- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Green Building Materials Market Size, Share | CAGR 10.2%

Global Green Building Materials Market Size, Share, Analysis By Product Type (Insulation, Roofing & Siding, Framing, Interior Finishes, Eco-friendly Concrete & Cement, Sustainable Wood), By Material Source (Recycled Content, Renewable Resources, Low-VOC, Bio-Based Materials), By Application (Residential Construction, Commercial Offices, Industrial Facilities, Institutional Buildings), By End-User (Real Estate Developers, Contractors, Government Agencies, Architecture Firms) Region & Key Players-Segment Overview, Dynamics, Strategies & Forecast 2026-2035

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

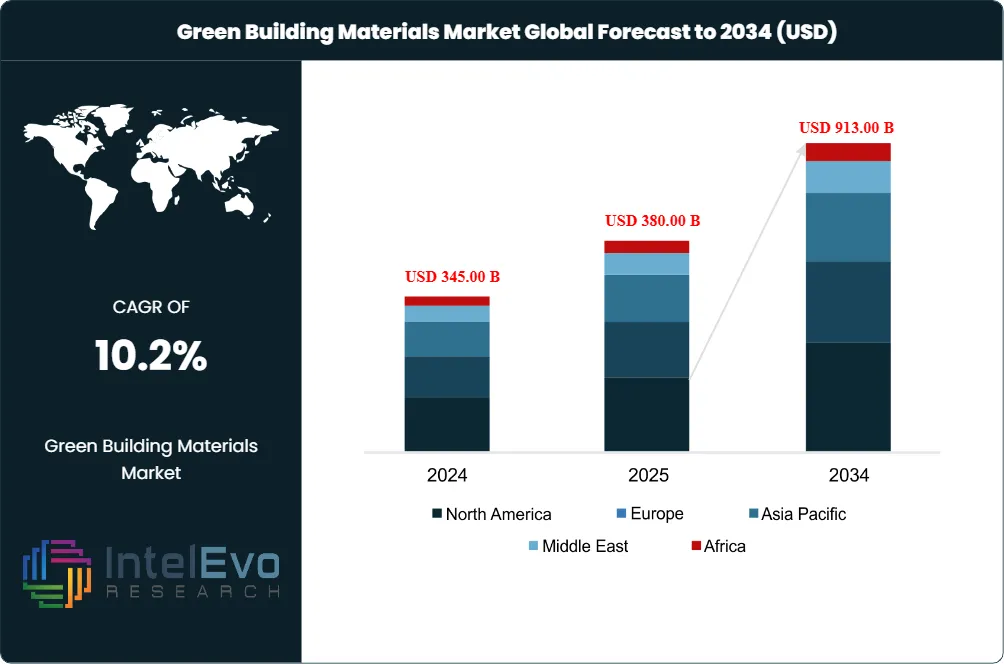

| USD 380.00 Billion | USD 913.00 Billion | 10.2% | North America, 34.0% |

The Green Building Materials Market was valued at approximately USD 345.00 Billion in 2024 and approximately USD 380.00 Billion in 2025. The market is projected to reach approximately USD 913.00 Billion by 2034, expanding at a CAGR of 10.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of approximately USD 533.00 billion over the analysis period, making it one of the construction sector's most capital-intensive transitions of the current decade.

Get More Information about this report -

Request Free Sample ReportThe primary demand driver is a structurally tightening regulatory environment: the U.S. Inflation Reduction Act of 2022 allocated over USD 369 billion toward climate and energy investments, including energy-efficient construction and renovation, while the European Union's Energy Performance of Buildings Directive (EPBD) mandates measurable energy efficiency improvements across renovated building stock. Together, these two policy frameworks directly incentivize substitution of conventional materials with certified alternatives, because compliance now determines access to public procurement contracts and tax relief programmes rather than merely conferring a marketing advantage.

Technology dynamics reinforce regulatory pressure. The U.S. Green Building Council launched LEED v5 in April 2025, placing embodied carbon for the first time at the centre of the point-scoring system, with 50% of credits linked to decarbonization outcomes. This revision compels architects, developers, and materials specifiers to source products carrying verified environmental product declarations (EPDs) — a requirement that insulation, roofing, structural, and interior materials must now satisfy to qualify for specification on LEED-targeted projects across North America. Simultaneously, BREEAM Outstanding category thresholds in the United Kingdom and European markets continue to tighten, expanding the addressable addressable opportunity for manufacturers of cellulose insulation, mineral wool, cross-laminated timber (CLT), and low-carbon cement.

