- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Green Petroleum Coke Market Size, Share, Trends & Forecast | 5.7% CAGR

Global Green Petroleum Coke Market Size, Share, Growth Analysis By Source (Anode, Fuel), By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) Industry Regional Outlook, Supply Chain Analysis, Market Dynamics, Competitive Landscape, Production Trends, Industrial Demand Insights, Strategic Developments & Forecast 2026–2034

Report Overview

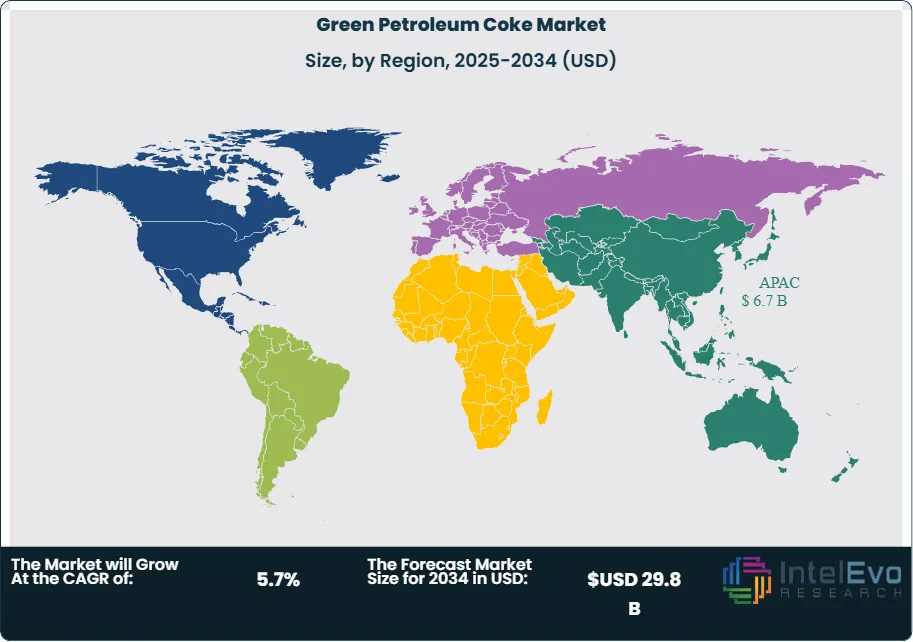

The Green Petroleum Coke Market was valued at USD 17.1 billion in 2024 and is projected to reach approximately USD 18.1 billion in 2025. The market is further expected to expand to nearly USD 29.8 billion by 2034, registering a compound annual growth rate (CAGR) of about 5.7% during the forecast period from 2026 to 2034. Growth in the market is driven by increasing demand for carbon-rich feedstock across aluminum smelting, cement manufacturing, and metallurgical industries. Green petroleum coke plays a critical role in anode production for aluminum and as a cost-efficient fuel in high-temperature industrial processes, supporting consistent consumption across heavy industrial sectors.

Get More Information about this report -

Request Free Sample ReportAdditionally, rising investments in refinery capacity expansion, infrastructure development, and industrial production in emerging economies are expected to further support market growth, while improvements in processing technologies and supply chain integration continue to strengthen global market dynamics.

Growth tracks industrial carbon demand that remains structurally tied to refinery throughput and the output of delayed coking units. Green petroleum coke stays an uncalcined, carbon-rich byproduct with variable sulfur and metals, which keeps pricing and addressable uses highly grade-dependent across fuels, anodes, graphite feedstock, and industrial heating.

Demand expands as aluminum smelting, metallurgical operations, cement kilns, and graphite producers prioritize dependable carbon inputs at scale. Aluminum-linked consumption remains a primary anchor, supported by capacity additions and modernization programs in downstream casting and smelting. Announced funding activity, including Golden Aluminum’s USD 22 million Nexcast project and a further USD 10 million Phase 1 allocation for a green aluminum smelter, signals sustained project pipelines that indirectly lift requirements for carbon-intensive consumables, including green coke used in anode and fuel value chains. On the supply side, availability follows refinery utilization, crude slate shifts, and maintenance cycles, which can tighten regional balances and widen spreads between low-sulfur and high-sulfur material.

