- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global High-Performance Computing as a Service Market Size | CAGR 13.5%

Global HPCasS Market Size, Share Analysis By Component (Solutions, Services), By Deployment (Public, Private, Hybrid, Multi-Cloud), By Organization (Large, SMEs), By Application (Research, AI & ML, Big Data, CFD, Genomics, Engineering Design, Cybersecurity), By End-User (Healthcare, BFSI, Government & Defense, IT & Telecom, Manufacturing, Energy, Aerospace) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 12.50 Billion | USD 39.00 Billion | 13.5% | North America, 42.0% |

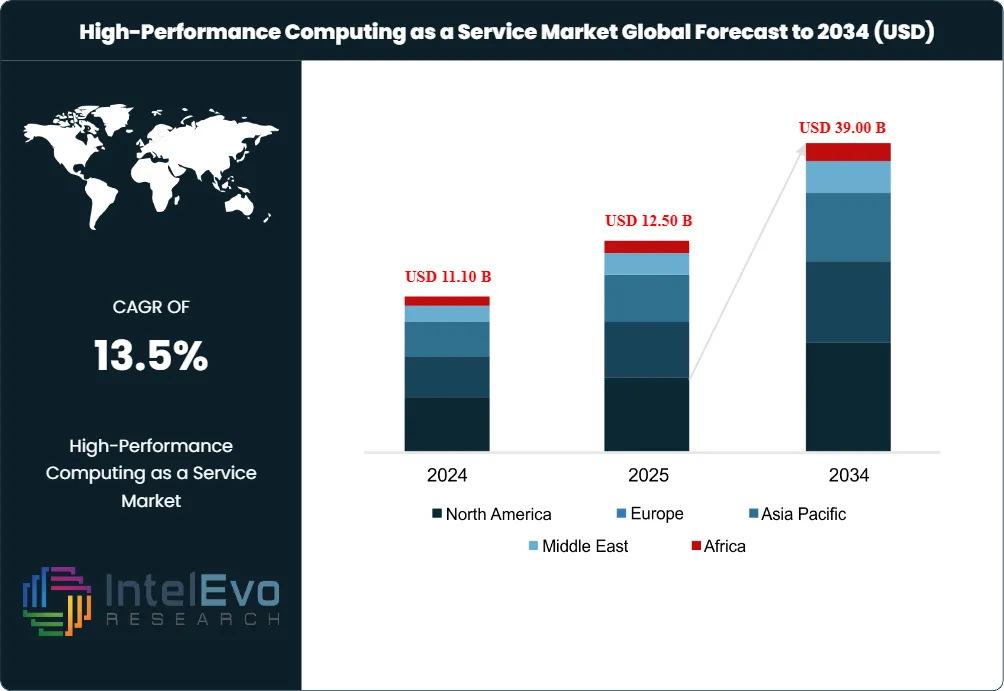

The High-Performance Computing as a Service Market was valued at USD 11.10 Billion in 2024 and USD 12.50 Billion in 2025. The market is projected to reach USD 39.00 Billion by 2034, expanding at a CAGR of 13.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 26.50 Billion over the analysis period. Demand is driven by AI training workload concentration at hyperscalers, accelerating cloud-burst patterns from on-premises supercomputing centers, and consumption-based pricing alignment with enterprise procurement preferences.

Get More Information about this report -

Request Free Sample ReportThe high-performance computing as a service market is anchored by Amazon Web Services (AWS) EC2 Hpc8a instances, Microsoft Azure HBv5 series, Google Cloud A3 instances, IBM Cloud HPC, Oracle Cloud Infrastructure HPC, and Hewlett Packard Enterprise (HPE) GreenLake for HPC. Data generation reached approximately 463 exabytes per day in 2025, propelling enterprise demand for parallel-data-processing workloads on cloud-delivered supercomputing. The U.S. hosts more than 110 active supercomputing sites, with exascale systems including Frontier at Oak Ridge National Laboratory and Aurora at Argonne National Laboratory setting public-sector performance benchmarks. Approximately 5 to 7 exascale supercomputers are operational worldwide as of 2025.