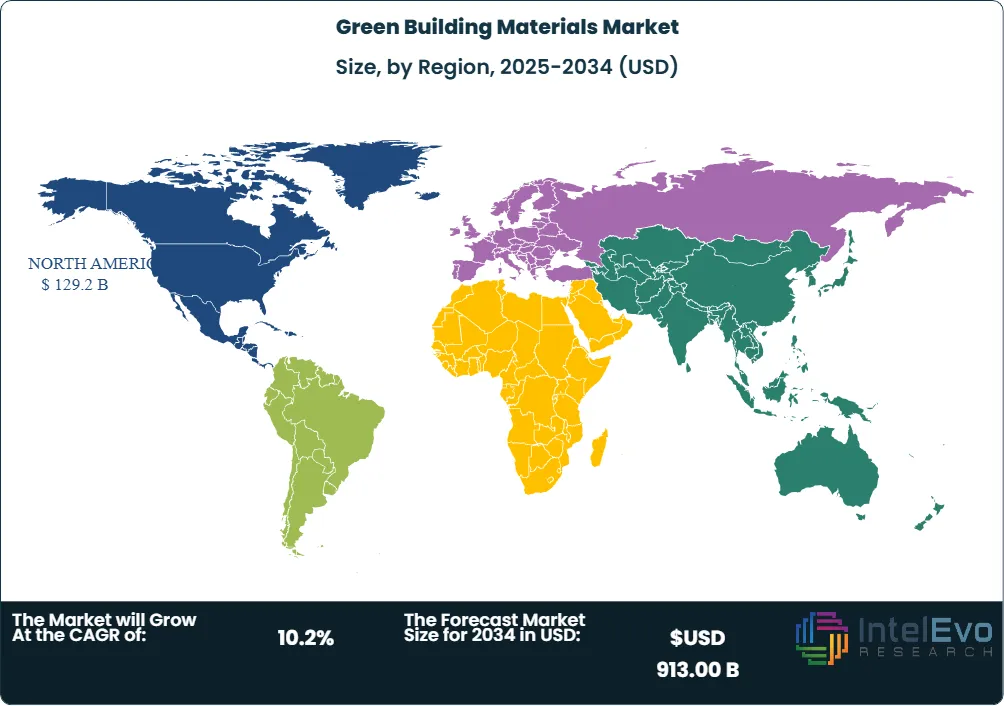

North America retained the leading regional position with approximately 34.0% of global market revenue in 2025 — roughly USD 129.2 billion — driven by the Inflation Reduction Act's 179D commercial building deduction expansion, state-level zero-energy-ready building mandates in California and Colorado, and the USGBC's LEED certification network covering more than 100,000 registered projects in 170 countries. Asia Pacific ranked second at approximately 27.0% of the global market, with China's mandate requiring all new projects to achieve Basic Grade green certification and India's updated Energy Conservation Building Code (ECBC 2024) compelling low-carbon material uptake in large commercial construction.

The competitive environment spans global diversified building materials conglomerates — Holcim Ltd, Saint-Gobain S.A., Kingspan Group plc, Owens Corning — alongside specialty material innovators targeting bio-based and circular segments. Over the trailing 12 months, disclosed M&A activity in the sector exceeded USD 4.0 billion, with CRH plc's USD 2.1 billion close of Eco Material Technologies and Holcim Ltd's EUR 1.85 billion agreement to take ownership of Xella representing the two largest deals. These transactions signal consolidation around circular and low-carbon material platforms rather than volume-based cement and aggregate capacity alone.

Through the forecast period ending 2034, industry analysis indicates that green building materials adoption in the residential segment will accelerate beyond its current pace, driven by net-zero housing mandates emerging in Germany, the Netherlands, and South Korea, and by retrofit incentive programmes that reduce consumer price sensitivity to premium green material pricing. The commercial segment will continue to command the largest absolute volume, anchored by institutional investor ESG screening that ties property valuations to LEED or BREEAM certification status — a relationship that real estate consultants now price into cap rate assumptions for commercial real estate assets in developed markets.

