- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Home EV Charger Market Size, Share & Forecast 2034 | CAGR 24.7%

Global Home EV Charger Market Size, Share, Analysis By Charger Type (Level 1, Level 2, Smart EV Chargers), By Power Output (Up to 7 kW, 7.1–22 kW, Above 22 kW), By Connectivity (Wi-Fi, Bluetooth, Cellular), By Installation Type (Wall-Mounted, Pedestal, Portable), By End-User (Households, Apartments, Fleet Owners) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Smart Charging Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 10.50 Billion | USD 76.80 Billion | 24.7% | Asia Pacific, 40.0% |

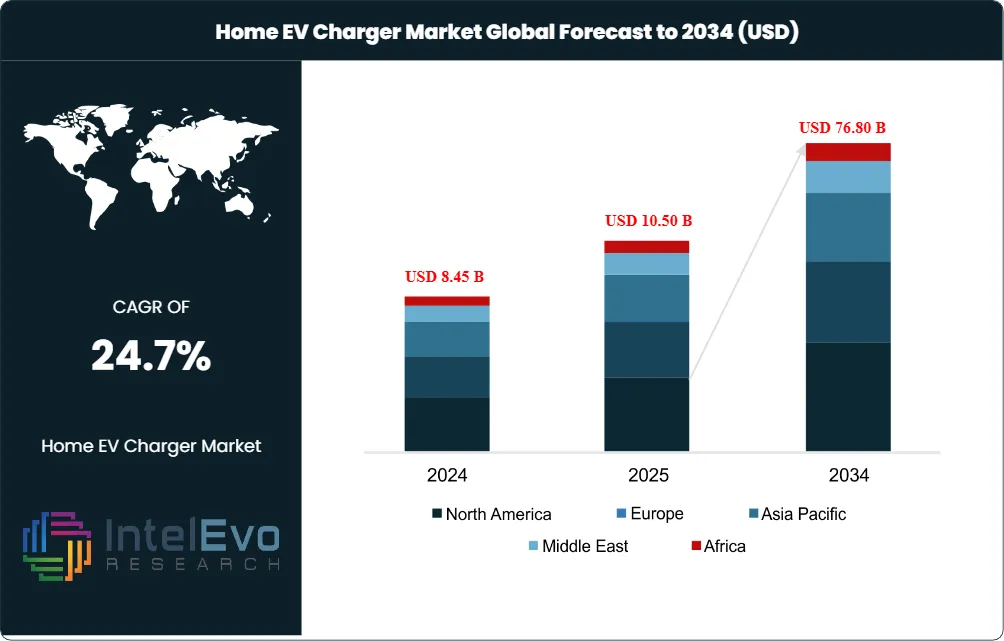

The Home EV Charger Market was valued at USD 8.45 Billion in 2024 and USD 10.50 Billion in 2025. The market is projected to reach USD 76.80 Billion by 2034, expanding at a CAGR of 24.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 66.30 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportDemand for home EV charger hardware is being pulled forward by passenger electric vehicle adoption rates that crossed 17% of global new car sales in 2024 according to International Energy Agency data, with home charging accounting for the majority of total energy delivered to private EVs in mature markets such as the United Kingdom, Norway, and the Netherlands. The U.S. Department of Energy estimates that 25.7 million private Level 1 and Level 2 charging ports at single-family homes will be required by 2030 to serve a projected fleet of 33 million electric vehicles, anchoring the long-run demand thesis for residential charging hardware.

Regulation continues to operate as a structural tailwind. The European Union's revised Energy Performance of Buildings Directive mandates pre-cabling for residential parking, while the Alternative Fuels Infrastructure Regulation (AFIR) sets corridor-charging benchmarks that reinforce home-charging investment confidence. In the United States, the Section 30C Alternative Fuel Vehicle Refueling Property Credit, modified by the One Big Beautiful Bill Act of July 2025, provides up to USD 1,000 toward home charger installations placed in service through June 30, 2026, in eligible census tracts. China's GB/T 18487 connector standard and India's FAME framework further widen the regulated installed base.

