- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Grid-Scale Energy Storage Market Size, Share | CAGR 12.5%

Global Grid-Scale Energy Storage Market Size, Share, Analysis By Technology (Battery Energy Storage Systems - BESS, Pumped Hydro, Thermal), By Duration (Short, Medium, Long-Duration), By Application (Renewable Integration, Grid Stabilization, Peak Shaving), By End-User (Utilities, IPPs, Commercial & Industrial) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Renewable Energy Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

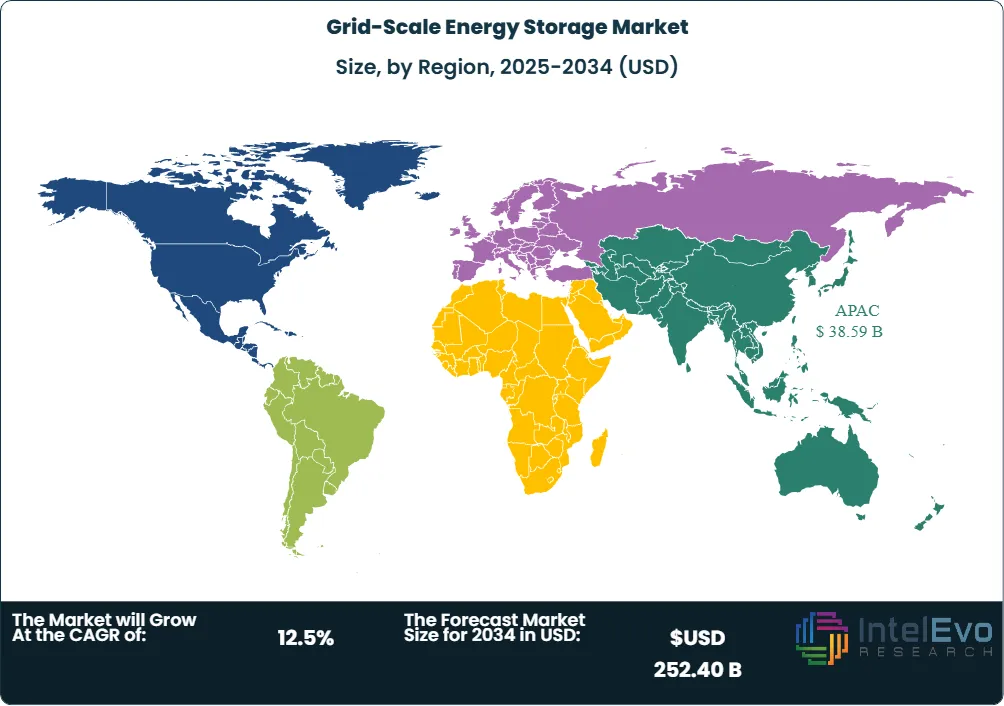

| USD 87.30 Billion | USD 252.40 Billion | 12.5% | Asia Pacific, 44.2% |

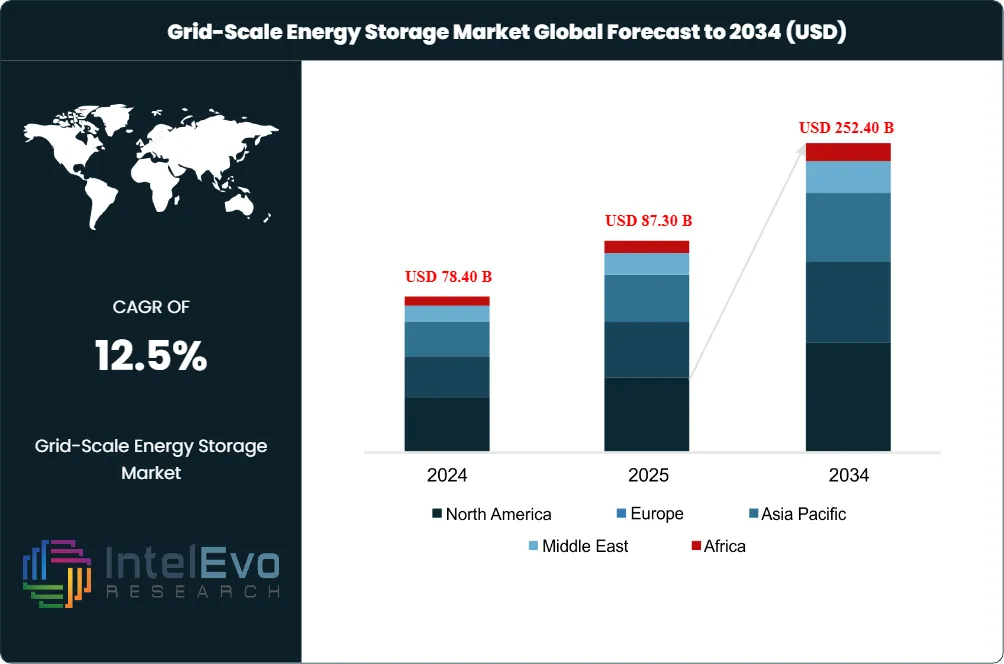

The Grid-Scale Energy Storage Market was valued at USD 78.40 Billion in 2024 and USD 87.30 Billion in 2025. The market is projected to reach USD 252.40 Billion by 2034, expanding at a CAGR of 12.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 165.10 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportDemand is anchored by the shift from renewable-energy buildout to firm, dispatchable power capacity across China, the United States, Germany, India, and Australia. The International Energy Agency recorded 108 GW of new battery storage capacity in 2025, 40% above 2024, while China commissioned 66.4 GW and 189.5 GWh of new-type storage during the year.

The grid-scale energy storage market expanded because solar and wind fleets now create midday surplus, evening ramps, and curtailment risk that cannot be solved by generation alone. In the United States, the Energy Information Administration reported 15 GW of utility-scale battery storage additions in 2025 and expects developers to add 24 GW in 2026, creating procurement pull for Tesla Megapack, CATL EnerOne, Sungrow PowerTitan, Fluence Gridstack, and BYD MC Cube systems.

Regulation is moving from market-access approval toward safety, interconnection, and domestic-content screening. FERC Order 841 and Order 2222 support wholesale participation for storage resources, while NFPA 855, UL 9540A, the 2024 International Fire Code, and the proposed NFPA 800 battery safety code shape siting and approval of lithium-ion projects after the January 2025 Moss Landing incident in California.

