- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Health Data Marketplace Market Size, Share | CAGR 18.6%

Global Health Data Marketplace Market Size, Share, Growth Analysis By Data Type (Clinical & EHR Data, Claims Data, Genomic & Multi-Omic Data, Wearable Device Data, Social Determinants of Health Data), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Pharma, Healthcare Providers, Payers, Government Agencies), By Data Modality, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 3.18 Billion | USD 14.76 Billion | 18.6% | North America, 42.1% |

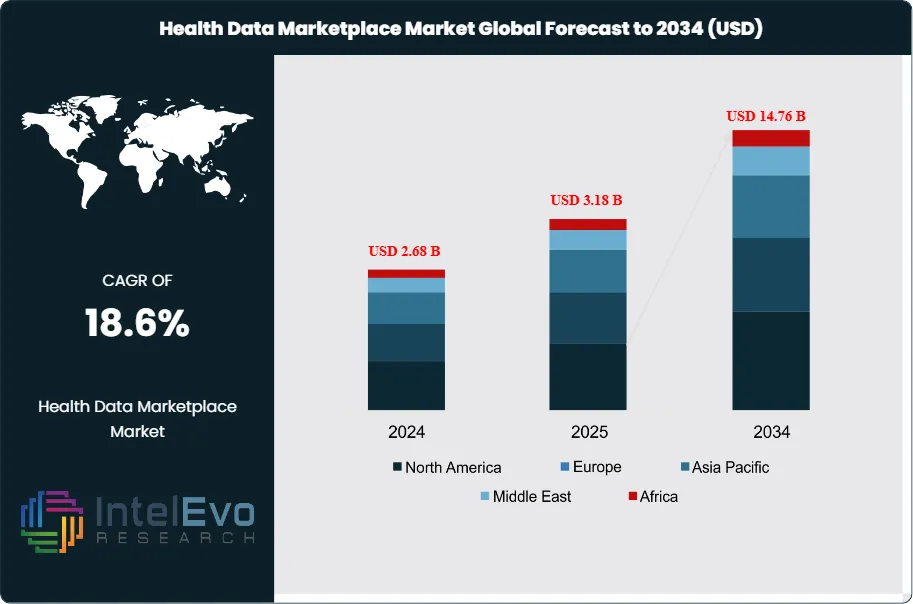

The Health Data Marketplace Market was valued at approximately USD 2.68 Billion in 2024 and reached USD 3.18 Billion in 2025. The market is projected to grow to USD 14.76 Billion by 2034, expanding at a CAGR of 18.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.58 Billion over the analysis period, driven by the intersection of accelerating healthcare digitization, rising demand for real-world evidence in drug development, and the expansion of privacy-preserving data technologies that enable compliant commercial exchange of sensitive patient information.

Get More Information about this report -

Request Free Sample ReportHealth data marketplaces are structured digital platforms that facilitate the discovery, licensing, and exchange of health-related datasets among data generators, including hospital systems, payers, pharmacy benefit managers, wearable device manufacturers, and genomics laboratories, and data consumers, including pharmaceutical companies, medical device developers, health insurers, government agencies, and academic researchers. The data assets transacted on these platforms span electronic health records, claims and administrative data, genomic and proteomic datasets, real-world evidence datasets, medical imaging libraries, patient-generated wearable data, and social determinants of health information. The convergence of these data types creates a composite view of patient health trajectories that has proven material value for clinical trial design, drug target identification, health technology assessment, and population health management.

Regulatory frameworks are both a driver and a shaper of the health data marketplace market. The 21st Century Cures Act in the United States mandated interoperability and data sharing standards across certified electronic health record systems, generating a structured data supply that health data marketplace operators have organized into commercial offerings. The Office of the National Coordinator for Health Information Technology’s implementation of Fast Healthcare Interoperability Resources (FHIR) application programming interfaces has reduced the technical friction of data extraction and standardization that previously limited marketplace scalability. In Europe, the European Health Data Space regulation, advancing through legislative process as of 2025, is expected to create a continental framework for secondary use of health data that will substantially expand the legally accessible data supply for marketplace transactions.