Cloud deployment captured the largest 2025 share at approximately 52.43% of the broader HPC market revenue, with the cloud HPC subset reaching USD 11.56 Billion in 2025 per industry analysis. Servers held 33.1% of HPC component spending, reflecting continuous demand for CPUs, GPUs, and high-speed interconnects. Government and defense led HPC end-use spending at 26.45% of 2025 revenue, anchored by U.S. Department of Energy National Laboratories, the Department of Defense, NASA, and equivalent European and Asian agencies. AI and machine learning workload integration has redrawn the HPCaaS landscape, with approximately 60% of AI development now using HPC environments for faster model processing.

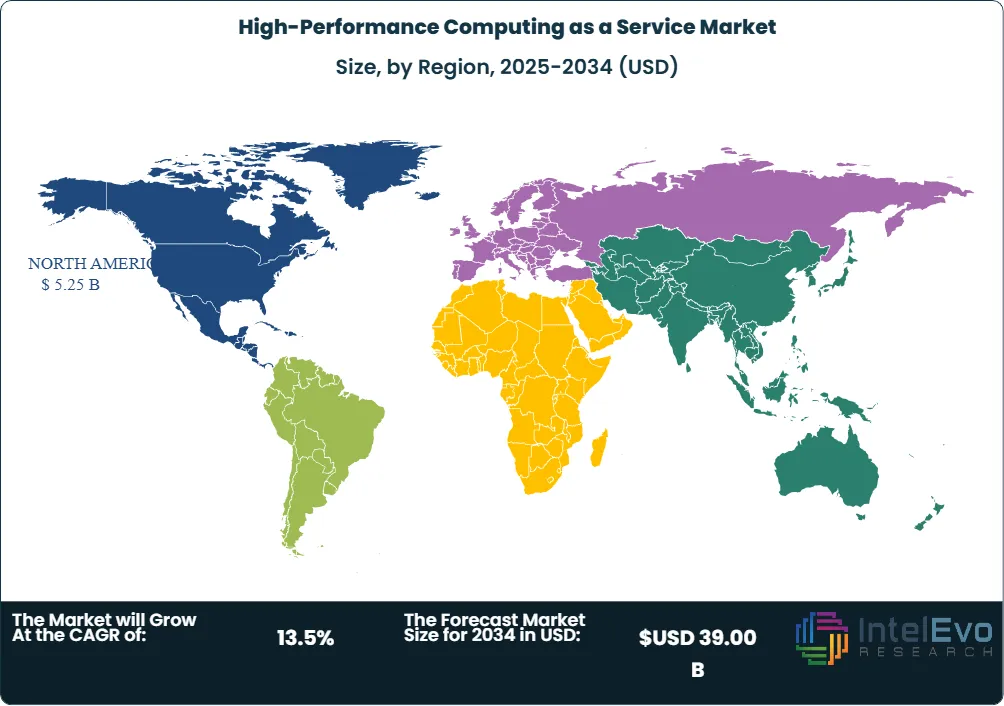

North America led the high-performance computing as a service market with approximately 42.0% revenue share in 2025, equivalent to roughly USD 5.25 Billion in regional revenue, anchored by AWS (Seattle), Microsoft (Redmond), Google Cloud (Mountain View), IBM (Armonk), and Oracle (Austin) hyperscaler concentration. Asia Pacific held the second-largest share and is forecast as the fastest-growing region driven by China's national supercomputer leadership, Japan's Fugaku and post-Fugaku roadmap, and India's National Supercomputing Mission. April 2026's general availability of AWS Interconnect multi-cloud connectivity, Google Cloud's seventh-generation Ironwood TPU achieving a 3.7-times Compute Carbon Intensity improvement over TPU v5p, and August 2024's AWS HPCaaS launch with GPU-cloud-cluster integration redrew competitive positioning at year-end 2025 through Q1 2026.