Technology competition is centered on lithium iron phosphate, sodium-ion batteries, flow batteries, pumped-storage hydropower, compressed-air energy storage, and thermal storage. Lithium iron phosphate supplied roughly 90% of 2025 battery storage deployments because cycle life, safety profile, and lower cobalt exposure matched grid duty cycles better than high-nickel automotive chemistries.

Asia Pacific held the largest 44.2% share of the grid-scale energy storage market in 2025 because China’s new-type storage capacity exceeded 144 GW by year-end and India moved from tenders toward scaled construction. North America followed with 31.0% share, supported by U.S. storage installations of 18.9 GW across utility, commercial, and residential systems in 2025 and a six-year projection of 500 GWh between 2026 and 2031.

Through 2034, market value will move from equipment procurement toward integrated revenue assurance, including trading software, augmentation contracts, warranty reserves, and capacity-market participation. This shift favors suppliers that pair hardware scale with bankable performance guarantees, including CATL, Tesla, Sungrow, Fluence, Wärtsilä, BYD, LG Energy Solution, Samsung SDI, HyperStrong, and Energy Vault.

Market Definition & Scope

The grid-scale energy storage market is defined as the global commercial activity surrounding stationary storage assets connected to transmission or distribution networks for bulk power shifting, frequency regulation, capacity support, congestion relief, black-start service, and renewable-energy integration. The market encompasses lithium-ion battery energy storage systems, sodium-ion systems, flow batteries, pumped-storage hydropower, compressed-air energy storage, thermal storage, power conversion systems, controls software, balance-of-plant engineering, and long-term maintenance services.

This analysis includes utility-owned assets, independent power producer projects, grid-operator procurements, merchant storage plants, co-located solar-plus-storage systems, and data-center-linked grid storage above commercial building scale. It excludes residential batteries, electric-vehicle traction packs, small uninterruptible power supplies, portable power stations, and behind-the-meter industrial systems that do not provide grid services. The grid-scale energy storage market sits within the parent power infrastructure and grid flexibility market, where batteries, pumped hydro, demand response, and transmission upgrades compete for capacity value.