Technology choices are shifting toward bidirectional charging, dynamic load management, and smart-home integration. In April 2025, ChargePoint disclosed a redesigned Level 2 platform that scales to 22 kW for European installations and reaches 19.2 kW on North American circuits, with vehicle-to-home and vehicle-to-grid pathways included as standard, signaling a category-wide upgrade cycle. Wallbox's Quasar 2 received UL certification as the first CCS1 bidirectional home charger to clear U.S. safety standards for DC residential equipment. Smart, networked devices accounted for roughly 65% of new residential deployments in 2024 according to industry analysis, a trajectory that compresses the addressable share for non-connected legacy units.

Asia Pacific led with approximately 40.0% revenue share in 2025, anchored by Chinese manufacturing scale, BYD's bundled charger franchise, and Korean fast-charging investments worth KRW 620 Billion in 2025. North America followed at 27.5%, supported by USD 5 Billion of NEVI corridor funding through 2026 and state-level rebates that range from USD 250 to USD 2,000 per home installation. Europe held 24.5%, propelled by Germany's Deutschlandnetz allocations and the United Kingdom's home-charging dependency that already exceeds 90% of EV owners. The forecast through 2034 anticipates compound consolidation among the top hardware makers, deeper integration between charger OEMs and energy management software, and an accelerated shift toward 11 kW and higher-power AC units as average EV battery capacity rises beyond 75 kWh.

Market Definition & Scope

The home EV charger market is defined as the design, manufacture, sale, and installation of alternating-current and direct-current charging equipment up to 22 kW that is permanently or semi-permanently affixed at single-family homes and multi-unit residential dwellings to replenish electric passenger vehicles and plug-in hybrid vehicles during overnight or extended parking. The market encompasses Level 1 (120V) units, Level 2 (208V-240V) wall-mounted and pedestal units, smart-networked equipment with Wi-Fi or cellular connectivity, bidirectional vehicle-to-home and vehicle-to-grid hardware, portable plug-in units, and the associated cable assemblies, mounting brackets, and load-management modules sold as integrated kits.

The scope covers original-equipment-bundled chargers shipped with new EVs, aftermarket retail purchases, utility-rebate-funded installations, and OEM-installer channels. The analysis excludes public DC fast charging stations above 22 kW, commercial fleet depot chargers, workplace chargers paid for by an employer, on-board vehicle charging electronics integrated into the EV itself, and battery-swapping infrastructure. Wireless inductive home charging is included where commercially deployed. The home EV charger market accounted for approximately 26% of total global EV charging infrastructure spending in 2025, the largest application slice of that parent category.

, By Power Output (Up to 7 kW, 7.1–22 kW, Above 22 kW), By Connectivity (Wi-Fi, Bluetooth, Cellular), By Installation Type (Wall-Mounted, Pedestal, Portable), By End-User (Households, Apartments, Fleet Owners) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Smart Charging Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The home EV charger market reached USD 10.50 Billion in 2025 and is forecast to expand to USD 76.80 Billion by 2034 at a CAGR of 24.7%, representing a USD 66.30 Billion absolute dollar opportunity.

- Segment Dominance (Charger Type): Level 2 wall-mounted units commanded approximately 67.6% of revenue share in 2025, supported by overnight 4-8 hour full-charge capability and broad EV compatibility.

- Segment Dominance (Connectivity): Smart, networked chargers held approximately 65.3% of revenue in 2025 and are projected to expand at a 21.4% CAGR as utilities tie rebate eligibility to OCPP-compliant equipment.

- Driver: U.S. Department of Energy modelling projects 25.7 million private Level 1 and Level 2 ports at single-family homes by 2030, generating approximately 27 million net additional installations.

- Restraint: Panel-upgrade requirements averaging USD 2,000 to USD 4,500 per residence delay roughly 30-40% of single-family installations in homes with electrical service older than 2005.

- Opportunity: Bidirectional vehicle-to-home equipment, exemplified by Wallbox's Quasar 2 and GM Energy's V2H platform, represents a USD 8-10 Billion incremental revenue pool by 2034 as utility V2G tariffs mature.

- Trend: Average selling prices for connected Level 2 home chargers fell to the USD 599-USD 799 mid-market band in 2025, with Emporia's Pro charger illustrating sub-USD 600 retail pricing for load-managed smart units.

- Regional: Asia Pacific led the home EV charger market in 2025 with approximately 40.0% share and USD 4.20 Billion in revenue, driven by Chinese passenger EV penetration above 45% of new sales.