Policy and compliance dynamics shape procurement decisions. Tighter air-emissions enforcement for SOx/NOx and particulate matter, rising carbon costs in select jurisdictions, and border-adjustment style mechanisms increase scrutiny of petcoke use in combustion-heavy applications, particularly cement and power. These pressures redirect demand toward controlled-use cases, better blending, and higher traceability, while elevating operational risk for facilities with limited abatement. Price volatility in crude, shipping constraints, and ESG-linked financing hurdles also remain material risks that can delay capacity builds or shift buyers toward substitutes such as coal blends, natural gas, or recycled carbon streams.

Asia-Pacific acts as the main volume engine, supported by industrialization and manufacturing depth, with the region sized at about USD 6.7 billion in 2024, or roughly 39% of global revenue, led by China, India, and Southeast Asia. Investment hotspots track aluminum and graphite ecosystems, including India’s planned graphite capacity additions such as HEG’s ₹3,500-crore program and Graphite India’s ₹50 crore stake for 31% in Godi, alongside recycling momentum that raises aluminum throughput and stabilizes downstream demand. Digitalization further improves market efficiency as refineries and large buyers adopt AI-driven yield optimization, predictive maintenance, and automated quality monitoring to reduce variability, improve sulfur management, and tighten contracting around consistent specifications.

, By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) Industry Regional Outlook, Supply Chain Analysis, Market Dynamics, Competitive Landscape, Production Trends, Industrial Demand Insights, Strategic Developments & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market grows from 17.1 billion USD, 2024 to 29.8 billion USD, 2034, at 5.7% CAGR, 2026-2034.

- Segment Dominance : The anode source leads demand at 75.2%, 2024.

- Segment Dominance: Spongy coke holds the largest product share at 39.5%, 2024, and aluminum remains the top end-use at 43.7%, 2024.

- Driver: Industrial anode and aluminum supply chains sustain high-volume consumption at 43.7%, 2024.

- Restraint: Quality and compliance constraints pressure higher-sulfur supply, estimated: 1.0% compliance-cost uplift, 2024.

- Opportunity: Refinery-linked availability supports incremental supply growth to 29.8 billion USD, 2034, enabling estimated: 2.0 billion USD, 2030 of new contract volume.

- Trend: Buyers tighten specification control and digitalize procurement, estimated: 15.0% adoption rate, 2027 of AI-enabled quality monitoring.

- Regional Analysis: Asia-Pacific reaches 6.7 billion USD, 2024, and sustains momentum at estimated: 5.9% CAGR, 2024-2034.

By Source

Anode-grade material continues to account for the bulk of global green petroleum coke consumption. In 2024, the anode source represented 75.2% of market volume. This concentration reflects the role of green coke as the primary carbon feedstock for anode manufacturing used in aluminum smelting and other high-temperature electrochemical and metallurgical processes. Buyers prioritize consistent carbon content and controllable impurity profiles because anode performance directly affects current efficiency, cell stability, and operating cost.

From 2025 onward, the anode segment should retain leadership as smelters pursue capacity additions, relining cycles, and incremental efficiency gains in potlines. Market expansion from 17.1 billion USD in 2024 to 29.8 billion USD by 2034, at 5.7% CAGR over 2024–2034, reinforces long-horizon demand for anode-grade supply. Producers increasingly tighten sourcing standards to manage sulfur and metals variability, which elevates the value of predictable refinery streams and robust quality control.

Fuel-grade demand remains material but more exposed to emissions compliance and switching economics. Cement kilns and industrial boilers use green coke where pricing remains favorable versus thermal coal, but tighter SOx and particulate limits raise operating cost in several jurisdictions. From 2025 onward, the fuel segment should grow unevenly by region, with stronger performance where abatement systems and permitting frameworks support continued petcoke combustion.

By Form

Spongy coke holds the leading position by form. In 2024, spongy coke accounted for 39.5% of the market. Its porous structure supports predictable reactivity and stable processing behavior, which suits blending, calcination feed, and select anode-related pathways depending on grade. Buyers also value its handling profile and the ability to achieve consistent furnace outcomes when operating conditions remain tight.

After 2025, form-based demand should increasingly track crude slate selection and refinery coking configurations. Heavier sour crudes can raise sulfur levels in output streams, which shifts relative demand toward forms and grades that end users can process within emissions and product-spec limits. This dynamic supports a widening quality spread between lower-impurity material and higher-sulfur alternatives in periods of constrained supply.

Digital quality management also gains traction across the value chain. Many refiners and industrial buyers now deploy inline analyzers and automated sampling to reduce off-spec risk. Industry interviews and procurement disclosures suggest estimated adoption of AI-assisted quality monitoring reaches 15% to 25% of large buyers by 2027, particularly in aluminum-linked supply chains where variability costs remain high.