, By Duration (Short, Medium, Long-Duration), By Application (Renewable Integration, Grid Stabilization, Peak Shaving), By End-User (Utilities, IPPs, Commercial & Industrial) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Renewable Energy Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The grid-scale energy storage market expanded from USD 87.30 Billion in 2025 to a projected USD 252.40 Billion by 2034 at a 12.5% CAGR, creating USD 165.10 Billion in absolute dollar opportunity.

- Segment Dominance: Lithium-ion battery energy storage led by technology with 71.8% share in 2025, equal to USD 62.68 Billion, because LFP chemistry dominated short-duration grid deployments.

- Segment Dominance: Renewable integration led by application with 44.6% share in 2025, equal to USD 38.94 Billion, because solar and wind curtailment created dispatch requirements in China, the United States, and Europe.

- Driver: Global battery storage additions reached 108 GW in 2025, and China alone commissioned 189.5 GWh of new-type storage, lifting demand for cells, inverters, transformers, and energy management software.

- Restraint: Safety and siting friction increased after the January 2025 Moss Landing fire, making UL 9540A testing, NFPA 855 compliance, emergency response plans, and community acceptance material project-gating items.

- Opportunity: The 2026-2031 U.S. installation outlook of 500 GWh creates a procurement opportunity above USD 55 Billion at current turnkey cost bands, before software, augmentation, and trading margins.

- Trend: Sodium-ion commercialization accelerated in April 2026 when CATL agreed to deliver 60 GWh of sodium-ion batteries to Beijing HyperStrong Technology over three years.

- Regional: Asia Pacific led with 44.2% share and USD 38.59 Billion in 2025 revenue, supported by China’s 144.7 GW cumulative new-type energy storage base and India’s 102 GWh tender activity.

Key Insights Summary

- Global battery storage capacity additions reached 108 GW in 2025, 40% above 2024, making battery storage the fastest-growing power technology tracked in that year.

- China commissioned 66.4 GW and 189.5 GWh of new-type energy storage in 2025, taking its cumulative new-type storage base to 144.7 GW by year-end.

- The United States installed 18.9 GW of battery energy storage systems in 2025 across utility, commercial, and residential segments, 52% above 2024, with Q4 alone adding 5.8 GW.

- U.S. developers plan to add 24 GW of utility-scale battery storage in 2026 after adding a record 15 GW in 2025, according to federal generator interconnection data.

- The European Union installed 27.1 GWh of new battery capacity in 2025, its 12th consecutive record year for storage deployment, with utility-scale systems becoming the demand center.

- CATL reported 661 GWh of lithium battery sales in 2025 and a 30.4% share of global energy-storage battery shipments, while its energy-storage integration shipments grew by more than 160% year on year.

- NREL’s 2025 utility-scale battery storage cost projection places four-hour lithium-ion systems at USD 147-339 per kWh in 2035, showing why battery project economics remain sensitive to cell cost, duration, and interconnection upgrades.

Competitive Landscape Overview

The grid-scale energy storage market is moderately consolidated by cell supply and fragmented by project development, installation, and operation. CATL, Tesla, Sungrow, and Fluence form the top supplier group, with disclosed 2025 shipment or revenue indicators above USD 20 Billion when Tesla Energy, Sungrow energy storage systems, CATL storage cells, and Fluence storage solutions are combined.

Competition is not only based on module cost. The highest-value bids combine LFP cell access, power conversion systems, augmentation terms, safety certifications, liquid-cooling design, trading software, and warranties that satisfy lenders in ERCOT, CAISO, PJM, NEM, Germany, and Italy.

The competitive field is shifting because Chinese suppliers dominate cell cost curves while U.S. and European project owners want tariff resilience, cybersecurity assurance, and bankable service support. Tesla, Fluence, Wärtsilä, and Energy Vault benefit when procurement teams price local execution risk, while CATL, BYD, Sungrow, EVE Energy, and HyperStrong gain when buyers prioritize cost per kWh and delivery speed.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| CATL | China | Leader | EnerOne, EnerC, Tener, sodium-ion cells | China, Europe, Middle East | Entered a 60 GWh sodium-ion battery supply arrangement with Beijing HyperStrong in April 2026 |

| Tesla, Inc. | United States | Leader | Megapack, Autobidder, Powerhub | North America, Europe, Australia | Reported 2025 energy generation and storage revenue of USD 12.77 Billion |