Artificial intelligence and machine learning integration is reshaping the health data marketplace market from a simple data brokerage model to a platform with embedded analytical intelligence. Leading marketplace operators now offer not only raw data access but also pre-trained predictive models, federated learning environments where algorithms train on distributed datasets without centralizing patient records, and synthetic data generation services that provide statistically representative datasets free of re-identification risk. These value-added capabilities command premium pricing and are attracting enterprise software and cloud infrastructure companies into the competitive set alongside traditional health information organizations.

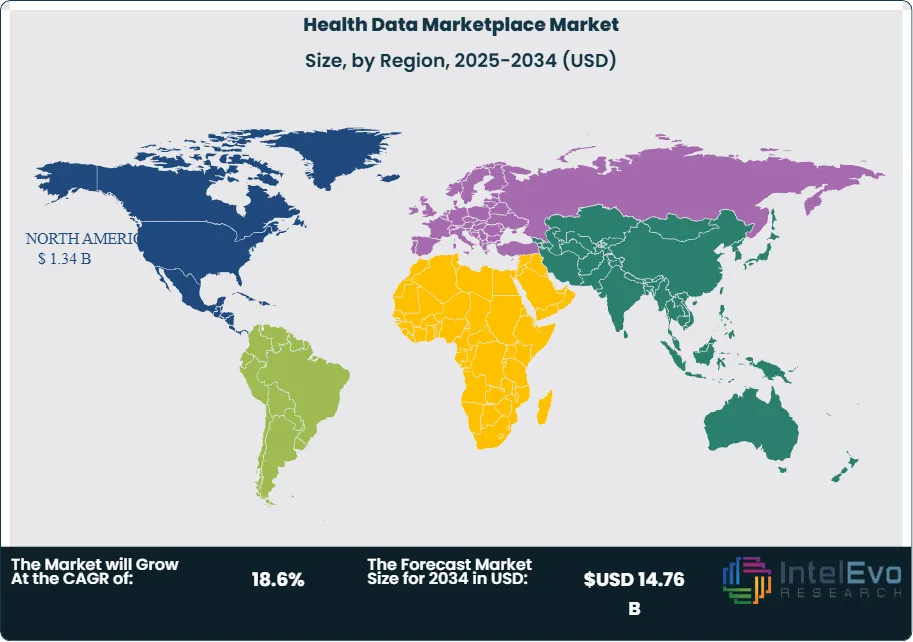

North America leads the health data marketplace market with a 42.1% share in 2025 at USD 1.34 Billion, anchored by the United States’ advanced healthcare data infrastructure, established HIPAA de-identification frameworks, and the concentrated demand from pharmaceutical R&D centers in Boston, New Jersey, and San Francisco. Asia Pacific is the fastest-growing regional market, propelled by China’s national health data governance initiatives, India’s expanding digital health infrastructure under the Ayushman Bharat Digital Mission, and Japan’s Medical Information Database infrastructure. Europe holds 26.8% of global market share, with Germany, the United Kingdom, and the Nordic countries leading data infrastructure development and regulatory framework creation.

, By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Pharma, Healthcare Providers, Payers, Government Agencies), By Data Modality, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global health data marketplace market was valued at USD 3.18 Billion in 2025 and is forecast to reach USD 14.76 Billion by 2034, expanding at a CAGR of 18.6% over the 2026–2034 forecast period.

- Segment Dominance: By data type, clinical and electronic health record data holds the largest share at 38.4% of the health data marketplace market in 2025, reflecting the depth and breadth of longitudinal patient information captured in hospital and physician practice record systems.

- Segment Dominance: By end-user, pharmaceutical and life sciences companies represent the dominant buyer segment at 44.7% of market revenue in 2025, driven by demand for real-world evidence to support drug development, regulatory submissions, and post-market surveillance obligations.

- Driver: The 21st Century Cures Act FHIR mandate and the expansion of electronic health record interoperability have increased the volume of structurally standardized health data available for secondary use by an estimated 340% between 2021 and 2025, directly expanding the data supply that health data marketplace operators can license and monetize.

- Restraint: Patient data privacy concerns and inconsistent cross-jurisdictional regulatory frameworks create compliance complexity that limits the geographic scope of marketplace transactions, with data localization requirements in the EU, China, and India each imposing distinct constraints on cross-border data flows that fragment what might otherwise be a unified global marketplace.