By Application

Aluminum remains the largest application for green petroleum coke. In 2024, aluminum accounted for 43.7% of global demand. The segment relies on green coke as a core carbon input to produce anodes used in electrolytic smelting, which keeps consumption tied to operating rates, expansion plans, and anode plant throughput. Producers and smelters increasingly focus on impurity control because sulfur and metals can affect anode reactivity and net carbon consumption per ton of metal.

From 2025 onward, aluminum’s share should stay resilient as lightweighting, packaging, and electrification support steady metal demand. The market also benefits from investment activity across casting, downstream rolling, and recycling that sustains smelter utilization in key regions. While recycling reduces primary metal intensity in mature markets, it does not remove the need for primary supply, especially where construction, grid investment, and transportation demand continue to expand.

Graphite electrodes and calcined coke applications should post faster growth from a smaller base as steelmakers and battery-related value chains expand graphite capacity. Cement and power station use remains more sensitive to regulation and fuel-switching economics. In higher-compliance regions, buyers increasingly shift petcoke toward controlled industrial uses rather than broad combustion, which changes the demand mix while keeping overall market growth intact over 2024–2034.

By Region

Asia Pacific leads the market and sets the pace for volume growth. In 2024, the region held 39.30% share and reached 6.7 billion USD in market value. Large-scale refining capacity, expanding aluminum and industrial manufacturing footprints, and steady infrastructure investment sustain demand for carbon feedstocks. China and India remain the principal consumption centers, while Southeast Asia grows as refining and materials capacity expands.

North America maintains stable demand supported by mature refinery systems and established downstream consumers in aluminum, cement, and industrial heating. The region’s supply position benefits from consistent coking output, but pricing remains exposed to crude differentials and refinery utilization rates. From 2025 onward, buyers should continue to prioritize lower-impurity streams to manage compliance and operational risk.

Europe shows steady but more regulated demand. Emissions standards and carbon-cost mechanisms constrain combustion-led growth, which shifts consumption toward applications with tighter process controls and clearer compliance pathways. The Middle East and Africa should grow from a smaller base as new refining and industrial projects come online, particularly in Gulf markets with expanding downstream portfolios. Latin America contributes incremental growth linked to industrial activity and refinery operations, with demand concentrated in cement and metals value chains where cost competitiveness remains a central procurement factor.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Source

- Anode

- Fuel

By Form

- Spongy Coke

- Honeycomb Coke

- Purge Coke

- Shot Coke

- Needle Coke

By Application

- Aluminum

- Graphite Electrode

- Cement

- Power Station

- Calcined Coke

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.1 B |

| Forecast Revenue (2034) | USD 29.8 B |

| CAGR (2025-2034) | 5.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Source (Anode, Fuel), By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Aluminium Bahrain (Alba), Weifang Lianxing New Material Technology Co., Ltd., Rain Carbon Inc., Asbury Carbons, AMINCO RESOURCES LLC., Atha Group, Oxbow Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) Industry Regional Outlook, Supply Chain Analysis, Market Dynamics, Competitive Landscape, Production Trends, Industrial Demand Insights, Strategic Developments & Forecast 2026–2034")

, By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) Industry Regional Outlook, Supply Chain Analysis, Market Dynamics, Competitive Landscape, Production Trends, Industrial Demand Insights, Strategic Developments & Forecast 2026–2034")

, By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others) Industry Regional Outlook, Supply Chain Analysis, Market Dynamics, Competitive Landscape, Production Trends, Industrial Demand Insights, Strategic Developments & Forecast 2026–2034")

Frequently Asked Questions

How big is the Green Petroleum Coke Market?

Global Green Petroleum Coke Market was valued at USD 17.1 billion in 2024 and is projected to reach USD 29.8 billion by 2034, growing at a CAGR of 5.7%. Explore key trends, drivers, industrial demand, and market opportunities.

Who are the major players in the Green Petroleum Coke Market?

Aluminium Bahrain (Alba), Weifang Lianxing New Material Technology Co., Ltd., Rain Carbon Inc., Asbury Carbons, AMINCO RESOURCES LLC., Atha Group, Oxbow Corporation

Which segments covered the Green Petroleum Coke Market?

By Source (Anode, Fuel), By Form (Spongy Coke, Honeycomb Coke, Purge Coke, Shot Coke, Needle Coke), By Application (Aluminum, Graphite Electrode, Cement, Power Station, Calcined Coke, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date