- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Hookah Market Size, Share, Rising Flavor & Lounge Demand | 9.1% CAGR

Global Hookah Market Size, Share & Analysis By Product Type (Flavor, Fruits, Mint, Chocolate, Others), By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others), Consumer Lifestyle Trends, Regulatory Impact, Competitive Strategies & Forecast 2025–2034

Report Overview

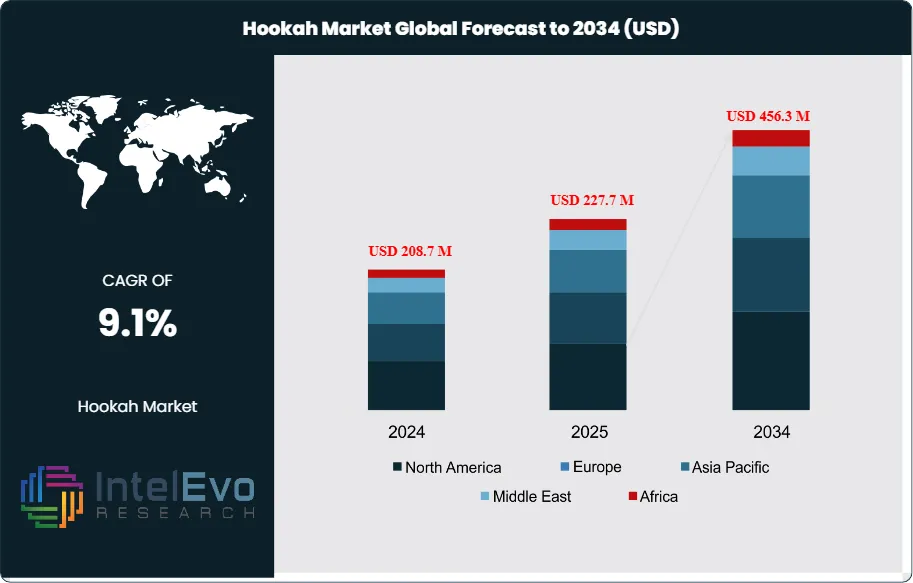

The Hookah Market is valued at approximately USD 208.7 million in 2024 and is projected to reach nearly USD 456.3 million by 2034, expanding at an estimated CAGR of around 9.1% during 2025–2034. Rising café culture, experiential lounges, and flavor innovation continue to fuel category momentum worldwide. Premium charcoal, herbal blends, and designer hookah setups are gaining strong traction among young adults and social nightlife segments. With social media influence and tourism-driven consumption growing rapidly, the hookah culture is evolving into a global lifestyle trend.

Get More Information about this report -

Request Free Sample ReportThe category has transitioned from a niche, culturally anchored pastime to a formal retail-and-lounge ecosystem with resilient, experience-led demand. After steady mid-single-digit expansion through the late 2010s, the market rebounded from pandemic-era disruptions as lounges reopened and at-home occasions persisted; volumes have normalized while average selling prices edged up on premium device designs and flavor innovation. Flavored shisha (molasses) now accounts for an estimated 70–75% of category value, while hardware—pipes, bowls, hoses, and heat-management devices—contributes roughly 20–25%, supported by premiumization and replacement cycles of 18–24 months.

Growth is underpinned by a young adult consumer base, social consumption occasions, and rapid flavor proliferation—fruit, mint, and confectionery notes together exceed 60% of new launches. E-commerce and direct-to-consumer channels, scaling from a low base, are gaining share and are projected to exceed 15% of retail sales by the mid-forecast period as age-gating and track-and-trace mature. On the supply side, modular metal and glass designs and standardized grommets have reduced assembly time and improved durability, while charcoal sourcing remains a sensitivity due to energy and freight cost volatility. Regulatory risk is the principal headwind: taxation, indoor-use restrictions, and flavor limitations in select jurisdictions can dampen lounge footfall and compress margins; health warnings and product standards add compliance costs but also professionalize the market.

Technology is a meaningful differentiator. Heat-management devices, precision-cut bowls, and electric/temperature-controlled heads improve heat distribution and reduce harshness, supporting higher repeat use. Contactless mouthpieces and disposable hoses, scaled post-pandemic, are now embedded hygiene features. Zero-nicotine herbal shisha and reduced-tobacco blends, albeit sub-scale, are expanding at double-digit rates as wellness-minded consumers seek alternatives.

Regionally, the Middle East & North Africa remains the demand anchor (≈35–40% of global spend) with high lounge density and tourist traffic, while South Asia and Türkiye form a sizable second cluster (≈20–25%) driven by cultural adoption. Europe (notably Germany and the U.K.) sustains steady lounge-led growth, and North America, though more regulated, is poised for above-trend expansion in compliant specialty retail. Investment hotspots include premium lounges in GCC cities, flavor houses with robust regulatory dossiers, electric heating platforms, and hygiene-driven accessories—segments positioned to outgrow the market average under the base-case outlook.

, By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others), Consumer Lifestyle Trends, Regulatory Impact, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Hookah Market is projected to reach USD 456.3 million from USD 208.7 million in 2024, reflecting a 9.1% CAGR, supported by experience-led social consumption, flavor proliferation, and premium device designs that lift average selling prices.