| Sungrow Power Supply | China | Leader | PowerTitan, PowerStack, PCS platforms | China, Europe, Americas, MEA | Shipped 43 GWh of energy storage systems in 2025, up 53.5% year on year |

| Fluence Energy | United States | Leader | Gridstack, Sunstack, Ultrastack, Fluence IQ | Americas, Europe, Asia Pacific | Reported fiscal 2025 revenue of USD 2.3 Billion and improved gross margin |

| BYD Company | China | Challenger | MC Cube, Blade Battery storage systems | China, Europe, Latin America | Expanded utility-scale LFP storage deployments across Asia Pacific and export markets |

| Wärtsilä Energy | Finland | Challenger | GridSolv Quantum, GEMS Digital Energy Platform | Europe, Americas, Australia | Continued GEMS-based project delivery for utility storage and hybrid power plants |

| Beijing HyperStrong Technology | China | Challenger | HyperBlock, storage system integration | China, Asia Pacific | Secured 60 GWh sodium-ion battery supply from CATL for 2026-2029 |

| LG Energy Solution | South Korea | Challenger | Grid-scale ESS cells and racks | North America, Europe, Asia | Shifted more manufacturing capacity toward LFP and stationary storage demand |

| Samsung SDI | South Korea | Niche Player | ESS cells, battery modules | Korea, Europe, North America | Pursued safer ESS chemistries and high-reliability modules for grid customers |

| Energy Vault | United States | Niche Player | B-VAULT, gravity storage, hydrogen storage | United States, Europe, Australia | Acquired the 175 MW/350 MWh McMurtre BESS project in ERCOT North in March 2026 |

Segmentation Analysis

The grid-scale energy storage market segments by technology, duration, application, and end-user, with value shifting from battery racks toward software, augmentation, and grid-service revenue optimization.

By Technology

The grid-scale energy storage market by technology is led by lithium-ion battery energy storage systems, which held 71.8% share in 2025 and generated USD 62.68 Billion in revenue. LFP chemistry dominates this segment because it avoids nickel and cobalt exposure, handles frequent cycling, and now represents roughly 90% of battery storage deployments. CATL, BYD, Tesla, Sungrow, Fluence, EVE Energy, and LG Energy Solution compete in this category through containerized systems, cell supply, or integrated engineering packages.

Pumped-storage hydropower captured 13.6% share in 2025, equal to USD 11.87 Billion, but its role is larger in stored-energy capacity than annual equipment revenue. China, India, Japan, the United States, and Europe continue to use pumped hydro for long-duration flexibility because reservoirs can deliver multi-hour and multi-day support that four-hour batteries cannot match at seasonal scale. Reuters reported nearly 200 GW of pumped storage in operation globally and about 570 GW under development, with China leading the pipeline.

Flow batteries, compressed-air systems, thermal storage, sodium-ion batteries, and hydrogen-linked storage accounted for the remaining 14.6% share in 2025, equivalent to USD 12.75 Billion. This group is commercially smaller than lithium-ion but more relevant for eight-hour and multi-day services. Form Energy, Hydrostor, ESS Tech, Invinity Energy Systems, Energy Vault, Sumitomo Electric, and Highview Power target durations where LFP augmentation costs rise and capacity-market value becomes more important than daily arbitrage.

By Duration

The grid-scale energy storage market by duration is led by systems below four hours, which held 45.0% share in 2025, or USD 39.29 Billion. Two-hour projects remain common in ERCOT, CAISO, Australia’s National Electricity Market, and parts of Europe because they monetize frequency response, reserve capacity, and solar ramp support with lower upfront capital. Tesla Megapack, Fluence Gridstack, Sungrow PowerTitan, and BYD MC Cube have high-volume configurations in this range.

Four-to-eight-hour systems captured 37.0% share in 2025, or USD 32.30 Billion, and represent the fastest commercial migration path through 2034. Utilities now request four-hour or longer systems because renewable penetration creates evening capacity needs rather than only ancillary services. U.S. procurement in California, Arizona, Nevada, and Texas, plus India’s solar-plus-storage tenders and Italy’s MACSE mechanism, push suppliers toward higher energy-to-power ratios and stricter degradation guarantees.

