- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Hot Tub Market Size, Trends, Growth & Forecast 2034 | 6.2% CAG

Global Hot Tub Market Size, Share & Analysis By Type (Portable Hot Tubs, Fixed Hot Tubs), By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) Industry Regions & Key Players – Market Structure, Consumer Trends, Pricing Analysis, Competitive Strategies & Forecast 2025–2034

Report Overview

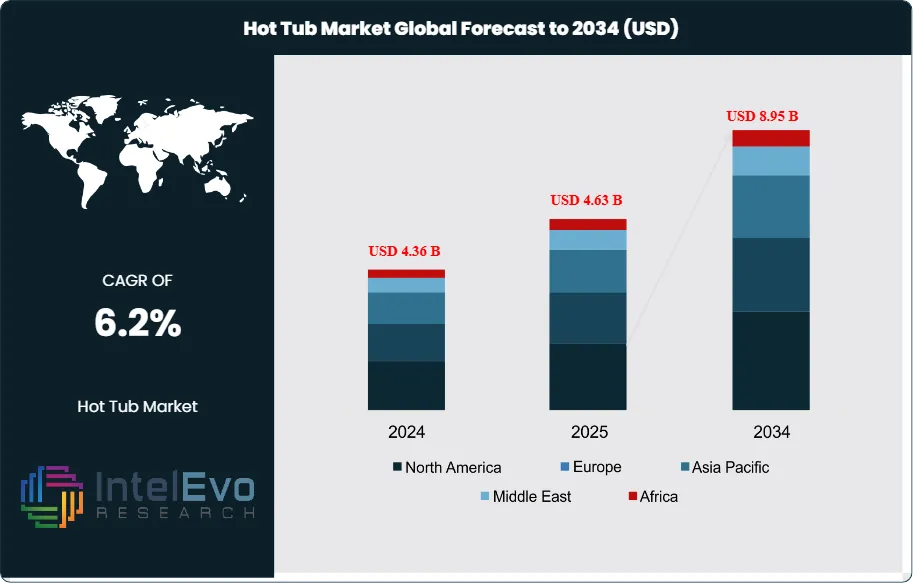

The Hot Tub Market was valued at approximately USD 4.36 Billion in 2024 and is expected to reach nearly USD 8.95 Billion by 2034, expanding at an estimated CAGR of around 6.2% during 2025–2034. Growing consumer focus on home wellness, hydrotherapy benefits, and premium outdoor living experiences is driving strong global demand. With smart features, energy-efficient designs, and rising residential installations, hot tubs are rapidly evolving into essential wellness assets. The market outlook remains highly positive as lifestyle upgrades and health-driven purchasing continue to surge.

Get More Information about this report -

Request Free Sample ReportSlowly evolving from a niche vacation home investment to a home-wellness mainstay, marketplace size expansion is based upon steady residential demand and growing commercial presence across hotels, resorts, and wellness centers. The pandemic-fueled life trends towards at-home rest and renewal continue to support penetration with the installed base already huge: 5.8–7.3 million units are predicted to number alone in the United States, and average unit lifespan is about 7.5 years, supporting a long-term replacement cycle and a healthy secondhand market with some 40% being resold/gifted.

Demand is spurred by hydrotherapy's perceived health benefit—stressed and muscle relief and circulation boost—and by sleep promotion, a prominent need since 132 million Americans experience weekly sleep disorders; a 15-minute soak 90 minutes before bedtime can help bring deeper sleep. Cost facilitates adoption: typical U.S. installations cost near USD 318 (standard range USD 157–490 based on difficulty at site), and periodic operating costs of some USD 10–20 per month keep ownership affordable. Supply-side issues persist, however. U.S. manufacture decreased at an average 0.6% annually during 2017–2022 amidst price pressure, supply-chain disruption, and offshoring competition and by regulation of safety/energy, water-constraint sites during dry spells, and volatility of inputs (e.g., pumps, acrylic).