Market Definition & Scope

The green building materials market is defined as the global commercial supply of construction products and systems that demonstrably reduce environmental impact across the product lifecycle — from raw material extraction through manufacture, installation, operational use, and end-of-life recovery — relative to conventional material alternatives performing equivalent functional roles. The market encompasses structural materials (low-carbon cement and concrete, recycled steel, engineered mass timber such as cross-laminated timber and glued laminated timber), thermal and acoustic insulation (cellulose, mineral wool, polyisocyanurate, bio-based foam), roofing systems (cool roofs, green living roofs, solar-integrated membranes), exterior siding and facade products, interior finishing materials (low-VOC paints and adhesives, recycled-content flooring, formaldehyde-free board products), and energy-efficient glazing and window assemblies.

This analysis covers new construction and renovation applications across residential, commercial, industrial, and infrastructure end-uses globally. Excluded from scope are mechanical, electrical, and plumbing (MEP) systems such as HVAC equipment, photovoltaic panels as standalone energy assets, and smart building control software — categories that function as building systems rather than structural or envelope materials. The green building materials market constitutes a sub-segment of the broader global construction materials market, which the World Green Building Council estimates consumes 40% of global energy-related carbon emissions — a statistic that defines the policy urgency driving materials substitution.

, By Material Source (Recycled Content, Renewable Resources, Low-VOC, Bio-Based Materials), By Application (Residential Construction, Commercial Offices, Industrial Facilities, Institutional Buildings), By End-User (Real Estate Developers, Contractors, Government Agencies, Architecture Firms) Region & Key Players-Segment Overview, Dynamics, Strategies & Forecast 2026-2035")

Key Takeaways

- Market Growth: The global green building materials market was valued at approximately USD 380.00 billion in 2025 and is projected to reach approximately USD 913.00 billion by 2034, at a CAGR of 10.2%, representing an absolute opportunity of approximately USD 533.00 billion.

- Segment Dominance (By Application): The insulation sub-segment held the largest application share at approximately 35.9% in 2025, driven by mandatory energy-efficiency code compliance and the measurable thermal performance benefits of cellulose, mineral wool, and advanced polyisocyanurate systems.

- Segment Dominance (By End-Use): The residential segment accounted for approximately 55.0% of total market revenue in 2025, supported by net-zero housing incentive programmes in the United States, European Union, and South Korea that lower upfront cost barriers for homebuilders.

- Driver: Mandatory certification frameworks — LEED v5, BREEAM Outstanding, and the EU EPBD — represent the primary structural driver; the USD 369 billion Inflation Reduction Act alone is estimated to catalyse approximately USD 45 billion in energy-efficient construction material investment through 2032.

- Restraint: Premium pricing relative to conventional materials remains the primary constraint, with green building materials commanding a cost premium of 15%-30% at the product level — a gap that limits adoption in price-sensitive developing markets and unsubsidised residential segments.

- Opportunity: The global building retrofit and renovation segment represents an addressable opportunity of approximately USD 120 billion within the green building materials addressable market by 2034, as energy performance regulations require upgrades to approximately 35%-40% of existing commercial building stock in developed economies.

- Trend: Digital material tracking via environmental product declarations (EPDs) and embodied carbon accounting tools is transitioning from voluntary differentiator to bid requirement, with the Australian Government's Low-Carbon Concrete Requirements mandating at least 40% embodied carbon reductions for public infrastructure procurements.

- Regional: North America led with approximately 34.0% of global market share in 2025, translating to approximately USD 129.2 billion, anchored by the U.S. Inflation Reduction Act, LEED certification leadership, and ENERGY STAR programme penetration across residential and commercial building sectors.

Key Insights Summary

- Buildings contribute approximately 40% of global energy-related carbon emissions, according to the World Economic Forum, with construction materials responsible for a material portion of embodied carbon; this figure drives regulatory urgency in more than 70 countries where green building certification has moved from voluntary to mandatory for public sector projects since 2023.

- The U.S. Department of Energy's Building Technologies Office estimates that advanced thermal insulation deployment in existing residential stock could cut annual U.S. building energy consumption by up to 15%, a finding that directly informs the Inflation Reduction Act's expanded 45L New Energy Efficient Home Credit, which covers qualifying insulation and envelope materials.