Eight-hour-plus systems represented 18.0% share in 2025, equal to USD 15.71 Billion, with pumped hydro, compressed air, iron-air batteries, thermal storage, and flow batteries carrying most activity. Long-duration installations surpassed 15 GWh in 2025, but venture funding declined sharply outside government-backed programs, which indicates that policy revenue certainty remains the deciding factor. Hydrostor, Form Energy, Energy Dome, Highview Power, and Invinity need capacity contracts, resilience credits, or industrial heat offtake to reach bankable scale.

By Application

The grid-scale energy storage market by application is led by renewable integration, which held 44.6% share in 2025 and generated USD 38.94 Billion. Solar curtailment in China, California, Germany, Spain, Australia, and India increases the value of midday charging and evening dispatch. Co-located solar-plus-storage assets also reduce interconnection costs because the inverter, transformer, substation, and grid queue position can be shared across generation and storage.

Peak capacity and resource adequacy accounted for 22.8% share in 2025, or USD 19.90 Billion. This segment grows when grid operators procure storage as a capacity resource rather than a merchant arbitrage tool. CAISO resource adequacy rules, ERCOT scarcity pricing, PJM capacity auctions, and National Electricity Market reforms create revenue stacks that allow developers to secure project finance with lower merchant exposure.

Ancillary services held 15.7% share in 2025, equal to USD 13.71 Billion, while transmission and distribution deferral held 10.1% share, or USD 8.82 Billion. Frequency regulation, spinning reserve, voltage support, and black-start services provide early revenue but saturate as battery penetration rises. Data-center-linked capacity and grid-connected microgrids represented 6.8% share, or USD 5.94 Billion, driven by AI load growth in Northern Virginia, Texas, Arizona, Dublin, Singapore, and Sydney.

By End-User

The grid-scale energy storage market by end-user is led by utilities and independent power producers, which held 61.5% share in 2025, equal to USD 53.69 Billion. NextEra Energy, AES Corporation, RWE, Enel Green Power, EDF Renewables, Iberdrola, and Neoen use storage to firm renewables, reduce imbalance charges, and bid into capacity markets. Procurement teams in this group favor warranties, insurance acceptance, liquid-cooling reliability, and proven interconnection execution over headline battery price alone.

Transmission and distribution operators held 18.4% share in 2025, or USD 16.06 Billion, because grid bottlenecks create demand for non-wires alternatives. Storage reduces transformer loading, absorbs local renewable peaks, and supports fast frequency response when new transmission is delayed. National Grid, TenneT, Terna, AEMO, CAISO, and state-level U.S. utilities use storage as a grid asset when regulatory recovery frameworks permit rate-base treatment.

Commercial aggregators, data-center operators, and public-sector buyers represented 20.1% share in 2025, or USD 17.55 Billion. Microsoft, Google, Amazon Web Services, Crusoe, and xAI increase demand for firm power around AI campuses, while military bases and municipal utilities use storage for resilience. This segment differs from utility procurement because buyers often value uptime, interconnection speed, and carbon-accounting claims more than pure arbitrage economics.

Regional Analysis

The grid-scale energy storage market in Asia Pacific held 44.2% share in 2025, equivalent to USD 38.59 Billion. China accounts for most regional value, with 66.4 GW and 189.5 GWh of new-type storage commissioned in 2025 and a cumulative new-type base of 144.7 GW. India is moving quickly from tendering to construction, with 102 GWh of energy storage tenders issued in 2025 and Maharashtra approving a 16,000 MWh BESS plan under the MAGESTIC program. Australia adds upside because AEMO’s 2026 power-market data show battery storage more than doubled its energy shifting, reducing peak-price stress during heat and data-center load growth.

North America accounted for 31.0% of the grid-scale energy storage market in 2025, valued at USD 27.06 Billion. The United States dominates regional demand, supported by 18.9 GW of 2025 storage installations and federal generator data showing 24 GW of planned utility-scale battery additions in 2026. Texas, California, Arizona, Nevada, and New York account for much of the operating fleet because they combine high solar penetration, power price volatility, and capacity needs. Canada adds pumped hydro, Ontario capacity procurements, and Alberta merchant projects, while Mexico remains constrained by grid policy and utility procurement uncertainty.

