- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Precision Fermentation Dairy Market Size & Forecast | CAGR 14.5%

Global Hospital Cyber Resilience Market Size, Share, Growth & Industry Analysis By Solution Type (Threat Detection & SIEM/SOAR, IoMT & Medical Device Security, Zero-Trust Network Access, IAM, Backup & Ransomware Resilience, Risk & Compliance), By Deployment Mode (Cloud SaaS, Hybrid, On-Premise), By Hospital Size (Large Systems, Community Hospitals, Critical Access) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 2.84 Billion | USD 9.62 Billion | 14.5% | North America, 46.8% |

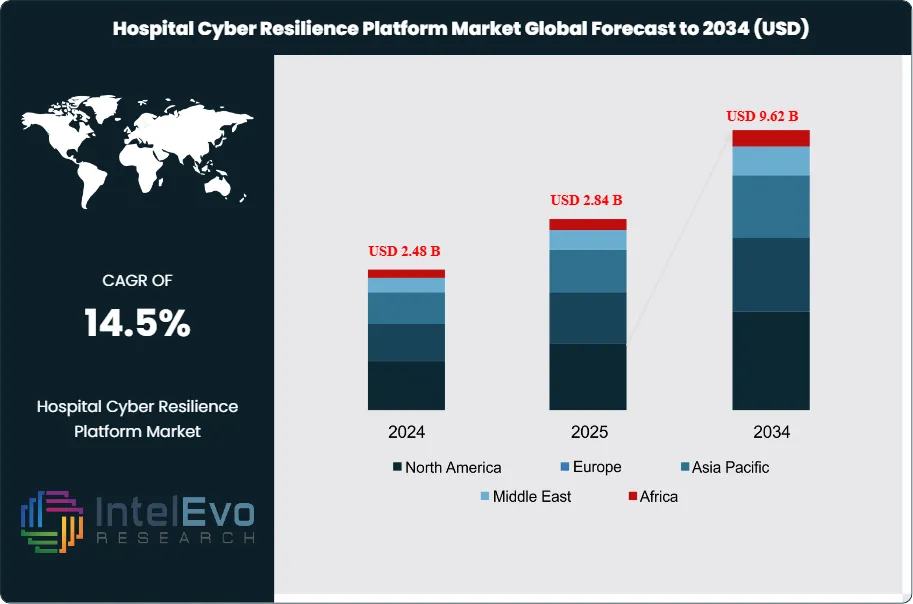

The Hospital Cyber Resilience Platform Market was valued at approximately USD 2.48 Billion in 2024 and reached USD 2.84 Billion in 2025. The market is projected to grow to USD 9.62 Billion by 2034, expanding at a CAGR of 14.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.78 Billion over the analysis period, driven by escalating ransomware attacks on healthcare infrastructure, stringent federal and international regulatory mandates for healthcare cyber security, and the rapid expansion of connected medical devices and Electronic Health Record systems that exponentially enlarge the hospital attack surface.

Get More Information about this report -

Request Free Sample ReportHospital cyber resilience platforms are integrated software suites that combine threat detection, medical device security, zero-trust network access, Security Information and Event Management (SIEM), Security Orchestration Automation and Response (SOAR), incident response playbooks, and cyber risk quantification tools into healthcare-specific deployments. These platforms address the unique security challenges of hospital environments, where clinical operational continuity requirements prevent full system shutdowns during active cyber incidents and where legacy medical devices running outdated firmware cannot accept endpoint security agents without vendor voiding of regulatory clearances. The hospital cyber resilience platform market has moved from niche IT security spending to a board-level capital allocation priority across health systems in North America, Europe, and increasingly Asia Pacific.

