- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

High-Performance Polyamides Market Size & Forecast 2034 | 7.0% CAGR

Global High-performance Polyamides Market Size, Share, Analysis Report By Form (Powder, Fibers, Pellets, Films, Sheets), Type (Polyarylamide, Polyamide 9T, Polyamide 46, Polyamide 6T, Polyamide 12, Polyamide 11, Polyphthalamide), Manufacturing Process (Blow Molding, Injection Molding), End-user Industry (Automotive, Industrial, Defense, Medical, Electronics), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

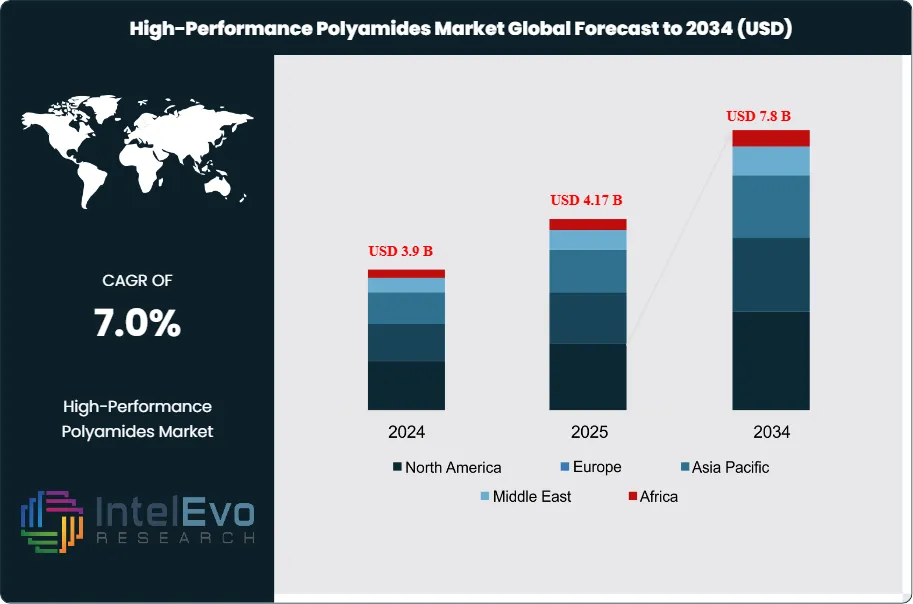

The High-Performance Polyamides Market size is projected to reach approximately USD 7.8 billion by 2034, up from USD 3.9 billion in 2024, growing at a CAGR of 7.0% during the forecast period from 2025 to 2034. The market is driven by the rising demand for lightweight, durable, and heat-resistant materials across industries such as automotive, aerospace, electrical & electronics, and industrial manufacturing. The adoption of high-performance polyamides in 3D printing, engineering plastics, and advanced composites is accelerating growth globally. As sustainability and material efficiency gain focus, polyamides are increasingly being preferred for applications requiring high strength-to-weight ratios, chemical resistance, and thermal stability.

Get More Information about this report -

Request Free Sample ReportHigh-Performance Polyamides (HPPA) are advanced engineering plastics known for their superior mechanical strength, heat resistance, and chemical durability. These materials go beyond the capabilities of standard polyamides like Nylon 6 or 66, making them ideal for use in harsh environments. HPPAs are commonly used in industries such as automotive, electronics, aerospace, and industrial manufacturing, where components are exposed to high temperatures, pressure, and corrosive substances. Their excellent dimensional stability and resistance to wear and fatigue also make them a preferred choice for precision parts like gears, fuel lines, connectors, and electrical housings. As industries push for lighter, stronger, and more reliable materials to improve performance and efficiency, the demand for high-performance polyamides continues to grow.

The growth dynamics of high-performance polyamides (HPPA) are strongly influenced by the increasing demand for lightweight, durable, and heat-resistant materials across key industries. In the automotive sector, HPPA is gaining traction due to the industry's push for lighter vehicles with better fuel efficiency and lower emissions. These materials replace metal components without compromising strength, especially in engine compartments and under-the-hood applications. In electronics, the miniaturization of devices and the need for heat-resistant parts have driven the use of HPPA in connectors, sockets, and circuit components.

