- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

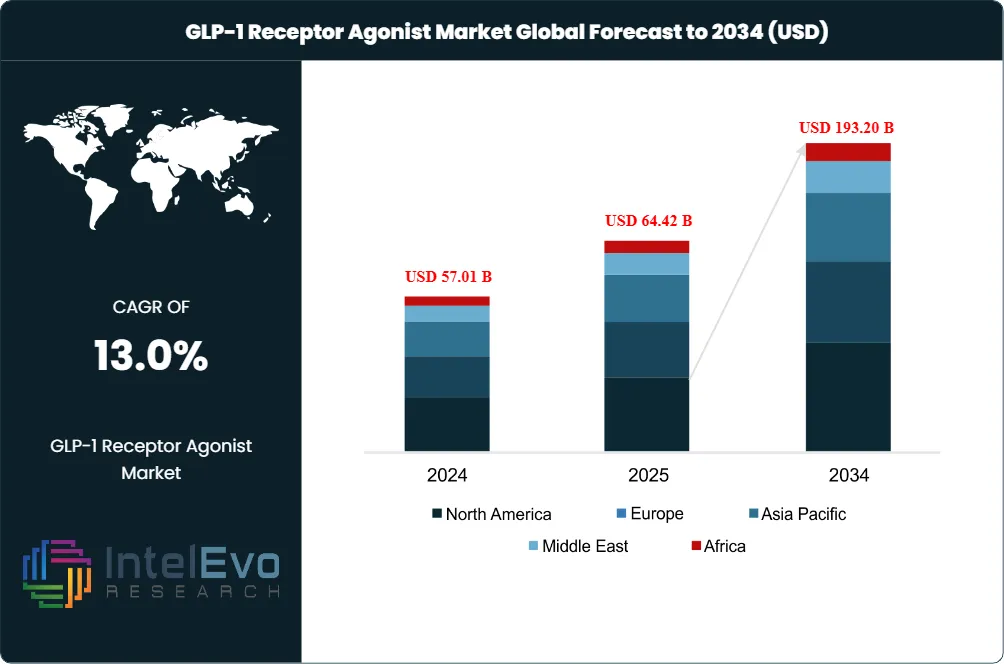

Global GLP-1 Receptor Agonist Market Size, Share & Forecast | CAGR 13.0%

Global GLP-1 Receptor Agonist Market Report: Market Size, Share, Growth Analysis By Product (Semaglutide, Tirzepatide, Dulaglutide, Liraglutide), By Application (Diabetes Management, Obesity Treatment, Cardiovascular Risk Reduction, NASH, CKD and Metabolic Disorders), By Route of Administration (Injectable and Oral Formulations), Regional Outlook, Regulatory Landscape, Clinical Pipeline Assessment, Key Company Profiles, Market Drivers, Challenges, Investment Opportunities and Strategic Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 64.42 Billion | USD 193.20 Billion | 13.0% | North America, 55.5% |

The GLP-1 Receptor Agonist Market was valued at USD 57.01 Billion in 2024 and USD 64.42 Billion in 2025. The market is projected to reach USD 193.20 Billion by 2034, expanding at a CAGR of 13.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 128.78 Billion over the analysis period. GLP-1 receptor agonists are a class of incretin-based medications that mimic the endogenous glucagon-like peptide-1 hormone to enhance insulin secretion, suppress glucagon release, delay gastric emptying, and promote satiety, delivering integrated glycemic control and weight reduction in patients with type 2 diabetes mellitus and obesity.

Get More Information about this report -

Request Free Sample ReportTwo pharmaceutical franchises dominate this market: Novo Nordisk A/S's semaglutide products (Ozempic, Wegovy, Rybelsus) generated USD 36.19 Billion in combined 2024 revenue, while Eli Lilly and Company's tirzepatide products (Mounjaro, Zepbound) reached USD 36.51 Billion in the same year. Tirzepatide achieved USD 5 Billion in Q1 2025 revenue alone, representing over 100% year-over-year growth and accounting for 39% of Eli Lilly's total quarterly revenue. Together, these two drug franchises produced over USD 72.7 Billion in 2024 sales, surpassing Merck's Keytruda (USD 31.68 Billion) as the highest-revenue therapeutic class in global pharmaceuticals. Analysts project that Eli Lilly's incretin portfolio, including the oral candidate orforglipron, could reach USD 101 Billion in peak annual sales.

