- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Healthcare Natural Language Processing Market Size | CAGR 20.6%

Global Healthcare Natural Language Processing Market Size, Share, Growth Analysis By Component (Software Solutions, NLP-Specific Services, GPU Compute Infrastructure), By Application (Clinical Documentation, Medical Coding, Decision Support, Pharmacovigilance, Population Health Analytics), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 4.86 Billion | USD 26.14 Billion | 20.6% | North America, 44.3% |

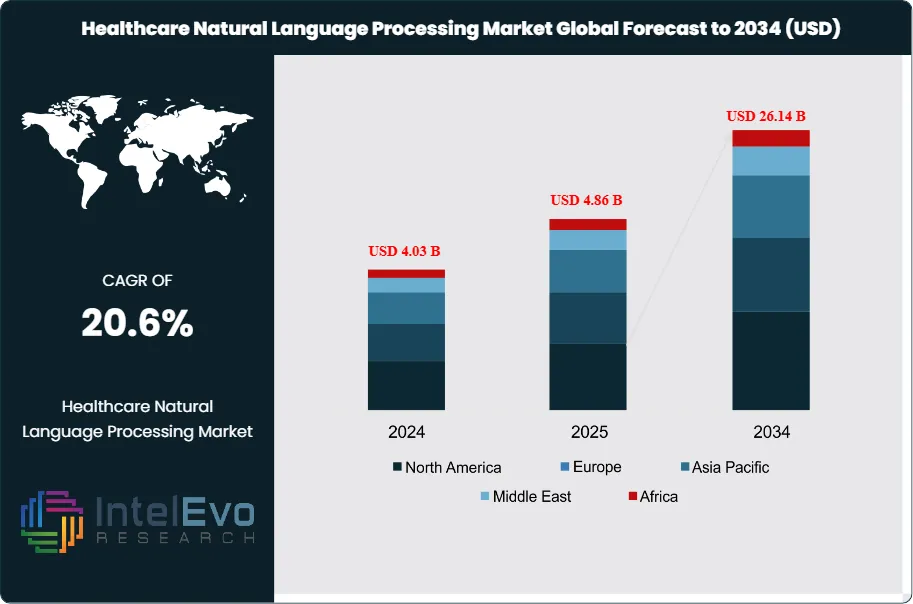

The Healthcare Natural Language Processing Market was valued at approximately USD 4.03 Billion in 2024 and reached USD 4.86 Billion in 2025. The market is projected to grow to USD 26.14 Billion by 2034, expanding at a CAGR of 20.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 21.28 Billion over the analysis period, driven by the explosive growth of unstructured clinical text data, the maturation of large language model architectures specifically trained on medical corpora, and the expanding commercial deployment of NLP-powered applications across clinical documentation, revenue cycle management, pharmacovigilance, and population health analytics.

Get More Information about this report -

Request Free Sample ReportHealthcare natural language processing applies computational linguistics, machine learning, and large language model technology to extract structured meaning from unstructured clinical text, including physician notes, radiology reports, pathology findings, discharge summaries, prior authorization correspondence, call center transcripts, and patient-generated communications. An estimated 80% of clinically relevant healthcare information is generated and stored in unstructured text formats within electronic health record systems, representing a vast reservoir of patient knowledge that conventional structured database analytics cannot access. Healthcare NLP converts this unstructured text into queryable, analyzable, and actionable data that supports clinical decision support, quality measurement, research, and administrative automation.

The generative AI revolution has fundamentally altered the healthcare NLP competitive environment since 2023. Large language models including GPT-4, Claude, Gemini, and specialized medical variants including Med-PaLM 2, NYUTron, and BioMedGPT have demonstrated clinical text comprehension capabilities that materially exceed prior generation NLP systems built on rule-based or classical machine learning architectures. These models perform clinical named entity recognition, relation extraction, temporal reasoning about clinical events, and generation of structured summaries from free-text notes at accuracy levels approaching clinical expert performance on benchmark evaluation sets. The commercial implication is that healthcare NLP solution providers must now compete on the basis of domain-specific model fine-tuning, healthcare regulatory compliance architecture, integration depth with EHR systems, and clinical workflow fit rather than core NLP model performance.