The Asia-Pacific region has become a key growth center for the high-performance polyamides (HPPA) market, largely due to the rapid development of industries like automotive, electronics, and consumer goods. Countries such as China, Japan, South Korea, and India are seeing increased demand for durable, lightweight, and heat-resistant materials that HPPA can offer. In the automotive sector, for example, there's a strong push to replace heavier metal components with advanced polymers like HPPA to improve fuel efficiency and reduce emissions.

The COVID-19 pandemic significantly impacted the high-performance polyamides (HPPA) market, particularly during its initial phases. Lockdowns and restrictions led to the temporary shutdown of manufacturing facilities and disrupted global supply chains, causing delays in production and delivery of HPPA materials. Key industries that rely heavily on HPPA, such as automotive and electronics, experienced reduced demand due to decreased consumer spending and halted production lines.

, Type (Polyarylamide, Polyamide 9T, Polyamide 46, Polyamide 6T, Polyamide 12, Polyamide 11, Polyphthalamide), Manufacturing Process (Blow Molding, Injection Molding), End-user Industry (Automotive, Industrial, Defense, Medical, Electronics), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The High-performance polyamides market is expected to reach USD 7.8 billion by 2034, growing at a robust CAGR of 7.0%, indicating strong market expansion.

- Form Segment Dominance: The form segment is dominated by pellets, accounting for over 24% of the market share. Pellets are preferred for their ease of handling and compatibility with injection molding and extrusion, making them ideal for producing complex parts in automotive, electronics, and consumer goods industries.

- Type Segment Insights: Polyphthalamides is anticipated to hold the largest market share, favored for its lightweight and space-saving properties. PPA is valued for its strong heat resistance and mechanical durability, making it ideal for high-temperature uses like automotive engine parts and electronic components.

- Driver: The growing need for lightweight, durable materials in cars and electronics is boosting demand for high-performance polyamides (HPPAs). Their strength, heat resistance, and reliability make them perfect for automotive parts and electrical components, especially as industries push for better efficiency and performance.

- Restraint: High-performance polyamides (HPPAs) are more costly to produce than standard plastics due to expensive raw materials and complex manufacturing. These higher costs can discourage adoption, especially among smaller companies or in price-sensitive industries, making it harder to replace cheaper alternatives.

- Opportunity: As sustainability becomes a priority, demand is rising for eco-friendly, bio-based high-performance polyamides. Made from renewable resources, these materials help reduce environmental impact and meet stricter regulations, making them an attractive choice for forward-thinking companies.

- Trend: The ongoing shift toward EVs and compact, high-performance electronics is driving demand for materials that can handle higher voltages, heat, and mechanical stress in smaller, lighter forms. HPPAs fit the bill perfectly, making them increasingly popular in cutting-edge applications.