Several regulatory and threat environment forces are structurally expanding the hospital cyber resilience platform market. The US Department of Health and Human Services updated the HIPAA Security Rule in 2024 with mandatory cyber security controls including multi-factor authentication, network segmentation requirements for clinical systems, and minimum cyber incident response plan standards for covered entities. The HHS 405(d) Program's Cybersecurity Practices for Healthcare Organizations provides specific technical guidance that health systems are operationalizing through cyber resilience platform deployments. The European Union's NIS2 Directive, effective from October 2024, classifies hospital operators as essential entities subject to strict incident reporting timelines, risk management obligations, and national supervisory authority audit exposure, compelling EU hospital procurement of compliant cyber resilience solutions. CISA's Healthcare and Public Health Sector Cybersecurity Framework continues to set minimum security posture expectations for US hospital networks participating in federal health programs.

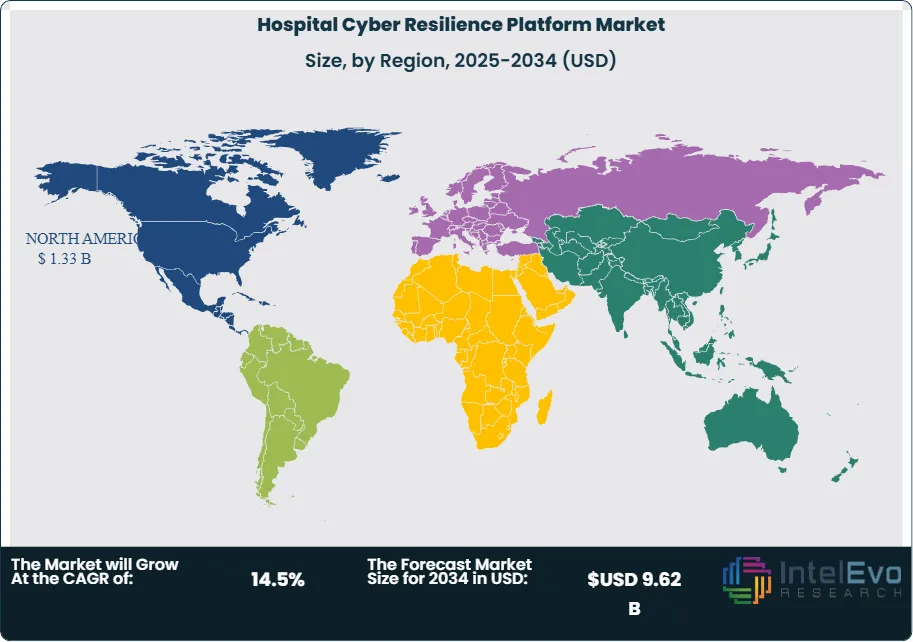

The average cost of a healthcare data breach reached USD 10.9 Million in 2024 per IBM's annual Security Cost Report, the highest of any industry sector for the fourteenth consecutive year, providing the most direct financial quantification of the risk that hospital cyber resilience platforms are designed to mitigate. North America led the hospital cyber resilience platform market with a 46.8% share in 2025, equivalent to USD 1.33 Billion. Europe is the second-largest and fastest-growing major region, advancing at a projected CAGR of 16.2% through 2034, driven by NIS2 Directive compliance demand across EU hospital networks.

, By Deployment Mode (Cloud SaaS, Hybrid, On-Premise), By Hospital Size (Large Systems, Community Hospitals, Critical Access) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Hospital Cyber Resilience Platform Market was valued at USD 2.84 Billion in 2025 and is forecast to reach USD 9.62 Billion by 2034, registering a CAGR of 14.5% during the 2026-2034 forecast period.

- Segment Dominance: By solution type, threat detection and SIEM/SOAR platforms held the largest share at 38.4% of the hospital cyber resilience platform market in 2025, reflecting health systems' prioritization of detection and response capability after high-profile ransomware attacks paralyzed hospital operations at multiple US and European health systems.

- Segment Dominance: By hospital size, large health systems and academic medical centers accounted for 52.6% of hospital cyber resilience platform revenues in 2025, driven by their extensive network complexity, high data breach liability exposure, and greater capital budget availability for enterprise security platform investment.