- Owens Corning disclosed in its April 2025 sustainability report that 51% of company revenue derived from energy-efficient product categories in 2024, while cumulative Scope 1 and Scope 2 market-based greenhouse gas emissions fell 43% from the 2018 base year — an 11 percentage point reduction achieved in 2024 alone.

- Kingspan Group plc reported in February 2026 that its QuadCore insulated panel formulation accounts for 27% of total global insulated panel revenue, with the company reducing its own greenhouse gas emissions by 70% since 2020 despite doubling total revenue over the same period — a derived R&D intensity metric that positions QuadCore as the sector's highest-carbon-efficiency insulated panel platform.

- The European walling market, estimated at EUR 12 billion in 2025, is projected to expand to EUR 16 billion by 2030 under the energy efficiency regulatory mandate framework, according to Holcim Ltd's investor presentation accompanying the October 2025 Xella acquisition — a CAGR implied at approximately 5.9% for that segment alone.

- India's updated Energy Conservation Building Code 2024 mandates energy-efficient, low-carbon materials in large commercial buildings, expanding the addressable green building materials base in one of the world's fastest-urbanising economies; the Indian Green Building Council registered more than 10.84 billion square feet of green-certified space by early 2025.

Competitive Landscape Overview

The global green building materials market is moderately consolidated, with the top four companies — Holcim Ltd, Saint-Gobain S.A., Kingspan Group plc, and Owens Corning — collectively holding a leading position across insulation, structural, roofing, and facade product categories, though none commands a single-digit percentage of a market this diffuse. Competition operates across three primary axes: technology differentiation (embodied carbon certification, EPD documentation, thermal performance coefficients), geographic scale (manufacturing proximity to construction markets to reduce transport emissions and logistics cost), and portfolio breadth (single-vendor envelope solutions vs. specialty product supply).

The competitive dynamic is shifting from price-per-unit toward total lifecycle cost and certification compatibility. LEED v5 and BREEAM Outstanding specifications increasingly require materials to carry third-party-verified EPDs, a barrier that advantages manufacturers with established certification infrastructure — primarily European and North American multinationals — over emerging regional competitors. Concurrently, M&A is accelerating platform consolidation: CRH plc's September 2025 closure of the USD 2.1 billion Eco Material Technologies deal and Holcim Ltd's EUR 1.85 billion agreement to bring Xella into its portfolio signal that incumbents are assembling circular-economy material platforms, positioning recycled-content and low-carbon products alongside conventional materials to serve the full building-materials value chain.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Holcim Ltd | Switzerland | Leader | ECOPact, ECOPlanet, Elevate roofing | Global | Concluded €1.85B binding deal for Xella walling (Oct 2025); CHF 15.7B net sales in 2025 |

| Saint-Gobain S.A. | France | Leader | ISOVER insulation, CertainTeed, WICONA glazing | Europe, N. America | Rolled out ISOVER bio-based glass wool line with 35% lower embodied carbon (Feb 2025) |

| Kingspan Group plc | Ireland | Leader | QuadCore insulated panels, KoolDuct, Kooltherm | Europe, Global | Posted record €9.2B revenue in 2025; entered North American roofing market |

| Owens Corning | USA | Leader | Fiberglas insulation, PINK Next Gen, Thermafiber | N. America, Europe | 51% of revenue from sustainable products in 2024; 43% Scope 1+2 GHG reduction vs 2018 baseline |

| BASF SE | Germany | Challenger | Elastopor, Neopor, Styropor EPS, Elastocool | Europe, Global | Committed EUR 19.5B to sustainable technology programmes through 2027 |

| CRH plc | Ireland/USA | Challenger | Eco Material SCMs, Oldcastle BuildingEnvelope | N. America | Closed USD 2.1B acquisition of Eco Material Technologies, a near-zero-carbon SCM producer (Sep 2025) |

| Sika AG | Switzerland | Niche Player | Sikaflex sealants, SikaRoof, SikaWall systems | Europe, APAC | Expanded circular-construction product range aligned with LEED v4.1 credits |

| ROCKWOOL International A/S | Denmark | Niche Player | ROCKWOOL stone wool, ROCKFON ceilings | Europe, Americas | Commissioned new high-capacity stone-wool line in the USA to capture IRA retrofit demand |

| Cemex S.A.B. de C.V. | Mexico | Niche Player | Vertua low-carbon cement, Regenera recycled aggregates | Latin America, Global | Expanded Regenera recycling unit; processes 400,000 tonnes of construction waste annually |