Key Insights Summary

- During 2024, more than 1.3 million public charging points were added globally, representing year-over-year expansion above 30%, per the International Energy Agency Global EV Outlook 2025.

- Private Level 1 and Level 2 ports installed at single-family residences are projected to total 25.7 million in the United States by 2030, accounting for 92% of the 28 million ports the National Laboratory of the Rockies estimates will be required to serve 33 million on-road EVs.

- Argonne National Laboratory expects U.S. lithium-ion battery pack costs to fall toward USD 86 per kWh by 2035, a trajectory that compounds downward pressure on charger electronics and bundled-purchase pricing.

- Wallbox disclosed cumulative shipments above 1 million chargers across more than 100 countries through June 30, 2025, in its Form 6-K filing with the U.S. Securities and Exchange Commission.

- Through Q2 2025, Tesla operated approximately 54.3% of all U.S. public DC fast-charging ports on a cumulative basis, an installed base that anchors brand pull-through into the residential Wall Connector channel.

- Section 30C of the U.S. Internal Revenue Code, as amended by the One Big Beautiful Bill Act of July 2025, allows a 30% tax credit capped at USD 1,000 per home charging port for residences placed in service through June 30, 2026, in eligible low-income or non-urban census tracts.

- China hosted approximately 65% of the global public charging stock and 60% of the global electric light-duty vehicle stock at year-end 2024 according to the IEA, a base that pulls residential charger demand into the country at scale.

Competitive Landscape Overview

The home EV charger market is moderately consolidated, with the top four hardware manufacturers (Tesla, ChargePoint, Wallbox, Schneider Electric) collectively holding an estimated 38% of 2025 revenue. Below this leadership tier, the field is fragmented across regional specialists, smart-home accessory brands, and electrical-equipment incumbents that compete on installation simplicity, software platform, and rebate eligibility rather than raw hardware specifications.

Competition is bifurcating along two axes. The first is the bundled-EV channel, where Tesla and BYD ship Wall Connectors and integrated home equipment with new vehicles to lock in the post-purchase charging experience. The second is the open-protocol smart-charger channel, where Wallbox, ChargePoint, Schneider Electric, and Emporia compete on OCPP compliance, utility-program approvals, and load-management software. Strategic pairings between charger OEMs and electrical-distribution leaders, such as the May 2025 alignment between Eaton and ChargePoint covering the United States, Canada, and Europe, are restructuring installer economics by combining switchgear with charging hardware in a single procurement workflow.

Competitive Landscape Matrix

| Company | HQ | Position | Key Home Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Tesla, Inc. | USA | Leader | Gen 3 Wall Connector, Universal Wall Connector | North America, Europe | Tall Pedestal mounting option for the Wall Connector debuted in February 2026 |

| ChargePoint Holdings | USA | Leader | Home Flex Level 2 | North America, Europe | Redesigned AC Level 2 architecture with up to 22 kW output disclosed in April 2025 |

| Wallbox N.V. | Spain | Leader | Pulsar Plus, Pulsar Pro, Quasar 2 | Europe, North America | UL certification for the Quasar 2 bidirectional home unit cleared in early 2025 |

| Schneider Electric | France | Leader | Schneider Charge, Charge Pro | Europe, North America | Charge Pro residential-grade unit for multifamily buildings introduced in January 2025 |

| Eaton Corporation | Ireland/USA | Challenger | Green Motion Home | North America, Europe | Joint infrastructure programme with ChargePoint covering three regions formalised in May 2025 |

| Siemens AG | Germany | Challenger | VersiCharge | Europe, North America | USD 25 Million stake in WiTricity advanced wireless residential pilots |

| ABB Ltd. | Switzerland | Challenger | Terra AC wallbox | Europe, Asia Pacific | Terra AC distribution agreements broadened across European utility tenders |

| Leviton Manufacturing | USA | Niche Player | Evr-Green Series | North America | Smart-home integration partnerships with Z-Wave and Matter protocols |

| Blink Charging | USA | Niche Player | HQ 200 home charger | North America | Distribution alliance with BetterFleet executed in February 2026 |

| Emporia | USA | Niche Player | EV Charger Pro | North America | Sub-USD 600 smart Level 2 unit with built-in load management gained Energy Star recognition |

By Charger Type

The home EV charger market by charger type is led by Level 2 (208V-240V) units, which captured approximately 67.6% of 2025 revenue. Level 2 hardware delivers full overnight charging within 4-8 hours, making it the structural workhorse of single-family residential installations. ChargePoint's Home Flex, Wallbox's Pulsar Plus, and Tesla's Gen 3 Wall Connector all anchor this segment with output bands between 7.7 kW and 11.5 kW. Level 1 units (120V) held about 24.8% of 2025 revenue, retaining a foothold among low-mileage households and PHEV owners where overnight 12-amp service satisfies daily replenishment without panel upgrades.

