinjector designs. For 10 million patients, single-use autoinjectors require production of 520 million units annually versus 130 million multi-dose pens, creating a 4x device volume differential that impacts manufacturing capacity, packaging waste, and unit economics.

Oral drug delivery systems accounted for 15.8% at approximately USD 923 million. Novo Nordisk's Rybelsus uses SNAC (sodium N-[8-(2-hydroxybenzoyl) amino] caprylate), an absorption enhancer that enables oral semaglutide to cross the gastric epithelium at approximately 1% bioavailability. Eli Lilly's orforglipron, a non-peptide small-molecule GLP-1 agonist, eliminates the need for permeation enhancers entirely, which could reduce oral formulation manufacturing complexity and cost. OPKO Health and Entera Bio announced an agreement in March 2025 to advance an oral GLP-1/glucagon tablet using Entera's oral peptide delivery technology. The oral segment is projected to grow at 22.8% CAGR through 2034 as orforglipron and competing oral candidates reach market authorization.

Connected and smart injection devices held 6.4% at approximately USD 374 million. Bluetooth-enabled pen caps (NovoPen 6, NovoPen Echo Plus) and smart autoinjectors transmit injection data to companion mobile applications, enabling dose tracking, adherence monitoring, and integration with continuous glucose monitors. Implantable and sustained-release systems comprised 4.8% at approximately USD 280 million, an emerging segment that includes osmotic pump subcutaneous implants designed to deliver continuous GLP-1 over 6 to 12 months. Vivani Medical is developing a subdermal implant for extended GLP-1 release, targeting guaranteed adherence for patients who struggle with injection compliance.

By Application

Type 2 diabetes management was the largest application for GLP-1 drug delivery systems in 2025 at 54.6% share and approximately USD 3.19 Billion. Diabetes patients have the longest treatment histories with GLP-1 therapies and established pen-based self-injection routines. Obesity and weight management held 36.2% at USD 2.11 Billion, the fastest-growing application because obesity indications require identical device platforms but serve a much larger addressable population, with 42.4% of U.S. adults classified as obese. Cardiovascular risk reduction and MASH comprised the remaining 9.2% at USD 537 million, with device demand growing following 2025 regulatory approvals expanding semaglutide labeling.

Regional Analysis

North America held the largest share of the GLP-1 drug delivery systems market at 57.2% in 2025, valued at approximately USD 3.34 Billion. The United States generates over 92% of regional device demand. Eli Lilly's USD 27 Billion manufacturing expansion and USD 3.5 Billion Pennsylvania injectable facility investment directly increase device assembly capacity. Gerresheimer's USD 180 million expansion of its Peachtree City, Georgia site (May 2024) targets autoinjector and inhaler production. BD operates major syringe and device manufacturing in Franklin Lakes, New Jersey, and Sandy, Utah. The concentration of both pharmaceutical and device manufacturing creates a vertically integrated supply chain unique to North America.

Europe accounted for 23.8% of the GLP-1 drug delivery systems market at approximately USD 1.39 Billion. Switzerland-based Ypsomed is one of the world's largest contract injection device manufacturers, supplying over 25 pharma partners globally from its Burgdorf headquarters. Stevanato Group, headquartered in Piombino Dese, Italy, produces glass prefilled syringes and the Aidaptus autoinjector from facilities in Italy, Germany, and the U.S. SCHOTT Pharma launched its 5.5 mL large-volume prefillable syringe platform in October 2025. Nemera (France) announced plans to add a reusable autoinjector to its portfolio in October 2024. EU MDR (Medical Device Regulation) compliance requirements shape device design timelines and certification costs across the region.