Europe represented 18.1% of the grid-scale energy storage market in 2025, equal to USD 15.80 Billion. The European Union installed 27.1 GWh of new battery capacity in 2025, with Germany, Italy, Spain, the Netherlands, and Poland moving toward larger front-of-meter projects. Italy’s MACSE mechanism, the United Kingdom’s cap-and-floor design for long-duration storage, and EU battery regulations create clearer revenue pathways but also raise compliance costs. European buyers often pay higher turnkey prices than China because grid codes, fire engineering, land costs, and local content expectations remain tougher.

Latin America held 3.6% of the grid-scale energy storage market in 2025, or USD 3.14 Billion. Chile leads deployment because solar curtailment in the Atacama region creates high value for evening dispatch. Brazil, Mexico, Colombia, and Peru are still earlier in adoption, with auction design and transmission planning more important than battery hardware availability. The region’s procurement checklist focuses on dollar-linked contracts, import duties, altitude performance, and lender acceptance for Chinese BESS suppliers.

Middle East and Africa accounted for 3.1% of the grid-scale energy storage market in 2025, equal to USD 2.71 Billion. Saudi Arabia, the United Arab Emirates, South Africa, Morocco, and Egypt lead demand because large solar parks and grid resilience programs create storage requirements. Gulf buyers favor utility-scale tender packages linked to solar independent power producers, while South Africa uses storage to reduce load-shedding exposure and support Eskom grid stability. Financing remains the main constraint in sub-Saharan Africa because sovereign risk and currency exposure raise project capital costs.

Country Analysis

The United States grid-scale energy storage market reached USD 25.10 Billion in 2025 and is projected to grow at an 11.8% CAGR through 2034. The market is driven by ERCOT volatility, CAISO resource adequacy, federal investment tax credits, and data-center load growth in Texas, Virginia, Arizona, and Nevada. The Energy Information Administration expects 24 GW of utility-scale battery storage additions in 2026, following 15 GW in 2025. Safety review became stricter after the Moss Landing incident, making NFPA 855, UL 9540A, local fire marshal approval, and emergency response planning central to project timelines.

China’s grid-scale energy storage market reached USD 31.60 Billion in 2025 and is projected to grow at an 12.1% CAGR through 2034. China commissioned 66.4 GW and 189.5 GWh of new-type storage in 2025, supported by provincial renewable pairing mandates, LFP overcapacity, and grid flexibility requirements. CATL, BYD, Sungrow, HyperStrong, EVE Energy, Gotion High-Tech, and CRRC Zhuzhou Institute form the domestic supply base. The April 2026 CATL-HyperStrong 60 GWh sodium-ion arrangement shows China’s ability to move alternative chemistries from pilot scale to power-sector deployment faster than Europe or North America.

Germany’s grid-scale energy storage market reached USD 4.20 Billion in 2025 and is forecast to grow at a 10.6% CAGR through 2034. Germany led EU battery additions in 2025 with 6.6 GWh and remains central to Europe’s storage demand because solar penetration, coal exit planning, and industrial power costs create flexibility value. RWE commissioned one of Germany’s large battery projects at Hamm and Neurath in 2025, while grid operators TenneT, Amprion, 50Hertz, and TransnetBW continue to address congestion. German procurement favors bankable suppliers with cybersecurity assurance, European service teams, and compliance with EU battery rules.

India’s grid-scale energy storage market reached USD 3.00 Billion in 2025 and is projected to grow at an 18.5% CAGR through 2034. India issued 69 storage tenders totaling 102 GWh in 2025, while the Central Electricity Authority projects storage requirements above 300 GWh by 2029-30. Solar Energy Corporation of India, NTPC, JSW Energy, Reliance Industries, Tata Power, and state distribution companies are moving procurement from pilot lots to multi-GWh contracts. Maharashtra’s April 2026 MAGESTIC approval for 16,000 MWh of BESS capacity adds a state-level model that links transmission upgrades, World Bank financing, and renewable-energy targets.