By Application

The insulation segment captured approximately 35.9% of global green building materials market revenue in 2025 — the largest single application — because thermal performance improvement delivers the most measurable payback for building owners through reduced heating and cooling expenditure. Green insulation materials, including cellulose derived from recycled newsprint, mineral wool (stone wool and glass wool), sheep's wool, and advanced bio-based polyurethane foams, provide R-values competitive with conventional fiberglass while carrying substantially lower lifecycle carbon profiles. Owens Corning's PINK Next Gen fiberglass insulation and Kingspan's Kooltherm phenolic foam boards exemplify products that satisfy both performance and environmental benchmarks demanded by LEED v5 Material & Resources credits. Between 2022 and 2025, the unit cost of mineral wool insulation per square metre fell by approximately 12% due to capacity expansions in Eastern Europe, making it more accessible for retrofit projects in price-sensitive residential markets.

The roofing segment held approximately 24.3% of application revenue in 2025 and is the fastest-growing application, supported by the proliferating adoption of cool roofs, solar-integrated membranes, and living green roofs in commercial and institutional projects. Cool roofs reflect solar radiation rather than absorbing it, and the U.S. Environmental Protection Agency's Energy Star Cool Roof qualification programme estimates that green roofs reduce building energy consumption by approximately 0.7% annually on a per-building basis — a modest unit improvement that scales significantly across urban real estate portfolios. Holcim Ltd's Elevate roofing and insulation platform and ROCKWOOL International's acoustic and fire-rated roof systems compete in the premium commercial segment, while James Hardie Industries plc and Bauder Ltd address the mid-market with fiber cement and bituminous membrane alternatives.

Interior finishing accounted for approximately 20.8% of application revenue in 2025. Products in this segment — low-VOC paints, formaldehyde-free medium-density fibreboard, recycled-content carpet tiles, and linoleum flooring — address indoor air quality, a growing specification criterion as developers pursue WELL Building Standard certification alongside LEED. Interface, Inc., which committed to a carbon-negative carpet tile product called Climate+, and Forbo Holding AG, with its Marmoleum natural linoleum range, demonstrate how sustainability commitments translate into product differentiation strategies within this segment. Framing contributed approximately 12.0%, led by engineered mass timber products including CLT and glued laminated timber (glulam), which sequester biogenic carbon and substitute for structurally equivalent but carbon-intensive conventional concrete and steel. Exterior siding rounded out the remaining approximately 7.0%, driven by fiber cement composites and recycled metal facade systems.

By End-Use Industry

The residential segment represented approximately 55.0% of green building materials revenue in 2025, retaining its dominant position because homebuilder volume and government incentive penetration are both substantial. In the United States, the IRA's Section 25C Energy Efficient Home Improvement Credit offers homeowners a 30% tax credit on qualifying insulation and exterior door products, directly lowering the cost premium barrier that historically constrained residential adoption. In Germany, the Kreditanstalt fur Wiederaufbau (KfW) Energy Efficient Renovation programme provides subsidised loans for insulation and window upgrades, channelling an estimated EUR 10 billion annually toward residential retrofit projects that use certified green materials. Developer economics further support residential dominance: green-certified single-family homes command resale price premiums of 7%-15% in markets where LEED and ENERGY STAR certification data are publicly accessible, creating a commercial incentive layered atop regulatory compliance.

Commercial construction accounted for approximately 37.9% of market revenue in 2025. Institutional investor demand for ESG-compliant assets, corporate net-zero commitments, and tenant preference for certified workspaces drive material specification decisions in office, retail, hospitality, and healthcare construction. Around 35%-40% of existing commercial building stock in developed economies is expected to require energy-efficiency upgrades before 2034 to comply with tightening performance standards — a retrofit pipeline that sustains demand for thermal insulation systems, facade refurbishment materials, and low-VOC interior products throughout the forecast period. Industrial and institutional end-use absorbed the remaining approximately 7.1% of revenue, with data centre construction emerging as an unexpected growth sub-channel: hyperscale operators including AWS, Microsoft, and Google have embedded scope 3 supplier decarbonisation requirements that compel structural and envelope material suppliers to provide EPDs as a condition of approval.