DC fast home chargers represented approximately 5.6% of 2025 revenue, driven principally by Wallbox's Quasar 2 bidirectional unit, which moves 24 kW of DC power directly into and out of the vehicle battery. Wireless inductive systems remained below 2.0% of 2025 revenue but are forecast to expand at a 34.8% CAGR through 2030 according to industry analysis, supported by Siemens' USD 25 Million strategic investment in WiTricity. Compared to Level 2, DC home equipment carries roughly 4-6 times the unit price, which constrains its near-term residential penetration.

By Power Output

Medium-power units in the 3.8 kW to 11 kW band led the home EV charger market with approximately 43.9% revenue share in 2025, reflecting alignment with the 7.7 kW to 11.5 kW onboard charger capacity of mainstream BEVs including Tesla Model Y, Hyundai Ioniq 5, and Volkswagen ID.4. High-power units above 11 kW held about 33.8% share and are forecast to expand at a 23.3% CAGR as 19.2 kW Level 2 architectures (NEMA 14-50 hardwired) gain traction following ChargePoint's April 2025 platform refresh. Low-power units up to 3.7 kW retained 22.3% share, anchored by portable plug-in models for PHEVs and apartment dwellers.

By Connectivity

Smart, networked chargers commanded approximately 65.3% of home EV charger revenue in 2025 and are projected to expand at a 21.4% CAGR through the forecast period. Networked devices enable dynamic load balancing, time-of-use rate scheduling, and utility demand-response participation, making them prerequisites for rebate eligibility under SMUD, ConEdison, Duke Energy, and most California Energy Commission programs. Non-smart units, mostly Level 1 plug-ins and entry-level pedestals, retained 34.7% share through 2025 but face structural decline as utilities and building codes increasingly require OCPP compliance.

By Installation Type

Wall-mounted units captured approximately 60.0% of 2025 revenue. Their compact form factor, integration with garage electrical panels, and weather-rated NEMA Type 4 enclosures (used by Wallbox Pulsar Plus and others) make them the default residential choice. Pedestal-mounted units held about 22.0% share, propelled by multifamily deployments where Tesla's February 2026 Tall Pedestal launch addresses the structural-wall constraint at apartment complexes and condominium parking decks. Portable plug-in units held 18.0%, posting a 19.6% CAGR through 2030 as renters and second-EV households adopt them as cost-efficient backup hardware.

By End-User

Single-family homes accounted for approximately 78.0% of 2025 home EV charger revenue, reflecting U.S. Department of Energy projections that 64% of all 2030 EV charging electricity will be delivered at single-family residences using L1 and L2 hardware. Multi-family residential dwellings held 22.0% share and represent the fastest-growing end-user segment, expanding from near-zero penetration five years ago to a 17% share of the U.S. market by 2030 per industry modelling. Curbside residential deployments, illustrated by itselectric's plan to scale New York City installations from 1,400 to 10,000 ports, sit at the intersection of multi-family and public categories.

