- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Green Hydrogen Electrolyzer Market Size, Share | CAGR 30.0%

Global Green Hydrogen Electrolyzer Market Size, Share Analysis By Tech (Alkaline, PEM, Solid Oxide, AEM, High-Temp, Hybrid), By Capacity (Below 100kW, 100kW-1MW, 1-10MW, 10-50MW, 50-100MW, Above 100MW), By Application (Power/Storage, Industrial Feedstock, Mobility, Ammonia, Steel, Chemical, Refueling), By End-User (Utilities, Chemical, Oil & Gas, Transport, Government) Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 4.5 Billion | USD 47.5 Billion | 30.0% | North America, 32.0% |

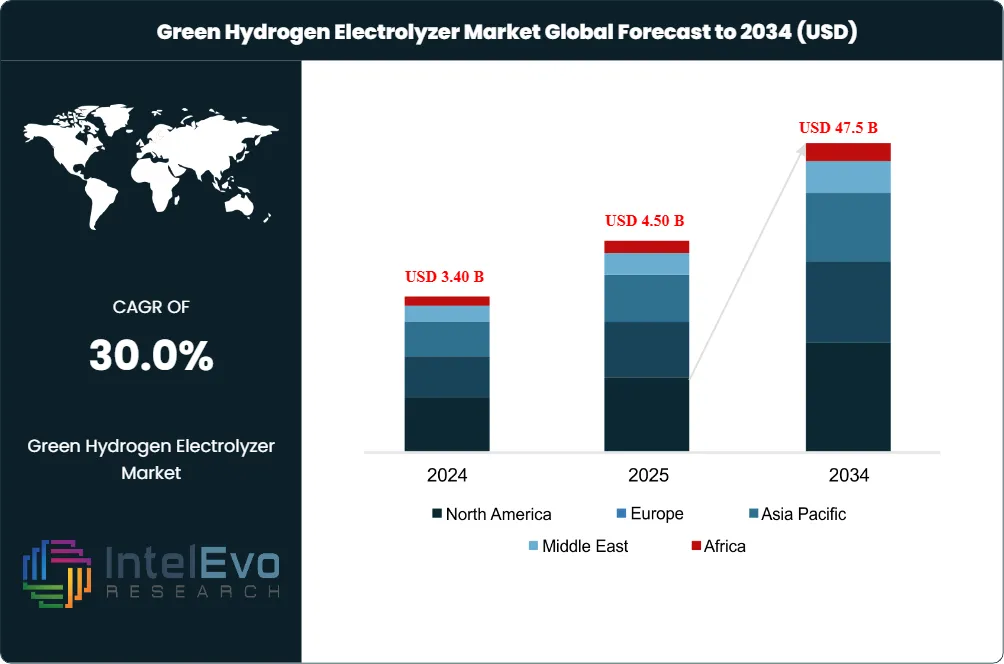

The Green Hydrogen Electrolyzer Market was valued at USD 3.40 Billion in 2024 and USD 4.50 Billion in 2025. The market is projected to reach USD 47.5 Billion by 2034, expanding at a CAGR of 30.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 43.0 Billion over the analysis period. The Green Hydrogen Electrolyzer Market is moving from auction-led pilot demand to industrial procurement as steel, ammonia, refining, and mobility off-takers convert decarbonization pledges into binding gigawatt-scale orders.

Get More Information about this report -

Request Free Sample ReportDemand momentum stems from converging policy floors. The US Inflation Reduction Act 45V Clean Hydrogen Production Tax Credit, finalized in January 2025, provides up to USD 3 per kg for projects under 4 kg CO2e per kg lifecycle emissions across a 10-year credit window. The EU Hydrogen Bank's third auction (IF25) launched with a EUR 1.1 Billion budget. India's SIGHT Programme committed INR 17,490 crore (approximately USD 2.1 Billion) for electrolyzer manufacturing incentives, with 15 firms awarded 3,000 MW of annual capacity by May 2025.

Technology mix is bifurcating. Alkaline (AWE) electrolyzers dominate large-scale industrial deployments, with Western alkaline systems priced at USD 750-1,300 per kW versus Chinese alkaline at USD 300-500 per kW. PEM systems hold a premium tier at USD 2,000-2,450 per kW, prized for renewable-energy dynamic response. SOEC remains at demonstration scale at USD 3,000-5,000 per kW. The IF25 auction's requirement that at least 75% of electrolyzer units originate outside China is reshaping European procurement and accelerating onshore manufacturing.