- Driver: Healthcare ransomware incidents increased by 64% between 2022 and 2025 according to HHS Office for Civil Rights breach reporting data, with average ransom payments in the healthcare sector reaching USD 1.6 Million per incident in 2025, compelling health systems to prioritize cyber resilience platform investment as an operational risk mitigation measure.

- Restraint: Hospital IT security budget constraints, where healthcare organizations allocate an average of only 4-7% of total IT spending to security compared to 10-15% in financial services, limit procurement of comprehensive cyber resilience platforms, with community hospitals and rural health systems most constrained by per-facility security budget availability.

- Opportunity: The Internet of Medical Things (IoMT) security segment, encompassing network-connected clinical devices including infusion pumps, patient monitors, imaging systems, and ventilators, represents the fastest-growing hospital cyber resilience addressable market estimated at USD 2.4 Billion by 2034 as health systems modernize device security postures.

- Trend: AI-powered threat detection using behavioral analytics trained on hospital network traffic patterns grew at approximately 34.6% adoption rate among large US and European health systems in 2025, enabling detection of anomalous lateral movement and data exfiltration with false-positive rates 60% lower than rule-based SIEM approaches.

- Regional Analysis: North America led the hospital cyber resilience platform market with a 46.8% share, equivalent to USD 1.33 Billion in 2025, driven by HIPAA Security Rule enforcement, HHS OCR breach penalty actions exceeding USD 135 Million in cumulative fines in 2024, and the world's largest private hospital sector by revenue.

Competitive Landscape Overview

The hospital cyber resilience platform market is moderately consolidated, with Palo Alto Networks, CrowdStrike, Microsoft, and Claroty collectively accounting for approximately 48% of global revenues in 2025. Competition centers on healthcare-specific threat intelligence depth, IoMT device visibility breadth, regulatory compliance automation capability, and clinical-workflow-aware incident response design. M&A activity has been intense, with Claroty's acquisition of Medigate creating the most specialized clinical device security platform and repositioning the combined company against both pure-play OT security vendors and general enterprise security platforms. New entrants from healthcare-specific cybersecurity specialists including Censinet and Cylera are gaining share in the medical device risk management segment that traditional enterprise security vendors underserved.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Palo Alto Networks | USA | Leader | Cortex XSIAM for Healthcare | North America & Global | Launched healthcare-specific XSIAM threat detection playbooks; Q1 2025. |

| CrowdStrike | USA | Leader | Falcon Complete for Healthcare | North America & Europe | Expanded Falcon Complete MDR coverage for hospital OT/IoMT environments; March 2025. |

| Microsoft (Azure Security) | USA | Leader | Microsoft Sentinel + Defender for Healthcare | Global | Launched pre-built HIPAA/HITECH compliance workbooks for hospital SIEM; Q2 2025. |

| Claroty | USA | Leader | Medigate Healthcare IoT Security Platform | North America & Europe | Acquired Medigate; rebranded as Claroty Healthcare; expanded into clinical OT security; 2025. |

| Cylera (Nuvolo) | USA | Challenger | Cylera AI-Powered Medical Device Security | North America | Signed enterprise contracts with five US health systems for medical device cyber resilience; Q3 2025. |

| Armis Security | USA | Challenger | Armis Centrix for Healthcare | North America & Europe | Expanded Centrix to cover EHR-connected device attack surface in 200+ hospitals; 2025. |

| Fortinet | USA | Challenger | FortiGate Healthcare Network Security | North America & Asia Pacific | Launched FortiGate hospital OT/IT convergence security bundle; Q1 2025. |

| Zscaler | USA | Niche Player | Zscaler Zero Trust Exchange for Healthcare | North America | Signed zero-trust network access deals with 12 US hospital networks for clinical staff access; 2025. |

| Censinet | USA | Niche Player | RiskOps Healthcare Vendor Risk Platform | North America | Expanded RiskOps to include supply chain cyber risk management for hospital procurement; Q3 2025. |

| Check Point Software | Israel | Niche Player | Infinity Architecture for Healthcare | Europe & North America | Launched Infinity for Clinical Networks targeting European hospital NIS2 compliance; Jan 2026. |