- Opportunity: The integration of genomic and multi-omic datasets with clinical records on health data marketplace platforms represents an addressable market exceeding USD 2.8 Billion by 2034, as pharmaceutical companies accelerate precision medicine pipelines that require linked genomic-phenotypic data to identify biomarker-stratified patient populations.

- Trend: Federated learning and privacy-enhancing computation technologies are enabling health data marketplace transactions where analytical value is extracted from patient data without the data leaving the originating institution, with adoption of these privacy-preserving architectures growing at an estimated 47% annually in 2025 across major marketplace platforms.

- Regional Analysis: North America leads the global health data marketplace market with a 42.1% share in 2025, representing USD 1.34 Billion, supported by mature HIPAA-compliant de-identification frameworks and concentrated pharmaceutical R&D demand for real-world evidence datasets.

Competitive Landscape Overview

The health data marketplace market exhibits moderate fragmentation in 2025, with the top four platforms collectively accounting for approximately 49% of global revenue. The competitive environment features three distinct player archetypes: established health information organizations that are digitizing and commercializing existing data assets, technology and cloud platform operators building marketplace infrastructure as an extension of healthcare IT offerings, and pure-play health data marketplace companies built around specific data modalities or buyer verticals. Competition centers on data breadth and longitudinal depth, de-identification and privacy compliance credibility, analytical value-added services, data linkage capabilities across sources, and API integration flexibility. Strategic acquisitions of specialty health data companies and electronic health record networks by marketplace operators accelerated significantly in 2024 and 2025, as scale of data supply increasingly determines marketplace pricing power and buyer retention.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| IQVIA | USA | Leader | IQVIA Real-World Data Platform | North America, Europe | Acquired a genomics data network in 2024 to link clinical records with multi-omic profiles; expanded federated analytics offering to 18 additional health systems in 2025. |

| Optum (UnitedHealth) | USA | Leader | Optum Health Data Marketplace | North America | Integrated Optum’s 340 Million patient claims database with linked EHR records in 2025; launched enterprise API access tier for pharma R&D teams. |

| IBM Watson Health (Merative) | USA | Challenger | Merative MarketScan | North America, Europe | Rebranded from IBM Watson Health to Merative in 2022; expanded MarketScan claims database with social determinants of health linkage layer completed in 2025. |

| Veeva Systems | USA | Challenger | Veeva Data Cloud | North America, Europe, APAC | Launched Veeva Data Cloud with integrated real-world evidence and clinical trial data linkage in 2024; expanded Asia Pacific data partnerships in Japan and South Korea. |

| Amazon Web Services (AWS Health) | USA | Challenger | AWS HealthLake Marketplace | North America, Europe, APAC | Launched HealthLake Marketplace data exchange capabilities in 2025; signed data supply agreements with five major U.S. health systems to populate the platform. |

| Datavant | USA | Niche Player | Datavant Health Data Ecosystem | North America | Completed a token-based patient matching network linking 500 Million patient records across 70,000 sites in 2025; raised USD 400 Million Series C in 2024. |

| Komodo Health | USA | Niche Player | Komodo Healthcare Map | North America | Launched AI-driven patient journey analytics layer on top of its 330 Million patient record map in 2025; expanded into payer analytics vertical. |

| FINN.ai / Inovalon | USA | Niche Player | Inovalon Data Platform | North America | Expanded Inovalon’s real-world data platform with prospective patient registry capabilities in 2025 following its take-private acquisition; added oncology-specific data modules. |

By Data Type

The health data marketplace market by data type is led by clinical and electronic health record data, which captured 38.4% of global revenue in 2025 at approximately USD 1.22 Billion. Clinical EHR data encompasses longitudinal patient records including diagnosis codes, medication histories, laboratory results, clinical notes, and procedure records extracted from certified EHR systems across hospital and ambulatory care settings. The structured, standardized nature of FHIR-compliant EHR data makes it the foundational asset class on which health data marketplace operators build their product offerings. Pharmaceutical companies are the primary buyers, using clinical data for safety signal detection, treatment pathway analysis, and real-world comparative effectiveness research. Claims and administrative data represents the second-largest data type segment at 26.7% of the market in 2025 at USD 849 Million. Claims data, generated by insurance payers and pharmacy benefit managers, provides comprehensive records of diagnoses, treatments, and medication fills across populations, with near-universal coverage within insured populations. Its primary limitation is the absence of clinical detail such as laboratory values and physician notes, which is why marketplace operators increasingly offer claims-plus-EHR linked datasets at premium price points. Genomic and multi-omic data represents 16.2% of the market at USD 515 Million, growing at above-market rates as precision medicine drug development accelerates demand for biomarker-stratified datasets. Patient-generated and wearable device data accounts for 11.4% at USD 362 Million. Social determinants of health and other data types represent the remaining 7.3%.