- Flavor Type: Flavored shisha leads with a 51.3% value share; fruit, mint, and chocolate profiles account for the bulk of launches and repeat purchases, sustaining higher-margin mix and brand-led differentiation.

- Hookah Configuration: Two-hose hookahs command over 67.2% share, evidencing the primacy of communal sessions and driving incremental sales of hoses, mouthpieces, and heat-management accessories in both retail and lounge settings.

- Driver: Demographic momentum from the 18–30 cohort—combined with group use comprising 76.3% of consumption occasions—amplifies lounge footfall and multi-user setups, reinforcing volume resilience and cross-sell opportunities.

- Restraint: Regulatory scrutiny on flavors and indoor smoking is the chief headwind; potential flavor limitations could directly pressure more than half of category revenue (51.3% share), while stricter venue rules compress lounge utilization and margin per session.

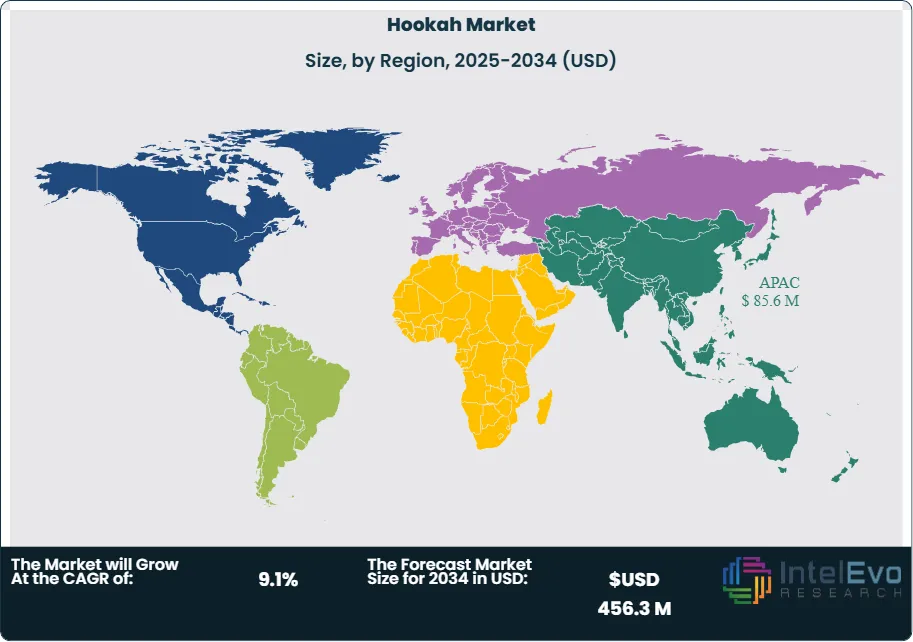

- Opportunity: Asia Pacific’s scale leadership (41% share) leaves room for premiumization in Tier-2/3 cities and travel corridors; electric and temperature-controlled heating systems and hygiene-focused accessories are poised for double-digit growth (≈12–14% CAGR) off a low base.

- Trend: Product innovation is shifting toward heat-management devices, precision bowls, and contactless/disposable hygiene components, while herbal/zero-nicotine blends expand from niche to meaningful share; online, age-gated sales are on track to reach the mid-teens of channel mix by 2030.

- Regional Analysis: Asia Pacific remains the revenue anchor at ~41%, with MENA and parts of Europe forming the next largest clusters via dense lounge networks; North America is smaller but projected to grow faster—high single-digit CAGR—where compliant specialty retail and premium lounges scale.

Product Type Analysis

The product mix in 2025 remains led by flavored shisha, which accounted for just over half of category value in 2023 (≈51.3%) and is holding near the 50–53% range as suppliers expand into dessert, beverage, and spice-inspired profiles. Fruit variants—apple, grape, berry, citrus—continue to anchor repeat purchase behavior and represent the largest slice within the broader “Flavor” umbrella, supported by steady launch cadence from global brands and regional producers. Mint retains outsized loyalty due to its cooling profile and strong mixability, while chocolate appeals to a distinct niche that skews toward premium and seasonal blends.

Innovation is shifting toward hybrid and exotic mixes (the “Others” bucket), including ice/menthol layers, spice–fruit pairings, and zero-nicotine herbal bases. These lines command a 5–10% price premium and are expanding faster than the category average (high-single-digit CAGR through 2030), aided by regulatory-compliant formulations and cleaner sensory profiles. Flavor houses with robust dossiers and consistent batch quality are winning lounge contracts and driving higher-margin assortments.

Age Group Analysis

The 18–30 cohort remains the primary demand engine in 2025, reflecting lounge-centric social occasions, flavor experimentation, and higher frequency of group sessions; this segment typically contributes the majority of occasions in urban markets. The 30–50 segment is expanding via premiumization—larger bowls, precision heat-management devices, and curated flavor flights—lifting average revenue per session in compliant venues.