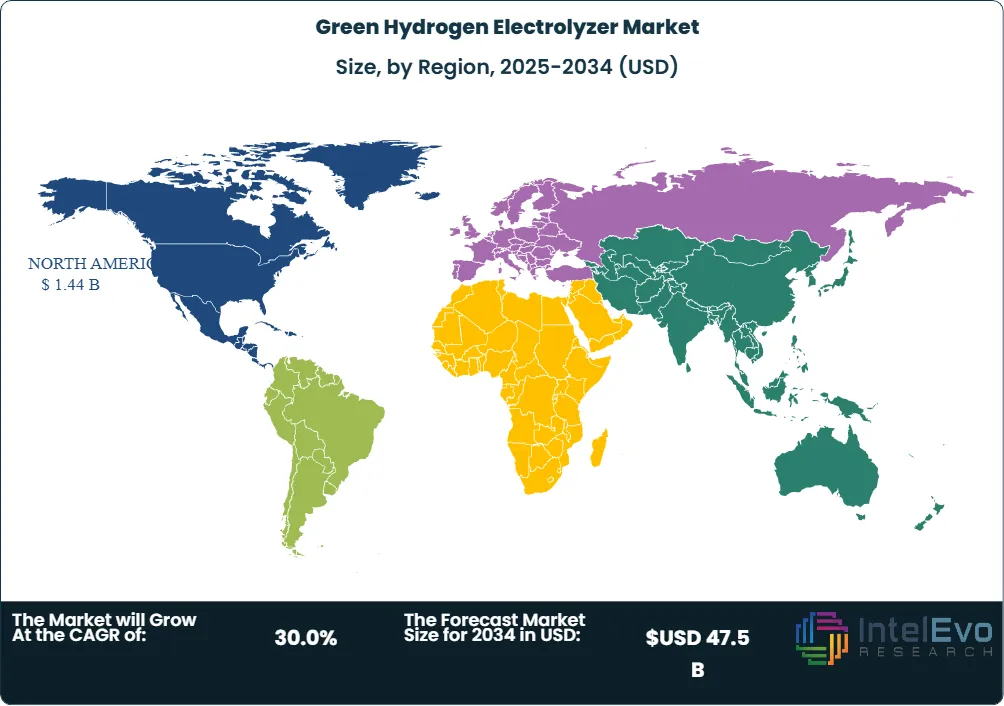

North America held the largest share of the Green Hydrogen Electrolyzer Market at 32.0% in 2025, generating USD 1.44 Billion, anchored by the IRA 45V credit and the US DOE's USD 7 Billion Regional Clean Hydrogen Hubs program. Europe captured 31.0% share at USD 1.35 Billion, with Germany committing USD 9.418 Billion under its National Hydrogen Strategy. Asia Pacific held 27.0% share at USD 1.26 Billion, led by China's 60% control of global manufacturing capacity and India's National Green Hydrogen Mission targeting 5 MMT annual production by 2030.

Forward-looking demand through 2034 will be driven by hard-to-abate industrial decarbonization, financial close on first-wave gigawatt projects, and consolidation of fragmented vendor pools through M&A. Hydrogen-as-a-feedstock procurement in steel, ammonia, and refining will absorb 60-70% of forecast electrolyzer capacity. The market is transitioning from venture-backed prototyping to bankable infrastructure procurement.

Market Definition & Scope

The Green Hydrogen Electrolyzer Market is defined as the global commercial market for water-electrolysis equipment that uses renewable electricity to split water into hydrogen and oxygen, producing hydrogen with lifecycle emissions of less than 4 kg CO2e per kg under IRA 45V or below 3 kg CO2e per kg of H2 under the EU RFNBO definition. The market encompasses electrolyzer stacks, balance-of-plant components, and integrated system packages across alkaline (AWE), Proton Exchange Membrane (PEM), Solid Oxide (SOEC), and Anion Exchange Membrane (AEM) technologies.