By Solution Type

The hospital cyber resilience platform market by solution type spans threat detection and SIEM/SOAR, IoMT and medical device security, zero-trust network access, identity and access management, backup and recovery, and risk assessment and compliance management. Threat detection and SIEM/SOAR held the dominant solution share at 38.4% of the hospital cyber resilience platform market in 2025, equivalent to approximately USD 1.09 Billion. Health systems have prioritized detection and response capability as their primary cyber resilience investment, recognizing that the extended dwell time of advanced threats in hospital networks, averaging 197 days for healthcare breaches versus 128 days across other sectors, makes threat detection speed a critical determinant of breach financial impact. Healthcare-specific SIEM deployments integrate clinical system log sources including Epic EHR audit logs, medical imaging PACS systems, clinical workstation authentication events, and building management system network traffic into unified threat analysis platforms with pre-built healthcare-specific detection rules.

IoMT and medical device security represented 24.6% of the hospital cyber resilience platform market in 2025 and is the fastest-growing solution segment at an estimated CAGR of 19.4% through 2034. The hospital IoMT attack surface is extraordinary in scale: a typical 500-bed hospital operates between 10,000 and 15,000 connected clinical devices, the majority of which run legacy operating systems including Windows XP and Windows 7 that cannot receive security patches without disrupting FDA device clearance status. Platforms from Claroty, Cylera, and Armis provide passive network discovery and risk classification of clinical devices without installing agents, enabling security teams to visualize and prioritize device vulnerability remediation without clinical operational disruption. Zero-trust network access held 16.8% of the market in 2025. Identity and access management (IAM) for clinical workflows accounted for 12.4%. Backup, recovery, and ransomware resilience solutions held 5.2%, and risk assessment and compliance management platforms represented the remaining 2.6%.

By Deployment Mode

The hospital cyber resilience platform market by deployment mode spans cloud-hosted SaaS, on-premise deployment, and hybrid deployment. Cloud-hosted SaaS deployment held the largest share at 48.6% of the hospital cyber resilience platform market in 2025, reflecting the healthcare sector's accelerating cloud adoption trend that migrated approximately 38% of hospital IT workloads to public cloud platforms by 2025. Cloud-hosted cyber resilience platforms provide health systems with continuous threat intelligence updates without on-premise infrastructure management, 24/7 Security Operations Center (SOC) access through managed detection and response services, and consumption-based pricing that converts large capital expenditure to predictable operational expenditure. Microsoft Sentinel, Palo Alto Networks Cortex XSIAM, and CrowdStrike Falcon Complete all deliver cloud-native SIEM and MDR capabilities to health systems that have migrated clinical workloads to Azure, AWS, or Google Cloud environments.

Hybrid deployment, which combines on-premise clinical network sensors with cloud-hosted analytics, SIEM, and SOC management, accounted for 34.8% of the hospital cyber resilience platform market in 2025 and is the preferred deployment architecture for large health systems with significant legacy on-premise clinical infrastructure including EMR servers, PACS storage, and clinical workstation fleets that cannot be immediately migrated to cloud. On-premise deployment held the remaining 16.6% of the market in 2025, concentrated among health systems with strict data sovereignty requirements for patient data, systems serving classified or military healthcare populations, and hospitals in regions with limited cloud connectivity infrastructure. On-premise share is declining progressively as cloud platform security certifications including FedRAMP authorization for government-adjacent healthcare operators resolve data residency concerns.

By Hospital Size

The hospital cyber resilience platform market by hospital size covers large health systems and academic medical centers, mid-size community hospitals, and small and critical access hospitals. Large health systems and academic medical centers held the dominant size segment share at 52.6% of the hospital cyber resilience platform market in 2025, equivalent to approximately USD 1.49 Billion. This segment encompasses multi-hospital health networks, university-affiliated hospitals, and tertiary care centers with complex network environments spanning multiple campuses, research facilities, and ambulatory care locations connected through enterprise networks. These organizations face the highest breach liability given the volume and sensitivity of patient data they manage, employ dedicated Chief Information Security Officers with board-level reporting relationships, and allocate enterprise-scale security budgets that can support comprehensive cyber resilience platform deployments. Academic medical centers also manage research data networks governed by NIH data security requirements under the NIH Data Management and Sharing Policy, adding regulatory complexity that drives comprehensive platform adoption.