Asia Pacific represented 13.4% at approximately USD 783 million in 2025, projected to grow at 16.9% CAGR through 2034. SHL Medical operates major autoinjector manufacturing facilities in Taiwan and China. Gerresheimer and Stevanato Group both maintain production sites in India for glass syringe and device component manufacturing. Eli Lilly launched the Mounjaro KwikPen in India in August 2025 at INR 14,000 (approximately USD 160) for a starting dose, signaling the entry of branded GLP-1 delivery into the Indian market. Amneal Pharmaceuticals announced USD 200 million investment in October 2024 for two Gujarat, India manufacturing facilities supporting GLP-1 therapeutic production. Corden Pharma committed USD 980 million in July 2024 to expand GLP-1 manufacturing capacity globally.

Latin America held 3.6% at approximately USD 210 million, and Middle East and Africa accounted for 2.0% at approximately USD 117 million. Cold chain logistics constraints in these regions limit penetration of temperature-sensitive prefilled pen injectors, creating opportunity for oral formulations and room-temperature-stable delivery technologies.

Country Analysis

The United States dominates the GLP-1 drug delivery systems market with an estimated value of USD 3.08 Billion in 2025 and a country-level CAGR of 14.6% through 2034. Eli Lilly's Zepbound KwikPen received FDA expanded labeling in February 2026 for a four-dose monthly configuration, reducing device unit requirements by 75%. Eli Lilly invested USD 3.5 Billion in a Pennsylvania injectable medicine facility in 2025. Gerresheimer expanded its Georgia autoinjector facility with USD 180 million. BD's U.S. operations supply glass prefilled syringe barrels and needle systems to multiple GLP-1 programs. The FDA's combination product regulatory framework (21 CFR Part 4) governs drug-device approval, creating 12 to 18 month device development lead times that affect time-to-market for new GLP-1 entrants.

Germany represents Europe's largest GLP-1 drug delivery systems market at approximately USD 420 million in 2025 with a CAGR of 12.4%. Gerresheimer AG, headquartered in Dusseldorf, is one of the world's leading pharmaceutical glass and device manufacturers. SCHOTT Pharma, based in Mainz, produces the syriQ BioPure platform of prefilled glass syringes. Boehringer Ingelheim's survodutide program, advancing through Phase 3 trials, will require dedicated delivery device partnerships. Germany's ISO 11608 compliance framework for pen injectors and autoinjectors sets the engineering standard adopted globally.

Switzerland contributes approximately USD 280 million to the GLP-1 drug delivery systems market in 2025. Ypsomed AG, headquartered in Burgdorf, manufactures the YpsoMate disposable autoinjector and UnoPen/ServoPen reusable pen platforms used across GLP-1, insulin, and biologic drug programs. Ypsomed supplies pen injector and autoinjector platforms to over 25 global pharmaceutical partners. The company's collaboration with BD on high-viscosity drug delivery (October 2024) positions it at the forefront of next-generation biologic injection technology.

Italy is a growing contributor at approximately USD 190 million in 2025, driven by Stevanato Group's global headquarters in Piombino Dese. Stevanato produces glass vials, prefilled syringes, cartridges, and the Aidaptus and Alina device platforms. The company's integrated offering from primary containment through final device assembly gives it a unique competitive position in GLP-1 supply chain consolidation. Stevanato has stated that autoinjectors and pen injectors will remain at the forefront of GLP-1 delivery for the foreseeable future.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Device Type

- Goods-to-Person Picking Robots

- Autonomous Forklifts

- Autonomous Inventory Robots

- Autonomous Tugger Robots

- Unmanned Ground Vehicles (UGVs)

- Delivery and Transport Robots

- Inspection and Surveillance Robots

- Cleaning and Disinfection Robots

- Collaborative Mobile Robots (Co-bots)

- Automated Guided Carts (AGCs)