Indication expansion is driving the market beyond type 2 diabetes into obesity, cardiovascular risk reduction, metabolic dysfunction-associated steatohepatitis (MASH), and emerging applications in neurodegenerative conditions and obstructive sleep apnea. In 2025, semaglutide (Wegovy) received approval for MASH with liver fibrosis in adults, while Rybelsus gained EU approval for cardiovascular risk reduction. Eli Lilly's orforglipron, the first oral small-molecule GLP-1 receptor agonist taken without food or water restrictions, completed three successful Phase 3 trials in 2025 across type 2 diabetes and obesity, triggering global regulatory submissions. In the ATTAIN-1 trial, orforglipron delivered average weight loss of 27.3 lbs (12.4%) at 72 weeks. These developments confirm that the GLP-1 class is transitioning from glucose-lowering agents into comprehensive metabolic disease management platforms.

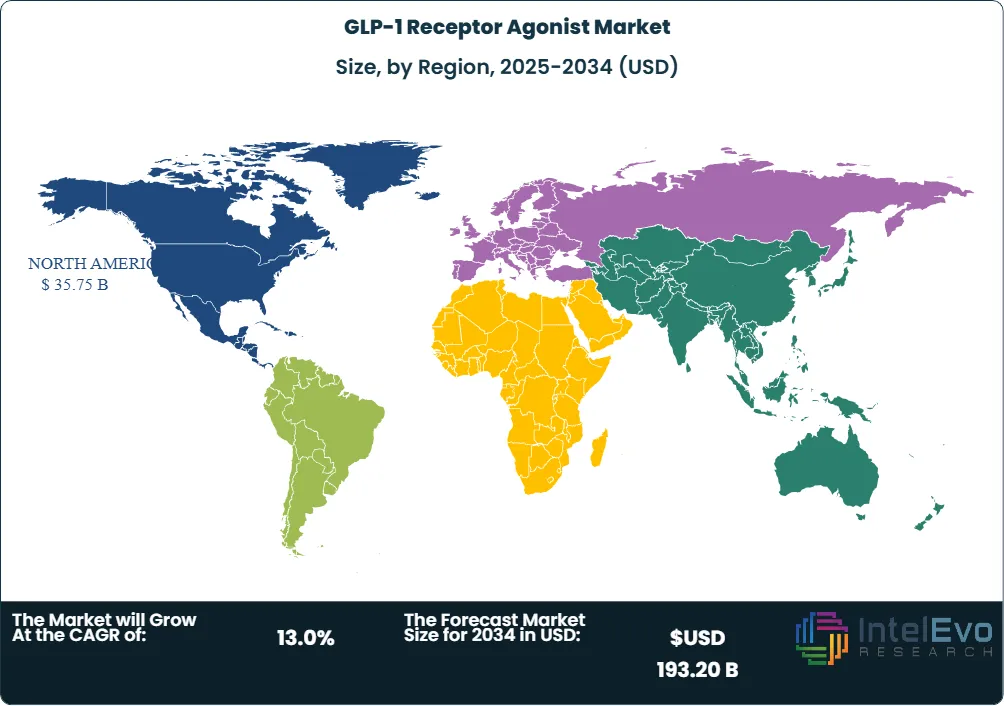

North America held 55.5% of the GLP-1 receptor agonist market in 2025 at approximately USD 35.75 Billion, anchored by the United States where approximately 12% of adults have used GLP-1 medications for weight management or diabetes treatment. Eli Lilly announced a USD 27 Billion U.S. manufacturing expansion across multiple sites in 2025 to address surging patient demand. Europe represented approximately 22.3% at USD 14.37 Billion, driven by Novo Nordisk's regulatory expansions and growing obesity treatment coverage. Asia Pacific accounted for 15.8% at USD 10.18 Billion, with China emerging as the fastest-growth national market following Innovent Biologics' regulatory approval of mazdutide, the first domestically developed GLP-1 drug in China.