This analysis includes electrolyzer stacks, power electronics, gas-liquid separators, water treatment systems, control software, and after-sales service contracts. Excluded: revenues from the sale of the hydrogen molecule itself, upstream renewable generation assets, downstream fuel-cell systems, hydrogen storage tanks, and refueling infrastructure. Excluded blue and grey hydrogen production technologies (steam methane reforming, autothermal reforming with CCS). The Green Hydrogen Electrolyzer Market is a sub-segment of the broader water electrolysis equipment parent market, of which green-certified systems account for the majority of new orders post-2024.

, By Capacity (Below 100kW, 100kW-1MW, 1-10MW, 10-50MW, 50-100MW, Above 100MW), By Application (Power/Storage, Industrial Feedstock, Mobility, Ammonia, Steel, Chemical, Refueling), By End-User (Utilities, Chemical, Oil & Gas, Transport, Government) Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Green Hydrogen Electrolyzer Market grew from USD 4.5 Billion in 2025 toward USD 47.5 Billion by 2034 at a CAGR of 30.0%, an absolute dollar opportunity of USD 43.0 Billion.

- Segment Dominance (Technology): Alkaline (AWE) electrolyzers held the largest technology share at 49.0% in 2025, valued at USD 2.21 Billion, anchored by lowest capex and the chlor-alkali manufacturing legacy.

- Segment Dominance (Application): Industrial hydrogen production for refining, ammonia, and chemicals held a 60.0% application share at USD 2.70 Billion, with steelmaking accelerating fastest.

- Driver: The IRA 45V tax credit at up to USD 3 per kg, finalized January 2025, plus EUR 1.1 Billion in the third EU Hydrogen Bank auction, anchored procurement decisions for 2026-2028 financial close.

- Restraint: EU Hydrogen Bank auction project withdrawals totaling 1.9 GW of awarded capacity in 2025 highlighted offtake risk and grid-connection delays as the primary capital-deployment barrier.

- Opportunity: Mobility and grid-injection segments represent a USD 8 Billion incremental opportunity by 2034 as containerized PEM units enter steel mill and utility-scale balancing applications.

- Trend: AI-driven predictive maintenance and gigafactory consolidation are dominant trends, with Topsoe, Siemens Energy, and Accelera by Cummins scaling to 500 MW per year per facility.

- Regional: North America led with 32.0% share and USD 1.44 Billion in revenue in 2025, anchored by the USD 7 Billion DOE Regional Clean Hydrogen Hubs program and the 45V credit.

Key Insights Summary

- IRA 45V finalized: The US Treasury finalized the IRA 45V Clean Hydrogen Production Tax Credit rules in January 2025, locking in up to USD 3 per kg for projects under 4 kg CO2e per kg lifecycle emissions across a 10-year window.

- EU Hydrogen Bank IF25: The third EU Hydrogen Bank auction launched in Q4 2025 with a EUR 1.1 Billion budget, requiring at least 75% of electrolyzer units to originate outside China.

- Plug Power 2025 throughput: Plug Power shipped over 185 MW of GenEco PEM electrolyzers in 2025, representing 203% year-over-year growth and bringing cumulative shipments past 317 MW with USD 187 Million in revenue.

- Cost spread: Chinese alkaline electrolyzers price at USD 300-500 per kW versus Western alkaline at USD 750-1,300 per kW; PEM systems command USD 2,000-2,450 per kW for premium applications.

- India SIGHT awards: By May 2025, 15 firms had been awarded 3,000 MW of annual electrolyzer manufacturing capacity under India's SIGHT Programme, backed by INR 17,490 crore (approximately USD 2.1 Billion).

- China manufacturing dominance: China controls roughly 60% of global electrolyzer manufacturing capacity in 2025, with LONGi Hydrogen scaled to 2 GW annual output.

- EU auction churn: Of 2.3 GW awarded under the second EU Hydrogen Bank auction, projects totaling 1.9 GW withdrew before signing grant agreements, prompting reserve list activation for 10 projects with 774 MW combined.

Competitive Landscape Overview

The Green Hydrogen Electrolyzer Market is moderately consolidated. The combined market share of the top five players (Thyssenkrupp Nucera, Siemens Energy, John Cockerill, Nel ASA, and Cummins Accelera) is estimated at 60-65% of global revenue in 2025. Competition is technology and project-pipeline led, with vendors competing on stack efficiency, capex per kW, regulatory pre-qualification, and gigawatt-scale execution.

