- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Green Chemicals Market Outlook Size, Growth & Trends | 11.8% CAGR

Global Green Chemicals Market Size, Share & Analysis By Product Type (Biopolymers, Bio-alcohols, Bio-organic Acids, Bio-ketones, Platform Chemicals, Others), By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics), Sustainability Regulations, Cost Competitiveness, Industry Leaders & Forecast 2025–2034

Report Overview

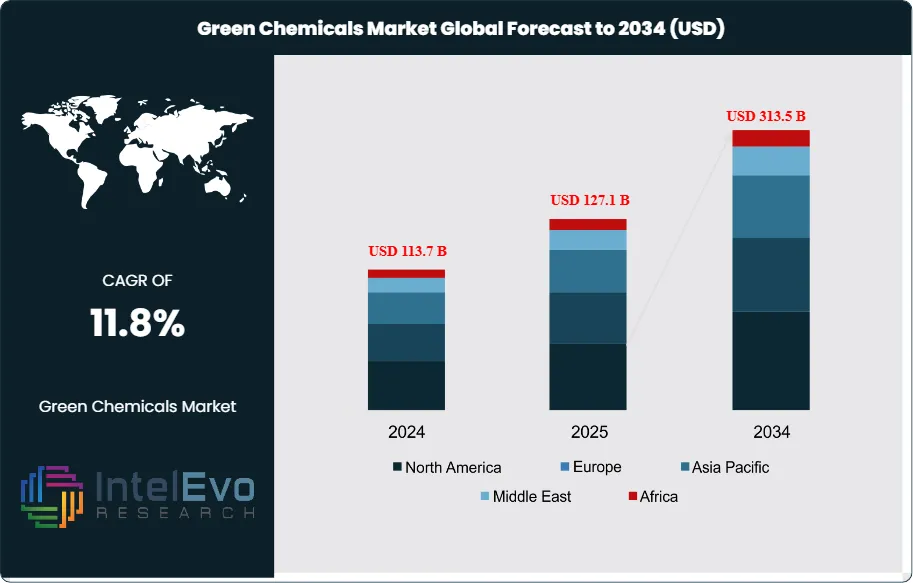

The Green Chemicals Market is estimated at USD 113.7 Billion in 2024 and is on track to reach roughly USD 313.5 Billion by 2034, implying a compound annual growth rate of 11.8% over 2024–2034. Growth is underpinned by a steady shift from petrochemical to bio-based and low-carbon inputs across packaging, textiles, agriculture, coatings, and consumer goods. Following feedstock price volatility in 2022, cost curves improved in 2023–2024 as renewable power availability rose and biobased feedstock supply stabilized, supporting margin recovery and reinvestment. Asia Pacific now accounts for an estimated 42–45% of global demand, Europe ~30–32% on the back of stringent sustainability regulations, and North America ~22–24% with accelerating corporate procurement of low-carbon materials. Over the forecast horizon, absolute growth is expected to be led by Asia, while Europe sustains premium pricing and faster adoption in specialty formulations.

Get More Information about this report -

Request Free Sample ReportDemand-side drivers include brand owner net-zero commitments, extended producer responsibility (EPR) for packaging, and end-market shifts toward low-VOC, non-toxic chemistries; more than 70% of large FMCG and apparel companies have announced Scope 3 targets, favoring green surfactants, solvents, and additives. On the supply side, scale in fermentation, catalysis, and electrified processing is narrowing the green premium; several key pathways—lactic acid to PLA, vegetable-oil-based polyols, and bio-ethanol to ethylene derivatives—are approaching cost parity at oil prices above USD 70–80/bbl. Regulatory momentum—from REACH and EU Green Deal provisions to emerging carbon disclosure rules—further embeds adoption, though risks persist around biomass availability, certification fragmentation, and capex intensity for first-of-a-kind plants.

Technological innovation is reshaping competitiveness. Synthetic biology and precision fermentation are lifting titers and yields by 10–25% versus prior generations; AI-assisted formulation design and digital twins are compressing development cycles by several months; and advanced recycling/CCU routes are opening drop-in options for solvents and monomers. Investment hotspots include bio-surfactants and specialty additives (projected CAGRs of ~13–16%), biopolymers such as PLA/PHA (~15%+), and high-performance, low-VOC coatings (~11–13%). India exemplifies the opportunity: green chemical concentrates for packaging, textiles, agriculture, and coatings are expanding within a chemical sector that contributes ~7% to GDP, employs 5+ million people, and is projected to grow from USD 220 billion (2022) to ~USD 300 billion by 2030. For investors, near-term value lies in platform technologies with multi-molecule optionality, regional feedstock integration in Asia, and specialty niches in Europe where regulatory tailwinds support premium margins.

, By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics), Sustainability Regulations, Cost Competitiveness, Industry Leaders & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Green Chemicals market is projected to expand from USD 113.7 billion in 2024 to USD 313.5 billion by 2034, reflecting a 11.8% CAGR; growth is propelled by regulatory pressure, brand-owner Scope 3 targets, and substitution of petrochemical inputs across packaging, textiles, agriculture, and coatings.