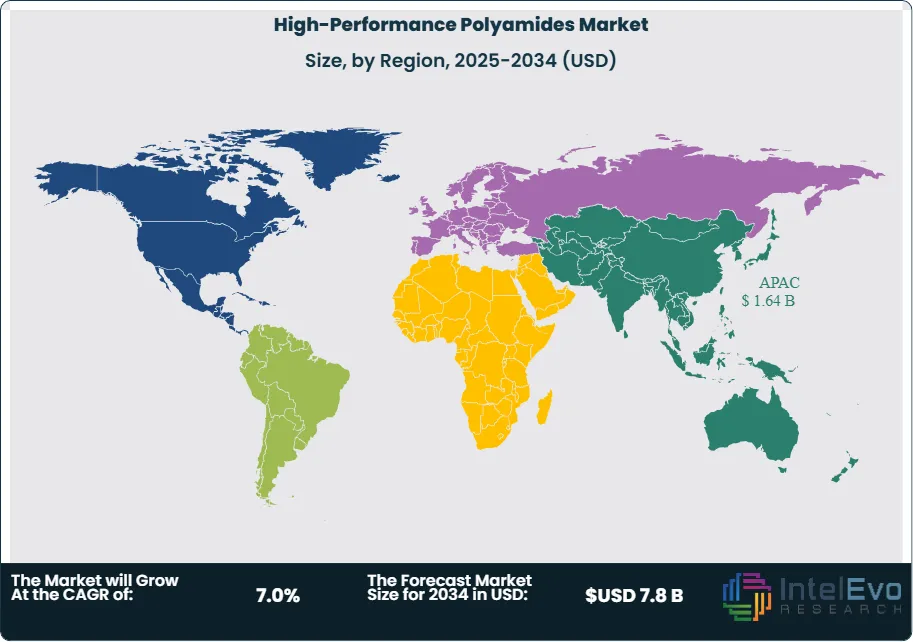

- Regional Analysis: The Asia-Pacific region is experiencing strong growth in the high-performance polyamides (HPPA) market due to expanding automotive, electronics, and consumer goods industries. Countries like China, Japan, and India are driving demand for lightweight, heat-resistant materials used in fuel-efficient vehicles and advanced electronics. Supportive policies and increased R&D investment are further boosting market growth.

Form Analysis:

The form segment is divided into powder, fibers, pellets, films, sheets, and others. The pellets segment dominated the market, with a market share of around 24% accounting for 0.8 billion 2024. Pellet form is widely preferred in the manufacturing industry because it is easy to handle, transport, and process. Its compatibility with common methods like injection molding and extrusion makes it ideal for mass production. Pellets are especially valued in sectors like automotive and electronics, where they are used to create intricate components such as connectors, housings, and structural parts. Their consistency and adaptability make them a crucial material in producing high-quality, durable products across various industries.

Type Analysis:

The type segment is divided into polyarylamide, polyamide 9T, polyamide 46, polyamide 6T, polyamide 12, polyamide 11, and polyphthalamides. The polyphthalamides segment dominated the market, with a market share of around 21% accounting for 0.7 billion 2024. Polyphthalamides (PPAs), a type of high-performance polyamide, are recognized for their exceptional thermal stability, mechanical strength, and chemical resistance. These qualities make them highly suitable for demanding industrial environments, particularly in the automotive and electronics sectors. In automotive applications, PPAs are often used in under-the-hood components such as air intake manifolds, coolant connectors, and fuel system parts, where exposure to high temperatures, harsh chemicals, and mechanical stress is common. Their ability to maintain structural integrity under these conditions helps enhance vehicle performance and longevity.

Manufacturing Process Analysis:

The manufacturing process segment is divided into blow molding and injection molding. The injection molding segment dominated the market, with a market share of around 56% accounting for 2.0 billion 2024. Injection molding is a highly efficient and versatile manufacturing process, especially valued for its ability to produce intricate components with great accuracy and a smooth surface finish. This technique involves injecting molten material—typically plastic or high-performance polymers—into a mold cavity where it cools and solidifies into the desired shape. It is extensively used in industries such as automotive, consumer electronics, and medical devices, where components often demand tight tolerances, consistent quality, and complex geometries. The process not only supports mass production but also reduces waste, making it cost-effective for large-scale manufacturing while ensuring repeatability and high precision in every unit produced.

End-user Industry Insights:

The end-user industry segment is divided into automotive, industrial, aerospace and defense, medical, electrical and electronics and others. The automotive segment dominated the market, with a market share of around 22% accounting for 0.8 billion 2024. The automotive industry heavily relies on high-performance polyamides because of their exceptional mechanical strength, heat resistance, and resistance to chemicals. These properties make them ideal for producing components that must endure harsh conditions, especially under the hood where temperatures and mechanical stress are high. High-performance polyamides are used in parts like engine covers, air intake manifolds, fuel system components, and structural reinforcements. Their lightweight nature also contributes to overall vehicle weight reduction, which supports better fuel efficiency and lower emissions—key goals for modern automotive design and sustainability efforts.

