- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Gout Therapeutics Market Size, Share & Forecast 2025–2034| 8.4% CAGR

Global Gout Therapeutics Market Size, Share, Analysis By Drug Class (NSAIDs, Corticosteroids, Colchicine, Urate-Lowering Agents), By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospitals, Clinics, Home Care Settings) Industry Region & Key Players – Industry Segment Overview, Epidemiology Trends, Treatment Landscape, Market Dynamics, Competitive Strategies, Innovation Pipeline, Regulatory Developments & Forecast 2025–2034

Report Overview

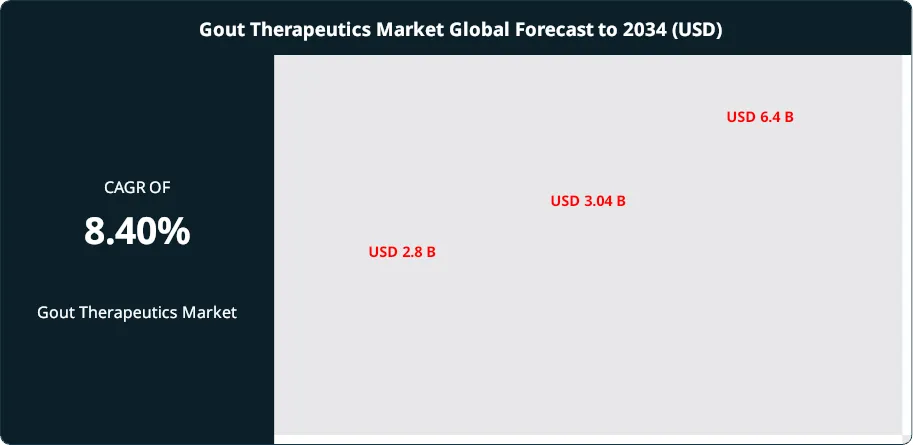

The Gout Therapeutics Market was valued at USD 2.8 Billion in 2024 and is estimated to reach approximately USD 3.04 Billion in 2025. Driven by increasing prevalence of gout, rising geriatric population, and growing adoption of advanced urate-lowering therapies, the market is projected to grow from about USD 3.30 Billion in 2026 to nearly USD 6.4 Billion by 2034, registering a compound annual growth rate (CAGR) of around 8.4% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportMarket expansion tracks the steady rise in gout prevalence and recurring flare burden, supported by aging populations, higher obesity rates, and sustained alcohol-related risk. Gout remains a painful inflammatory arthritis that commonly affects the feet, ankles, knees, wrists, and elbows. Persistent hyperuricemia drives long-term joint damage and comorbidity risk, which keeps demand for urate-lowering therapy and anti-inflammatory control elevated. Across developed markets, treated prevalence is assumed to grow at 4–6% per year through 2034, with flare-related visits representing roughly 30–35% of gout-related direct costs.

Therapy demand continues to shift toward higher-efficacy biologics and combination strategies for refractory disease. Biologics are estimated to account for about 28% of 2024 revenues and may approach 40% by 2034 as payers accept targeted options for severe patients and as real-world evidence improves positioning. Supply-side dynamics favor manufacturers that can scale sterile injectables, ensure cold-chain reliability, and secure contract development and manufacturing capacity amid periodic API constraints. Pricing remains under pressure in oral agents as generics expand, while specialty products sustain premium net pricing through outcomes-backed contracting and tighter patient segmentation.

Regulatory bodies are tightening benefit–risk expectations around cardiovascular safety, renal considerations, and drug–drug interactions, which influences label language and post-market surveillance intensity. Technology is reshaping both development and care pathways. AI-enabled trial design and biomarker analytics can reduce recruitment time by 10–15% in late-stage programs, while automation in pharmacovigilance improves signal detection and reporting speed. Digital adherence tools and remote monitoring support urate target attainment, which reduces flare frequency and reinforces value arguments in reimbursement negotiations.