Market Definition & Scope

The high-performance computing as a service market is defined as the global commercial activity covering cloud-delivered, on-demand access to parallel-compute clusters, accelerator-equipped GPU and TPU instances, high-speed interconnects, parallel file systems, and managed orchestration software for compute-intensive workloads. The market includes Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) HPC offerings delivered through public cloud (AWS, Azure, Google Cloud, OCI, IBM Cloud), hosted private cloud (HPE GreenLake, Dell APEX), and colocation models with HPC overlay services.

This analysis includes high-performance technical computing (HPTC) workloads such as computational fluid dynamics, finite element analysis, molecular dynamics, weather modeling, seismic imaging, and genomics, as well as high-performance business computing (HPBC) workloads including risk analytics, fraud detection, real-time pricing, and large-scale machine-learning training. Excluded are general-purpose cloud compute services without HPC accelerators or interconnects, classical hardware sales without managed-service wrappers, on-premises supercomputers without service overlays, and pure quantum computing services. The high-performance computing as a service market sits within the broader HPC parent market valued at approximately USD 56.67 Billion in 2025.

, By Deployment (Public, Private, Hybrid, Multi-Cloud), By Organization (Large, SMEs), By Application (Research, AI & ML, Big Data, CFD, Genomics, Engineering Design, Cybersecurity), By End-User (Healthcare, BFSI, Government & Defense, IT & Telecom, Manufacturing, Energy, Aerospace) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The high-performance computing as a service market grew from USD 12.50 Billion in 2025 toward a forecast value of USD 39.00 Billion by 2034 at a 13.5% CAGR.

- Segment Dominance: Public cloud captured approximately 71.5% of HPCaaS revenue in 2024, anchored by AWS, Azure, Google Cloud, and Oracle Cloud Infrastructure offerings.

- Segment Dominance: Government and defense held the largest 26.45% share of HPC end-use spending in 2025, anchored by U.S. Department of Energy, Department of Defense, NASA, and European Defense Fund programs.

- Driver: Daily data generation reached approximately 463 exabytes per day in 2025, propelling enterprise demand for parallel-compute workloads on cloud-delivered supercomputing.

- Restraint: HPC operational expense remains substantial, with cryogenic cooling, GPU power density, and high-bandwidth interconnect requirements driving total cost of ownership.

- Opportunity: AI and machine learning convergence represents the largest forecast-period opportunity, with approximately 60% of AI development now running on HPC environments for faster model training.

- Trend: AMD EPYC 5th Generation processor adoption expanded across AWS, Azure, Google Cloud, and OCI during 2025, redefining x86 HPC instance performance baselines.

- Regional: North America led with 42.0% share in 2025 equivalent to roughly USD 5.25 Billion, while Asia Pacific is the fastest-growing region driven by China and Japan exascale programs.

Key Insights Summary

- AWS announced Interconnect multi-cloud general availability in April 2026, providing managed private connectivity that links Amazon Virtual Private Cloud directly to other cloud providers' VPCs.

- Amazon S3 Files launched in April 2026, making S3 buckets accessible as high-performance file systems on AWS compute resources with approximately 1-millisecond latencies.

- Google Cloud's seventh-generation Ironwood TPU achieved approximately 3.7-times improvement in Compute Carbon Intensity (CCI) compared to TPU v5p architecture per Google announcement.

- Microsoft Azure unveiled a distributed-edge HPCaaS platform in March 2025 designed for real-time AI and physics modeling, signaling accelerating shift toward edge HPC integration.

- AWS announced a new HPC-as-a-Service offering integrated with GPU-cloud-clusters in August 2024, enabling enterprises to address advanced simulations and compute loads.

- Compu Dynamics launched a dedicated AI and High-Performance Computing Services division in April 2025, providing comprehensive solutions covering system design, equipment procurement, construction, daily operations, and long-term maintenance with liquid-cooling emphasis.

- More than 90% of organizations utilize cloud services as of 2025, supporting HPCaaS adoption alongside the 5 to 7 exascale supercomputers operational worldwide.