Market Definition & Scope

The GLP-1 receptor agonist market is defined as the global commercial segment for medications that activate the glucagon-like peptide-1 receptor to treat type 2 diabetes mellitus, obesity, and related cardiometabolic conditions. The market encompasses single GLP-1 receptor agonists (semaglutide, liraglutide, dulaglutide, exenatide, lixisenatide), dual GIP/GLP-1 receptor agonists (tirzepatide), triple agonists (retatrutide, under clinical development), oral small-molecule GLP-1 agonists (orforglipron, under regulatory review), and combination therapies (CagriSema: cagrilintide plus semaglutide). Both injectable/parenteral and oral formulations are included across all dosing frequencies (daily, weekly, and investigational monthly).

This analysis includes branded originator products and authorized biosimilars sold through hospital pharmacies, retail pharmacies, specialty pharmacies, and online channels. The report explicitly excludes DPP-4 inhibitors (sitagliptin, saxagliptin), SGLT-2 inhibitors (dapagliflozin, empagliflozin), insulin therapies, and bariatric surgery procedures. It also excludes compounded semaglutide preparations produced by compounding pharmacies outside manufacturer authorization. The GLP-1 receptor agonist market represents the fastest-growing therapeutic class within the broader diabetes and obesity drug market, which exceeded USD 130 Billion globally in 2025.

, By Application (Diabetes Management, Obesity Treatment, Cardiovascular Risk Reduction, NASH, CKD and Metabolic Disorders), By Route of Administration (Injectable and Oral Formulations), Regional Outlook, Regulatory Landscape, Clinical Pipeline Assessment, Key Company Profiles, Market Drivers, Challenges, Investment Opportunities and Strategic Forecast 2026-2034")

Key Takeaways

- Market Growth: The GLP-1 receptor agonist market grew from USD 64.42 Billion in 2025 to a projected USD 193.20 Billion by 2034, at a 13.0% CAGR, representing USD 128.78 Billion in absolute dollar opportunity.

- Segment Dominance (By Product): Semaglutide (Ozempic, Wegovy, Rybelsus) held the largest product share at 52.8% in 2025 at approximately USD 34.0 Billion, driven by first-mover positioning in both type 2 diabetes and obesity indications across injectable and oral formulations.

- Segment Dominance (By Application): Type 2 diabetes mellitus accounted for 58.4% of application revenue in 2025 at approximately USD 37.6 Billion, because the diabetes indication carries broader insurance coverage and longer treatment histories than the newer obesity indication.

- Driver: The convergence of global obesity prevalence (42.4% of U.S. adults per Lancet data) and clinical evidence demonstrating 12 to 24% body weight reduction is expanding the addressable patient population from an estimated 37 million type 2 diabetes patients to over 100 million obese adults in the United States alone.

- Restraint: High list prices of USD 900 to USD 1,300 per month for branded GLP-1 injectables limit access among uninsured and underinsured populations, and anticipated semaglutide patent expiries beginning in 2026 threaten originator revenue streams.

- Opportunity: Oral GLP-1 formulations represent a USD 50+ Billion revenue opportunity by 2034. Eli Lilly's orforglipron completed three Phase 3 trials in 2025 and triggered global regulatory submissions, offering a once-daily pill without food or water restrictions that could reshape the competitive field.

- Trend: Dual and triple receptor agonists are outperforming single-target GLP-1 drugs in clinical trials. Tirzepatide (dual GIP/GLP-1) generated USD 36.51 Billion in 2024, and Eli Lilly's retatrutide (triple GLP-1/GIP/glucagon agonist) demonstrated 24.2% body weight reduction in Phase 2.

- Regional: North America led the GLP-1 receptor agonist market with 55.5% share valued at USD 35.75 Billion in 2025, supported by the concentration of Novo Nordisk and Eli Lilly manufacturing and commercial operations in the United States and Denmark.

Key Insights Summary

- Eli Lilly's tirzepatide franchise (Mounjaro plus Zepbound) generated USD 36.51 Billion in full-year 2024 revenue and USD 5 Billion in Q1 2025 alone, representing over 100% year-over-year growth (Eli Lilly SEC filing, Q1 2025).

- Novo Nordisk's semaglutide franchise (Ozempic, Wegovy, Rybelsus) generated USD 36.19 Billion in full-year 2024 revenue. Ozempic produced DKK 64.5 Billion in H1 2025 and Wegovy contributed DKK 36.8 Billion in the same period (Novo Nordisk H1 2025 earnings).