Region Analysis:

Asia-Pacific Leads With 42% Market Share in the High-performance Polyamides Market. The high-performance polyamides (HPPA) market in the Asia-Pacific region is witnessing significant growth, primarily fueled by the region's expanding industrial base and rising demand for high-tech materials. Countries such as China, Japan, South Korea, and India are at the forefront, with booming sectors like automotive, electronics, and industrial manufacturing actively adopting HPPA for its superior thermal stability, mechanical strength, and chemical resistance. In the automotive industry, HPPA is increasingly replacing metal components to reduce vehicle weight and improve fuel efficiency, aligning with stringent environmental regulations and consumer demand for energy-efficient solutions. Similarly, in the electronics sector, HPPA’s insulating properties and high heat resistance make it ideal for components used in smartphones, laptops, and other high-performance gadgets. Government initiatives that support domestic manufacturing, R&D investments, and favorable trade policies are also contributing to the regional market's momentum. Furthermore, as the demand for electric vehicles (EVs) and 5G technologies accelerates, the need for high-performance polymers like HPPA is expected to rise, positioning Asia-Pacific as a key hub for both production and consumption of these advanced materials.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product Type

- Polyamide 6 (PA6)

- Polyamide 66 (PA66)

- Polyamide 46 (PA46)

- Polyamide 12 (PA12)

- Specialty Polyamides (PA610, PA11, PA612, Others)

- Polyarylamide

- Polyphthalamide

- Other

By Form

- Powder

- Fibers

- Pellets

- Films

- Sheets

- Others

By Manufacturing Process

- Blow Molding

- Injection Molding

By Application

- Automotive Components

- Aerospace & Defense

- Electrical & Electronics

- Industrial & Manufacturing

- 3D Printing & Additive Manufacturing

- Consumer Goods

- Others

By End-Use Industry

- Automotive

- Aerospace

- Electronics

- Industrial Equipment & Machinery

- Medical Devices

- Consumer Goods

- Others

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.17 B |

| Forecast Revenue (2034) | USD 7.8 B |

| CAGR (2025-2034) | 7.0% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, Polyamide 6 (PA6), Polyamide 66 (PA66), Polyamide 46 (PA46), Polyamide 12 (PA12), Specialty Polyamides (PA610, PA11, PA612, Others), Polyarylamide, Polyphthalamide, Other), By Form (Powder, Fibers, Pellets, Films, Sheets, Others), By Manufacturing Process (Blow Molding, Injection Molding), By Application (Automotive Components, Aerospace & Defense, Electrical & Electronics, Industrial & Manufacturing, 3D Printing & Additive Manufacturing, Consumer Goods, Others), By End-Use Industry (Automotive, Aerospace, Electronics, Industrial Equipment & Machinery, Medical Devices, Consumer Goods, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Arkema, BASF SE, Evonik Industries AG, Lanxess, Royal DSM, SABIC, Toray Industries Inc, Asahi Kasei, DuPont, Koninklijke DSM N.V., KURARAY CO. LTD., Mitsui Chemicals, RTP Company, Teknor Apex Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Type (Polyarylamide, Polyamide 9T, Polyamide 46, Polyamide 6T, Polyamide 12, Polyamide 11, Polyphthalamide), Manufacturing Process (Blow Molding, Injection Molding), End-user Industry (Automotive, Industrial, Defense, Medical, Electronics), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Type (Polyarylamide, Polyamide 9T, Polyamide 46, Polyamide 6T, Polyamide 12, Polyamide 11, Polyphthalamide), Manufacturing Process (Blow Molding, Injection Molding), End-user Industry (Automotive, Industrial, Defense, Medical, Electronics), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Type (Polyarylamide, Polyamide 9T, Polyamide 46, Polyamide 6T, Polyamide 12, Polyamide 11, Polyphthalamide), Manufacturing Process (Blow Molding, Injection Molding), End-user Industry (Automotive, Industrial, Defense, Medical, Electronics), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

High-performance Polyamides market

Published Date : 11 Jun 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date