Regulatory engagement with healthcare NLP has intensified. The FDA’s Software as a Medical Device framework applies to NLP applications that meet the definition of a device, specifically those that analyze clinical text to support diagnosis, treatment recommendation, or patient monitoring decisions. The FDA’s predetermined change control plan framework, applicable to AI and ML-based software as a medical device, allows manufacturers to specify algorithm update protocols in advance, reducing the regulatory burden of continuous model improvement cycles. The EU Medical Device Regulation’s requirements for clinical evaluation and post-market surveillance apply to NLP-based diagnostic support tools, creating compliance obligations that favor established healthcare IT vendors with existing MDR infrastructure over pure-play AI entrants.

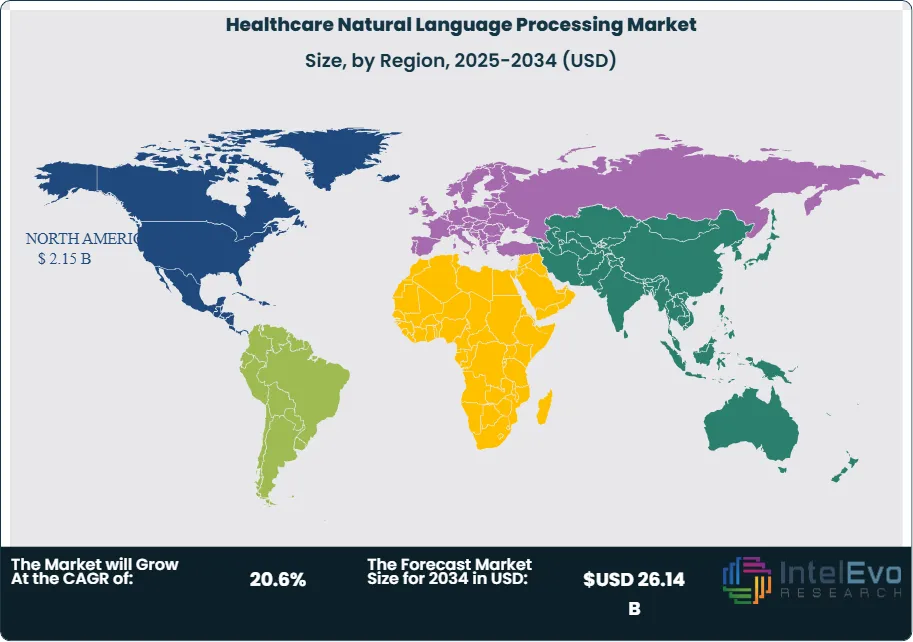

North America leads the healthcare natural language processing market with a 44.3% share in 2025 at USD 2.15 Billion, anchored by the United States’ concentration of EHR adoption, health system scale, and health AI investment. Asia Pacific is the fastest-growing region, driven by China’s national health informatization program, Japan’s Society 5.0 health technology initiative, and India’s rapidly digitizing healthcare system generating substantial unstructured clinical data volumes. Europe holds 24.8% of the global market, with Germany, France, and the United Kingdom leading NLP adoption in clinical documentation, diagnostics support, and pharmacovigilance.

, By Application (Clinical Documentation, Medical Coding, Decision Support, Pharmacovigilance, Population Health Analytics), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global healthcare natural language processing market was valued at USD 4.86 Billion in 2025 and is forecast to reach USD 26.14 Billion by 2034, expanding at a CAGR of 20.6% over the 2026–2034 forecast period.

- Segment Dominance: By component, software solutions hold the largest share at 62.4% of the healthcare NLP market in 2025, driven by platform-based NLP deployment across clinical documentation automation, revenue cycle management, and clinical decision support applications at health system scale.