By Material Type

Structural materials — encompassing low-carbon cement, fly-ash supplementary cementitious materials (SCMs), recycled steel, and engineered mass timber — held approximately 37.0% of market revenue in 2025. This segment benefits from the highest absolute volume of raw material consumption per building project, as structural components represent the largest material mass in any construction activity. CRH plc's September 2025 closure of the Eco Material Technologies acquisition secured access to approximately seven million tonnes of annual fly ash and pozzolan recycling capacity across 125 North American locations, making CRH among the most vertically integrated low-carbon cementitious materials producers in the region. Exterior materials — insulated panels, roofing systems, fiber cement cladding, and facade glazing — captured approximately 27.0% of revenue in 2025, with the Kingspan QuadCore insulated panel formulation and Saint-Gobain's WICONA structural glazing system representing leading products by technical specification citation. Interior materials accounted for approximately 26.0%, and bio-based and specialty materials captured the remaining approximately 10.0%, a fast-growing niche driven by hempcrete, mycelium composites, and bio-based polyurethane systems.

Regional Analysis

North America held the largest regional share of the global green building materials market at approximately 34.0% in 2025, equating to approximately USD 129.2 billion. The United States dominates the region, supported by the U.S. Green Building Council's LEED programme — the most widely adopted green building rating system globally — alongside the Inflation Reduction Act's USD 369 billion investment mandate, the ENERGY STAR certification programme administered by the U.S. Environmental Protection Agency, and California's 2025 Title 24 code cycle, which tightened both operational and embodied carbon limits for new commercial construction. Canada's Greener Homes Initiative, which provides low-interest loans for retrofit projects, funnels demand specifically into cellulose and mineral wool insulation — materials where domestic producers including Knauf Insulation and CertainTeed maintain installed manufacturing capacity.

Europe captured approximately 28.0% of global market revenue in 2025, at approximately USD 106.4 billion. The EU's Energy Performance of Buildings Directive and the Carbon Border Adjustment Mechanism (CBAM), which raises the effective cost of high-carbon imports, together create a structural cost advantage for domestic low-carbon material producers. Germany leads European demand through its Energiewende policy framework and the national Renovation Wave programme targeting climate-neutral building stock by 2045. The Netherlands has mandated whole-life-carbon assessments for all large buildings, while Scandinavian markets — Denmark, Sweden, and Norway — operate the most advanced embodied carbon tracking systems, directly influencing Kingspan, ROCKWOOL International, and Saint-Gobain's product development priorities.

Asia Pacific accounted for approximately 27.0% of global market revenue in 2025, equating to approximately USD 102.6 billion. China's national standard requiring Basic Grade green certification for all new projects drives volume, while provincial embodied-carbon benchmarks introduced in Guangdong and Jiangsu elevate specification standards beyond the basic threshold. India's ECBC 2024 update and Indonesia's Green Building Council rating system expand adoption in high-growth urbanising markets, though fragmented municipal code enforcement moderates near-term uptake. Australia and Singapore, both technically mature markets, are exporting best-practice frameworks across the ASEAN region, strengthening supply chain localisation in Malaysia, Vietnam, and Thailand where Kingspan and Saint-Gobain have manufacturing operations.

Latin America held approximately 6.5% of global market revenue in 2025, representing approximately USD 24.7 billion. Brazil's Procel Edifica labelling system and the March 2026 launch of the Green and Resilient Model Cities Program — piloting in Recife, Salvador, and Curitiba with backing from C40 Cities and the Global Covenant of Mayors — signal rising government commitment to green construction practices. The Mexican market, which benefits from proximity to U.S. supply chains and LEED project activity in commercial real estate, is the region's second-largest contributor. Multilateral lending institutions, including the International Finance Corporation, are increasingly directing green bond proceeds into residential construction projects in the region, reducing reliance on government subsidy alone.

Middle East & Africa represented approximately 4.5% of global market revenue in 2025, at approximately USD 17.1 billion. The UAE's Estidama Pearl Rating System and Saudi Arabia's Vision 2030 infrastructure programme — encompassing NEOM and other zero-carbon urban developments — are creating concentrated demand for facade insulation, cool roofing, and energy-efficient glazing suited to extreme heat climates. South Africa and Kenya represent the largest sub-Saharan markets, where international development finance is beginning to support green material supply chain localisation. Regional demand is constrained by limited domestic manufacturing of certified green materials, making logistics cost and import tariffs critical procurement considerations for project developers across the Middle East and North Africa.