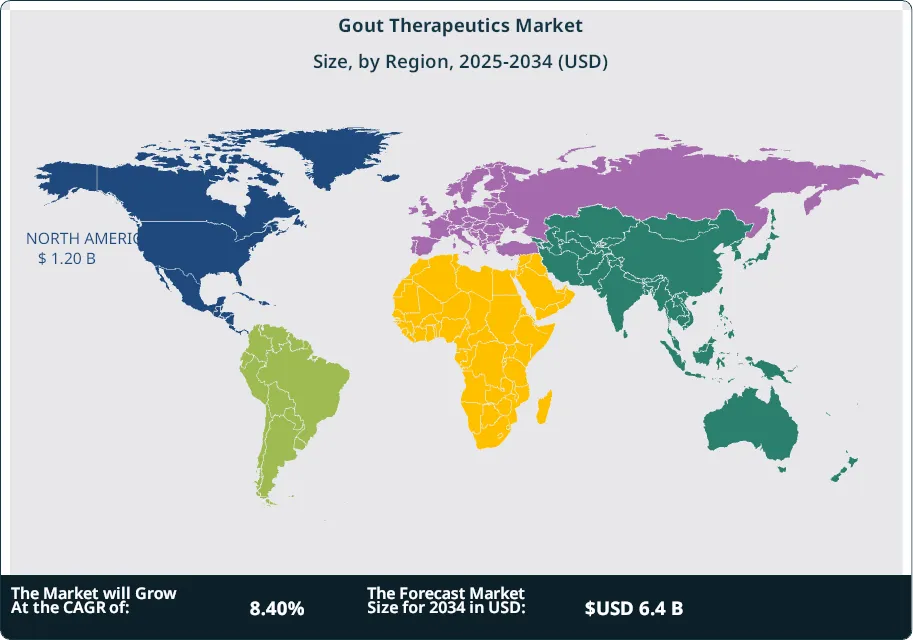

Regionally, North America is projected to hold about 38% of 2024 revenue, supported by specialty access and higher diagnosis rates. Europe follows near 27% with tighter pricing controls but stable volume growth. Asia-Pacific is expected to exceed 25% by 2034 as diagnosis improves and specialist capacity expands, with urban China and India emerging as investment hotspots for clinical development, manufacturing localization, and digital chronic-care programs. The pandemic period delayed diagnosis and initiation in many systems, but deferred demand has largely normalized, with residual risk centered on access volatility and provider capacity constraints.

, By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospitals, Clinics, Home Care Settings) Industry Region & Key Players – Industry Segment Overview, Epidemiology Trends, Treatment Landscape, Market Dynamics, Competitive Strategies, Innovation Pipeline, Regulatory Developments & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands at 8.6% CAGR, 2024-2034, scaling to 5.4 billion USD, 2032 from 2.4 billion USD, 2022. It reaches estimated: 2.8 billion USD, 2024 under the same growth trajectory.

- Segment Dominance : NSAIDs lead the drug class mix at 46.0% share, 2024. This segment delivers estimated: 1.3 billion USD, 2024 in revenue.

- Segment Dominance: Chronic gout drives utilization at 67.0% share, 2024. This indication contributes estimated: 1.9 billion USD, 2024 in revenue.

- Driver: Aging demographics increase incidence and accelerate demand at estimated: 4.5% prevalence growth, 2024. Rising awareness supports earlier diagnosis at estimated: 12.0% increase in diagnosed patients, 2024.

- Restraint: Hospital access and acute-care capacity constraints limit timely treatment at estimated: 8.0% care delays, 2024. Pricing pressure on established oral therapies compresses net realization at estimated: 3.0% annual erosion, 2024.

- Opportunity: Biologics adoption expands addressable severe and refractory populations to estimated: 0.8 billion USD, 2024. Combination regimens create incremental value at estimated: 18.0% of treated patients, 2024.

- Trend: Developers scale multi-pathway combination approaches at estimated: 22.0% pipeline share, 2024. Digital tools improve adherence and monitoring at estimated: 15.0% adoption in managed care settings, 2024.

- Regional Analysis: North America leads with 39.4% share, 2024, generating estimated: 1.1 billion USD, 2024. Asia Pacific posts the fastest growth at estimated: 10.2% CAGR, 2024-2034 led by Japan, China, and India.

By Type

The gout therapeutics market in 2025 continues to be led by nonsteroidal anti-inflammatory drugs, which account for approximately 46 percent of total revenue. NSAIDs remain the primary intervention for acute flare management due to rapid pain control, widespread availability, and extensive generic penetration. Their use remains particularly strong in early-stage diagnosis and emergency care settings, where immediate symptom relief is prioritized over long-term disease modification.

Urate-lowering agents represent the fastest-growing drug class as clinical practice increasingly shifts toward sustained serum urate control. Xanthine oxidase inhibitors and uricosuric therapies form the backbone of chronic management, supported by updated treatment guidelines and higher patient adherence rates. This segment is expected to expand at a high single-digit CAGR beyond 2025, driven by new product launches and broader use in moderate to severe disease profiles.

Corticosteroids and colchicine maintain defined but narrower roles. Corticosteroids are commonly prescribed for patients who cannot tolerate NSAIDs or colchicine, although relapse risk after discontinuation continues to limit prolonged use. Colchicine retains a stable position due to its effectiveness in suppressing neutrophil-mediated inflammation during acute attacks, particularly in patients with recurrent flares.

By Application

Chronic gout represents the dominant application segment, contributing roughly 67 percent of total market revenue in 2025. Growth in this segment reflects a shift in clinical focus toward long-term disease control, driven by improved diagnosis rates and expanded access to urate-lowering therapies. Commercial availability of multiple chronic treatment options has increased treatment persistence, supporting steady revenue growth through the forecast period.

Acute gout accounts for a smaller share of the market, as therapies in this segment focus on short-term symptom relief rather than disease modification. NSAIDs, colchicine, and corticosteroids remain standard options during acute flares, particularly in emergency and urgent care settings. Lower treatment adherence and limited duration of use constrain revenue contribution compared with chronic therapies.