- Segment Dominance: By application, clinical documentation and medical transcription represents the dominant application at 34.2% of market revenue in 2025, reflecting the immediate productivity and accuracy gains that NLP-powered ambient documentation and voice recognition deliver to physician workflows burdened by EHR data entry demands.

- Driver: Physician administrative burden from EHR documentation requirements consumes an estimated 2.0 to 2.5 hours of physician time per 8-hour clinical shift in U.S. ambulatory care settings, a burden directly correlated with physician burnout affecting over 63% of U.S. physicians as of 2025, creating institutional and individual demand for NLP-powered ambient documentation tools that reduce documentation time by 40 to 60%.

- Restraint: Clinical NLP model performance is highly sensitive to institutional linguistic variation, with models trained on one health system’s clinical notes demonstrating 8 to 22% performance degradation when applied to notes from a different institution without domain adaptation, creating implementation complexity and ongoing maintenance costs that limit rapid deployment at scale.

- Opportunity: The pharmaceutical industry’s pharmacovigilance and real-world evidence NLP applications represent an addressable market of USD 4.1 Billion by 2034, as drug safety teams deploy NLP to automatically extract adverse event signals from electronic health records, social media, and patient support program communications at a scale and speed that manual review processes cannot achieve.

- Trend: Ambient clinical intelligence platforms, which use always-on microphone and NLP to passively capture and structure clinical conversations during patient visits without physician interaction, achieved adoption at over 450 U.S. health systems by the end of 2025, establishing ambient documentation as the fastest-growing healthcare NLP deployment category with 68% year-over-year growth.

- Regional Analysis: North America leads the global healthcare natural language processing market with a 44.3% share in 2025, representing USD 2.15 Billion, supported by near-universal EHR adoption under Meaningful Use mandates, a concentrated health AI investment ecosystem, and acute physician documentation burden creating immediate NLP demand.

Competitive Landscape Overview

The healthcare natural language processing market is moderately consolidated at the platform level, with the top four players collectively accounting for approximately 46% of global market revenue in 2025. The competitive environment has been significantly disrupted by the emergence of large language model-native companies offering healthcare NLP capabilities that outperform prior-generation vendors on clinical text comprehension benchmarks, forcing established health IT companies to rapidly integrate LLM capabilities through acquisition, partnership, or internal development. Three competitive archetypes define the market: established health IT and EHR vendors embedding NLP natively into clinical workflow platforms, specialized healthcare AI companies building purpose-built NLP products for clinical and administrative applications, and hyperscaler cloud platforms providing healthcare NLP APIs and services that health system IT teams use to build custom applications. Strategic acquisitions accelerated in 2024 and 2025 as established companies paid premiums to acquire ambient documentation and clinical NLP startups before their technology advantages translated into competitive displacement.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Nuance (Microsoft) | USA | Leader | DAX Copilot ambient documentation | North America, Europe | Expanded DAX Copilot to 450+ health systems by end of 2025; integrated Azure OpenAI GPT-4 models into DAX clinical note generation, reducing documentation time by 50%. |

| Epic Systems | USA | Leader | Epic Nebula NLP / Suki integration | North America | Launched Epic Nebula NLP platform in 2025, enabling health systems to build custom NLP workflows on Epic data; deepened Suki ambient documentation partnership across Epic-installed base. |

| Google Cloud (Health AI) | USA | Challenger | MedLM / Healthcare NLP API | North America, Europe, APAC | Released MedLM commercial API in 2024, enabling healthcare enterprises to deploy fine-tuned medical language models; signed health system partnerships in 15 countries. |

| AWS (Amazon HealthScribe) | USA | Challenger | Amazon HealthScribe NLP | North America, Europe | Expanded HealthScribe ambient clinical documentation to specialty workflows including cardiology and oncology in 2025; integrated with major EHR platforms via FHIR APIs. |

| Suki AI | USA | Challenger | Suki Assistant ambient AI | North America, Europe | Reached 1 million patient notes generated per month milestone in 2025; secured strategic investment from Google and expanded EHR integrations to 10 platforms. |