By Deployment Mode

The health data marketplace market by deployment mode is dominated by cloud-based platforms, which account for 71.8% of global market revenue in 2025 at USD 2.28 Billion. Cloud deployment enables the elastic compute infrastructure required to process and query petabyte-scale health datasets, provides the API accessibility that data buyer organizations require for programmatic data access, and supports the federated learning and privacy-enhancing computation architectures increasingly demanded by regulated buyers. Major cloud providers including AWS, Microsoft Azure, and Google Cloud have each developed health data marketplace capabilities that integrate with their broader cloud ecosystems, creating bundled value propositions for enterprise health and life sciences customers. On-premise deployment represents 18.6% of the market at USD 591 Million, primarily serving government health agencies, national health services, and defense health organizations that cannot place sensitive population health data on third-party cloud infrastructure for regulatory or security reasons. Hybrid deployment models account for the remaining 9.6% at USD 305 Million, reflecting organizations that maintain primary data storage on-premise while accessing marketplace analytics and data linkage services through secure cloud environments.

By End-User

The health data marketplace market by end-user is dominated by pharmaceutical and life sciences companies, which represent 44.7% of global revenue in 2025 at USD 1.42 Billion. Drug development organizations are the most consistent and highest-value buyers on health data marketplace platforms, using real-world data for every phase of the drug development cycle, from disease epidemiology characterization in target identification, through clinical trial site selection and patient population sizing, to post-approval safety monitoring and health technology assessment submissions. Health insurance and managed care organizations represent the second-largest end-user segment at 19.3% of the market in 2025 at USD 614 Million, purchasing health data to support actuarial modeling, care management program design, network adequacy analysis, and value-based contract performance measurement. Government and public health agencies account for 14.8% at USD 471 Million, deploying health data marketplace resources for population surveillance, pandemic preparedness modeling, and health system performance benchmarking. Healthcare providers and hospital systems, academic and research institutions, and medical device companies collectively represent the remaining 21.2% of the market.

By Data Modality

The health data marketplace market by data modality is bifurcated between structured data offerings and unstructured or imaging-based data offerings, with emerging federated and synthetic data products representing a rapidly growing third category. Structured data offerings, encompassing coded diagnosis, procedure, medication, and laboratory fields queryable through standard database environments, account for 58.6% of market revenue in 2025 at USD 1.86 Billion. These datasets are the most immediately actionable for pharmaceutical analytics, epidemiology, and health economics modeling, and command the highest transaction volumes on established marketplace platforms. Unstructured and imaging data offerings, including natural language processing-analyzed clinical notes, radiology DICOM image libraries, pathology slide repositories, and genomic sequence files, represent 28.4% of the market at USD 903 Million. These assets require more sophisticated analytical infrastructure on the buyer side but provide uniquely rich clinical context unavailable in coded data alone. Synthetic and federated data products account for 13.0% of the market at USD 413 Million in 2025, a segment growing at an estimated 38% annually as privacy regulations tighten and buyers seek data access models that eliminate re-identification risk.

Regional Analysis

North America

North America accounts for 42.1% of the global health data marketplace market in 2025, representing USD 1.34 Billion, and is the world’s most mature region for commercial health data exchange. The United States market is underpinned by the HIPAA Safe Harbor and Expert Determination de-identification frameworks, which provide legally defensible pathways for commercializing patient health information without individual consent requirements. The Office of the National Coordinator for Health Information Technology’s FHIR R4 implementation mandate for certified EHR systems, effective from 2021 and gaining compliance momentum through 2025, has dramatically increased the volume and standardization of electronically available health data. The 21st Century Cures Act’s information blocking prohibitions have reduced institutional barriers to data sharing, expanding the data supply available to marketplace operators. The U.S. pharmaceutical industry’s concentration of global R&D investment, representing approximately USD 105 Billion annually in 2025, creates persistent high-value demand for real-world evidence datasets that health data marketplace operators in the United States are uniquely positioned to supply. Canada’s market, representing approximately 11% of the regional total, is evolving as pan-Canadian health data governance frameworks under Health Canada’s digital health strategy create structured national data assets for secondary use.