Competitive Landscape Overview

The high-performance computing as a service market is highly concentrated, with the top four hyperscalers (Amazon Web Services, Microsoft Corporation, Google LLC, and IBM Corporation) collectively representing an estimated 65 to 72% of 2025 revenue. AWS holds the leading position through EC2 Hpc8a HPC-focused instances powered by 5th Generation AMD EPYC, AWS ParallelCluster orchestration, FSx for Lustre parallel file system, and AWS Interconnect multi-cloud connectivity. Microsoft Azure HBv5 series, Azure CycleCloud, and Microsoft HPC Pack anchor the second-largest position, with the March 2025 distributed-edge HPCaaS platform extending real-time AI and physics modeling capability. Google Cloud's HPC offerings include A3 GPU instances, Cluster Toolkit, and the seventh-generation Ironwood TPU.

Competitive evolution centers on three axes: GPU-and-accelerator inventory depth, multi-cloud and hybrid-cloud orchestration capability, and energy-efficiency and sustainability positioning. Oracle Cloud Infrastructure expanded with E6 VM and bare-metal instances on 5th Generation AMD EPYC during 2025, providing high-performance, cost-effective alternatives for distributed workloads. HPE GreenLake for HPC and Dell APEX HPC anchor the on-premises-managed-service alternative. NVIDIA DGX Cloud expanded across hyperscaler partners during 2025, providing turn-key AI-HPC managed-service capability. CoreWeave continued expansion of NVIDIA H200 and Blackwell GPU deployments. Strategic moves through 2025 included AWS-EC2-Hpc8a launch, Microsoft Azure SQL Server 2025 on AMD EPYC, OCI E6 instance launch, and April 2025's Compu Dynamics AI and HPC Services division formation.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Amazon Web Services | USA | Leader | EC2 Hpc8a, ParallelCluster, FSx for Lustre | North America, Europe, Asia Pacific | Apr 2026 launched AWS Interconnect multi-cloud GA |

| Microsoft Corporation | USA | Leader | Azure HBv5, Azure CycleCloud, HPC Pack | North America, Europe, Asia Pacific | Mar 2025 unveiled distributed-edge HPCaaS platform |

| Google LLC | USA | Leader | Cluster Toolkit, Ironwood TPU, A3 instances | North America, Asia Pacific | Apr 2026 Ironwood TPU achieved 3.7x CCI vs TPU v5p |

| IBM Corporation | USA | Leader | IBM Cloud HPC, Spectrum LSF, Cloud Paks | North America, Europe | Continued NTT DATA Asia Pacific partnership through 2025 |

| Oracle Corporation | USA | Challenger | OCI HPC, E6 VM and bare metal instances | North America, Europe | 2025 launched OCI E6 on 5th Gen AMD EPYC |

| Hewlett Packard Enterprise | USA | Challenger | HPE GreenLake for HPC, Cray EX | North America, Europe, Asia Pacific | Continued Cray EX supercomputer expansion 2025 |

| Dell Technologies | USA | Challenger | Dell APEX HPC, PowerEdge servers | North America, Europe | 2025 expanded APEX HPC with NVIDIA partnership |

| NVIDIA Corporation | USA | Niche Player | DGX Cloud, Omniverse Cloud | North America, Asia Pacific | 2025 expanded DGX Cloud across hyperscaler partners |

| CoreWeave Inc. | USA | Niche Player | Bare-metal GPU cloud, Kubernetes-native HPC | North America, Europe | 2025 expanded NVIDIA H200 and Blackwell deployments |

| Penguin Solutions | USA | Niche Player | Penguin POD HPC cloud, Stratus services | North America | Continued Federal HPC contract wins through 2025 |

Segmentation Analysis

The high-performance computing as a service market is segmented by component, deployment model, organization size, application, and end-user vertical, each producing distinct competitive and adoption patterns across the forecast period.

By Component

Solutions captured approximately 64% of high-performance computing as a service market revenue in 2025, anchored by managed compute clusters, GPU-accelerator-equipped instances, parallel file systems, and orchestration platforms. AWS ParallelCluster, Microsoft Azure CycleCloud, Google Cloud Cluster Toolkit, IBM Spectrum LSF, and HPE Cluster Management Software lead the solutions category. Services held approximately 36% of 2025 revenue covering implementation consulting, custom-cluster design, and managed-operations contracts delivered by HPE Pointnext, Dell ProDeploy, IBM Consulting, and specialized firms including Compu Dynamics. April 2025's Compu Dynamics launch of a dedicated AI and HPC Services division provides comprehensive solutions covering system design, equipment procurement, construction, daily operations, and long-term maintenance with liquid-cooling emphasis.