| Veradigm (Allscripts) | USA | Niche Player | Veradigm NLP Analytics | North America | Launched NLP-powered real-world evidence extraction platform in 2025, enabling pharmaceutical companies to mine clinical notes from Veradigm’s 180 million patient network. |

| Iqvia (NLP Solutions) | USA | Niche Player | IQVIA NLP Workbench | North America, Europe | Expanded IQVIA NLP Workbench with large language model integration in 2025, targeting pharmacovigilance automation and clinical trial eligibility screening use cases. |

| Abridge | USA | Niche Player | Abridge ambient documentation AI | North America | Raised USD 150 Million Series C in 2024; expanded to 50+ health systems including UPMC, Kaiser Permanente, and Yale New Haven Health with generative AI note generation. |

By Component

The healthcare natural language processing market by component is led by software solutions, which captured 62.4% of global revenue in 2025 at approximately USD 3.03 Billion. Healthcare NLP software encompasses cloud-based SaaS platforms, on-premise software deployments, and API-accessible NLP services that health systems, payers, and pharmaceutical companies use to build NLP-powered workflows. The SaaS delivery model has become dominant within the software segment, with an estimated 71% of new healthcare NLP software contracts in 2025 structured as subscription-based cloud deployments rather than perpetual license or on-premise installations. This shift reflects health system IT organizations’ preference for vendor-managed infrastructure that reduces the burden of model maintenance, security patching, and HIPAA-compliant data management. NLP-specific services, encompassing implementation, integration, training, and ongoing model customization, represent 28.4% of the healthcare NLP market at USD 1.38 Billion in 2025. Services revenue is growing alongside software as health systems require specialized clinical informatics expertise to configure NLP models for institution-specific clinical note styles, specialty terminology, and workflow integration requirements that out-of-the-box software products cannot address without customization. Hardware, primarily the GPU compute infrastructure required for large language model inference and training, accounts for 9.2% of the market at USD 447 Million, a segment growing as on-premise and hybrid deployment models gain traction among health systems with data sovereignty requirements.

By Application

The healthcare natural language processing market by application is dominated by clinical documentation and medical transcription, which represents 34.2% of global revenue in 2025 at USD 1.66 Billion. This application segment encompasses traditional computer-assisted physician documentation, voice recognition transcription, and the rapidly growing ambient clinical intelligence category where NLP passively captures and structures clinical conversations. Ambient documentation platforms including Nuance DAX, Suki, Abridge, and DeepScribe are the fastest-growing products within this segment, with adoption accelerating as large language model-generated clinical notes achieve quality ratings from physicians that equal or exceed manually authored notes in blind evaluation studies. Revenue cycle management and clinical coding represents the second-largest application at 22.6% of the market in 2025 at USD 1.10 Billion. NLP-powered coding assistance automatically suggests ICD-10-CM, CPT, and HCC codes from clinical note text, reducing coding error rates by an estimated 18 to 25% and accelerating claim submission timelines. Clinical decision support accounts for 16.8% of the market at USD 816 Million, with NLP enabling real-time extraction of relevant patient history from unstructured notes to populate clinical alerts, care gap notifications, and evidence-based treatment recommendations. Pharmacovigilance and drug safety represents 12.4% at USD 603 Million, growing as pharmaceutical post-market surveillance obligations expand. Population health analytics, patient sentiment analysis, and other applications account for the remaining 14.0%.

By Deployment Mode

The healthcare natural language processing market by deployment mode reflects the evolving infrastructure preferences of health system and payer IT organizations navigating data privacy, latency, and cost considerations for AI workloads. Cloud-based deployment accounts for 58.6% of market revenue in 2025 at USD 2.85 Billion, driven by the availability of pre-trained healthcare-specific large language models on major cloud platforms, elastic compute scaling for variable NLP workloads, and the vendor-managed HIPAA Business Associate Agreement infrastructure that accelerates security compliance processes. Major cloud providers including Microsoft Azure, Google Cloud, and AWS have each established dedicated healthcare AI service portfolios that bundle NLP capabilities with compliant data storage and identity management, creating comprehensive deployment environments that health system IT organizations prefer to assembling individual components. On-premise deployment represents 27.8% of the market at USD 1.35 Billion, concentrated among large academic medical centers and government health agencies with data sovereignty requirements, high volumes of sensitive unstructured data, and the IT infrastructure investment capacity to operate GPU compute environments internally. Hybrid deployment models account for 13.6% at USD 661 Million, reflecting organizations that process de-identified or lower-sensitivity NLP workloads in cloud environments while retaining identifiable patient data processing on internal infrastructure.