Regional Analysis

North America

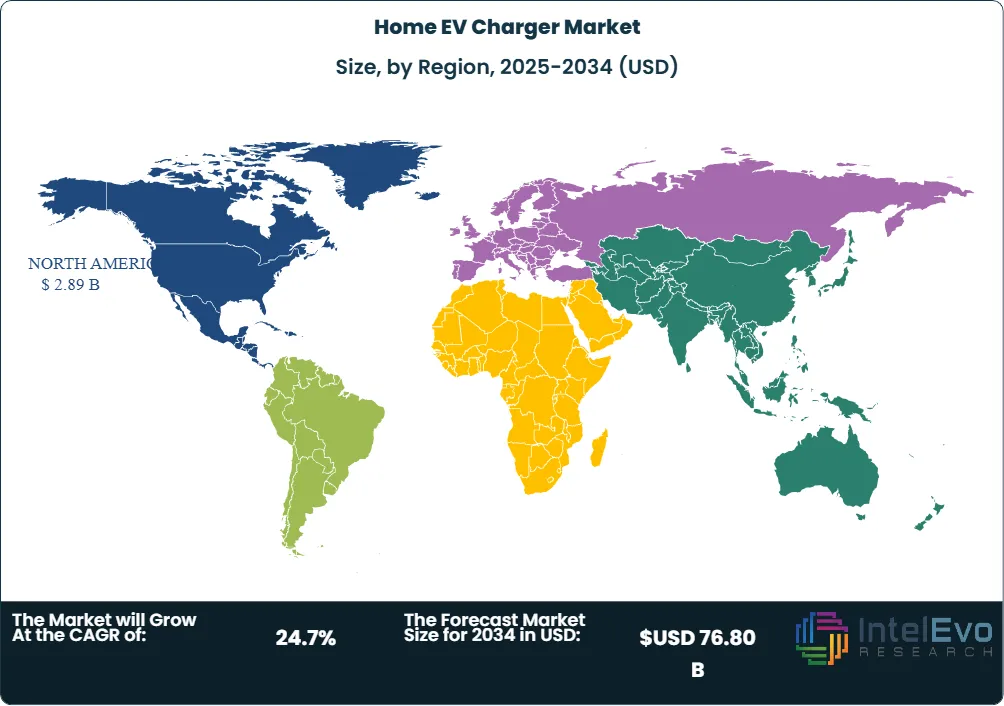

North America held approximately 27.5% of the home EV charger market in 2025, generating USD 2.89 Billion in revenue. The United States dominates with USD 2.45 Billion, anchored by the IRS Section 30C credit (30% up to USD 1,000) for installations placed in service through June 30, 2026. Canada contributed USD 0.32 Billion, supported by provincial rebates in British Columbia and Quebec. Mexico added USD 0.12 Billion, with Nuevo Leon and Mexico City driving urban adoption. The U.S. NEVI program's USD 5 Billion corridor allocation through 2026 spills indirectly into residential demand by reducing range anxiety. State-level programs such as the California Energy Commission's USD 56.5 Million Communities in Charge multifamily lane, opened through February 27, 2026, deepen coverage at apartment buildings.

Europe

Europe held approximately 24.5% of the home EV charger market in 2025, equivalent to USD 2.57 Billion. Germany led with USD 0.84 Billion, supported by the Deutschlandnetz programme's EUR 2 Billion fast-charger allocation and accelerated depreciation rules introduced from July 2025 for corporate charger investments. The United Kingdom contributed USD 0.61 Billion, where the Office for Zero Emission Vehicles' EV Chargepoint Grant funds up to GBP 350 per household for renters and flat owners. France added USD 0.48 Billion under the France 2030 programme. The Alternative Fuels Infrastructure Regulation (AFIR), in force since April 2024, mandates 150 kW corridor stations every 60 km along TEN-T core roads, indirectly reinforcing residential charging confidence. The revised Energy Performance of Buildings Directive requires pre-cabling at residential parking, a structural pull on installation volumes through 2030.

Asia Pacific

Asia Pacific led the home EV charger market in 2025 with approximately 40.0% share and USD 4.20 Billion in revenue. China commanded USD 2.94 Billion, propelled by passenger EV penetration crossing 45% of new sales in 2025 and BYD's bundled home-charger offering that ships with most BEVs. Japan contributed USD 0.46 Billion under the Green Growth Strategy targeting 150,000 charging points by 2030. South Korea added USD 0.34 Billion, supported by a 40% increase in the 2025 charging-infrastructure budget to KRW 620 Billion. India recorded USD 0.21 Billion, underpinned by FAME II extensions and three state-owned oil marketing companies that built nearly 8,000 fast-charging points across 2023-2024 funded by the FAME Phase II scheme. Australia and Southeast Asia together accounted for USD 0.25 Billion.

Latin America

Latin America held approximately 4.5% of the home EV charger market in 2025, contributing USD 0.47 Billion. Brazil led with USD 0.21 Billion, supported by ABNT NBR IEC 61851 standard adoption and Sao Paulo's growing EV registration base. Mexico recorded USD 0.13 Billion, while Chile added USD 0.07 Billion under its Electromobility Strategy 2050 targeting 100% zero-emission new-vehicle sales by 2035. Colombia and Argentina collectively accounted for USD 0.06 Billion. The region remains constrained by limited residential incentive budgets, but rising EV imports from Chinese manufacturers and Tesla's Mexico expansion are seeding aftermarket charger demand. Cross-region sourcing through Asian factories continues to compress hardware ASPs in Latin American retail channels.

