- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Golf Cart and NEV Market Size & Forecast 2024–2034 | 9.3% CAGR

Global Golf Cart and Neighborhood Electric Vehicle (NEV) Market Size, Share & Industry Analysis By Product Type (Golf Carts, Neighborhood Electric Vehicles), By Battery Type (Lead-Acid, Lithium-Ion), By Application (Golf Courses, Residential Communities, Commercial Use, Campuses & Parks), By End-User (Hospitality, Corporate Campuses, Municipal Fleets), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034

Report Overview

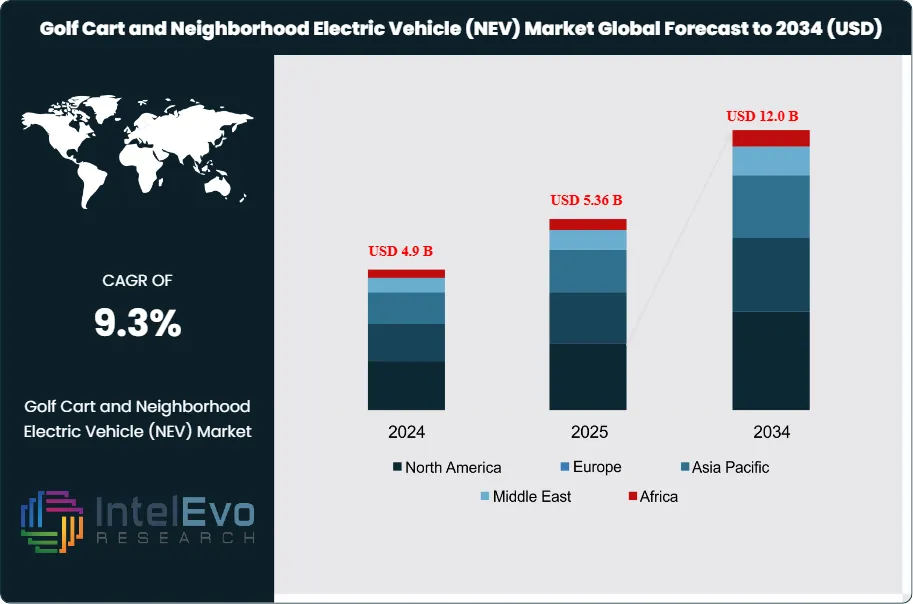

The Golf Cart and Neighborhood Electric Vehicle (NEV) Market was valued at USD 4.9 Billion in 2024 and is projected to reach approximately USD 12.0 Billion by 2034. The market is estimated to grow to around USD 5.36 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 9.3% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportThe market spans vehicle sales, fleet programs, parts, battery packs, charging hardware, and aftersales service. Golf carts continue to anchor volumes in golf, hospitality, and gated communities, while road-legal NEVs expand the addressable market through access to designated low-speed public roads and planned mobility zones.

Demand growth reflects a clear shift from single-use recreation to everyday utility. In mature retirement and master-planned communities, adoption has moved from convenience to default mobility, with more than 50,000 carts and low-speed vehicles operating in The Villages and residents using them for about 80% of local trips. Commercial buyers now drive a larger share of incremental demand through campus logistics, industrial transport, and last-mile delivery trials. Electric models already dominate the mix, with electric golf carts accounting for over 85% of sales in 2022, supported by 30–40% lower ownership costs versus gas alternatives and demand uplift of about 30% during periods of higher fuel prices.

On the supply side, scale players and specialist manufacturers compete through platform upgrades, premium features, and battery performance. Textron’s Specialized Vehicles business reported nearly USD 1.7 billion in revenue in 2022, while E-Z-GO production exceeded 143,000 units from 2021 to early 2023; Yamaha produced around 44,000 units and generated about USD 350 million in 2022. Product differentiation increasingly centers on road compliance, safety content, and comfort. Luxury and performance positioning also rises, illustrated by a road-legal cart developed with Garia that pairs a 10.24 kWh lithium-ion pack with up to 80 km range and region-specific top-speed limits.