Country Analysis

The United States green building materials market was valued at approximately USD 82.0 billion in 2025, with a country-level CAGR estimated at 8.2% from 2025 to 2034, anchored by the deepest LEED certification infrastructure globally and the most comprehensive federal incentive architecture. The Inflation Reduction Act's 45L credit extension, 25C home improvement credit, and 179D commercial building deduction collectively accelerate specification of insulation, energy-efficient windows and doors, and cool roofing systems in both new construction and renovation projects. The Western United States — particularly California, Washington, and Oregon — contributes approximately 34% of U.S. market value, driven by strict Title 24 energy codes and state procurement mandates requiring embodied-carbon limits on public infrastructure. Federal agencies through the General Services Administration now apply Environmental Product Declaration review to building material procurement, setting a precedent that is migrating into state and municipal procurement frameworks.

Germany's green building materials market reached approximately USD 28.5 billion in 2025, growing at an estimated country CAGR of 9.1% through 2034. The KfW Bundesfoerderbank's Bundesfoerderung fur effiziente Gebaeude (BEG) programme channelled EUR 18 billion in 2023 into energy-efficient construction and renovation, creating sustained demand for insulation systems, heat-pump-compatible ventilation materials, and Passive House-compliant building envelopes. German manufacturers including Knauf Gips KG and Heidelberg Materials AG occupy anchor positions in the domestic supply chain, with Knauf's mineral wool and gypsum board systems specified across both public social housing renovations and private new-build projects targeting the German Energy Savings Ordinance GEG 2023 compliance threshold.

China's green building materials market was valued at approximately USD 55.0 billion in 2025 — reflecting the country's massive construction volume — with an estimated country CAGR of 11.8% through 2034, the highest among the four country profiles. National policy requires all new buildings to meet the Basic Grade of China's Three-Star Green Building Certification, while the 14th Five-Year Plan (2021-2025) set a target of 70% of new urban buildings meeting green standards. Provincial governments in Guangdong and Jiangsu have extended embodied carbon benchmarks beyond the national baseline. Domestic manufacturers including China National Building Material Co. Ltd. (CNBM), a state-owned enterprise, dominate the structural materials segment, though multinational suppliers including Sika AG, BASF SE, and Saint-Gobain operate manufacturing facilities catering to commercial and institutional specifications.

India's green building materials market reached approximately USD 18.0 billion in 2025, with an estimated country CAGR of 13.5% through 2034 — the fastest among the four country profiles — reflecting the combination of rapid urbanisation, government housing programmes, and tightening energy codes. The ECBC 2024 update mandates energy-efficient, low-carbon materials in large commercial buildings for the first time, while the Pradhan Mantri Awas Yojana urban housing programme is beginning to incorporate green material specifications into contractor bid requirements. The Indian Green Building Council, affiliated with the Confederation of Indian Industry, surpassed 10.84 billion square feet of registered green-certified space in early 2025, making India the world's second-largest LEED-certified market by floor area. Domestic cement producers such as UltraTech Cement Ltd. are integrating fly ash and GGBS blends into standard product lines, while international suppliers including Sika AG and Knauf Gips KG are expanding local manufacturing to serve commercial project demand.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Application