- Autonomous Shelf-Scanning Robots

- Security and Patrol Robots

- Others

By Application

- Warehousing and Logistics

- Manufacturing and Industrial Automation

- Retail and E-commerce Fulfillment

- Healthcare and Hospitals

- Hospitality

- Agriculture

- Defense and Security

- Transportation and Airports

- Energy and Utilities

- Mining

- Education and Research

- Food and Beverage

- Pharmaceuticals

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.84 B |

| Forecast Revenue (2034) | USD 18.62 B |

| CAGR (2025-2034) | 13.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Device Type, (Goods-to-Person Picking Robots, Autonomous Forklifts, Autonomous Inventory Robots, Autonomous Tugger Robots, Unmanned Ground Vehicles (UGVs), Delivery and Transport Robots, Inspection and Surveillance Robots, Cleaning and Disinfection Robots, Collaborative Mobile Robots (Co-bots), Automated Guided Carts (AGCs), Autonomous Shelf-Scanning Robots, Security and Patrol Robots, Others), By Application, (Warehousing and Logistics, Manufacturing and Industrial Automation, Retail and E-commerce Fulfillment, Healthcare and Hospitals, Hospitality, Agriculture, Defense and Security, Transportation and Airports, Energy and Utilities, Mining, Education and Research, Food and Beverage, Pharmaceuticals, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVO NORDISK A/S, ELI LILLY AND COMPANY, YPSOMED AG, SHL MEDICAL AG, STEVANATO GROUP S.P.A., GERRESHEIMER AG, BECTON, DICKINSON AND COMPANY (BD), SCHOTT PHARMA AG & CO. KGAA, OWEN MUMFORD LTD., NEMERA, WEST PHARMACEUTICAL SERVICES, INC., ANTARES PHARMA (HALOZYME), RECIPHARM AB, DATWYLER HOLDING AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Type 2 Diabetes Management, Obesity and Weight Management, Cardiovascular Risk Reduction and Metabolic Disorders), By End User, Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Technological Advancements, Pipeline Innovations and Forecast 2026-2034")

, By Application (Type 2 Diabetes Management, Obesity and Weight Management, Cardiovascular Risk Reduction and Metabolic Disorders), By End User, Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Technological Advancements, Pipeline Innovations and Forecast 2026-2034")

, By Application (Type 2 Diabetes Management, Obesity and Weight Management, Cardiovascular Risk Reduction and Metabolic Disorders), By End User, Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends, Technological Advancements, Pipeline Innovations and Forecast 2026-2034")

Frequently Asked Questions

How big is the GLP-1 Drug Delivery Systems Market?

The Global GLP-1 Drug Delivery Systems Market was valued at USD 5.13 Billion in 2024 and USD 5.84 Billion in 2025, and is projected to reach USD 18.62 Billion by 2034, growing at a CAGR of 13.8% from 2026 to 2034. Market growth is driven by the increasing adoption of GLP-1 therapies for diabetes and obesity, alongside rising demand for patient-centric and convenient drug delivery solutions.

Who are the major players in the GLP-1 Drug Delivery Systems Market?

NOVO NORDISK A/S, ELI LILLY AND COMPANY, YPSOMED AG, SHL MEDICAL AG, STEVANATO GROUP S.P.A., GERRESHEIMER AG, BECTON, DICKINSON AND COMPANY (BD), SCHOTT PHARMA AG & CO. KGAA, OWEN MUMFORD LTD., NEMERA, WEST PHARMACEUTICAL SERVICES, INC., ANTARES PHARMA (HALOZYME), RECIPHARM AB, DATWYLER HOLDING AG, Others

Which segments covered the GLP-1 Drug Delivery Systems Market?

By Device Type, (Goods-to-Person Picking Robots, Autonomous Forklifts, Autonomous Inventory Robots, Autonomous Tugger Robots, Unmanned Ground Vehicles (UGVs), Delivery and Transport Robots, Inspection and Surveillance Robots, Cleaning and Disinfection Robots, Collaborative Mobile Robots (Co-bots), Automated Guided Carts (AGCs), Autonomous Shelf-Scanning Robots, Security and Patrol Robots, Others), By Application, (Warehousing and Logistics, Manufacturing and Industrial Automation, Retail and E-commerce Fulfillment, Healthcare and Hospitals, Hospitality, Agriculture, Defense and Security, Transportation and Airports, Energy and Utilities, Mining, Education and Research, Food and Beverage, Pharmaceuticals, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

GLP-1 Drug Delivery Systems Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date