Sales to individuals below legal purchase age are prohibited in most markets; enforcement tightening keeps this segment immaterial in formal channels. Users above 50 represent a smaller but stable base in culturally embedded markets, favoring classic profiles and traditional set-ups, with loyalty tempered by health and taxation dynamics.

Type Analysis

Two-hose hookahs continue to dominate (≈67.2% share in 2023; broadly stable into 2025) given ease of use, lower unit cost, and suitability for small groups at home and in lounges. Replacement cycles of 18–24 months and the adoption of modular stems sustain repeat hardware demand.

Three-hose systems, while a minority, are gaining traction in high-traffic lounges and event settings as operators seek to maximize table throughput and multi-user engagement. With rising adoption of heat-management devices and quick-light charcoals, 3-hose configurations are projected to outgrow the market (≈7–8% CAGR through 2030) in tourism and student-dense districts.

Application Analysis

Group use remains the dominant application (≈76.3% share in 2023; mid-70s in 2025) due to the social nature of the category and the economics of on-premise service. Higher seating utilization, flavor rotation, and accessory upsell (disposable tips, hoses) continue to lift venue yields.

Personal use, though smaller, is the faster-growing application, propelled by compact devices, electric/temperature-controlled heads, and online flavor subscriptions. From a low base, at-home occasions are expanding at high-single to low-double-digit rates in markets with restrictive indoor-use policies, shifting sales toward premium bowls and hygiene-forward components.

Distribution Channel Analysis

Specialty stores remain the primary retail channel (≈53.5% share in 2023; trending toward ~50–52% in 2025) as consumers value product expertise, authenticity checks, and accessory breadth. Bars and cafés—key on-premise nodes—benefit from post-pandemic social recovery, tourist flows, and curated tasting menus, accounting for a sizable minority of value with above-average margins.

Online continues to gain share from a low base, supported by age-gated checkout, click-and-collect, and direct-to-consumer flavor drops; in leading markets, the online mix is tracking toward the mid-teens by 2027. The “Others” channel (convenience, tobacconists, independent kiosks) caters to refill and impulse purchases, but faces compliance and assortment depth constraints.

End-Use Analysis

Commercial venues (lounges/bars/cafés) account for the largest value share, driven by service fees, premium device fleets, and higher flavor rotation per table. Investments in ventilation, contactless mouthpieces, and staff training have improved session consistency and raised spend per visit.

Household use represents a substantial and rising share as consumers adopt compact devices and electric heating for convenience and discretion. Hospitality and entertainment (hotels, resorts, events) remain smaller but fast-growing, particularly in tourist hubs, festivals, and premium nightlife corridors where curated experiences command price premiums.

By Region

Asia Pacific remains the demand anchor into 2025, sustaining an estimated ~41% global share on the back of large urban populations, cultural adoption, and expanding specialty retail in India, Southeast Asia, and parts of East Asia. The Middle East & Africa continues to post high per-capita consumption with dense lounge networks and tourism-led spend, while Europe (notably Germany and the U.K.) benefits from formalized specialty retail and stringent quality standards.

North America, though smaller, is on a faster trajectory (high-single-digit CAGR through 2030) as compliant specialty retail and premium lounges scale in metropolitan areas. Latin America is emerging from a low base—Mexico and Brazil lead—with growth tempered by regulatory variability and import costs. Across regions, investment hotspots include GCC premium lounges, APAC flavor manufacturing with documented compliance, and age-gated e-commerce platforms in North America and Europe.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Flavor

- Fruits

- Mint

- Chocolate

- Others

By Age Group

- Below 18 Years

- 18 to 30 Years

- 30 to 50 years

- Above 50 years

By Type

- 2 Hose

- 3 Hose

By Application

- Group Use

- Personal Use

By Distribution Channel

- Bars and Cafes

- Specialty Stores

- Online

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 208.7 M |

| Forecast Revenue (2034) | USD 456.3 M |

| CAGR (2024-2034) | 9.1% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Flavor, Fruits, Mint, Chocolate, Others), By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Evolution Hookahs, Social Smoke, Inc., HAZE Tobacco, LLC, Mya Hookah, ALZawrae Industrial Company, Ed Hardy Hookah, Starbuzz Hookahs, AL Andalus Flavoured Tobacco & Molasses Co. LLC, CLOUD Tobacco, Inc., METCO Ltd, Regal Hookahs, Fumari, Inc., Japan Tobacco, Inc., Anahi Hookahs, MUJEEBSONS, AL Fakher Tobacco Trading LLC, Tianbao Glass |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others), Consumer Lifestyle Trends, Regulatory Impact, Competitive Strategies & Forecast 2025–2034")

, By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others), Consumer Lifestyle Trends, Regulatory Impact, Competitive Strategies & Forecast 2025–2034")

, By Age Group (Below 18 Years, 18 to 30 Years, 30 to 50 years, Above 50 years), By Type (2 Hose, 3 Hose), By Application (Group Use, Personal Use), By Distribution Channel (Bars and Cafes, Specialty Stores, Online, Others), Consumer Lifestyle Trends, Regulatory Impact, Competitive Strategies & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date