Europe

Europe represents 26.8% of the global health data marketplace market in 2025 at USD 852 Million. The region’s market is shaped by the tension between the General Data Protection Regulation’s stringent consent and purpose limitation requirements for personal data processing and the European Health Data Space regulation’s mandate to unlock health data for secondary use in research, policy, and innovation. The European Health Data Space, advancing through the EU legislative process with adoption anticipated by 2025 to 2026, is expected to create a continental data governance framework that will dramatically expand the legally accessible health data supply for marketplace transactions by harmonizing secondary use rules across all 27 EU member states. Germany leads the European market, with its statutory health insurance claims data from over 105 funds representing one of the richest longitudinal population health databases in the world, and the Digital Healthcare Act creating pathways for digital health application data to flow into research infrastructures. The United Kingdom’s NHS, with its population-scale primary care and hospital records and established research data services including the Clinical Practice Research Datalink and NHS Digital, operates some of the world’s most valuable health data assets. The Nordic countries, particularly Finland and Denmark, have pioneered health data registry systems and ethical frameworks for secondary use that are being adopted as reference models across Europe.

Asia Pacific

Asia Pacific accounts for 20.4% of the global health data marketplace market in 2025 at USD 649 Million and is the fastest-growing regional market, projected to expand at a CAGR exceeding 24% through 2034. China is the largest and fastest-growing national market in the region, with the National Health Commission’s National Medical Data Center initiative creating a centralized infrastructure for aggregating hospital electronic health records across provincial networks. China’s Personal Information Protection Law and data localization requirements create a distinct regulatory environment that shapes both domestic marketplace architecture and international data exchange restrictions. Japan’s Medical Information Database infrastructure provides linked claims and EHR data for a population of 130 million, and the Ministry of Health, Labour and Welfare has established frameworks for secondary use of this data for pharmaceutical research that are actively utilized by domestic and multinational drug developers. India’s health data marketplace is at an earlier developmental stage but growing rapidly under the Ayushman Bharat Digital Mission, which is creating a national health ID system linking patient records across public and private providers. South Korea’s Health Insurance Review and Assessment Service database provides comprehensive claims records for 51 million insured individuals, and regulatory frameworks for de-identified data research use are well established.

Latin America

Latin America represents 6.1% of the global health data marketplace market in 2025 at USD 194 Million. Brazil is the dominant market, with its Lei Geral de Proteção de Dados (LGPD) data protection framework providing a regulatory structure analogous to GDPR that is shaping compliant health data commercialization pathways. The Brazilian health system’s unique combination of a large unified public health system (SUS) with extensive claims and clinical data and a growing private health insurance sector creates a dual-track data asset landscape. Mexico’s Seguro Popular successor program and IMSS data systems represent substantial secondary use opportunities, with initial framework development underway. Colombia and Argentina have enacted their own data protection frameworks that pharmaceutical companies operating regional real-world evidence programs must navigate. The primary constraint across Latin America is the fragmentation of health data systems, inconsistent digital infrastructure quality across public and private sectors, and limited dedicated health data governance frameworks that create compliance uncertainty for marketplace operators.

Middle East & Africa

Middle East & Africa represents 4.6% of the global health data marketplace market in 2025 at USD 146 Million. The United Arab Emirates leads regional market development, with the Dubai Health Authority and Abu Dhabi Department of Health having established structured electronic health record systems and data governance frameworks that enable controlled secondary use of health data for research and commercial purposes. The UAE’s Health Data Law provides consent-based pathways for health data sharing that international pharmaceutical companies are beginning to utilize for regional real-world evidence generation. Saudi Arabia’s Vision 2030 digital health transformation has invested substantially in hospital information system modernization, generating data assets that the Saudi Health Council is developing governance frameworks to make available for research. South Africa represents the most developed sub-Saharan market, with academic health centers at major universities maintaining research databases that support clinical studies. The African continent’s health data marketplace potential is significant given its disease burden diversity and underrepresented population genetics, but infrastructure gaps and regulatory immaturity limit near-term commercial activity to specific research partnerships rather than scalable marketplace transactions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Data Type