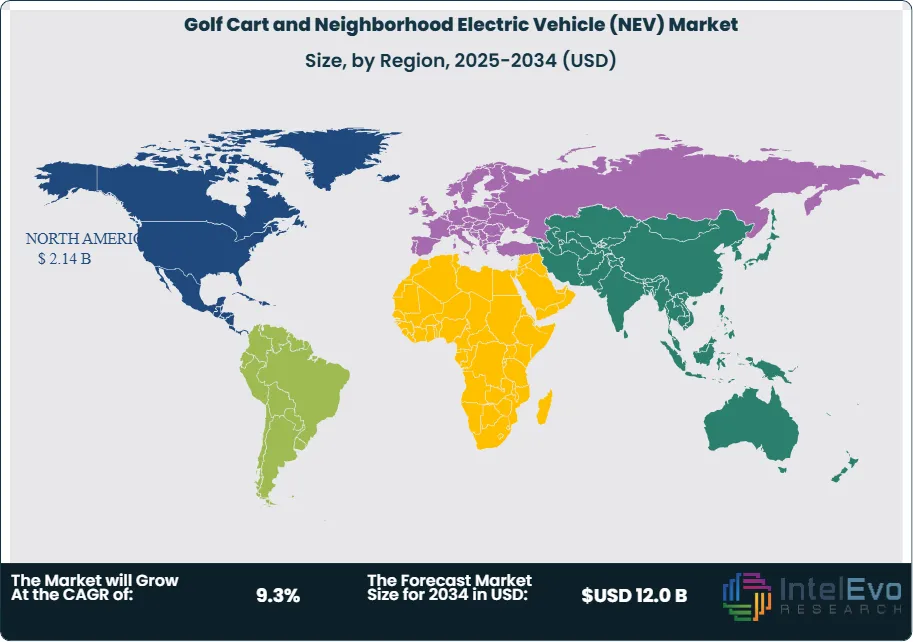

Regulation shapes market access and risk. NEV and low-speed vehicle rules set speed caps, lighting, braking, and occupant protection requirements, but fragmented city and state policies create compliance complexity and liability exposure. Battery input costs, warranty reserves, and charging availability remain key downside risks. Technology offsets these pressures. Telematics, geofencing, and app-based fleet control accelerate digitization, while AI-enabled diagnostics and predictive maintenance reduce downtime for commercial fleets. North America is expected to retain roughly 45% of revenue, with investment hotspots in community mobility corridors and resort clusters; Europe benefits from low-emission zones; Asia-Pacific shows faster growth in industrial parks and tourism-led development.

Market Size, Share & Industry Analysis By Product Type (Golf Carts, Neighborhood Electric Vehicles), By Battery Type (Lead-Acid, Lithium-Ion), By Application (Golf Courses, Residential Communities, Commercial Use, Campuses & Parks), By End-User (Hospitality, Corporate Campuses, Municipal Fleets), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 4.5 billion USD, 2023 to 10.8 billion USD, 2033 and sustains 9.1% CAGR, 2024-2034.

- Segment Dominance : Golf carts hold 56.0% share, 2024, supported by high utilization across golf and resort mobility.

- Segment Dominance: Golf course applications account for 40.0% share, 2024, driven by routine on-course transport demand.

- Driver: Demand rises as buyers prioritize low-emission, low-noise mobility, estimated: 85.0% electric share, 2024.

- Restraint: Regulatory limits and road-access constraints cap deployment, estimated: 25.0 mph speed ceiling, 2024.

- Opportunity: NEVs gain runway in last-mile delivery and short commutes as range improves, estimated: 80.0 km range, 2024.

- Trend: Manufacturers push premium, connected features to lift ASPs, estimated: 10.1 inch infotainment display, 2024.

- Regional Analysis: North America leads with 40.0% share, 2024, supported by strong recreational and residential adoption.

By Type

Golf carts remain the volume anchor in 2025, holding 56% market share in 2023 and sustaining leadership as courses, resorts, and private communities keep standardizing electric fleets. You see this segment win on simple economics. Operators target lower running costs and quieter operations, and electric models already represented over 85% of sales in 2022. Battery upgrades extend daily utilization and reduce charging downtime, which supports higher fleet turnover and steadier replacement demand.

Neighborhood Electric Vehicles accounted for 44% market share in 2023 and gain faster momentum into 2026 as more jurisdictions formalize low-speed corridors and signage. You see NEVs expand beyond community transport into campus shuttles and controlled last-mile delivery routes because they carry stronger safety content than traditional carts and can legally access select public roads. Market growth also tracks incentive programs for zero-emission mobility and improving lithium-ion pack performance, with premium road-legal models now advertising up to 80 km range on a single charge.

By Application

Golf courses led applications with 40% market share in 2023 and keep their lead through 2025 because cart fleets sit at the core of daily operations. You see course managers shift procurement toward electric platforms to cut fuel exposure and maintenance needs. Total cost of ownership remains a decisive metric, with electric platforms delivering 30% to 40% lower ownership costs versus gas alternatives in typical use profiles.