Technology is redefining value propositions. IoT-enabled "smart" tubs include remote temperature and filter control, usage tracking, and predictive maintenance; advanced insulation, variable-speed pumps, and interconnections with heat pumps minimize energy usage; and advanced sanitation (UV/ozone) reduces chemical consumption. Premiumization is enhanced by customizable jets, LED ambiance and onboard sound, with AI-enhanced diagnostics minimizing downtime and service cost.

Regionally, North America leads with installed base and retail infrastructure—some 4,500 U.S.-based retailers host 360,700 spa-industry workers, with four key hot-tub vendors generating 58% revenue and typical outlet generating ~USD 500,000 per year—indicating a consolidated but scaleable channel. Europe is still large and is accelerating upgrade retrofits based on efficiency-driven initiatives, and Asia Pacific is fastest-growing opportunity as middle-class demand shifts to transportable and mid-premium units. Infrastructure hotspots are smart, energy-efficient platforms, aftermarket chemicals and services, and hospitality/wellness initiatives, and adherence to safety guidelines (e.g., 104°F max; ~100°F kids) and sustainability attributes will create differentiation to winners.

, By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) Industry Regions & Key Players – Market Structure, Consumer Trends, Pricing Analysis, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The hot tub industry is set to grow to USD 4.36 Billion in 2024 to USD 8.95 Billion by 2034 (CAGR 6.2%, 2025–2034), driven by home adoption for health and wellness reasons, a huge base for installations (≈5.8–7.3 million units across the United States), and durable replacements/upgrade cycles (≈7.5-year average tenure)

- Product Type: Portable hot tubs lead with ~57% share through lower capex and fast installation; average cost of U.S. install is ~USD 318 (range USD 157–490) with ongoing use being ~USD 10–20/month and further reinforcing affordability.

- End Use: Residential accounts for ~74% demand because homeowners want hydrotherapy to assist with stress, to relax muscles and to sleep—as relevant because 132 million Americans suffer weekly sleep interruptions; 15 minutes soak 90 minutes prior to bedtime makes sleep deeper.

- Distribution Channel: Offline retailing captures ~65% share through experience-based buying and services support through ~4,500 U.S.-based specialties stores and average sales through outlets nearing USD 500,000 reinforcing local demo, install, and after-sales amenities.

- Driver: Health-and-wellness monetization is accelerating: post-pandemic home-spa investments, hospitality upgrades, and increasing aftermarket services (chemicals, filters, maintenance) all boost utilization and lifetime value per unit.

- Restraint: Supply-side pressure persists with U.S.-made hot-tub manufacture decreasing at roughly 0.6% annually (2017–2022), and volatility of input prices (pumps and acrylics) and water/energy regulations keeps margins back and prolongs lead times for water-/energy-constricted

- Opportunity: Smart/energy-efficient products (Internet of Things controls, variable-speed pumps, add-on heat pumps, UV/ozone sanitations) and aftermarket subscription services can expand beyond base business; incremental global revenue of ~USD 2.2 billion to 2033 suggests opportunity for premium products and subscription revenue services.

- Trend: Scaling through digitization—remote tracking and monitoring, usage-based analysis, and AI-enhanced diagnostics reduce maintenance cost and downtime—while premiumization (LED ambiance, customizable jets, integrated sound) boosts ASPs disproportionately to opex increases.