- Eli Lilly's orforglipron achieved average weight loss of 27.3 lbs (12.4%) at 72 weeks in the Phase 3 ATTAIN-1 trial and demonstrated superior A1C reduction of 1.3 to 1.6% from baseline in the ACHIEVE-1 trial, triggering global regulatory submissions in 2025 (Eli Lilly, August 2025).

- Pfizer completed the acquisition of Metsera for approximately USD 4.9 Billion in November 2025, gaining MET-097i, a weekly and monthly injectable GLP-1 receptor agonist entering Phase 3 development (Pfizer, November 2025).

- Approximately 12% of U.S. adults have used GLP-1 drugs for weight management or diabetes treatment, and the U.S. obesity rate of 42.4% among adults creates a total addressable population exceeding 100 million individuals.

- Semaglutide supply shortages that constrained market growth throughout 2023 and 2024 were resolved by February 2025, enabling Novo Nordisk to restore full commercial availability across all dosage strengths.

- Eli Lilly announced a USD 27 Billion U.S. manufacturing expansion in 2025 across multiple sites to scale GLP-1 production capacity, the largest single-company pharma manufacturing investment in U.S. history.

Competitive Landscape Overview

The GLP-1 receptor agonist market is highly consolidated, with two companies controlling over 85% of global revenue. Novo Nordisk A/S and Eli Lilly and Company together generated over USD 72.7 Billion in GLP-1-related sales in 2024. Novo Nordisk held the first-mover advantage through semaglutide, but Eli Lilly's tirzepatide has eroded that lead by demonstrating superior weight loss efficacy in head-to-head trials, with tirzepatide now accounting for two-thirds of all new obesity drug prescriptions in the United States. Competition is intensifying along four dimensions: oral formulation convenience, where Eli Lilly's orforglipron leads Novo Nordisk's oral semaglutide; multi-receptor targeting, where triple agonists like retatrutide push beyond dual-agonist tirzepatide; dosing frequency reduction, with monthly injectables from Metsera/Pfizer; and pricing, where anticipated semaglutide patent expiries beginning in 2026 will open the biosimilar channel. AstraZeneca, Pfizer (via Metsera), Amgen, Viking Therapeutics, Boehringer Ingelheim (survodutide), and Structure Therapeutics are advancing late-stage GLP-1 pipelines that will fragment Novo-Lilly dominance from 2027 onward.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product/Pipeline | Geo Strength | Founded | Recent Strategic Move |

| Novo Nordisk A/S | Denmark | Leader | Ozempic, Wegovy, Rybelsus, CagriSema | Global | 1923 | Wegovy MASH approval; oral semaglutide FDA filing (2025) |

| Eli Lilly | US | Leader | Mounjaro, Zepbound, orforglipron, retatrutide | Global | 1876 | Orforglipron Phase 3 success; USD 27B mfg expansion (2025) |

| Pfizer Inc. | US | Challenger | MET-097i (via Metsera), oral GLP-1 | Global | 1849 | USD 4.9B Metsera acquisition (Nov 2025) |

| AstraZeneca | UK | Challenger | ECC5004 (oral GLP-1RA) | Global | 1999 | EMA obesity approval expected (Apr 2025) |

| Boehringer Ingelheim | Germany | Challenger | Survodutide (dual GCG/GLP-1) | Global | 1885 | Phase 3 obesity and MASH trials (2025) |

| Amgen Inc. | US | Challenger | MariTide (AMG 133) | Global | 1980 | Phase 2 obesity data (2024); Phase 3 initiated |

| Viking Therapeutics | US | Niche | VK2735 (dual GIP/GLP-1) | US | 2012 | Phase 2 oral VK2735 trial initiated (Jan 2025) |

| Innovent Biologics | China | Niche | Mazdutide | China, Asia | 2011 | First Chinese-approved GLP-1; JD Health partnership (Jul 2025) |

By Product

Semaglutide (Ozempic, Wegovy, Rybelsus) dominated the GLP-1 receptor agonist market with 52.8% product share in 2025 at approximately USD 34.0 Billion. Ozempic, approved for type 2 diabetes, is the highest-revenue individual GLP-1 product globally. Wegovy, the obesity-indicated formulation, received expanded approval in 2025 for MASH with liver fibrosis, broadening its addressable market. Rybelsus, the oral semaglutide tablet, gained EU approval in September 2025 for cardiovascular risk reduction. Novo Nordisk's dominance in this segment reflects its decade-long clinical investment in semaglutide across 70+ clinical trials. Supply shortages that constrained availability through 2024 were resolved by February 2025, restoring full commercial distribution.