- Segment Dominance – Feedstock Source: Plant-based routes lead with 76.1% share, supported by mature sugar/starch and vegetable-oil supply chains and improving process yields that are narrowing the green premium to low-double digits in scaled assets.

- Segment Dominance – Product Type: Biopolymers command 39.2% share, driven by rapid adoption of PLA/PHA and bio-PE in rigid and flexible packaging; procurement programs at FMCG and retail brands are shifting volumes toward compostable and bio-attributed materials.

- Segment Dominance – End Use: Chemicals & materials account for 37.3% of demand as green solvents, surfactants, polyols, and additives integrate into adhesives, coatings, and intermediates where drop-in compatibility and compliance premiums sustain uptake.

- Driver: Corporate decarbonization is accelerating demand—over two-thirds of large FMCG/apparel companies now disclose Scope 3 reduction plans—while EPR and product-carbon-labeling rules are boosting adoption in packaging and specialty chemicals.

- Restraint: Cost and scale remain hurdles: green formulations often carry a 10–25% price premium versus fossil incumbents, and first-of-a-kind facilities face 20–40% higher capex and multi-year ramp-up risks tied to biomass availability and certification.

- Opportunity: Fastest growth is expected in biopolymers and biosurfactants (≈13–16% CAGR through 2034); India emerges as a manufacturing and demand hotspot as its chemicals sector scales from USD 220B (2022) to ~USD 300B (2030) with policy support for sustainable inputs.

- Trend: Process innovation—synthetic biology, precision fermentation, and electrified/reactive distillation—has lifted titers and yields by ~10–20% and, alongside AI-assisted formulation and digital twins, is shortening commercialization cycles by several months; leaders include BASF, Braskem (bio-PE), Corbion/NatureWorks (PLA), and Evonik (biosurfactants).

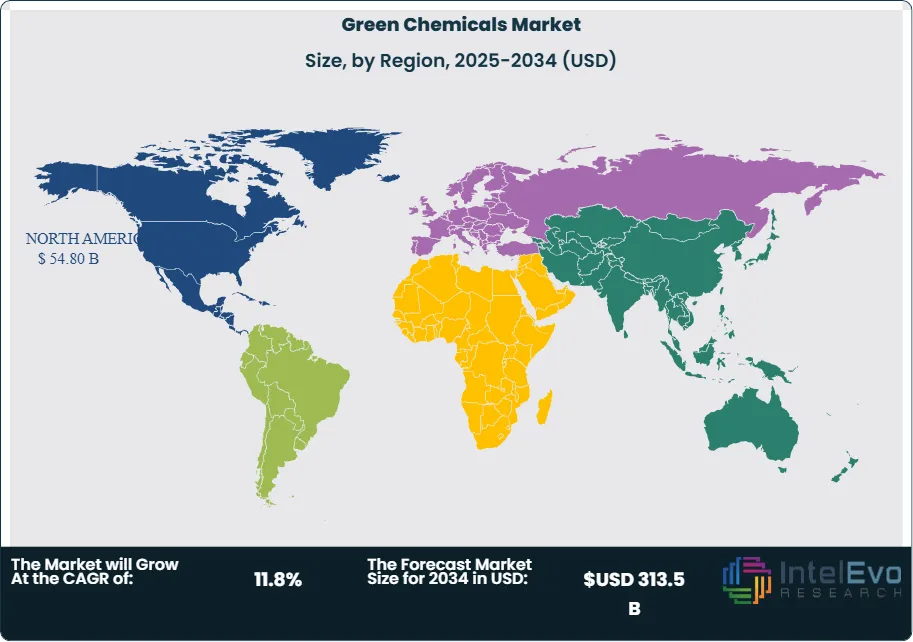

- Regional Analysis: North America led in 2024 with 48.2% share (~USD 53.8B), buoyed by corporate procurement and incentives; Asia Pacific is the fastest-growing region (~12–14% CAGR) on capacity build-outs and feedstock proximity, while Europe sustains premium pricing under Green Deal and REACH-driven substitution.

Type Analysis

Biopolymers remain the anchor of product demand, accounting for an estimated ~39.2% of global green-chemicals revenues in 2024 and poised to outpace the broader market through 2030–2034 as packaging, consumer goods, and automotive interiors prioritize compostable and bio-attributed materials. PLA, PHA, bio-PE, and starch blends are gaining share on the back of brand-owner targets and extended producer responsibility (EPR) rules; leaders such as NatureWorks/Corbion (PLA), Braskem (bio-PE), and Danimer (PHA) are expanding capacity and downstream partnerships. Bio-alcohols (e.g., bio-ethanol, bio-butanol) and platform chemicals (lactic, succinic, itaconic acids) are benefiting from drop-in compatibility with existing value chains, supporting cost-down trajectories as plants scale. Bio-organic acids and bio-ketones occupy smaller, specialty niches but command pricing power in high-purity food, pharma, and coatings applications.