Mid-size community hospitals represented 31.8% of the hospital cyber resilience platform market in 2025. These facilities typically have 200-500 beds, operate with IT staff of 5-20 professionals responsible for both operational technology and security functions, and represent the segment most dependent on managed detection and response service models where the cyber resilience platform vendor provides SOC oversight. Small and critical access hospitals held the remaining 15.6% of the market in 2025. This segment is the most underserved in terms of current cyber resilience platform adoption, as procurement and implementation costs present barriers for facilities with total IT budgets of USD 500,000-2 Million annually. Federal programs including the HHS Rural Health Cybersecurity Program and CISA's healthcare sector support initiatives are specifically designed to improve cyber resilience platform adoption among small and critical access hospitals through subsidized tools, training, and technical assistance.

By End-User Organization Type

The hospital cyber resilience platform market by end-user organization type covers for-profit health systems, non-profit and religious health systems, government and public hospitals, and academic and research medical centers. Non-profit and religious health systems held the largest end-user type share at 38.4% of the hospital cyber resilience platform market in 2025, reflecting the dominance of non-profit hospital ownership in the US healthcare sector where non-profit hospitals account for approximately 60% of total hospital beds. For-profit health systems accounted for 26.8% of the market in 2025, characterized by corporate procurement standardization that drives larger average contract values with enterprise-wide cyber resilience platform deployments. Government and public hospitals represented 22.6% of the market, driven by national health system procurement in Europe, Canada, Australia, and Asia Pacific where government-operated hospital networks face NIS2, NHS Digital Standards, and equivalent national cyber security mandates. Academic and research medical centers held the remaining 12.2% of the hospital cyber resilience platform market by end-user type in 2025.

Regional Analysis

North America

North America hospital cyber resilience platform market held a 46.8% share in 2025, generating approximately USD 1.33 Billion in revenue. The United States is the dominant national market, driven by the world's largest private hospital sector, the most extensive HIPAA Security Rule regulatory enforcement apparatus, and the healthcare sector's position as the most targeted industry for ransomware attacks globally. HHS Office for Civil Rights reported 725 healthcare data breach incidents affecting 500 or more individuals in 2024, each requiring breach notification, regulatory cooperation, and potential civil monetary penalty exposure reaching USD 1.9 Million per violation category per year. These enforcement actions have transformed cyber resilience from an IT discretionary budget item to a C-suite financial risk management priority at US health systems. The CISA Healthcare and Public Health Sector Cybersecurity Framework and HHS 405(d) Cybersecurity Practices guide provide specific security control guidance that US hospitals operationalize through cyber resilience platform procurement. Canada's healthcare sector faces equivalent regulatory pressure through provincial privacy legislation including PHIPA in Ontario and PIPA in British Columbia, combined with Canada's Bill C-26 cyber security legislation that extends critical infrastructure protection requirements to healthcare operators. Mexico is an emerging cyber resilience market as its expanding private hospital sector adopts international security standards under cross-border patient data sharing requirements.

Europe

Europe held approximately 26.4% of the global hospital cyber resilience platform market in 2025, generating approximately USD 750 Million. The NIS2 Directive, effective October 2024, classifies hospital operators as essential entities under the EU critical infrastructure framework, imposing mandatory cybersecurity risk management measures, incident reporting to national competent authorities within 24 hours of significant incidents, and supervision and enforcement by national cybersecurity authorities. This regulatory framework has created the most significant single regulatory-driven procurement event in the European hospital cyber resilience platform market, with hospital procurement committees accelerating vendor evaluation processes to achieve NIS2 compliance ahead of national implementation deadline extensions. Germany is the largest European hospital cyber resilience market, where the Federal Office for Information Security (BSI) provides specific healthcare sector cyber security guidance through its IT-Grundschutz framework and actively audits hospital compliance with NIS2 obligations. The UK's NHS Digital Cyber Security Strategy mandates cyber resilience standards across NHS England-funded providers, with NHS organizations required to achieve Cyber Essentials Plus certification and demonstrate network defense capability to NHS Digital auditors. France, Netherlands, and Sweden each represent significant hospital cyber resilience markets where national healthcare cybersecurity programs are directing hospital investment toward compliant platform adoption.