By End-User

The healthcare natural language processing market by end-user is primarily served by healthcare providers and hospital systems, which account for 48.4% of market revenue in 2025 at USD 2.35 Billion. Hospitals and health systems are the largest deployers of clinical documentation NLP, coding assistance, and clinical decision support applications, motivated by physician productivity improvement, revenue cycle optimization, and quality metric performance. Academic medical centers are disproportionately active early adopters, combining large volumes of complex clinical notes with the research infrastructure and informatics expertise required to implement and evaluate NLP systems. Pharmaceutical and life sciences companies represent the second-largest end-user segment at 24.6% of the market in 2025 at USD 1.20 Billion, deploying NLP for pharmacovigilance, clinical trial recruitment and eligibility screening, real-world evidence extraction, and competitive intelligence analysis. Health insurance and managed care organizations account for 16.8% at USD 816 Million, applying NLP to prior authorization processing, claims audit, care management program identification, and member communication analysis. Government agencies and research institutions represent the remaining 10.2% at USD 496 Million, funding NLP programs for public health surveillance, health services research, and national health data infrastructure development.

Regional Analysis

North America

North America accounts for 44.3% of the global healthcare natural language processing market in 2025, representing USD 2.15 Billion, and is the world’s leading region by both commercial deployment activity and health AI investment. The United States’ near-universal adoption of certified EHR systems under the Health Information Technology for Economic and Clinical Health (HITECH) Act has created the unstructured clinical text data infrastructure that healthcare NLP requires to deliver value, with an estimated 2.3 Billion clinical notes generated annually across the U.S. health system. The concentration of health AI venture capital investment in the United States, which attracted over USD 6.1 Billion in digital health funding in 2024, has produced a dense ecosystem of healthcare NLP startups competing across clinical documentation, diagnostics, and administrative automation use cases. The Office of the National Coordinator for Health Information Technology’s FHIR API mandate has improved structured data access and standardized the interface layer through which NLP systems extract and return processed clinical information. Physician burnout at rates exceeding 63% of U.S. physicians in 2025, with documentation burden identified as the leading contributing factor in American Medical Association surveys, has elevated ambient documentation NLP from an IT initiative to a physician retention and organizational resilience strategy at major health systems. Canada contributes approximately 13% of the North American market, with provincial health systems and academic medical centers deploying NLP for clinical research and population health analytics supported by Canadian Institutes of Health Research funding.

Europe

Europe represents 24.8% of the global healthcare natural language processing market in 2025 at USD 1.21 Billion, with market development shaped by the tension between the General Data Protection Regulation’s stringent data processing requirements and the European Health Data Space’s mandate to unlock health data for research and innovation. Germany leads the European market, with its digital health act creating reimbursement pathways for digital health applications including NLP-powered clinical decision support tools, and major university hospitals deploying NLP for clinical documentation and research data extraction. The United Kingdom’s NHS has invested in NLP infrastructure through the NHS Artificial Intelligence Laboratory and the NHSX Data Strategy, with specific NLP programs targeting clinical coding automation, patient correspondence processing, and population health analytics. France’s Health Data Hub, established as a national secure data environment for health research, provides a GDPR-compliant infrastructure for NLP research on French population health data that is generating clinical NLP models for French-language medical text. The Nordic countries, particularly Finland and Denmark, have established themselves as advanced health informatics environments with high-quality national health registers and progressive data governance frameworks that enable healthcare NLP research and commercial deployment. The EU AI Act’s risk classification framework, placing healthcare diagnostic NLP in the high-risk category requiring conformity assessment, is establishing compliance obligations that favor established healthcare IT vendors with existing regulatory infrastructure.