- Residential Buildings

- Commercial Buildings

- Industrial Buildings

- Institutional Buildings

- Infrastructure Projects

- Renovation and Retrofitting

- Green Roofing Systems

- Interior Construction

- Exterior Construction

- Others

By End-Use Industry

- Residential Construction

- Commercial Construction

- Industrial Construction

- Healthcare Facilities

- Educational Institutions

- Hospitality and Tourism

- Government and Public Infrastructure

- Retail and Mixed-Use Developments

- Transportation Infrastructure

- Others

By Material Type

- Insulation Materials

- Structural Materials

- Green Cement and Concrete

- Recycled Steel

- Bamboo and Engineered Wood

- Low-Emission Glass

- Sustainable Flooring Materials

- Roofing Materials

- Paints and Coatings

- Recycled Plastic Building Materials

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 380.00 B |

| Forecast Revenue (2034) | USD 913.00 B |

| CAGR (2025-2034) | 10.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application, (Residential Buildings, Commercial Buildings, Industrial Buildings, Institutional Buildings, Infrastructure Projects, Renovation and Retrofitting, Green Roofing Systems, Interior Construction, Exterior Construction, Others), By End-Use Industry, (Residential Construction, Commercial Construction, Industrial Construction, Healthcare Facilities, Educational Institutions, Hospitality and Tourism, Government and Public Infrastructure, Retail and Mixed-Use Developments, Transportation Infrastructure, Others), By Material Type, (Insulation Materials, Structural Materials, Green Cement and Concrete, Recycled Steel, Bamboo and Engineered Wood, Low-Emission Glass, Sustainable Flooring Materials, Roofing Materials, Paints and Coatings, Recycled Plastic Building Materials, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HOLCIM LTD, SAINT-GOBAIN S.A., KINGSPAN GROUP PLC , OWENS CORNING, BASF SE , CRH PLC, SIKA AG , ROCKWOOL INTERNATIONAL A/S, CEMEX S.A.B. DE C.V. , PPG INDUSTRIES, INC., HEIDELBERG MATERIALS AG , KNAUF GIPS KG, JAMES HARDIE INDUSTRIES PLC , FORBO HOLDING AG, ARMSTRONG WORLD INDUSTRIES, INC. , STORA ENSO OYJ, INTERFACE, INC. , ALUMASC GROUP PLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material Source (Recycled Content, Renewable Resources, Low-VOC, Bio-Based Materials), By Application (Residential Construction, Commercial Offices, Industrial Facilities, Institutional Buildings), By End-User (Real Estate Developers, Contractors, Government Agencies, Architecture Firms) Region & Key Players-Segment Overview, Dynamics, Strategies & Forecast 2026-2035")

, By Material Source (Recycled Content, Renewable Resources, Low-VOC, Bio-Based Materials), By Application (Residential Construction, Commercial Offices, Industrial Facilities, Institutional Buildings), By End-User (Real Estate Developers, Contractors, Government Agencies, Architecture Firms) Region & Key Players-Segment Overview, Dynamics, Strategies & Forecast 2026-2035")

, By Material Source (Recycled Content, Renewable Resources, Low-VOC, Bio-Based Materials), By Application (Residential Construction, Commercial Offices, Industrial Facilities, Institutional Buildings), By End-User (Real Estate Developers, Contractors, Government Agencies, Architecture Firms) Region & Key Players-Segment Overview, Dynamics, Strategies & Forecast 2026-2035")

Frequently Asked Questions

How big is the Green Building Materials Market?

The Global Green Building Materials Market was valued at approximately USD 345.00 Billion in 2024 and approximately USD 380.00 Billion in 2025, and is projected to reach approximately USD 913.00 Billion by 2034, growing at a CAGR of 10.2% from 2026 to 2034. Market growth is driven by sustainable construction, energy-efficient buildings, and eco-friendly building materials.

Who are the major players in the Green Building Materials Market?

HOLCIM LTD, SAINT-GOBAIN S.A., KINGSPAN GROUP PLC , OWENS CORNING, BASF SE , CRH PLC, SIKA AG , ROCKWOOL INTERNATIONAL A/S, CEMEX S.A.B. DE C.V. , PPG INDUSTRIES, INC., HEIDELBERG MATERIALS AG , KNAUF GIPS KG, JAMES HARDIE INDUSTRIES PLC , FORBO HOLDING AG, ARMSTRONG WORLD INDUSTRIES, INC. , STORA ENSO OYJ, INTERFACE, INC. , ALUMASC GROUP PLC, Others

Which segments covered the Green Building Materials Market?

By Application, (Residential Buildings, Commercial Buildings, Industrial Buildings, Institutional Buildings, Infrastructure Projects, Renovation and Retrofitting, Green Roofing Systems, Interior Construction, Exterior Construction, Others), By End-Use Industry, (Residential Construction, Commercial Construction, Industrial Construction, Healthcare Facilities, Educational Institutions, Hospitality and Tourism, Government and Public Infrastructure, Retail and Mixed-Use Developments, Transportation Infrastructure, Others), By Material Type, (Insulation Materials, Structural Materials, Green Cement and Concrete, Recycled Steel, Bamboo and Engineered Wood, Low-Emission Glass, Sustainable Flooring Materials, Roofing Materials, Paints and Coatings, Recycled Plastic Building Materials, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Green Building Materials Market

Published Date : 01 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date