Asia Pacific

Asia Pacific held approximately 17.8% of the global hospital cyber resilience platform market in 2025, generating approximately USD 505 Million, and represents a rapidly growing region at a projected CAGR of 16.8% through 2034. Australia is the most mature Asia Pacific hospital cyber resilience market, where the Australian Cyber Security Centre's Essential Eight framework and the Australian Prudential Regulation Authority's healthcare sector guidelines provide specific security control requirements that hospitals are implementing through cyber resilience platform deployments. Australia's My Health Record system, the national electronic health record infrastructure, has required participating health providers to implement specific network security and access control measures that drive cyber resilience platform adoption among Australian hospital networks. Japan's hospital sector is experiencing growing cyber attack frequency, with the Osaka General Medical Center ransomware incident in 2022 prompting the Ministry of Health, Labour and Welfare to issue specific healthcare cybersecurity guidelines and increase government-funded cyber security support programs for hospital networks. South Korea's healthcare cyber resilience market is growing rapidly as its Ministry of Science and ICT extends National Cybersecurity Framework requirements to healthcare entities. India represents the fastest-growing individual Asia Pacific hospital cyber resilience market, driven by its expanding private hospital sector and increasing digital health infrastructure adoption under the Ayushman Bharat Digital Mission.

Latin America

Latin America held approximately 5.8% of the global hospital cyber resilience platform market in 2025, generating approximately USD 165 Million. Brazil is the dominant regional market, where the LGPD (Lei Geral de Proteção de Dados) health data protection requirements and increasing healthcare ransomware attack frequency are driving private hospital chain procurement of cyber resilience platforms. Brazil's private hospital sector, led by large national chains operating multi-site networks, has begun enterprise-scale cyber resilience platform procurement modeled on US health system approaches, with cloud-hosted SIEM and MDR service models particularly well-suited to the distributed network architectures of multi-hospital chains. Mexico is the second-largest Latin American hospital cyber resilience market, where IMSS (Instituto Mexicano del Seguro Social) and ISSSTE government hospital networks are investing in national-scale cyber resilience infrastructure following documented attack incidents. Colombia and Argentina represent secondary markets where private hospital growth and regional cybersecurity regulation development are driving early-stage cyber resilience platform adoption. The region's overall market growth is constrained by lower average hospital IT budgets, limited local cybersecurity talent for implementation and management, and fragmented regulatory frameworks that provide less uniform procurement pressure than US or EU equivalent mandates.

Middle East & Africa

The Middle East and Africa region held approximately 3.2% of the global hospital cyber resilience platform market in 2025, generating approximately USD 91 Million. Saudi Arabia is the most active regional market, where Vision 2030 healthcare digitalization programs have significantly expanded hospital digital infrastructure and consequently increased cyber attack surface. The Saudi National Cybersecurity Authority's Essential Cybersecurity Controls mandate applies to healthcare entities operating in Saudi Arabia, driving hospital procurement of cyber resilience platforms that demonstrate conformity with NCA control requirements. The UAE's Healthcare Cybersecurity Framework, administered through the Dubai Health Authority and Department of Health Abu Dhabi, establishes mandatory security standards for licensed healthcare providers, with regular compliance assessments that incentivize platform adoption. South Africa is the leading African hospital cyber resilience market, where the Protection of Personal Information Act (POPIA) healthcare data provisions and increasing ransomware attack frequency targeting South African hospital groups are driving private hospital cyber resilience investment. Israel contributes disproportionately to the regional market through its world-class cybersecurity technology sector, with several hospital-focused cyber security companies developing platform technologies that serve both domestic Israeli hospital clients and international export markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Solution Type