Asia Pacific

Asia Pacific accounts for 21.6% of the global healthcare natural language processing market in 2025 at USD 1.05 Billion and is the fastest-growing regional market, projected to expand at a CAGR exceeding 25% through 2034. China is the dominant national market, with the National Health Commission’s Health Informatization Plan mandating EHR adoption at tier-3 hospitals and generating substantial volumes of Chinese-language clinical text that domestic NLP companies including Alibaba Health, Tencent Miying, and Ping An Good Doctor are building specialized models to analyze. China’s investment in medical AI has produced large language models specifically pre-trained on Chinese medical literature and clinical notes, with BioMedGPT and HuaTuo demonstrating competitive performance on Chinese medical NLP benchmarks. Japan’s healthcare NLP market is advancing under the Ministry of Health, Labour and Welfare’s AI strategy for healthcare, with NTT and Fujitsu leading development of Japanese-language clinical NLP systems for documentation and diagnostic support. India’s healthcare NLP market is growing rapidly as Ayushman Bharat Digital Mission creates a national digital health infrastructure, and domestic health AI companies including Niramai and Qure.ai are developing multilingual NLP capabilities for India’s linguistically diverse patient population. Australia’s Australian Digital Health Agency has funded NLP pilot programs targeting clinical coding automation and population health analytics.

Latin America

Latin America represents 5.6% of the global healthcare natural language processing market in 2025 at USD 272 Million, a market at an earlier stage of development constrained by heterogeneous EHR adoption rates, underdeveloped health informatics infrastructure, and the need for Spanish and Portuguese language clinical NLP models with sufficient training data to achieve clinical-grade performance. Brazil is the dominant market, with its large hospital networks including Rede D’Or and Hospital das Clínicas system deploying NLP for clinical coding assistance and administrative automation. Brazil’s Lei Geral de Proteção de Dados data protection framework shapes compliant data processing requirements for NLP applications handling patient health information. Mexico’s IMSS health system, serving over 72 million beneficiaries, represents a significant potential deployment environment for NLP-powered clinical documentation and coding tools. Colombia and Argentina are emerging markets with growing private hospital group investment in digital health technology. International NLP vendors targeting Latin America face the challenge of adapting models trained primarily on English-language clinical text to the linguistic patterns of Latin American Spanish and Brazilian Portuguese medical documentation, requiring local clinical corpus development partnerships.

Middle East & Africa

Middle East & Africa accounts for 3.7% of the global healthcare natural language processing market in 2025 at USD 180 Million. The United Arab Emirates is the regional leader in healthcare NLP adoption, with Dubai Health Authority and Abu Dhabi Health Services Company (SEHA) deploying NLP tools for clinical documentation, patient communication analytics, and administrative automation at their respective hospital networks. The UAE’s strategic commitment to becoming a regional health technology hub, supported by the Dubai Future Foundation’s health AI initiatives and Abu Dhabi’s Hub71 technology ecosystem, is attracting international healthcare NLP vendors to establish regional development centers. Saudi Arabia’s Vision 2030 health transformation program has invested in hospital information system modernization across the Ministry of Health’s 400+ hospital network, creating a structured data environment for NLP deployment. Arabic-language clinical NLP presents a specific technical challenge given Arabic’s morphological complexity and the diglossia between Modern Standard Arabic and regional dialects used in patient communication. South Africa’s academic hospital sector, centered at major universities, represents the most developed sub-Saharan NLP research environment, with several clinical NLP research programs producing South African English and Afrikaans medical language models.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software Solutions

- NLP-Specific Services

- Hardware (GPU Compute Infrastructure)