Tirzepatide (Mounjaro, Zepbound) held 33.6% share at approximately USD 21.7 Billion in 2025. Tirzepatide is a dual GIP/GLP-1 receptor agonist that achieved superior weight loss versus semaglutide in head-to-head SURMOUNT-5 trial results. Zepbound's launch in November 2023 accelerated Eli Lilly's obesity market capture; tirzepatide now accounts for two-thirds of new obesity drug prescriptions in the U.S. Eli Lilly reported Q1 2025 tirzepatide revenue of USD 5 Billion, representing over 100% year-over-year growth. Dulaglutide (Trulicity, Eli Lilly) held 6.2% at approximately USD 4.0 Billion but faces declining share because of cannibalization by tirzepatide. Liraglutide (Victoza/Saxenda, Novo Nordisk), exenatide (Byetta/Bydureon, AstraZeneca), and lixisenatide held the remaining 7.4%.

By Application

Type 2 diabetes mellitus was the largest application segment of the GLP-1 receptor agonist market in 2025 at 58.4% share and approximately USD 37.6 Billion. GLP-1 agonists are now embedded in American Diabetes Association and European Association for the Study of Diabetes treatment algorithms as preferred second-line therapy after metformin, with growing evidence supporting first-line use in patients with cardiovascular risk factors. Approximately 537 million adults worldwide live with diabetes, according to the International Diabetes Federation, and type 2 diabetes accounts for over 90% of cases. Obesity management held 34.8% share at approximately USD 22.4 Billion, the fastest-growing application segment at a projected 18.5% CAGR through 2034. Cardiovascular risk reduction accounted for 4.3% at USD 2.8 Billion following the SELECT and SOUL trial results demonstrating semaglutide's 20% reduction in major adverse cardiovascular events. MASH/NASH and other emerging indications comprised the remaining 2.5% at USD 1.6 Billion.

By Route of Administration

Injectable/parenteral formulations dominated the GLP-1 receptor agonist market with 87.3% share in 2025 at approximately USD 56.2 Billion. Weekly subcutaneous injections (semaglutide 2.4mg, tirzepatide 15mg) represent the standard of care for both diabetes and obesity. Prefilled pen delivery devices from Novo Nordisk (FlexTouch) and Eli Lilly (KwikPen) have improved patient adherence through simplified self-administration. Oral formulations held 12.7% at approximately USD 8.2 Billion, led by Rybelsus (oral semaglutide 14mg daily). The oral segment is projected to grow at 22.8% CAGR through 2034, accelerating if Eli Lilly's orforglipron (once-daily pill without food/water restrictions) receives regulatory approval, which analysts expect in 2026 or 2027. Monthly injectable candidates, including Pfizer/Metsera's MET-097i, could further reshape the route-of-administration landscape from 2028 onward.

Regional Analysis

North America held the largest share of the GLP-1 receptor agonist market at 55.5% in 2025, valued at approximately USD 35.75 Billion. The United States generated over 90% of regional revenue because of its large obese population (42.4% of adults), favorable insurance coverage for diabetes medications, and the concentration of Eli Lilly's U.S. manufacturing operations. Eli Lilly announced USD 27 Billion in U.S. manufacturing expansion in 2025 to scale tirzepatide and orforglipron production. Novo Nordisk resolved semaglutide supply shortages by February 2025. Medicare Part D coverage expansion for obesity drugs, enacted under the Inflation Reduction Act provisions, is projected to add 3 to 5 million eligible patients. Canada represents approximately USD 1.8 Billion in market value.