Middle East and Africa

The Middle East and Africa region held approximately 3.5% of the home EV charger market in 2025 with USD 0.37 Billion in revenue, but is projected to post the highest regional CAGR at 17.4% through 2030 according to industry analysis. The United Arab Emirates led with USD 0.13 Billion under the Green Mobility Initiative and Dubai Electricity and Water Authority's EV Green Charger network rebates for villa owners. Saudi Arabia contributed USD 0.10 Billion, propelled by the Public Investment Fund's Lucid Motors stake and Vision 2030 mobility targets. Israel added USD 0.06 Billion, supported by EV stock that crossed 280,000 vehicles in 2025. South Africa, Egypt, and Morocco together contributed USD 0.08 Billion, driven by mining-sector and corporate fleet electrification spilling into employee-home installations.

Country Analysis

United States

The U.S. home EV charger market reached USD 2.45 Billion in 2025 and is forecast to grow at a 25.4% CAGR through 2034, outpacing the global average. Section 30C of the Internal Revenue Code, as amended by the One Big Beautiful Bill Act signed in July 2025, provides a 30% tax credit capped at USD 1,000 per residential charging port for installations placed in service through June 30, 2026, in eligible census tracts. The U.S. Department of Energy projects 25.7 million private Level 1 and Level 2 ports at single-family homes by 2030, against 33 million on-road EVs. State-level programs including California's USD 56.5 Million Communities in Charge multifamily lane (open through February 27, 2026), New York's USD 21 Million Central Hudson Make-Ready program, and PSE&G's New Jersey installation credit deepen residential rebate coverage. Tesla, ChargePoint, Wallbox, and Emporia together represent the bulk of U.S. retail volume.

China

China's home EV charger market reached USD 2.94 Billion in 2025 with a 24.2% projected CAGR through 2034. Passenger EV penetration crossed 45% of new-car sales in 2025, the trigger demographic for residential charger demand. The country's GB/T 18487-3 connector standard governs all home-charging hardware, while local subsidies in Shanghai, Shenzhen, and Guangzhou provide CNY 2,000-CNY 5,000 per household installation. BYD's bundled charger franchise, paired with the company's 1,000-volt supercharging strategy unveiled in 2025, drives roughly 38% of new home installations in tier-one cities. Apartment-dwelling households face a structural constraint, with only about 20% of Chinese EV owners holding access to private home chargers per Rabobank analysis, which preserves a long-term tailwind for public-supplemented residential charging models.

Germany

Germany's home EV charger market reached USD 0.84 Billion in 2025, expanding at a 22.8% projected CAGR through 2034. The Bundesregierung's KfW 442 program provided up to EUR 10,200 per household for combined PV plus charger plus battery installations through its 2024-2025 cycle, seeding more than 350,000 home installations. Beginning July 2025, accelerated depreciation provisions allow corporate buyers to write off home-charger investments faster, expanding the at-home company-car charging segment. Mennekes, Webasto, and ABL (acquired by Wallbox) anchor domestic manufacturing, while Schneider Electric and Eaton serve the smart-grid integration layer. Germany's homeownership rate of 49% creates a structural multifamily challenge that the EU Energy Performance of Buildings Directive's pre-cabling mandate progressively addresses.

United Kingdom

The U.K. home EV charger market reached USD 0.61 Billion in 2025 with a 23.5% projected CAGR through 2034. The Office for Zero Emission Vehicles' EV Chargepoint Grant covers 75% up to GBP 350 per home charger for renters and flat owners, while the EV Infrastructure Grant provides up to GBP 30,000 to landlords. More than 90% of U.K. EV owners rely on home charging according to International Energy Agency observations, the highest share among major Western markets. Pod Point, Andersen, Ohme, and Wallbox lead U.K. retail share, while Octopus Energy's tariff-integrated Intelligent Octopus Go program enrolled more than one million chargers by 2025, embedding home chargers into demand-response economics. The U.K.'s 2035 ban on new internal-combustion vehicle sales sustains volume momentum.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Charger Type