Residential areas captured 28% market share in 2023 and continue to expand as gated communities and retirement villages treat low-speed mobility as default transport for short trips. You see demand rise where residents rely on carts and NEVs for a high share of local journeys. Commercial use represented 22% market share in 2023, supported by hotels and resorts that prioritize fast guest movement and service logistics. The “others” segment held 10% in 2023 and grows through campuses, parks, and large properties that require frequent intra-site transport.

By End-Use

Residential building end-use gains share as developers design mobility-friendly communities with parking bays, charging points, and dedicated paths. You see this segment favor golf carts for local movement and NEVs where road-legal access applies. Higher electric adoption also supports lower noise and improves neighborhood acceptance in dense developments.

Commercial building end-use tracks hospitality, retail complexes, and institutional campuses that run daily shuttle loops and service operations. You see fleet buyers demand telematics, geofencing, and app-based access control to reduce misuse and improve utilization. Industrial building end-use expands in warehouses, ports, and large plants where low-speed vehicles handle site logistics. Safety compliance and uptime define purchasing, and predictive maintenance reduces stoppages as connected diagnostics becomes standard.

By Region

North America leads with about 40% market share in 2023 and remains the largest revenue pool in 2025 due to high golf participation, large retirement communities, and favorable low-speed vehicle rules in many states. You see the United States drive fleet replacements in resorts and master-planned communities, while corporate campuses sustain steady orders. Electrification stays high, supported by established dealer networks and service ecosystems.

Europe accelerates adoption where cities restrict combustion vehicles and promote small electric mobility in controlled zones, estimated: 25% market share, 2025. Asia Pacific shows faster unit growth as tourism assets expand and industrial parks scale internal transport, estimated: 23% market share, 2025. Latin America and the Middle East and Africa remain earlier-stage markets but gain traction in resorts and large commercial properties, estimated: 7% market share, 2025 and estimated: 5% market share, 2025. You should expect uneven policy enforcement and charging availability to shape near-term outcomes across these emerging regions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Golf Carts

- Neighborhood Electric Vehicles (NEVs)

By Application

- Golf Courses

- Residential Areas

- Commercial Use (hotels, resorts, etc.)

- Others (e.g., campuses, parks)

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.36 B |

| Forecast Revenue (2034) | USD 12.0 B |

| CAGR (2025-2034) | 9.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, Golf Carts, Neighborhood Electric Vehicles (NEVs), By Application, Golf Courses, Residential Areas, Commercial Use (hotels, resorts, etc.), Others (e.g., campuses, parks) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | STAR EV, Garia, Yamaha Golf-Car Company, American Custom Golf Cars, Polaris Industries, Bradshaw Electric Vehicles, E-Z-GO (Textron Inc.), Club Car (Ingersoll Rand), Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share & Industry Analysis By Product Type (Golf Carts, Neighborhood Electric Vehicles), By Battery Type (Lead-Acid, Lithium-Ion), By Application (Golf Courses, Residential Communities, Commercial Use, Campuses & Parks), By End-User (Hospitality, Corporate Campuses, Municipal Fleets), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Product Type (Golf Carts, Neighborhood Electric Vehicles), By Battery Type (Lead-Acid, Lithium-Ion), By Application (Golf Courses, Residential Communities, Commercial Use, Campuses & Parks), By End-User (Hospitality, Corporate Campuses, Municipal Fleets), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Market Size, Share & Industry Analysis By Product Type (Golf Carts, Neighborhood Electric Vehicles), By Battery Type (Lead-Acid, Lithium-Ion), By Application (Golf Courses, Residential Communities, Commercial Use, Campuses & Parks), By End-User (Hospitality, Corporate Campuses, Municipal Fleets), Regional Outlook, Competitive Landscape, Market Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Golf Cart and Neighborhood Electric Vehicle (NEV) Market?

The Global Golf Cart and Neighborhood Electric Vehicle (NEV) Market was valued at USD 4.9 Billion in 2024 and is projected to reach USD 12.0 Billion by 2034, growing at a CAGR of 9.3% from 2026–2034. Explore key trends, demand for low-speed electric vehicles, market drivers, and future growth opportunities.

Who are the major players in the Golf Cart and Neighborhood Electric Vehicle (NEV) Market?

STAR EV, Garia, Yamaha Golf-Car Company, American Custom Golf Cars, Polaris Industries, Bradshaw Electric Vehicles, E-Z-GO (Textron Inc.), Club Car (Ingersoll Rand), Other Key Players

Which segments covered the Golf Cart and Neighborhood Electric Vehicle (NEV) Market?

By Product Type, Golf Carts, Neighborhood Electric Vehicles (NEVs), By Application, Golf Courses, Residential Areas, Commercial Use (hotels, resorts, etc.), Others (e.g., campuses, parks)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Golf Cart and Neighborhood Electric Vehicle (NEV) Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date