- Threat Detection & SIEM/SOAR

- IoMT & Medical Device Security

- Zero-Trust Network Access

- Identity & Access Management

- Backup, Recovery & Ransomware Resilience

- Risk Assessment & Compliance Management

By Deployment Mode

- Cloud-Hosted SaaS

- Hybrid Deployment

- On-Premise Deployment

By Hospital Size

- Large Health Systems & Academic Medical Centers

- Mid-Size Community Hospitals

- Small & Critical Access Hospitals

By End-User Organization Type

- Non-Profit & Religious Health Systems

- For-Profit Health Systems

- Government & Public Hospitals

- Academic & Research Medical Centers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.84 B |

| Forecast Revenue (2034) | USD 9.62 B |

| CAGR (2025-2034) | 14.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Solution Type, Threat Detection & SIEM/SOAR, IoMT & Medical Device Security, Zero-Trust Network Access, Identity & Access Management, Backup, Recovery & Ransomware Resilience, Risk Assessment & Compliance Management, By Deployment Mode, Cloud-Hosted SaaS, Hybrid Deployment, On-Premise Deployment, By Hospital Size, Large Health Systems & Academic Medical Centers, Mid-Size Community Hospitals, Small & Critical Access Hospitals, By End-User Organization Type, Non-Profit & Religious Health Systems, For-Profit Health Systems, Government & Public Hospitals, Academic & Research Medical Centers |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PALO ALTO NETWORKS, CROWDSTRIKE, MICROSOFT (AZURE SECURITY), CLAROTY (MEDIGATE), CYLERA (NUVOLO), ARMIS SECURITY, FORTINET, ZSCALER, CENSINET, CHECK POINT SOFTWARE, SENTINELONE, MEDIGATE (INTEGRATED INTO CLAROTY), OLVID (HEALTHCARE COMMS SECURITY), IMPRIVATA (THYCOTIC), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud SaaS, Hybrid, On-Premise), By Hospital Size (Large Systems, Community Hospitals, Critical Access) Industry Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud SaaS, Hybrid, On-Premise), By Hospital Size (Large Systems, Community Hospitals, Critical Access) Industry Trends & Forecast 2026–2034")

, By Deployment Mode (Cloud SaaS, Hybrid, On-Premise), By Hospital Size (Large Systems, Community Hospitals, Critical Access) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Hospital Cyber Resilience Platform Market?

Global Hospital cyber resilience market valued at USD 2.48B in 2024, reaching USD 9.62B by 2034, growing at a CAGR of 14.5% from 2026–2034.

Who are the major players in the Hospital Cyber Resilience Platform Market?

PALO ALTO NETWORKS, CROWDSTRIKE, MICROSOFT (AZURE SECURITY), CLAROTY (MEDIGATE), CYLERA (NUVOLO), ARMIS SECURITY, FORTINET, ZSCALER, CENSINET, CHECK POINT SOFTWARE, SENTINELONE, MEDIGATE (INTEGRATED INTO CLAROTY), OLVID (HEALTHCARE COMMS SECURITY), IMPRIVATA (THYCOTIC), OTHERS

Which segments covered the Hospital Cyber Resilience Platform Market?

By Solution Type, Threat Detection & SIEM/SOAR, IoMT & Medical Device Security, Zero-Trust Network Access, Identity & Access Management, Backup, Recovery & Ransomware Resilience, Risk Assessment & Compliance Management, By Deployment Mode, Cloud-Hosted SaaS, Hybrid Deployment, On-Premise Deployment, By Hospital Size, Large Health Systems & Academic Medical Centers, Mid-Size Community Hospitals, Small & Critical Access Hospitals, By End-User Organization Type, Non-Profit & Religious Health Systems, For-Profit Health Systems, Government & Public Hospitals, Academic & Research Medical Centers

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Hospital Cyber Resilience Platform Market

Published Date : 23 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date