Australia’s grid-scale energy storage market reached USD 2.40 Billion in 2025 and is projected to grow at a 15.4% CAGR through 2034. The National Electricity Market rewards batteries through arbitrage, frequency control ancillary services, capacity firming, and network support. AEMO’s early 2026 data showed large-scale battery energy shifting more than doubled, helping reduce evening peak pressure during heat and data-center demand growth. Neoen, AGL Energy, Origin Energy, Akaysha Energy, Energy Vault, Tesla, Fluence, and Wärtsilä remain visible suppliers and asset owners.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Battery Energy Storage Systems (BESS)

- Pumped Hydro Storage

- Thermal Energy Storage

- Others

By Duration

- Short-Duration Storage

- Medium-Duration Storage

- Long-Duration Storage

- Others

By Application

- Renewable Energy Integration

- Grid Stabilization

- Peak Shaving & Load Management

- Others

By End-User

- Utilities

- Independent Power Producers (IPPs)

- Commercial & Industrial

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 87.30 B |

| Forecast Revenue (2034) | USD 252.40 B |

| CAGR (2025-2034) | 12.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Battery Energy Storage Systems (BESS), Pumped Hydro Storage, Thermal Energy Storage, Others), By Duration, (Short-Duration Storage, Medium-Duration Storage, Long-Duration Storage, Others), By Application, (Renewable Energy Integration, Grid Stabilization, Peak Shaving & Load Management, Others), By End-User, (Utilities, Independent Power Producers (IPPs), Commercial & Industrial, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED (CATL), TESLA, INC., SUNGROW POWER SUPPLY CO., LTD., FLUENCE ENERGY, INC., BYD COMPANY LIMITED, WÄRTSILÄ CORPORATION, BEIJING HYPERSTRONG TECHNOLOGY CO., LTD., LG ENERGY SOLUTION, LTD., SAMSUNG SDI CO., LTD., EVE ENERGY CO., LTD., GOTION HIGH-TECH CO., LTD., ENERGY VAULT HOLDINGS, INC., FORM ENERGY, INC., HYDROSTOR INC., ESS TECH, INC., INVINITY ENERGY SYSTEMS PLC, HIGHVIEW POWER LIMITED, POWIN LLC, CRRC ZHUZHOU INSTITUTE CO., LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Duration (Short, Medium, Long-Duration), By Application (Renewable Integration, Grid Stabilization, Peak Shaving), By End-User (Utilities, IPPs, Commercial & Industrial) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Renewable Energy Tech Trends & Forecast 2026-2034")

, By Duration (Short, Medium, Long-Duration), By Application (Renewable Integration, Grid Stabilization, Peak Shaving), By End-User (Utilities, IPPs, Commercial & Industrial) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Renewable Energy Tech Trends & Forecast 2026-2034")

, By Duration (Short, Medium, Long-Duration), By Application (Renewable Integration, Grid Stabilization, Peak Shaving), By End-User (Utilities, IPPs, Commercial & Industrial) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Renewable Energy Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Grid-Scale Energy Storage Market?

The Global Grid-Scale Energy Storage Market was valued at USD 78.40 Billion in 2024 and USD 87.30 Billion in 2025, and is projected to reach USD 252.40 Billion by 2034, growing at a CAGR of 12.5% from 2026 to 2034. Market growth is driven by battery energy storage systems, renewable energy integration, and smart grid technologies.

Who are the major players in the Grid-Scale Energy Storage Market?

CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED (CATL), TESLA, INC., SUNGROW POWER SUPPLY CO., LTD., FLUENCE ENERGY, INC., BYD COMPANY LIMITED, WÄRTSILÄ CORPORATION, BEIJING HYPERSTRONG TECHNOLOGY CO., LTD., LG ENERGY SOLUTION, LTD., SAMSUNG SDI CO., LTD., EVE ENERGY CO., LTD., GOTION HIGH-TECH CO., LTD., ENERGY VAULT HOLDINGS, INC., FORM ENERGY, INC., HYDROSTOR INC., ESS TECH, INC., INVINITY ENERGY SYSTEMS PLC, HIGHVIEW POWER LIMITED, POWIN LLC, CRRC ZHUZHOU INSTITUTE CO., LTD., Others

Which segments covered the Grid-Scale Energy Storage Market?

By Technology, (Battery Energy Storage Systems (BESS), Pumped Hydro Storage, Thermal Energy Storage, Others), By Duration, (Short-Duration Storage, Medium-Duration Storage, Long-Duration Storage, Others), By Application, (Renewable Energy Integration, Grid Stabilization, Peak Shaving & Load Management, Others), By End-User, (Utilities, Independent Power Producers (IPPs), Commercial & Industrial, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Grid-Scale Energy Storage Market

Published Date : 06 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date