- Level 1 Chargers

- Level 2 Chargers

- Smart EV Chargers

- Others

By Power Output

- Up to 7 kW

- 7.1–22 kW

- Above 22 kW

- Others

By Connectivity

- Wi-Fi Enabled

- Bluetooth-Enabled

- Cellular Connected

- Others

By Installation Type

- Wall-Mounted

- Pedestal-Mounted

- Portable Chargers

- Others

By End-User

- Individual Households

- Residential Apartments

- Fleet Owners

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 10.50 B |

| Forecast Revenue (2034) | USD 76.80 B |

| CAGR (2025-2034) | 24.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Charger Type, (Level 1 Chargers, Level 2 Chargers, Smart EV Chargers, Others), By Power Output, (Up to 7 kW, 7.1–22 kW, Above 22 kW, Others), By Connectivity, (Wi-Fi Enabled, Bluetooth-Enabled, Cellular Connected, Others), By Installation Type, (Wall-Mounted, Pedestal-Mounted, Portable Chargers, Others), By End-User, (Individual Households, Residential Apartments, Fleet Owners, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TESLA, INC., CHARGEPOINT HOLDINGS, INC., WALLBOX N.V., SCHNEIDER ELECTRIC SE, ABB LTD., SIEMENS AG, EATON CORPORATION PLC, LEVITON MANUFACTURING CO., INC., BLINK CHARGING CO., EMPORIA ENERGY, EVIQO, WEBASTO GROUP, LECTRON, MENNEKES ELEKTROTECHNIK GMBH, DELTA ELECTRONICS, INC., ENPHASE ENERGY, INC., FLO INC., BYD COMPANY LTD., ANDERSEN EV, POD POINT GROUP HOLDINGS PLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Power Output (Up to 7 kW, 7.1–22 kW, Above 22 kW), By Connectivity (Wi-Fi, Bluetooth, Cellular), By Installation Type (Wall-Mounted, Pedestal, Portable), By End-User (Households, Apartments, Fleet Owners) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Smart Charging Tech Trends & Forecast 2026-2034")

, By Power Output (Up to 7 kW, 7.1–22 kW, Above 22 kW), By Connectivity (Wi-Fi, Bluetooth, Cellular), By Installation Type (Wall-Mounted, Pedestal, Portable), By End-User (Households, Apartments, Fleet Owners) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Smart Charging Tech Trends & Forecast 2026-2034")

, By Power Output (Up to 7 kW, 7.1–22 kW, Above 22 kW), By Connectivity (Wi-Fi, Bluetooth, Cellular), By Installation Type (Wall-Mounted, Pedestal, Portable), By End-User (Households, Apartments, Fleet Owners) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Smart Charging Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Home EV Charger Market?

The Global Home EV Charger Market was valued at USD 8.45 Billion in 2024 and USD 10.50 Billion in 2025, and is projected to reach USD 76.80 Billion by 2034, growing at a CAGR of 24.7% from 2026 to 2034. Market growth is driven by rising EV adoption, smart charging solutions, and residential charging infrastructure.

Who are the major players in the Home EV Charger Market?

TESLA, INC., CHARGEPOINT HOLDINGS, INC., WALLBOX N.V., SCHNEIDER ELECTRIC SE, ABB LTD., SIEMENS AG, EATON CORPORATION PLC, LEVITON MANUFACTURING CO., INC., BLINK CHARGING CO., EMPORIA ENERGY, EVIQO, WEBASTO GROUP, LECTRON, MENNEKES ELEKTROTECHNIK GMBH, DELTA ELECTRONICS, INC., ENPHASE ENERGY, INC., FLO INC., BYD COMPANY LTD., ANDERSEN EV, POD POINT GROUP HOLDINGS PLC, Others

Which segments covered the Home EV Charger Market?

By Charger Type, (Level 1 Chargers, Level 2 Chargers, Smart EV Chargers, Others), By Power Output, (Up to 7 kW, 7.1–22 kW, Above 22 kW, Others), By Connectivity, (Wi-Fi Enabled, Bluetooth-Enabled, Cellular Connected, Others), By Installation Type, (Wall-Mounted, Pedestal-Mounted, Portable Chargers, Others), By End-User, (Individual Households, Residential Apartments, Fleet Owners, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date