By Deployment Model

Public cloud deployment captured approximately 71.5% of high-performance computing as a service market revenue in 2024 because hyperscaler economics, on-demand pricing, and global region availability align with enterprise procurement preferences. AWS, Microsoft Azure, Google Cloud, Oracle Cloud Infrastructure, and IBM Cloud anchor the public cloud segment. Hosted private cloud held approximately 18% revenue share, dominated by HPE GreenLake for HPC, Dell APEX HPC, and IBM Cloud Pak deployments. Colocation captured the remaining 10.5% share through facility leasing arrangements where enterprises place HPC infrastructure inside third-party data centers. Hybrid deployment is forecast to grow at the fastest CAGR through 2030, propelled by enterprise preference for combining on-premises supercomputers with cloud-burst capacity for peak workloads.

By Organization Size

Large enterprises captured approximately 73% of high-performance computing as a service market revenue in 2025, anchored by major banks, oil and gas majors, automotive OEMs, aerospace primes, pharmaceutical companies, and federal government agencies. Small and medium enterprises (SMEs) held the remaining 27% share, expanding as pay-per-use pricing eliminates capital-expenditure barriers. Approximately 55% of advanced industrial and scientific workloads are forecast to use HPC clusters or HPCaaS models by year-end 2025, marking continued shift from traditional on-premises setups toward cloud-burst patterns. SMEs are forecast to grow faster through 2030 because consumption-based pricing eliminates the need for upfront capital investments and specialized HPC operations talent.

By Application

High-performance technical computing (HPTC) captured approximately 58% of high-performance computing as a service market revenue in 2025, addressing computational fluid dynamics, finite element analysis, molecular dynamics, weather modeling, seismic imaging, genomics, and engineering simulation workloads. AI training and inference workloads represented approximately 26% of 2025 revenue, growing fastest as approximately 60% of AI development now uses HPC environments for faster model processing. High-performance business computing (HPBC) held approximately 16% share covering risk analytics, fraud detection, real-time pricing, and high-frequency trading workloads. AI workload growth is forecast to overtake HPTC through 2030 as generative AI training cluster demand at OpenAI, Anthropic, Google DeepMind, Meta, and emerging foundation-model laboratories continues.

By End-User Vertical

Government and defense captured approximately 26.45% of high-performance computing as a service market revenue in 2025, the largest end-user vertical, anchored by U.S. Department of Energy National Laboratories, Department of Defense, NASA, and equivalent European Centre for Medium-Range Weather Forecasts (ECMWF) and Asian programs. BFSI held approximately 19% share through JPMorgan Chase, Goldman Sachs, BlackRock, HSBC, and Renaissance Technologies risk-modeling and quantitative-trading workloads. Manufacturing captured 14% share, anchored by BMW, Toyota, Boeing, and Airbus simulation workloads. Healthcare and life sciences held 11% share at Pfizer, Roche, and Genomics England. Energy held 10% share at ExxonMobil, Shell, and Chevron seismic-imaging workloads. Academia and research, retail, and other verticals account for the remaining 19.55% demand.

Regional Analysis

The global high-performance computing as a service market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with North American hyperscaler concentration and Asia Pacific exascale-program investment driving the geographic mix.

North America

North America led the high-performance computing as a service market with approximately 42.0% share in 2025, equivalent to roughly USD 5.25 Billion in regional revenue. The United States anchors regional supply through AWS (Seattle), Microsoft (Redmond), Google Cloud (Mountain View), IBM (Armonk), Oracle (Austin), HPE (Houston), Dell (Round Rock), and NVIDIA (Santa Clara). The country hosts more than 110 active supercomputing sites including Frontier at Oak Ridge National Laboratory and Aurora at Argonne National Laboratory exascale systems. Department of Energy National Laboratories, Department of Defense, NASA, and the National Science Foundation drive federal demand. Canada anchors regional supply through OVHcloud Canada and Penguin Solutions, supported by the Innovation, Science and Economic Development Canada Digital Strategy.