Competitive pressure intensified through 2025 as Plug Power tripled GenEco shipments to 185 MW, Cummins Accelera launched a 500 MW per year PEM facility in Guadalajara, Spain, and John Cockerill closed a USD 134.5 Million capital increase. M&A surfaced when H2 Green Steel acquired electrolyzer startup HydroGenics in Q1 2025. Bosch entered the North American market by commissioning its Hybrion PEM facility at Farmington Hills, Michigan in March 2026.

China-based vendors including LONGi Hydrogen and Sungrow are reshaping global price benchmarks at USD 300-500 per kW, while Western vendors anchor on quality, efficiency, and IRA/EU local-content compliance. The competitive matrix below benchmarks the ten most strategically active vendors.

Competitive Landscape Matrix

| Company | Headquarters | Position | Lead Technology | Geographic Strength | Recent Strategic Move |

| Thyssenkrupp Nucera | Dortmund, Germany | Leader | Pressurized alkaline (AWE) | EU, MENA, US | Delivered 2 GW NEOM alkaline backlog through 2025 |

| Siemens Energy AG | Munich, Germany | Leader | PEM (Silyzer line) | EU, US, Asia | Built 54 MW PEM unit at BASF Ludwigshafen in 2025 |

| Nel ASA | Oslo, Norway | Leader | PEM and alkaline | Norway, US, EU | Won EUR 135 Million EU Innovation Fund grant in October 2024 |

| Plug Power Inc. | Latham, New York, US | Leader | PEM GenEco platform | US, EU, Asia | Reported USD 187 Million electrolyzer revenue in 2025 |

| John Cockerill | Seraing, Belgium | Challenger | Pressurized alkaline | EU, India, China JV | Raised USD 134.5 Million in June 2025 capital increase |

| Cummins Inc. (Accelera) | Columbus, Indiana, US | Challenger | PEM electrolyzers | US, EU | Launched 500 MW PEM Guadalajara plant in April 2025 |

| LONGi Hydrogen | Xi'an, China | Challenger | Alkaline and PEM | China, Asia export | Scaled to 2 GW annual manufacturing capacity by 2025 |

| Asahi Kasei Corporation | Tokyo, Japan | Challenger | Alkaline electrolysis | Japan, EU, North America | Signed MoU with De Nora for pressurized alkaline systems |

| ITM Power plc | Sheffield, UK | Niche Player | PEM electrolyzers | UK, EU, APAC | Signed 300 MW APAC supply agreement in May 2025 |

| Bloom Energy Inc. | San Jose, US | Niche Player | Solid Oxide (SOEC) | US, South Korea | Won 200 MW SOEC contract for South Korea in Q2 2025 |

Segmentation Analysis

The Green Hydrogen Electrolyzer Market is segmented across four primary dimensions: by technology, by capacity, by application, and by end-user industry. Each dimension reflects a distinct procurement decision: technology determined by cost-vs-flexibility trade-off, capacity determined by project scale, application determined by hydrogen offtake destination, and end-user determined by industrial decarbonization roadmap.

By Technology

Alkaline (AWE) electrolyzers held the largest technology share at 49.0% in 2025, generating USD 2.21 Billion in revenue. The segment benefits from over a century of chlor-alkali manufacturing experience, lowest stack capex, and longer stack lifetimes. Thyssenkrupp Nucera's pressurized alkaline backlog includes the 1 GW NEOM delivery and gigawatt-scale projects in Saudi Arabia and Spain. Asahi Kasei expanded its alkaline portfolio through a September 2024 MoU with De Nora targeting small-scale pressurized systems.

PEM electrolyzers captured 35.0% technology share at USD 1.58 Billion in 2025, dominating renewable-coupled applications due to faster dynamic response and 30 bar output pressure. Plug Power, Siemens Energy (Silyzer), Nel ASA, and ITM Power anchor the PEM segment. SOEC held 9.0% share at USD 405 Million; Topsoe's 500 MW per year SOEC manufacturing facility in Denmark came online in 2025. AEM held 7.0% share at USD 315 Million and is forecast to record one of the fastest CAGRs as compact, precious-metal-free systems target distributed deployment. AEM is the procurement checklist option for buyers seeking PEM-class flexibility at alkaline-class capex.