Europe accounted for 22.3% of the GLP-1 receptor agonist market at approximately USD 14.37 Billion in 2025. Novo Nordisk's European headquarters in Bagsvaerd, Denmark, anchors regional supply and regulatory strategy. Rybelsus received EU approval in September 2025 for cardiovascular risk reduction, expanding its labeled indications beyond glycemic control. The UK's National Institute for Health and Care Excellence (NICE) and Germany's G-BA have broadened reimbursement coverage for GLP-1 therapies in obesity, although access remains more restrictive than in the U.S. Boehringer Ingelheim, headquartered in Ingelheim am Rhein, is advancing survodutide through European Phase 3 trials.

Asia Pacific represented 15.8% of the GLP-1 receptor agonist market at approximately USD 10.18 Billion in 2025 and is projected to register the fastest regional CAGR of 17.2% through 2034. China is the primary growth engine, with Innovent Biologics achieving the first domestic GLP-1 drug approval (mazdutide) and partnering with JD Health in July 2025 for online distribution. India's diabetes population exceeds 100 million, and Medtronic invested USD 50 million in the India Diabetes Center in July 2025. Japan and South Korea represent mature pharmaceutical markets with growing obesity treatment coverage. Latin America held 3.9% at USD 2.51 Billion, and Middle East and Africa accounted for 2.5% at USD 1.61 Billion.

Country Analysis

The United States dominates the GLP-1 receptor agonist market with an estimated value of USD 32.4 Billion in 2025 and a country-level CAGR of 14.1% through 2034. Approximately 12% of U.S. adults have used GLP-1 medications for weight management or diabetes. Eli Lilly's USD 27 Billion manufacturing expansion, the largest pharma capital investment in U.S. history, spans multiple sites designed to increase tirzepatide and orforglipron production capacity. Eli Lilly's revenue grew 38% in H1 2025 and 41% year-over-year, driven almost entirely by its incretin franchise. The FDA accepted Eli Lilly's orforglipron regulatory submission following successful Phase 3 results in ACHIEVE-1 (type 2 diabetes) and ATTAIN-1 (obesity). Medicare Part D expansion for obesity indications will further enlarge the addressable patient pool.

Denmark serves as the global headquarters and primary R&D center for Novo Nordisk A/S, the originator of semaglutide. Novo Nordisk reported H1 2025 revenue of DKK 76.8 Billion, with Ozempic generating DKK 64.5 Billion and Wegovy contributing DKK 36.8 Billion in H1 2025. However, lower-than-expected Wegovy sales prompted Novo Nordisk to cut its 2025 guidance. Novo Nordisk's CagriSema (cagrilintide 2.4mg plus semaglutide 2.4mg) Phase 3 topline results in overweight/obese patients with type 2 diabetes were announced in March 2025. The country's pharmaceutical ecosystem contributes approximately USD 3.2 Billion in direct GLP-1 market value.

China is the fastest-growing national market, valued at approximately USD 4.8 Billion in 2025 with a projected CAGR of 19.3%. Innovent Biologics became the first Chinese company with regulatory approval for a GLP-1 drug (mazdutide) and partnered with JD Health in July 2025 for online sales channel development. Hansoh Pharmaceutical Group and PegBio Co. are advancing domestic GLP-1 candidates through Chinese clinical trials. China's diabetes population exceeds 140 million, and obesity prevalence is rising rapidly in urban centers, creating an addressable market that rivals the United States in patient volume.

Germany represents Europe's largest GLP-1 receptor agonist market at approximately USD 4.1 Billion in 2025 with a CAGR of 12.8%. Boehringer Ingelheim International GmbH is advancing survodutide, a dual glucagon/GLP-1 receptor agonist, through Phase 3 clinical trials for obesity and MASH. Germany's G-BA reimbursement decisions in 2025 expanded coverage for injectable GLP-1 therapies in patients with BMI above 30 and cardiometabolic comorbidities.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product

- Semaglutide

- Liraglutide

- Dulaglutide

- Exenatide

- Lixisenatide

- Tirzepatide

- Albiglutide

- Efpeglenatide

- Others

By Application

- Type 2 Diabetes Mellitus

- Obesity and Weight Management

- Cardiovascular Risk Reduction

- Non-Alcoholic Steatohepatitis (NASH)

- Chronic Kidney Disease (CKD)

- Polycystic Ovary Syndrome (PCOS)