Europe

Europe held approximately 25% of high-performance computing as a service market revenue in 2025, valued near USD 3.13 Billion. Germany leads regional demand through Forschungszentrum Julich, the Leibniz Supercomputing Centre (LRZ), and the High Performance Computing Center Stuttgart (HLRS). The United Kingdom anchors supply through ARCHER2 at the University of Edinburgh and the Met Office. France contributes through GENCI and the European Centre for Medium-Range Weather Forecasts (ECMWF). The European Union EuroHPC Joint Undertaking committed EUR 7 Billion through 2027 across pre-exascale and exascale systems including LUMI in Finland, Leonardo in Italy, MareNostrum 5 in Spain, and Jupiter in Germany.

Asia Pacific

Asia Pacific captured approximately 21% of high-performance computing as a service market revenue in 2025, valued near USD 2.63 Billion, and is forecast as the fastest-growing region. China leads regional demand through Tianhe and Sunway TaihuLight supercomputer programs, with Alibaba Cloud, Tencent Cloud, and Huawei Cloud providing localized HPCaaS supply. Japan anchors regional supply through the Fugaku supercomputer at RIKEN and the post-Fugaku roadmap, with Fujitsu and NEC providing domestic vendor capacity. India's National Supercomputing Mission allocated INR 4,500 Crore through the Department of Science and Technology. South Korea contributes through KISTI, while Australia anchors demand through the Pawsey Supercomputing Centre.

Latin America

Latin America accounted for approximately 7% of high-performance computing as a service market revenue in 2025. Brazil leads regional adoption through Petrobras seismic-imaging workloads, Embraer aerospace simulation, and the Santos Dumont supercomputer at the National Laboratory for Scientific Computing (LNCC). Mexico contributes through PEMEX, CONACYT-funded research programs, and academic collaborations with U.S. National Laboratories. Argentina, Chile, and Colombia represent emerging demand pockets supported by mining, energy, and academic-research pilots. AWS Sao Paulo, Azure Brazil South, and Google Cloud Sao Paulo regions accelerate capacity additions through 2027.

Middle East & Africa

Middle East and Africa held approximately 5% of high-performance computing as a service market revenue in 2025. Saudi Arabia anchors regional demand through Saudi Aramco seismic-imaging workloads and the King Abdulaziz City for Science and Technology (KACST) Shaheen supercomputer. The United Arab Emirates contributes through Technology Innovation Institute (Abu Dhabi) and G42 Cloud HPCaaS offerings. Israel anchors regional demand through Bank Leumi, Bank Hapoalim, and Teva Pharmaceutical Industries computational workloads. South Africa contributes through the Centre for High Performance Computing (CHPC). Vision 2030 funding accelerates capacity additions through 2027.

Country Analysis

United States

The United States high-performance computing as a service market reached approximately USD 4.55 Billion in 2025, with country CAGR tracking near 13.8% through 2034. Demand concentrates at JPMorgan Chase, Goldman Sachs, ExxonMobil, Pfizer, Boeing, Lockheed Martin, and federal agencies including Department of Energy, Department of Defense, NASA, and the National Institutes of Health. Domestic supply concentrates at AWS (Seattle), Microsoft (Redmond), Google Cloud (Mountain View), IBM (Armonk), Oracle (Austin), HPE (Houston), Dell (Round Rock), NVIDIA (Santa Clara), and CoreWeave (Roseland). The CHIPS and Science Act allocated USD 52 Billion through fiscal year 2027 for domestic semiconductor manufacturing, indirectly supporting HPC processor and memory supply chains. Frontier at Oak Ridge and Aurora at Argonne anchor public exascale capacity.