By Capacity

Above-2 MW systems held the dominant capacity share at 65.0% in 2025, generating USD 2.93 Billion. Industrial offtakers in refining, ammonia, and steel require 5 MW-plus systems, driving large-scale procurement. Plug Power's 100 MW GenEco array deployed at GALP's Sines Refinery in Portugal and ITM Power's 300 MW APAC power-plant supply agreement signed in May 2025 illustrate the gigawatt-class trajectory of this segment.

The 500 kW to 2 MW segment held 28.0% share at USD 1.26 Billion in 2025, primarily serving mid-scale industrial gas, on-site refueling, and pilot project applications. Nel Hydrogen's 2.5 MW containerized PEM unit shipped to the Aberdeen Hydrogen Hub in March 2025 illustrates the segment's modular procurement pattern. The below-500 kW segment captured 7.0% share at USD 315 Million, populated by AEM and small PEM units in residential, small-commercial, and mobility applications. The above-2 MW segment exceeded the below-500 kW segment by 58 percentage points in 2025, illustrating the asymmetric weight of industrial-scale procurement in determining overall market revenue.

By Application

Industrial hydrogen production for refining, ammonia, methanol, and chemicals dominated the application segment at 60.0% share in 2025, generating USD 2.70 Billion. Plug Power's 100 MW Sines Refinery deployment in Portugal, Thyssenkrupp Nucera's 500 MW Saudi Arabia contract, and the BASF-Siemens Energy 54 MW Ludwigshafen unit producing 8,000 metric tons of green hydrogen annually anchor industrial demand. Power-to-gas and energy storage held 22.0% share at USD 990 Million, used for grid balancing and seasonal renewable storage.

Mobility applications captured 12.0% share at USD 540 Million in 2025, supplying hydrogen refueling stations and fuel-cell electric vehicle infrastructure. NTPC's high-altitude Leh hydrogen mobility project commissioned in November 2024 and the V.O. Chidambaranar Port Authority pilot illustrate emerging mobility deployment. Grid injection and other applications held 6.0% share. The industrial production application share exceeded mobility by 48 percentage points in 2025, reflecting the front-loaded weight of decarbonization mandates in heavy industry over the consumer transport pivot.

By End-User Industry

Chemicals and refining held the largest end-user share at 38.0% in 2025, generating USD 1.71 Billion. Refiners including BP (Aberdeen Hydrogen Hub joint venture), Shell (Holland Hydrogen 1, 200 MW PEM Rotterdam), and GALP anchor procurement. Steel and heavy industry captured 22.0% share at USD 990 Million, with H2 Green Steel's acquisition of HydroGenics in Q1 2025 illustrating vertical integration. Power and utilities held 17.0% share at USD 765 Million, anchored by Iberdrola, NTPC, and major US utilities adopting electrolyzers for grid balancing.

Mobility and transportation took 13.0% share at USD 585 Million, supporting fuel cell vehicles, buses, and shipping demonstrators. The Toyota-Bosch collaboration signaled by Bosch's March 2026 Farmington Hills commissioning targets the mobility segment specifically. Other end users including electronics, food processing, and laboratory applications took 10.0% share. The chemicals/refining end-user share exceeded all consumer-transport-adjacent applications combined, anchoring the procurement checklist for vendors prioritizing bankable industrial offtakers.

Regional Analysis

The Green Hydrogen Electrolyzer Market is concentrated in North America, Europe, and Asia Pacific, which together accounted for 90.0% of revenue in 2025. Latin America and Middle East and Africa contributed 10.0% combined but include the largest single project pipelines globally including NEOM.

North America

North America held the largest share of the Green Hydrogen Electrolyzer Market at 32.0% in 2025, generating USD 1.44 Billion. The United States contributed approximately USD 1.30 Billion, Canada USD 0.10 Billion, and Mexico USD 0.04 Billion. The IRA 45V tax credit (up to USD 3 per kg, finalized January 2025), the USD 7 Billion DOE Regional Clean Hydrogen Hubs program, and Treasury Department final rules anchor demand. Plug Power, Cummins Accelera, Bloom Energy, and Air Products are domestic vendor anchors. Bosch's March 17, 2026 Farmington Hills electrolyzer commissioning marked a German entrant scaling US PEM manufacturing. Accelera by Cummins delivered a 35 MW PEM electrolyzer to a New York industrial hydrogen facility in September 2025.