By Application

- Clinical Documentation and Medical Transcription

- Revenue Cycle Management and Clinical Coding

- Clinical Decision Support

- Pharmacovigilance and Drug Safety

- Population Health Analytics

- Patient Sentiment Analysis and Other Applications

By Deployment Mode

- Cloud-Based Deployment

- On-Premise Deployment

- Hybrid Deployment

By End-User

- Healthcare Providers and Hospital Systems

- Pharmaceutical and Life Sciences Companies

- Health Insurance and Managed Care Organizations

- Government Agencies and Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.86 B |

| Forecast Revenue (2034) | USD 26.14 B |

| CAGR (2025-2034) | 20.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software Solutions, NLP-Specific Services, Hardware (GPU Compute Infrastructure)), By Application, (Clinical Documentation and Medical Transcription, Revenue Cycle Management and Clinical Coding, Clinical Decision Support, Pharmacovigilance and Drug Safety, Population Health Analytics, Patient Sentiment Analysis and Other Applications), By Deployment Mode, (Cloud-Based Deployment, On-Premise Deployment, Hybrid Deployment), By End-User, (Healthcare Providers and Hospital Systems, Pharmaceutical and Life Sciences Companies, Health Insurance and Managed Care Organizations, Government Agencies and Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NUANCE COMMUNICATIONS (MICROSOFT), GOOGLE CLOUD (HEALTH AI), EPIC SYSTEMS, ABRIDGE, AMAZON WEB SERVICES (HEALTHSCRIBE), SUKI AI, VERADIGM (ALLSCRIPTS), IBM WATSON HEALTH (MERATIVE), 3M HEALTH INFORMATION SYSTEMS, OPTUM (UNITEDHEALTH GROUP), DEEPSCRIBE, AUGMEDIX, IODINE SOFTWARE, LINGUAMATICS (IQVIA), NFERENCE, CLINITHINK, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Clinical Documentation, Medical Coding, Decision Support, Pharmacovigilance, Population Health Analytics), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Clinical Documentation, Medical Coding, Decision Support, Pharmacovigilance, Population Health Analytics), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Clinical Documentation, Medical Coding, Decision Support, Pharmacovigilance, Population Health Analytics), By Deployment Mode (Cloud, On-Premise, Hybrid), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Healthcare Natural Language Processing Market?

The Global Healthcare Natural Language Processing Market was valued at USD 4.03 Billion in 2024 and is projected to reach USD 26.14 Billion by 2034, growing at a CAGR of 20.6% from 2026 to 2034, driven by rising adoption of AI-powered clinical documentation solutions, increasing use of NLP in electronic health records, medical coding, clinical analytics, and advancements in generative AI, voice recognition, and healthcare interoperability technologies worldwide.

Who are the major players in the Healthcare Natural Language Processing Market?

NUANCE COMMUNICATIONS (MICROSOFT), GOOGLE CLOUD (HEALTH AI), EPIC SYSTEMS, ABRIDGE, AMAZON WEB SERVICES (HEALTHSCRIBE), SUKI AI, VERADIGM (ALLSCRIPTS), IBM WATSON HEALTH (MERATIVE), 3M HEALTH INFORMATION SYSTEMS, OPTUM (UNITEDHEALTH GROUP), DEEPSCRIBE, AUGMEDIX, IODINE SOFTWARE, LINGUAMATICS (IQVIA), NFERENCE, CLINITHINK, Others

Which segments covered the Healthcare Natural Language Processing Market?

By Component, (Software Solutions, NLP-Specific Services, Hardware (GPU Compute Infrastructure)), By Application, (Clinical Documentation and Medical Transcription, Revenue Cycle Management and Clinical Coding, Clinical Decision Support, Pharmacovigilance and Drug Safety, Population Health Analytics, Patient Sentiment Analysis and Other Applications), By Deployment Mode, (Cloud-Based Deployment, On-Premise Deployment, Hybrid Deployment), By End-User, (Healthcare Providers and Hospital Systems, Pharmaceutical and Life Sciences Companies, Health Insurance and Managed Care Organizations, Government Agencies and Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Healthcare Natural Language Processing Market

Published Date : 22 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date