Germany

Germany's high-performance computing as a service market reached approximately USD 750 Million in 2025, the largest single-country market within Europe with country CAGR near 13% through 2034. Forschungszentrum Julich operates the JUWELS modular supercomputer alongside the upcoming Jupiter exascale system funded through the EuroHPC Joint Undertaking. The Leibniz Supercomputing Centre (LRZ) operates SuperMUC-NG and the High Performance Computing Center Stuttgart (HLRS) operates Hawk. BMW, Volkswagen, Mercedes-Benz, BASF, Siemens, and Deutsche Bank drive enterprise demand. The Federal Ministry of Education and Research (BMBF) committed EUR 3 Billion through 2026 for digital infrastructure including HPC, with the Gauss Centre for Supercomputing coordinating national capacity allocation.

China

China's high-performance computing as a service market reached approximately USD 1.20 Billion in 2025, with country CAGR near 16% through 2034, the highest among major economies. Domestic supply concentrates at Alibaba Cloud, Tencent Cloud, Huawei Cloud, and Baidu Cloud, complemented by domestic supercomputer programs at the National Supercomputing Center in Tianjin, Wuxi, and Guangzhou. Demand concentrates at Industrial and Commercial Bank of China, BYD, Sinopec, ByteDance, JD.com, and Huawei for AI training, simulation, and analytics workloads. The 14th Five-Year Plan prioritizes domestic supercomputer leadership, with China hosting more supercomputers in the Top500 list than any other country.

Japan

Japan's high-performance computing as a service market reached approximately USD 580 Million in 2025, with country CAGR near 12% through 2034. The Fugaku supercomputer at RIKEN Center for Computational Science in Kobe ranks among the most powerful systems globally and provides cloud-burst capacity to Japanese enterprises and academic institutions. Toyota anchors automotive simulation demand, Hitachi drives industrial demand, and NEC and Fujitsu provide domestic vendor supply. The post-Fugaku roadmap targets exascale-class capacity by 2030 under the METI and Cabinet Office Computing Initiative, with HPC modernization eligible for Green Innovation Fund support.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Solutions

- HPC Infrastructure as a Service (IaaS)

- HPC Platform as a Service (PaaS)

- HPC Software and Management Platforms

- Data Storage and Management Solutions

- Cloud-Based Compute Services

- Workload Scheduling and Resource Management Solutions

- Analytics and Visualization Platforms

- Security and Compliance Solutions

- Others

- Services

- Consulting Services

- Deployment and Integration Services

- Managed Services

- Support and Maintenance Services

- Training and Professional Services

By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Multi-Cloud Deployment

- Community Cloud

- Others

By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

By Application

- Scientific Research and Simulation

- Artificial Intelligence and Machine Learning

- Big Data Analytics

- Modeling and Simulation

- Computational Fluid Dynamics (CFD)

- Risk Analysis and Financial Modeling

- Drug Discovery and Genomics

- Weather Forecasting and Climate Modeling

- Engineering Design and Testing

- Rendering and Visualization

- Seismic Processing and Exploration

- Cybersecurity and Threat Analysis

- Others

By End-User Vertical

- Healthcare and Life Sciences

- Banking, Financial Services, and Insurance (BFSI)