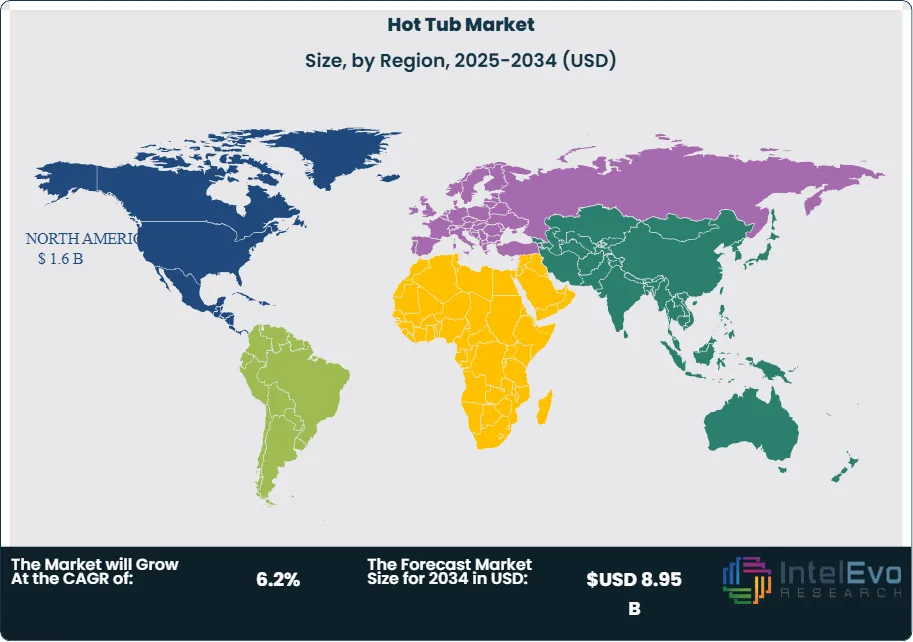

- Regional Analysis: North America leads at ~38% share by virtue of high disposable incomes and an efficient retail/service network; Europe remains relevant with efficiency-driven retro fit demand, and Asia Pacific is the fastest-growing opportunity as middle-class end-users increasingly adopt portable and mid-premium models and is projected to outgrow global CAGR.

Type Analysis

Portable hot tubs remain the volume anchor of the category, accounting for an estimated ~57% of global sales in the 2024 baseline and sustaining leadership into 2025 as households prioritize fast installation, lower upfront cost, and the flexibility to relocate units. Continued innovation in inflatable and lightweight shell designs, better insulation, and variable-speed pumps has improved total cost of ownership—typical U.S. installation averages around USD 318, with ongoing energy/maintenance outlays commonly in the USD 10–20 per month range—supporting first-time adoption and upgrades alike. As manufacturers bundle app-based controls and remote diagnostics into sub-premium price tiers, portable systems are expected to defend a >55% share through the medium term.

Fixed hot tubs (≈43% in 2024) address a different buyer profile: owners investing in durable outdoor living spaces, hospitality venues, and wellness rooms seeking higher jet density, bespoke seating, and integrated lighting/audio. Although higher installation complexity and site prep extend project timelines, fixed units can enhance property value and command higher average selling prices (ASPs). Into 2025–2030, premiumization—multi-zone hydrotherapy, heat-pump add-ons, UV/ozone sanitation—should lift mix and margins, even as portables continue to dominate unit volumes.

End-User Analysis

Residential demand anchors market scale, representing roughly 74% of purchases in 2024 and remaining the primary growth engine in 2025 amid sustained home-wellness spending, renovation activity, and work-from-home lifestyles. Health outcomes drive intent: hydrotherapy for stress relief and recovery, alongside sleep benefits (e.g., short warm-water sessions before bedtime) underpin frequent use and a resilient replacement cycle of ~7–8 years. Broad price ladders—from entry inflatables to feature-rich premium models—have widened household addressability across regions.

Commercial deployments—approximately 26% of the market—span hotels, resorts, fitness/wellness centers, and short-term rental properties, where hot tubs elevate guest experience and RevPAR. Purchasing cycles are longer and compliance stricter (water quality, temperature limits, safety), but specification levels are higher, supporting ASPs and aftermarket revenue (chemicals, filters, service contracts). With wellness tourism expanding and hospitality capex normalizing post-pandemic, 2025–2028 should see steady commercial retrofit and new-build demand, particularly in resort corridors and alpine/leisure destinations.

Distribution Channel Analysis

Offline retail remains the dominant route to market (~65% share in 2024) and continues to be decisive in 2025 due to experiential selling—on-site wet tests, installation planning, financing, and service onboarding. The channel’s depth, especially in North America (≈4,500 specialty outlets with average store revenue near USD 0.5 million), supports high-touch consultative sales and localized after-sales care that reduce ownership friction and boost attachment rates for accessories and maintenance plans.