Europe

Europe captured 31.0% of the Green Hydrogen Electrolyzer Market in 2025, valued at USD 1.35 Billion. Germany, the United Kingdom, Spain, France, and the Netherlands lead European demand. The EU Hydrogen Bank concluded its second auction in 2025 awarding EUR 992 Million across 15 projects, with the third (IF25) auction launched in Q4 2025 with a EUR 1.1 Billion budget. The 75% non-China electrolyzer origin requirement is steering procurement to Thyssenkrupp Nucera, Siemens Energy, John Cockerill, ITM Power, and Nel ASA. Germany's National Hydrogen Strategy committed USD 9.418 Billion. The Hamburg Green Hydrogen Hub deploys 100 MW from Siemens Energy. Plug Power completed installation of a 100 MW GenEco array at GALP's Sines Refinery in Portugal in January 2026.

Asia Pacific

Asia Pacific held 27.0% share of the Green Hydrogen Electrolyzer Market in 2025, valued at USD 1.26 Billion, and is forecast to record one of the fastest CAGRs through 2034. China dominates regional manufacturing with roughly 60% global share and LONGi Hydrogen scaled to 2 GW annual capacity. India advanced its National Green Hydrogen Mission with INR 19,744 crore (approximately USD 2.4 Billion) total outlay; SECI awarded 3,000 MW of annual electrolyzer manufacturing capacity to 15 firms through Tranche I and II under the SIGHT Programme. Japan's Asahi Kasei expanded alkaline systems internationally, while Bloom Energy secured a 200 MW SOEC contract for South Korea in Q2 2025. Australia and Singapore anchor export-oriented green hydrogen project pipelines.

Latin America

Latin America held a 5.0% share of the Green Hydrogen Electrolyzer Market in 2025, valued at USD 225 Million. Brazil, Chile, and Argentina anchor regional demand. Chile's National Green Hydrogen Strategy targets export-grade production tied to its Atacama solar resource. Brazil's Pecem and Rio Grande do Norte hydrogen hub announcements are attracting Thyssenkrupp Nucera and Siemens Energy under ANEEL-coordinated tenders. The region offers premium solar capacity factors of 30-35%, supporting LCOH below USD 2.50 per kg in optimized projects.

Middle East & Africa

Middle East and Africa accounted for 5.0% of the Green Hydrogen Electrolyzer Market in 2025, valued at USD 225 Million. Saudi Arabia anchors regional demand through NEOM's 1.2 GW project, with Thyssenkrupp Nucera supplying alkaline electrolyzer capacity. The UAE, Oman, Egypt, and Morocco are advancing export-oriented green hydrogen mega-projects. The region offers some of the lowest LCOH globally given combined solar-wind hybrid capacity factors above 50%.

Country Analysis

The Green Hydrogen Electrolyzer Market is shaped at the country level by national hydrogen strategies, electrolyzer-specific manufacturing incentives, and the maturity of industrial offtake. The United States, Germany, China, and India anchor four distinct procurement playbooks.

United States

The United States Green Hydrogen Electrolyzer Market reached approximately USD 1.30 Billion in 2025 and is projected to grow at a CAGR of 31.5% through 2034. Federal policy drives demand: the IRA 45V Clean Hydrogen Production Tax Credit at up to USD 3 per kg finalized January 2025, the USD 7 Billion DOE Regional Clean Hydrogen Hubs program funding seven hubs, and the DOE Hydrogen Shot targeting USD 1 per kg production cost. Plug Power's Woodbine, Georgia facility produced 300 metric tons of liquid hydrogen in April 2025. Bosch commissioned its Farmington Hills, Michigan electrolyzer facility on March 17, 2026 for North American R&D. Nel Hydrogen US received purchase orders worth USD 13 Million combined across Q1 2025.