Despite its smaller share, acute gout treatment remains clinically significant. Rising awareness and earlier diagnosis continue to support demand, especially in newly diagnosed patients and those experiencing intermittent flare episodes.

By End-Use

Hospitals remain the largest end-user segment in 2025, driven by their central role in managing acute gout flares and severe complications. Many hospitals operate dedicated rheumatology units that support both inpatient flare management and outpatient follow-up for chronic disease. High patient inflow and access to specialist care reinforce hospital dominance in therapeutic utilization.

Clinics represent a growing share of the market, supported by the expansion of rheumatology practices, primary care networks, and urgent care centers. These facilities increasingly manage long-term gout care, including medication titration and monitoring of serum urate levels. Collaboration between clinics and hospitals improves continuity of care and supports stable demand across treatment settings.

Home care settings account for a smaller but rising portion of end-use demand. Increased use of oral urate-lowering agents and improved patient education support outpatient and self-managed treatment models, particularly among stable chronic patients.

By Region

North America remains the largest regional market, holding approximately 39.4 percent of global revenue in 2025. High disease prevalence, strong diagnosis rates, and established reimbursement frameworks support sustained demand in the United States and Canada. Access to specialist care and long-term therapy adherence continue to underpin regional performance.

Europe maintains a substantial share, supported by aging demographics and standardized treatment protocols across major healthcare systems. Western European markets show stable growth, while parts of Eastern Europe demonstrate gradual uptake as awareness and access improve.

Asia Pacific is the fastest-growing regional market, led by Japan, China, and India. Rising gout prevalence, improving healthcare infrastructure, and higher disposable income levels drive accelerated adoption of both acute and chronic therapies. Latin America and the Middle East and Africa remain smaller markets but show steady expansion as diagnostic capacity and treatment awareness increase beyond 2025.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Drug Class

- NSAIDs

- Corticosteroids

- Colchicine

- Urate-Lowering Agents

By Disease Condition

- Acute Gout

- Chronic Gout

By End-User

- Hospital

- Clinics

- Home Care Setting

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.04 B |

| Forecast Revenue (2034) | USD 6.4 B |

| CAGR (2025-2034) | 8.40% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Drug Class (NSAIDs, Corticosteroids, Colchicine, Urate-Lowering Agents), By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospital, Clinics, Home Care Setting) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AstraZeneca, Sun Pharmaceutical Industries Ltd, Merck & Co Inc, Addex Therapeutics, Amgen Inc, Boehringer Ingelheim International GmbH, Pfizer Inc, TEIJIN LIMITED, Takeda Pharmaceutical Company Limited, AbbVie Inc, JW Pharmaceutical Corporation, GSK plc, Antares Pharma, Lilly, Teva Pharmaceuticals Industries Ltd, Astellas Pharma Inc, Novartis AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospitals, Clinics, Home Care Settings) Industry Region & Key Players – Industry Segment Overview, Epidemiology Trends, Treatment Landscape, Market Dynamics, Competitive Strategies, Innovation Pipeline, Regulatory Developments & Forecast 2025–2034")

, By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospitals, Clinics, Home Care Settings) Industry Region & Key Players – Industry Segment Overview, Epidemiology Trends, Treatment Landscape, Market Dynamics, Competitive Strategies, Innovation Pipeline, Regulatory Developments & Forecast 2025–2034")

, By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospitals, Clinics, Home Care Settings) Industry Region & Key Players – Industry Segment Overview, Epidemiology Trends, Treatment Landscape, Market Dynamics, Competitive Strategies, Innovation Pipeline, Regulatory Developments & Forecast 2025–2034")

Frequently Asked Questions

How big is the Gout Therapeutics Market?

The Global Gout Therapeutics Market was valued at USD 2.8 Billion in 2024 and is projected to reach USD 6.4 Billion by 2034, growing at a CAGR of 8.4% from 2026–2034. Discover market trends, key drivers, treatment innovations, competitive landscape, and future opportunities in the gout treatment industry.

Who are the major players in the Gout Therapeutics Market?

AstraZeneca, Sun Pharmaceutical Industries Ltd, Merck & Co Inc, Addex Therapeutics, Amgen Inc, Boehringer Ingelheim International GmbH, Pfizer Inc, TEIJIN LIMITED, Takeda Pharmaceutical Company Limited, AbbVie Inc, JW Pharmaceutical Corporation, GSK plc, Antares Pharma, Lilly, Teva Pharmaceuticals Industries Ltd, Astellas Pharma Inc, Novartis AG

Which segments covered the Gout Therapeutics Market?

By Drug Class (NSAIDs, Corticosteroids, Colchicine, Urate-Lowering Agents), By Disease Condition (Acute Gout, Chronic Gout), By End-User (Hospital, Clinics, Home Care Setting)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date