- Prediabetes

- Metabolic Syndrome

- Others

By Route of Administration

- Subcutaneous Injection

- Once-Daily Injection

- Once-Weekly Injection

- Oral Administration

- Intravenous Administration

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 64.42 B |

| Forecast Revenue (2034) | USD 193.20 B |

| CAGR (2025-2034) | 13.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Semaglutide, Liraglutide, Dulaglutide, Exenatide, Lixisenatide, Tirzepatide, Albiglutide, Efpeglenatide, Others), By Application, (Type 2 Diabetes Mellitus, Obesity and Weight Management, Cardiovascular Risk Reduction, Non-Alcoholic Steatohepatitis (NASH), Chronic Kidney Disease (CKD), Polycystic Ovary Syndrome (PCOS), Prediabetes, Metabolic Syndrome, Others), By Route of Administration, (Subcutaneous Injection, Oral Administration, Intravenous Administration, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NOVO NORDISK A/S, ELI LILLY AND COMPANY, PFIZER INC., ASTRAZENECA PLC, BOEHRINGER INGELHEIM INTERNATIONAL GMBH, AMGEN INC., SANOFI S.A., VIKING THERAPEUTICS, INC., INNOVENT BIOLOGICS, INC., HANSOH PHARMACEUTICAL GROUP CO., LTD., STRUCTURE THERAPEUTICS INC., ALTIMMUNE, INC., ZEALAND PHARMA A/S, AMNEAL PHARMACEUTICALS, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Diabetes Management, Obesity Treatment, Cardiovascular Risk Reduction, NASH, CKD and Metabolic Disorders), By Route of Administration (Injectable and Oral Formulations), Regional Outlook, Regulatory Landscape, Clinical Pipeline Assessment, Key Company Profiles, Market Drivers, Challenges, Investment Opportunities and Strategic Forecast 2026-2034")

, By Application (Diabetes Management, Obesity Treatment, Cardiovascular Risk Reduction, NASH, CKD and Metabolic Disorders), By Route of Administration (Injectable and Oral Formulations), Regional Outlook, Regulatory Landscape, Clinical Pipeline Assessment, Key Company Profiles, Market Drivers, Challenges, Investment Opportunities and Strategic Forecast 2026-2034")

, By Application (Diabetes Management, Obesity Treatment, Cardiovascular Risk Reduction, NASH, CKD and Metabolic Disorders), By Route of Administration (Injectable and Oral Formulations), Regional Outlook, Regulatory Landscape, Clinical Pipeline Assessment, Key Company Profiles, Market Drivers, Challenges, Investment Opportunities and Strategic Forecast 2026-2034")

Frequently Asked Questions

How big is the GLP-1 Receptor Agonist Market?

The Global GLP-1 Receptor Agonist Market was valued at USD 57.01 Billion in 2024 and USD 64.42 Billion in 2025, and is projected to reach USD 193.20 Billion by 2034, growing at a CAGR of 13.0% from 2026 to 2034. Market growth is driven by the rising prevalence of type 2 diabetes and obesity, expanding therapeutic indications, and increasing adoption of advanced incretin-based therapies.

Who are the major players in the GLP-1 Receptor Agonist Market?

NOVO NORDISK A/S, ELI LILLY AND COMPANY, PFIZER INC., ASTRAZENECA PLC, BOEHRINGER INGELHEIM INTERNATIONAL GMBH, AMGEN INC., SANOFI S.A., VIKING THERAPEUTICS, INC., INNOVENT BIOLOGICS, INC., HANSOH PHARMACEUTICAL GROUP CO., LTD., STRUCTURE THERAPEUTICS INC., ALTIMMUNE, INC., ZEALAND PHARMA A/S, AMNEAL PHARMACEUTICALS, INC., Others

Which segments covered the GLP-1 Receptor Agonist Market?

By Product, (Semaglutide, Liraglutide, Dulaglutide, Exenatide, Lixisenatide, Tirzepatide, Albiglutide, Efpeglenatide, Others), By Application, (Type 2 Diabetes Mellitus, Obesity and Weight Management, Cardiovascular Risk Reduction, Non-Alcoholic Steatohepatitis (NASH), Chronic Kidney Disease (CKD), Polycystic Ovary Syndrome (PCOS), Prediabetes, Metabolic Syndrome, Others), By Route of Administration, (Subcutaneous Injection, Oral Administration, Intravenous Administration, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

GLP-1 Receptor Agonist Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date