Germany

Germany generated approximately USD 530 Million in Green Hydrogen Electrolyzer Market revenue in 2025 and is forecast to grow at a country CAGR of 28.0% through 2034. Germany's National Hydrogen Strategy committed USD 9.418 Billion. Domestic vendors Thyssenkrupp Nucera (Dortmund), Siemens Energy (Munich), and Bosch (Stuttgart) anchor European technology leadership. The Hamburg Green Hydrogen Hub deploys 100 MW from Siemens Energy at the former Moorburg coal site, producing 10,000 metric tons of green hydrogen annually starting in 2027. BASF and Siemens Energy commissioned a 54 MW PEM unit (Germany's largest at the time) at BASF's Ludwigshafen complex in 2025.

China

China generated approximately USD 760 Million in Green Hydrogen Electrolyzer Market revenue in 2025 and is forecast to record a country CAGR of 32.0% through 2034. China controls roughly 60% of global electrolyzer manufacturing capacity, with LONGi Hydrogen, Sungrow Hydrogen, and Cockerill Jingli Hydrogen (CJH) anchoring scale. Chinese alkaline systems price at USD 300-500 per kW versus Western pricing at USD 750-1,300 per kW. The national hydrogen pilot program targets commercial-scale readiness by 2028, with subsidies stimulating provincial deployment. Concerns over efficiency claims raised by BloombergNEF in October 2024 prompted European procurement to require third-party verification of stack performance.

India

India generated approximately USD 250 Million in Green Hydrogen Electrolyzer Market revenue in 2025 and is forecast to grow at a country CAGR of 38.0% through 2034. The National Green Hydrogen Mission commits INR 19,744 crore (approximately USD 2.4 Billion) through 2029-30, including INR 17,490 crore for the SIGHT Programme. SECI awarded 3,000 MW of annual electrolyzer manufacturing capacity to 15 firms by May 2025, and 19 firms received cumulative 862,000 tonnes annual green hydrogen production allocations. The Green Hydrogen Certification Scheme of India (GHCI) launched in April 2025. In October 2025, MNRE designated Deendayal Port (Gujarat), V.O. Chidambaranar Port (Tamil Nadu), and Paradip Port (Odisha) as Green Hydrogen Hubs. Domestic vendors include Reliance, ACME, Greenko, and Ohmium.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Alkaline Water Electrolyzer (AWE)

- Proton Exchange Membrane (PEM) Electrolyzer

- Solid Oxide Electrolyzer (SOEC)

- Anion Exchange Membrane (AEM) Electrolyzer

- High-Temperature Electrolyzer

- Pressurized Electrolyzer

- Hybrid Electrolyzer Systems

- Others

By Capacity

- Below 100 kW

- 100 kW–1 MW

- 1 MW–10 MW

- 10 MW–50 MW

- 50 MW–100 MW

- Above 100 MW

- Others

By Application

- Power Generation and Energy Storage

- Industrial Feedstock Production

- Transportation and Mobility

- Ammonia Production

- Methanol Production

- Oil Refining

- Steel Manufacturing

- Chemical Processing

- Grid Balancing and Renewable Energy Integration

- Hydrogen Refueling Stations

- Power-to-Gas (P2G)