- Government and Defense

- Information Technology and Telecommunications

- Manufacturing

- Energy and Utilities

- Automotive

- Aerospace and Defense

- Academic and Research Institutions

- Media and Entertainment

- Oil and Gas

- Retail and E-Commerce

- Construction and Engineering

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 12.50 B |

| Forecast Revenue (2034) | USD 39.00 B |

| CAGR (2025-2034) | 13.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Solutions, Services), By Deployment Model, (Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud Deployment, Community Cloud, Others), By Organization Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), By Application, (Scientific Research and Simulation, Artificial Intelligence and Machine Learning, Big Data Analytics, Modeling and Simulation, Computational Fluid Dynamics (CFD), Risk Analysis and Financial Modeling, Drug Discovery and Genomics, Weather Forecasting and Climate Modeling, Engineering Design and Testing, Rendering and Visualization, Seismic Processing and Exploration, Cybersecurity and Threat Analysis, Others), By End-User Vertical, (Healthcare and Life Sciences, Banking, Financial Services, and Insurance (BFSI), Government and Defense, Information Technology and Telecommunications, Manufacturing, Energy and Utilities, Automotive, Aerospace and Defense, Academic and Research Institutions, Media and Entertainment, Oil and Gas, Retail and E-Commerce, Construction and Engineering, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AMAZON WEB SERVICES INC., MICROSOFT CORPORATION, GOOGLE LLC (ALPHABET INC.), IBM CORPORATION, ORACLE CORPORATION, HEWLETT PACKARD ENTERPRISE, DELL TECHNOLOGIES INC., NVIDIA CORPORATION, COREWEAVE INC., PENGUIN SOLUTIONS INC., ATOS SE (EVIDEN), FUJITSU LIMITED, NEC CORPORATION, LENOVO GROUP LTD., ALIBABA CLOUD, TENCENT CLOUD, HUAWEI TECHNOLOGIES CO. LTD., LAMBDA LABS INC., CRUSOE ENERGY SYSTEMS, CIRRASCALE CLOUD SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Public, Private, Hybrid, Multi-Cloud), By Organization (Large, SMEs), By Application (Research, AI & ML, Big Data, CFD, Genomics, Engineering Design, Cybersecurity), By End-User (Healthcare, BFSI, Government & Defense, IT & Telecom, Manufacturing, Energy, Aerospace) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Public, Private, Hybrid, Multi-Cloud), By Organization (Large, SMEs), By Application (Research, AI & ML, Big Data, CFD, Genomics, Engineering Design, Cybersecurity), By End-User (Healthcare, BFSI, Government & Defense, IT & Telecom, Manufacturing, Energy, Aerospace) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Public, Private, Hybrid, Multi-Cloud), By Organization (Large, SMEs), By Application (Research, AI & ML, Big Data, CFD, Genomics, Engineering Design, Cybersecurity), By End-User (Healthcare, BFSI, Government & Defense, IT & Telecom, Manufacturing, Energy, Aerospace) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the High-Performance Computing as a Service Market?

The Global High-Performance Computing as a Service Market was valued at USD 11.10 Billion in 2024 and USD 12.50 Billion in 2025, and is projected to reach USD 39.00 Billion by 2034, growing at a CAGR of 13.5% from 2026 to 2034. Market growth is driven by increasing adoption of cloud-based HPC, AI workloads, and advanced analytics applications.

Who are the major players in the High-Performance Computing as a Service Market?

AMAZON WEB SERVICES INC., MICROSOFT CORPORATION, GOOGLE LLC (ALPHABET INC.), IBM CORPORATION, ORACLE CORPORATION, HEWLETT PACKARD ENTERPRISE, DELL TECHNOLOGIES INC., NVIDIA CORPORATION, COREWEAVE INC., PENGUIN SOLUTIONS INC., ATOS SE (EVIDEN), FUJITSU LIMITED, NEC CORPORATION, LENOVO GROUP LTD., ALIBABA CLOUD, TENCENT CLOUD, HUAWEI TECHNOLOGIES CO. LTD., LAMBDA LABS INC., CRUSOE ENERGY SYSTEMS, CIRRASCALE CLOUD SERVICES, Others

Which segments covered the High-Performance Computing as a Service Market?

By Component, (Solutions, Services), By Deployment Model, (Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud Deployment, Community Cloud, Others), By Organization Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), By Application, (Scientific Research and Simulation, Artificial Intelligence and Machine Learning, Big Data Analytics, Modeling and Simulation, Computational Fluid Dynamics (CFD), Risk Analysis and Financial Modeling, Drug Discovery and Genomics, Weather Forecasting and Climate Modeling, Engineering Design and Testing, Rendering and Visualization, Seismic Processing and Exploration, Cybersecurity and Threat Analysis, Others), By End-User Vertical, (Healthcare and Life Sciences, Banking, Financial Services, and Insurance (BFSI), Government and Defense, Information Technology and Telecommunications, Manufacturing, Energy and Utilities, Automotive, Aerospace and Defense, Academic and Research Institutions, Media and Entertainment, Oil and Gas, Retail and E-Commerce, Construction and Engineering, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

High-Performance Computing as a Service Market

Published Date : 17 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date