- Clinical and Electronic Health Record Data

- Claims and Administrative Data

- Genomic and Multi-Omic Data

- Patient-Generated and Wearable Device Data

- Social Determinants of Health Data

By Deployment Mode

- Cloud-Based Platforms

- On-Premise Deployment

- Hybrid Deployment

By End-User

- Pharmaceutical and Life Sciences Companies

- Health Insurance and Managed Care Organizations

- Government and Public Health Agencies

- Healthcare Providers and Hospital Systems

- Academic and Research Institutions

- Medical Device Companies

By Data Modality

- Structured Data Offerings

- Unstructured and Imaging Data

- Synthetic and Federated Data Products

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.18 B |

| Forecast Revenue (2034) | USD 14.76 B |

| CAGR (2025-2034) | 18.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Data Type, (Clinical and Electronic Health Record Data, Claims and Administrative Data, Genomic and Multi-Omic Data, Patient-Generated and Wearable Device Data, Social Determinants of Health Data), By Deployment Mode, (Cloud-Based Platforms, On-Premise Deployment, Hybrid Deployment), By End-User, (Pharmaceutical and Life Sciences Companies, Health Insurance and Managed Care Organizations, Government and Public Health Agencies, Healthcare Providers and Hospital Systems, Academic and Research Institutions, Medical Device Companies), By Data Modality, (Structured Data Offerings, Unstructured and Imaging Data, Synthetic and Federated Data Products) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IQVIA, OPTUM (UNITEDHEALTH GROUP), DATAVANT, VEEVA SYSTEMS, MERATIVE (IBM WATSON HEALTH), KOMODO HEALTH, INOVALON, AMAZON WEB SERVICES (AWS HEALTHLAKE), MICROSOFT (AZURE HEALTH DATA SERVICES), GOOGLE CLOUD (HEALTHCARE API), DEFINITIVE HEALTHCARE, SYMPHONY HEALTH (ICON PLC), HEALTH CATALYST, ARCADIA, TRUVETA, FLATIRON HEALTH (ROCHE), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Pharma, Healthcare Providers, Payers, Government Agencies), By Data Modality, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Pharma, Healthcare Providers, Payers, Government Agencies), By Data Modality, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User (Pharma, Healthcare Providers, Payers, Government Agencies), By Data Modality, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Health Data Marketplace Market?

The Global Health Data Marketplace Market was valued at USD 2.68 Billion in 2024 and is projected to reach USD 14.76 Billion by 2034, growing at a CAGR of 18.6% from 2026 to 2034, driven by rising adoption of digital healthcare ecosystems, increasing demand for secure healthcare data exchange platforms, advancements in AI and blockchain technologies, and expanding use of real-world health data for clinical research, precision medicine, and healthcare analytics worldwide.

Who are the major players in the Health Data Marketplace Market?

IQVIA, OPTUM (UNITEDHEALTH GROUP), DATAVANT, VEEVA SYSTEMS, MERATIVE (IBM WATSON HEALTH), KOMODO HEALTH, INOVALON, AMAZON WEB SERVICES (AWS HEALTHLAKE), MICROSOFT (AZURE HEALTH DATA SERVICES), GOOGLE CLOUD (HEALTHCARE API), DEFINITIVE HEALTHCARE, SYMPHONY HEALTH (ICON PLC), HEALTH CATALYST, ARCADIA, TRUVETA, FLATIRON HEALTH (ROCHE), Others

Which segments covered the Health Data Marketplace Market?

By Data Type, (Clinical and Electronic Health Record Data, Claims and Administrative Data, Genomic and Multi-Omic Data, Patient-Generated and Wearable Device Data, Social Determinants of Health Data), By Deployment Mode, (Cloud-Based Platforms, On-Premise Deployment, Hybrid Deployment), By End-User, (Pharmaceutical and Life Sciences Companies, Health Insurance and Managed Care Organizations, Government and Public Health Agencies, Healthcare Providers and Hospital Systems, Academic and Research Institutions, Medical Device Companies), By Data Modality, (Structured Data Offerings, Unstructured and Imaging Data, Synthetic and Federated Data Products)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Health Data Marketplace Market

Published Date : 21 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date