- Others

By End-User Industry

- Energy and Utilities

- Chemical Industry

- Oil and Gas

- Transportation and Mobility

- Steel and Metal Manufacturing

- Power Generation

- Mining

- Food and Beverage

- Healthcare and Pharmaceuticals

- Semiconductor and Electronics

- Government and Public Infrastructure

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.50 B |

| Forecast Revenue (2034) | USD 47.5 B |

| CAGR (2025-2034) | 30.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Alkaline Water Electrolyzer (AWE), Proton Exchange Membrane (PEM) Electrolyzer, Solid Oxide Electrolyzer (SOEC), Anion Exchange Membrane (AEM) Electrolyzer, High-Temperature Electrolyzer, Pressurized Electrolyzer, Hybrid Electrolyzer Systems, Others), By Capacity, (Below 100 kW, 100 kW–1 MW, 1 MW–10 MW, 10 MW–50 MW, 50 MW–100 MW, Above 100 MW, Others), By Application, (Power Generation and Energy Storage, Industrial Feedstock Production, Transportation and Mobility, Ammonia Production, Methanol Production, Oil Refining, Steel Manufacturing, Chemical Processing, Grid Balancing and Renewable Energy Integration, Hydrogen Refueling Stations, Power-to-Gas (P2G), Others), By End-User Industry, (Energy and Utilities, Chemical Industry, Oil and Gas, Transportation and Mobility, Steel and Metal Manufacturing, Power Generation, Mining, Food and Beverage, Healthcare and Pharmaceuticals, Semiconductor and Electronics, Government and Public Infrastructure, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THYSSENKRUPP NUCERA AG & CO. KGAA, SIEMENS ENERGY AG, NEL ASA, PLUG POWER INC., JOHN COCKERILL, CUMMINS INC. (ACCELERA), LONGI HYDROGEN, ASAHI KASEI CORPORATION, ITM POWER PLC, BLOOM ENERGY INC., AIR LIQUIDE S.A., AIR PRODUCTS AND CHEMICALS, INC., MCPHY ENERGY S.A., TOPSOE A/S, OHMIUM INTERNATIONAL, ELECTRIC HYDROGEN CO., HYSATA, SUNGROW HYDROGEN, H-TEC SYSTEMS GMBH, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Capacity (Below 100kW, 100kW-1MW, 1-10MW, 10-50MW, 50-100MW, Above 100MW), By Application (Power/Storage, Industrial Feedstock, Mobility, Ammonia, Steel, Chemical, Refueling), By End-User (Utilities, Chemical, Oil & Gas, Transport, Government) Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Capacity (Below 100kW, 100kW-1MW, 1-10MW, 10-50MW, 50-100MW, Above 100MW), By Application (Power/Storage, Industrial Feedstock, Mobility, Ammonia, Steel, Chemical, Refueling), By End-User (Utilities, Chemical, Oil & Gas, Transport, Government) Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Capacity (Below 100kW, 100kW-1MW, 1-10MW, 10-50MW, 50-100MW, Above 100MW), By Application (Power/Storage, Industrial Feedstock, Mobility, Ammonia, Steel, Chemical, Refueling), By End-User (Utilities, Chemical, Oil & Gas, Transport, Government) Region & Key Players-Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Green Hydrogen Electrolyzer Market?

The Global Green Hydrogen Electrolyzer Market was valued at USD 3.40 Billion in 2024 and USD 4.50 Billion in 2025, and is projected to reach USD 47.5 Billion by 2034, growing at a CAGR of 30.0% from 2026 to 2034. Market growth is driven by renewable energy expansion, green hydrogen production, and global decarbonization initiatives.

Who are the major players in the Green Hydrogen Electrolyzer Market?

THYSSENKRUPP NUCERA AG & CO. KGAA, SIEMENS ENERGY AG, NEL ASA, PLUG POWER INC., JOHN COCKERILL, CUMMINS INC. (ACCELERA), LONGI HYDROGEN, ASAHI KASEI CORPORATION, ITM POWER PLC, BLOOM ENERGY INC., AIR LIQUIDE S.A., AIR PRODUCTS AND CHEMICALS, INC., MCPHY ENERGY S.A., TOPSOE A/S, OHMIUM INTERNATIONAL, ELECTRIC HYDROGEN CO., HYSATA, SUNGROW HYDROGEN, H-TEC SYSTEMS GMBH, Others

Which segments covered the Green Hydrogen Electrolyzer Market?

By Technology, (Alkaline Water Electrolyzer (AWE), Proton Exchange Membrane (PEM) Electrolyzer, Solid Oxide Electrolyzer (SOEC), Anion Exchange Membrane (AEM) Electrolyzer, High-Temperature Electrolyzer, Pressurized Electrolyzer, Hybrid Electrolyzer Systems, Others), By Capacity, (Below 100 kW, 100 kW–1 MW, 1 MW–10 MW, 10 MW–50 MW, 50 MW–100 MW, Above 100 MW, Others), By Application, (Power Generation and Energy Storage, Industrial Feedstock Production, Transportation and Mobility, Ammonia Production, Methanol Production, Oil Refining, Steel Manufacturing, Chemical Processing, Grid Balancing and Renewable Energy Integration, Hydrogen Refueling Stations, Power-to-Gas (P2G), Others), By End-User Industry, (Energy and Utilities, Chemical Industry, Oil and Gas, Transportation and Mobility, Steel and Metal Manufacturing, Power Generation, Mining, Food and Beverage, Healthcare and Pharmaceuticals, Semiconductor and Electronics, Government and Public Infrastructure, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Green Hydrogen Electrolyzer Market

Published Date : 25 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date