From a feedstock lens, plant-based routes dominate with ~76.1% share in 2024, reflecting mature supply chains for sugars, starches, and vegetable oils; microorganisms are gaining traction in precision fermentation where yield gains of 10–20% are being reported, improving unit economics. Looking into 2025+, we expect biopolymers to post low-to-mid-teens CAGR, while bio-alcohols and platform chemicals expand at high single to low double digits as carbon-intensity thresholds and product-carbon disclosure requirements tighten across major markets.

Application Analysis

Packaging is the largest application, absorbing an estimated ~40–45% of biopolymer and bio-derived inputs as retailers and FMCG players accelerate transitions to compostable films, bio-PE bottles, and recyclable, low-VOC coatings. Adoption is reinforced by single-use plastic restrictions and recycled-content mandates, with procurement programs increasingly specifying bio-attributed or mass-balanced content. Coatings, adhesives, and sealants represent another sizable pool of demand, supported by green solvents, bio-based polyols, and low-toxicity additives that meet indoor-air-quality and product-safety standards.

Beyond consumer packaging, agriculture (bio-stimulants, biodegradable mulch), textiles and apparel (bio-based fibers/finishes), and personal care (biosurfactants, bio-emollients) are scaling from pilot to commercial volumes, collectively expected to grow at ~12–15% CAGR through the next decade. Electronics and transportation are emerging use cases, where drop-in bio-solvents and engineered biopolymers enable decarbonization without redesigning production assets—an important lever for cost-effective compliance.

End-Use Analysis

The chemical sector is the leading end-use, representing ~37.3% of market demand in 2024 as producers reformulate solvents, surfactants, resins, and intermediates to reduce Scope 1–3 emissions and align with customer specifications. Multinationals are leveraging mass-balance certification and green-attributed feedstocks to deliver low-carbon grades in adhesives, coatings, and performance materials, often at a modest premium where regulatory or brand-value benefits justify the switch.

Food & beverages and packaging are the fastest adopters of biopolymers and bio-alcohols, aided by safety certifications and rapid LCA verification cycles; pharmaceuticals and personal care are expanding use of high-purity bio-based inputs for excipients, actives, and mild surfactants. Automotive and transportation are integrating bio-polyols and bio-based composites in interiors and lightweighting, while building & construction is shifting to low-VOC coatings and bio-asphalt modifiers—together pointing to broadening end-use diversity and resilience of demand.

Regional Analysis

North America led in 2024 with ~48.2% share (≈USD 53.8 billion), underpinned by corporate procurement of low-carbon materials, incentives that improve after-tax project returns, and deep downstream markets in packaging and specialty chemicals. Europe remains a price-premium market due to REACH, Green Deal initiatives, and product-carbon disclosures that push rapid substitution in high-value niches; leaders such as BASF and Evonik are scaling biosurfactants and green intermediates in partnership with consumer brands.

Asia Pacific is the fastest-growing region (often cited at ~12–14% CAGR through 2034), supported by feedstock proximity, biorefinery build-outs, and expanding demand in China, India, and Southeast Asia. India, in particular, is emerging as a manufacturing and consumption hub: its chemicals sector (projected to rise from ~USD 220B in 2022 to ~USD 300B by 2030) provides scale for green concentrates in packaging, textiles, agriculture, and coatings. Latin America leverages sugarcane ethanol platforms (notably Brazil) for bio-ethylene and downstream derivatives, while the Middle East & Africa are early-stage but strategically investing in bio-based and CCU routes to diversify away from fossil incumbency and meet export-market standards.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Based on Product Type

- Biopolymers

- Bio-alcohols

- Bio-organic Acids

- Bio-ketones

- Platform Chemicals

- Others

Based on Source

- Plant-Based

- Animal-Based

- Microorganisms

Based on End-Use

- Chemical

- Food & Beverages

- Pharmaceuticals

- Automotive & Transportation

- Paints & Coatings

- Packaging

- Building & Construction

- Textiles & Apparel

- Electronics & Consumer Goods

- Personal Care & Cosmetics

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 113.7 B |

| Forecast Revenue (2034) | USD 313.5 B |

| CAGR (2024-2034) | 11.8% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Biopolymers, Bio-alcohols, Bio-organic Acids, Bio-ketones, Platform Chemicals, Others), By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Novozymes A/S, Toray Industries, Inc., Braskem, Corbion N.V., Valero Energy Corporation, Amyris, Inc., BASF SE, DSM, DuPont, Mitsubishi Chemical Group Corporation, BioAmber, Inc., Archer Daniels Midland, Green Plains Inc., Evonik Industries AG, PTT Global Chemical, SABIC, POET, LLC, Cargill, Incorporated, Arkema, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics), Sustainability Regulations, Cost Competitiveness, Industry Leaders & Forecast 2025–2034")

, By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics), Sustainability Regulations, Cost Competitiveness, Industry Leaders & Forecast 2025–2034")

, By Source (Plant-Based, Animal-Based, Microorganisms), By End-Use (Chemical, Food & Beverages, Pharmaceuticals, Automotive & Transportation, Paints & Coatings, Packaging, Building & Construction, Textiles & Apparel, Electronics & Consumer Goods, Personal Care & Cosmetics), Sustainability Regulations, Cost Competitiveness, Industry Leaders & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date