Online accounts for ~35% and is the faster-growing complement as consumers comparison-shop across brands, configurations, and delivery options. Enhanced digital journeys—3D/AR visualization, virtual consultations, and transparent installation quoting—are compressing decision cycles and extending reach into underserved ZIP codes. The prevailing outlook is omnichannel: dealers integrate e-commerce front ends and marketplace presence while preserving in-person services (site surveys, delivery/craning, water-care training) that are critical to satisfaction and repeat purchases.

Regional Analysis

North America leads with about 38% share (≈USD 1.6 billion in 2024), supported by a large installed base, high discretionary spending, and mature retail/service infrastructure. The U.S. remains the bellwether for premium features and aftermarket monetization, while Canada benefits from strong cottage/leisure home ownership. Europe is a sizeable, more efficiency-driven market in 2025, with Northern and Western countries emphasizing low-energy operation, smart controls, and stringent safety and environmental standards that favor insulated cabinets and advanced filtration.

Asia Pacific is the fastest-rising opportunity through 2030 as middle-income households in China and Southeast Asia trade up to portable and mid-premium units, and Japan/Australia sustain steady replacement. Vendor partnerships with local installers and hospitality groups are expanding access and service coverage. Latin America and the Middle East & Africa are smaller but expanding, propelled by resort development, luxury residential projects, and urban affluent cohorts in Brazil, Mexico, the UAE, and Saudi Arabia. Across emerging regions, success hinges on climate-appropriate energy solutions, financing options, and dealer networks that can execute complex installations reliably.

Comparative Summary

The three profiled companies occupy distinct strategic positions across the hot tub market's competitive spectrum. Jacuzzi Brands commands the market from its leadership position with unmatched brand equity, a multi-brand portfolio spanning all price tiers, and the financial resources of Investindustrial. Bullfrog Spas competes as an innovator-challenger, using its patented JetPak technology, domestic manufacturing base, and factory-direct retail model to carve out a 20% global share. Nordic Hot Tubs fills a deliberate niche in the value segment, delivering handcrafted therapeutic products at accessible price points to first-time buyers and cost-conscious consumers. As the market navigates energy regulation changes, tariff pressures, and growing demand for smart-connected products, each company's strategic choices in R&D investment, supply chain configuration, and channel development will determine whether they gain or concede ground through the remainder of the decade.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Portable Hot Tubs

- Fixed Hot Tubs

By End-User

- Residential

- Commercial

By Distribution Channel

- Offline

- Online

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 4.36 B |

| Forecast Revenue (2034) | USD 8.95 B |

| CAGR (2024-2034) | 6.2% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Portable Hot Tubs, Fixed Hot Tubs), By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Jacuzzi Brands, Nordic Hot Tubs, Bullfrog Spas, Coast Hot Tubs, PDC Spas, Blue Falls Manufacturing, Caldera Spas, Artesian Spas, Canadian Spa Company, Cal Spas, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) Industry Regions & Key Players – Market Structure, Consumer Trends, Pricing Analysis, Competitive Strategies & Forecast 2025–2034")

, By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) Industry Regions & Key Players – Market Structure, Consumer Trends, Pricing Analysis, Competitive Strategies & Forecast 2025–2034")

, By End-User (Residential, Commercial), By Distribution Channel (Offline, Online) Industry Regions & Key Players – Market Structure, Consumer Trends, Pricing Analysis, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the Hot Tub Market?

The Hot Tub Market will rise from USD 4.36 Bn in 2024 to nearly USD 8.95 Bn by 2034, driven by wellness lifestyles, hydrotherapy demand, and smart energy-efficient designs.

Who are the major players in the Hot Tub Market?

Jacuzzi Brands, Nordic Hot Tubs, Bullfrog Spas, Coast Hot Tubs, PDC Spas, Blue Falls Manufacturing, Caldera Spas, Artesian Spas, Canadian Spa Company, Cal Spas, Other Key Players

Which segments covered the Hot Tub Market?

By Type (Portable Hot Tubs, Fixed Hot Tubs), By End-User (Residential, Commercial), By Distribution Channel (Offline, Online)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date